Quick Navigation

Report Overview

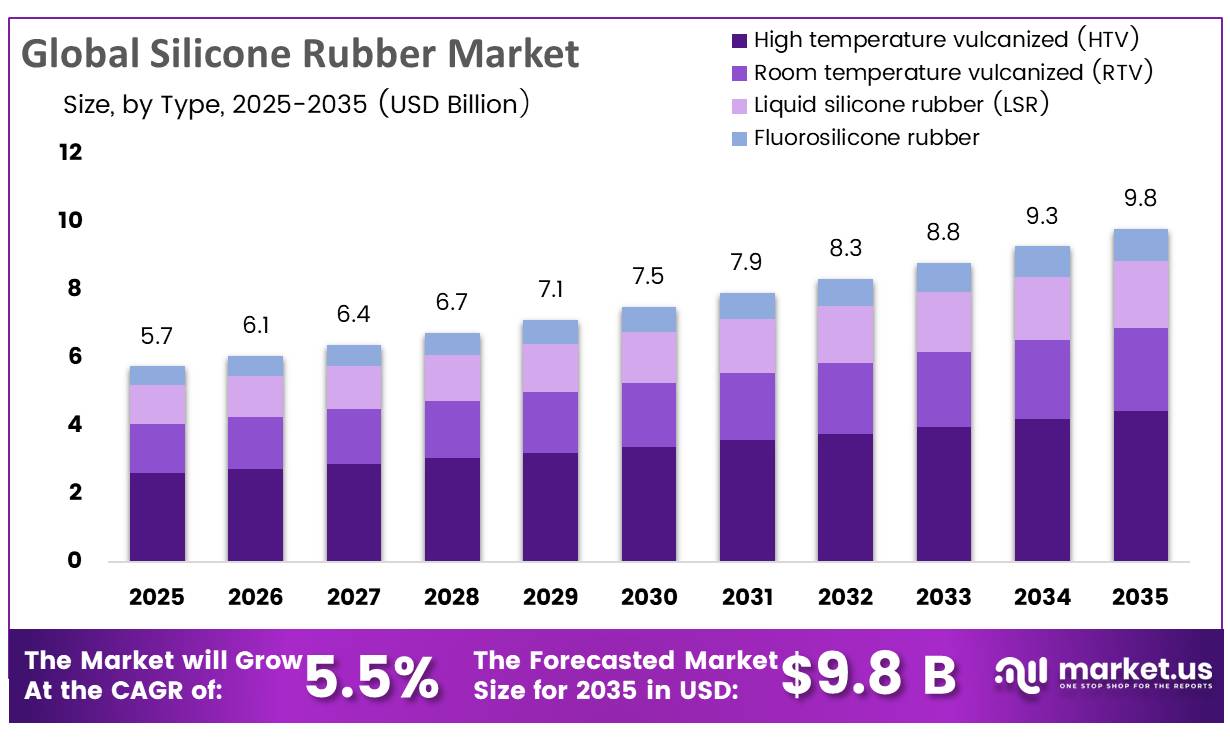

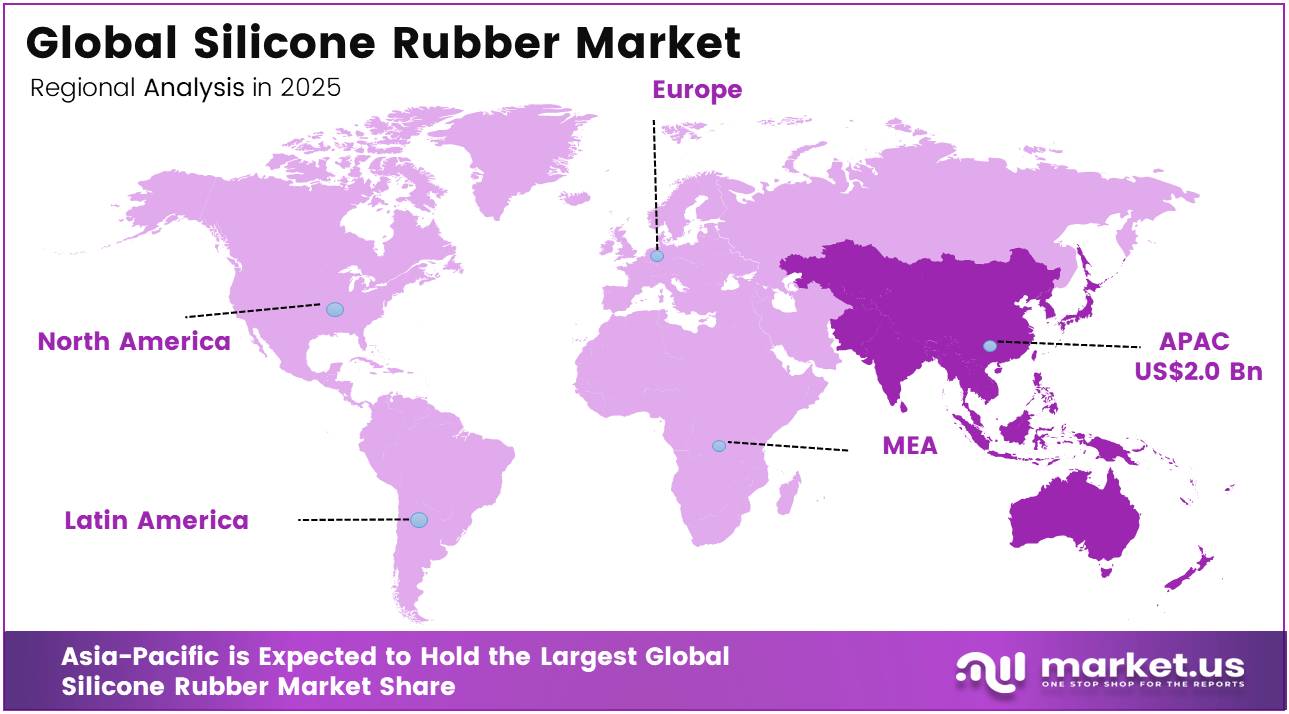

In 2025, the Global Silicone Rubber Market was valued at USD 5.7 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 5.5%, reaching about USD 9.8 billion by 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 35.1% share, holding USD 2.0 billion in revenue.

Silicone rubber, valued for its thermal stability, chemical resistance, and durability, functions as a critical elastomer across the automotive, electronics, healthcare, and construction sectors. Silicon metal, the principal feedstock used in silicone manufacturing, underpins this material’s expanding industrial footprint globally.

- In January 2026, according to the U.S. Geological Survey, 5 domestic facilities produced ferrosilicon and silicon metal in 2025, all located east of the Mississippi River. The same source notes that silicon metal imports in 2025 rose by nearly 50% over 2024 levels, reflecting tariff uncertainty and concerns over future export restrictions.

Key Takeaways

- The global silicone rubber market was valued at USD 5.7 billion in 2025.

- The global silicone rubber market is projected to grow at a CAGR of 5.5% and is estimated to reach USD 9.8 billion by 2035.

- On the basis of type, the high temperature vulcanized (HTV) silicone rubber dominated the market, constituting 45.2% of the total market share.

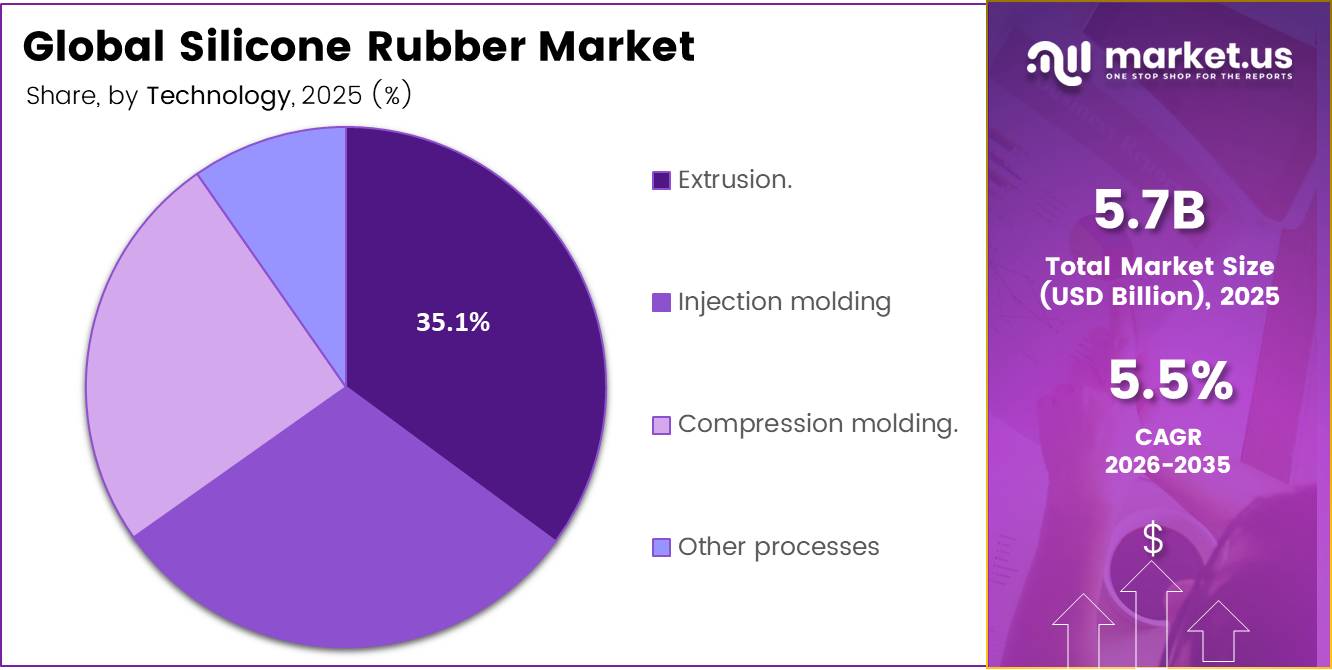

- Based on the technology, the extrusion technology dominated the silicone rubber market, with a substantial market share of around 35.1%.

- Among the end-user industries, the automotive & transportation industry held a major share in the silicone rubber market, accounting for 30.1% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the silicone rubber market, accounting for 35.1% of the total global consumption.

In February 2026, USGS reported that the average U.S. price for 75%-grade ferrosilicon was about 3% more than the 2024 annual average, while silicon metal prices in 2025 declined due to oversupply and weak demand from the aluminum and silicon industries Import data from USGS further shows Brazil supplied 38% and Canada 29% of silicon metal imports between 2021 and 2024, highlighting supply concentration prompting diversification and capacity investment. Sustained government focus on securing feedstock supply chains is expected to support continued growth opportunities for the silicone rubber industry.

In 2026, continued semiconductor and EV electrification expansion is reinforcing this shift, with material suppliers prioritizing high-purity and application-specific silicone formulations rather than general-purpose elastomers, tightening the link between advanced manufacturing and specialty silicone demand.

Type Analysis

High temperature vulcanized (HTV) a significant type.

High Temperature Vulcanized (HTV) Silicone Rubber leads with 45.2% share, structurally dominant due to its high crosslink density, superior thermal oxidative stability, and long-term dielectric endurance under continuous heat cycling. This makes it the important material for EV power electronics insulation, battery pack gaskets, and high-voltage connector housings. In EV architectures emerging in 2025, HTV is increasingly selected for thermal runaway containment barriers, where dimensional stability under rapid thermal shock is critical. Industrial electrification trends and grid-scale battery deployment further reinforce its dominance.

Liquid Silicone Rubber (LSR) is the fastest-growing segment due to hydrosilylation curing chemistry, ultra-low viscosity flow behavior, and micro-molding capability enabling sub-millimeter precision components. Its rapid adoption in medical microfluidics, wearable biosensors, and EV sensor sealing systems is structurally driven by automation-compatible injection molding and zero-post-cure requirements. Fluorosilicone Rubber, though smaller, is strategically critical due to fluorinated side-chain chemistry providing hydrocarbon fuel resistance and extreme chemical inertness, essential in aerospace and defense fuel systems.

Technology Analysis

Extrusion Held a Major Share of the Global Silicone Rubber Market

Extrusion holds the leading position among silicone rubber processing technologies at 35.1%, favored for continuous, high-volume output of seals, tubing, and profiles used in automotive and construction applications. In September 2025, according to the European Parliament, silicon metal has remained on the EU’s Critical Raw Materials list since 2014 owing to its importance to the semiconductor, photovoltaic, and electronic component industries. In March 2024, according to the European Council, the Critical Raw Materials Act set a target of at least 40% EU processing capacity and capped any single non-EU country’s supply share at 65% by 2030.

Injection molding is emerging as the fastest-growing processing technology, valued for precision manufacturing of complex components for electronics and medical devices. In September 2025, according to the European Parliament, silicon metal processing in Europe remains concentrated at industrial sites in Spain, Germany, and France’s Auvergne-Rhône-Alpes region, supporting feedstock availability for this expanding segment.

End Use Analysis

Silicone Rubber Are Mostly Utilized in the Automotive & Transportation Sector.

Automotive & Transportation leads with 30.1% share, driven by silicone’s unmatched role in thermal interface stability, vibration damping under dynamic load cycles, and dielectric insulation in high-voltage EV systems. The EV transition is structurally reshaping demand toward advanced silicone systems for battery thermal runaway barriers, inverter sealing, and powertrain insulation. The next-generation EV platforms in China and Europe are increasingly standardizing silicone-based elastomer systems for safety-critical battery architecture design.

Electrical & Electronics is the fastest-growing segment, structurally driven by semiconductor node shrinking, AI server thermal densification, and 5G/mmWave device proliferation. Silicone rubber is essential for thermal interface management (TIM), chip encapsulation, and PCB protection against moisture ion migration. In 2025, Dow advanced next-generation electronics-grade silicones designed for AI accelerator heat dissipation systems, while Asia-based fabs are scaling demand for ultra-low ionic contamination elastomers.

Key Market Segments

By Type

- High temperature vulcanized (HTV)

- Room temperature vulcanized (RTV)

- Liquid silicone rubber (LSR)

- Fluorosilicone rubber

By Technology

- Extrusion

- Injection molding

- Compression molding

- Other processes

By End Use

- Automotive & transportation

- Building & construction

- Electrical & electronics

- Medical & healthcare

- Industrial and consumer products

Driver Analysis

EV thermal-barrier and high-voltage sealing demand

Electric vehicle architecture is increasing silicone intensity per vehicle because battery packs, busbars, connectors, cable harnesses, thermal-interface zones, and fire-containment elements all require heat resistance, dielectric stability, and compression-set performance that commodity elastomers struggle to match. WACKER has explicitly positioned silicones for battery-pack safety, thermal barriers, thermal management, and power electronics, while its published materials note up to 4x higher silicone content in EVs versus internal-combustion vehicles; that multiplier is the clearest structural reason this driver adds more to silicone rubber growth than headline vehicle production alone would suggest.

On the demand side, the IEA reported that electric car sales exceeded 20 million in 2025 and represented about one-quarter of new-car sales worldwide, with first-quarter 2025 sales up 35% year on year and 2025 full-year growth around 20%, creating a large installed base for silicone gaskets, potting, tubing, and shielding components.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV thermal-barrier and high-voltage sealing demand | +1.6% | North America core, EU, China, South Korea, Japan, India spill-over | Short term (≤ 2 years) |

| Medical-grade silicone shift in tubing, wearables, and devices | +1.1% | North America core, EU, Japan, China urban clusters, India private-care spill-over | Medium term (2-4 years) |

| Power cable, grid insulation, and renewable balance-of-system expansion | +0.9% | China, India, GCC, EU, North America | Medium term (2-4 years) |

| Electronics miniaturization and power-electronics protection | +1.2% | China, Taiwan, South Korea, Japan, EU industrial base, North America | Short term (≤ 2 years) |

| Food-contact and safer-material substitution under tighter chemical rules | +0.7% | EU core, UK alignment spill-over, North America premium applications, APAC export chains | Short term (≤ 2 years) |

| Asian monomer capacity scale-up and regional compounding localization | +0.8% | China core, India, Southeast Asia, export-linked EU and North America | Medium term (2-4 years) |

Restraint Analysis

Logistics and lead-time uncertainty

Residual logistics dislocations from the pandemic era, compounded by episodic container shortages, port congestion, and geopolitical route disruptions, continue to weigh on silicone rubber consumption because many converters and OEMs now operate with longer and more variable lead times, often stretching procurement cycles from 6–8 weeks pre‑2020 to 10–14 weeks for some specialty compound shipments during 2024–2025.

Strategically, these logistics and policy‑induced delays translate into higher safety‑stock requirements, increased working‑capital lock‑up, and greater risk of stock‑outs for small and mid‑size molders, which respond by limiting SKU proliferation and avoiding aggressive silicone substitution programs in favor of materials with more predictable local availability, thereby trimming about one CAGR point off the market’s potential growth via slower rollout of new silicone applications, especially in export‑oriented North American and European manufacturing clusters.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile silicon metal and energy costs | -1.4% | China core, EU, North America, Japan | Short term (≤ 2 years) |

| Logistics and lead-time uncertainty | -1.1% | North America, EU, APAC export corridors | Short term (≤ 2 years) |

| Complex food-contact and medical compliance | -0.9% | EU core, North America, Japan, high-end APAC | Medium term (2-4 years) |

| High CapEx and permitting for new capacity | -1.0% | China, EU, North America, Middle East | Long term (≥ 4 years) |

| Customer qualification inertia in critical uses | -0.8% | Automotive, aerospace, medical hubs globally | Medium term (2-4 years) |

| Margin pressure from rising wages and raw-material costs | -1.2% | Global, with acute impact in EU and North America | Short term (≤ 2 years) |

Opportunity Analysis

Advanced molding, design-for-silicone, and turnkey assemblies

By offering end‑to‑end services—finite‑element analysis of seals and gaskets, topology optimization for silicon parts, over‑molding of inserts, and integrated assembly delivery—silicone specialists can move into higher value‑add positions that may capture 10–20% of the component’s full value instead of the 3–8% typical of raw material share, generating potential margin uplift of 5–10 percentage points and enabling volume growth as OEMs outsource design to specialized partners.

This is white space because many converters in emerging manufacturing corridors still lack advanced CAE tools and materials engineering capabilities, and as smart manufacturing trends in silicone molding gain traction, providers that package material + process + design could tap incremental TAM in complex assemblies in automotive, electronics, and industrial sectors, contributing an estimated 1.2 percentage points of CAGR upside over the baseline through better win rates, cross‑selling, and stickier multi‑year contracts.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Smart and sensor-integrated silicone systems | +1.5% | North America core, EU, China, South Korea, Japan | Medium term (2-4 years) |

| Low-carbon and bio-based silicone rubber portfolio | +1.3% | EU core, UK, North America, Japan, premium APAC | Short term (≤ 2 years) |

| Advanced molding, design-for-silicone, and turnkey assemblies | +1.2% | China, Southeast Asia, India, Eastern Europe, Mexico | Medium term (2-4 years) |

| Conductive and electronic-grade silicone for next-gen electronics | +1.4% | China, Taiwan, South Korea, Japan, US, EU industrial hubs | Medium term (2-4 years) |

| Silicone solutions for aging populations and assistive devices | +1.0% | Japan, EU, North America, China urban regions | Long term (≥ 4 years) |

| Circular and recyclable silicone ecosystems and take-back schemes | +0.9% | EU, North America, developed APAC | Long term (≥ 4 years) |

Challenges Analysis

Complex multi-step processing

High Consistency Rubber and Liquid Silicone Rubber processes must manage mixing ratios, cure kinetics, and mold design with tight tolerances; for example, injection molding of HCR or LSR requires precise dosing, screw homogeneity, and cavity filling, and even a 2–3% deviation in viscosity or cure time can increase scrap rates by 5–10% and extend cycle times from 30–40 seconds to 50–60 seconds per part.

At the plant level, this complexity translates into OEE variability where lines often run at 60–75% of theoretical capacity instead of above 85%, with standard‑deviation in yield and cycle times adding 0.5–1.0 days of extra lead time per batch and raising cost‑per‑unit by several percent, especially in small and mid‑size molders without advanced process‑control or simulation tools.

Strategically, mitigating this challenge requires capital investment in better automation, in‑mold sensors, advanced process simulation, and operator training over a 2–4‑year horizon, along with design‑for‑manufacturing engagement with customers to simplify part geometries; until these measures are broadly rolled out, the complexity continues to impose roughly a 1.1 percentage point friction drag on the market’s maximum CAGR through higher scrap, longer qualification cycles, and slower scale‑up of new silicone‑heavy applications.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Complex multi-step processing | -1.1% | Global manufacturing hubs | Medium term (2-4 years) |

| Supply chain and trade volatility | -1.3% | North America, EU, APAC logistics corridors | Long term (≥ 4 years) |

| Cross-functional collaboration gaps | -0.9% | Global, esp. large enterprises | Medium term (2-4 years) |

| Skilled silicone processing talent shortage | -1.0% | China, Southeast Asia, India, Eastern Europe, Mexico | Long term (≥ 4 years) |

| Digitalization and data integration lag | -0.8% | EU, North America, APAC industrial clusters | Medium term (2-4 years) |

| Supplier risk and compliance burden | -1.0% | EU regulatory hubs, North America, export-focused APAC | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Supply‑Chain Disruption from Conflict‑Related Trade and Transit Risks

Geopolitical tensions and war-related disruptions are increasingly introducing measurable supply-chain risks into the global silicone rubber market, especially across trade routes and sourcing networks exposed to political instability. Shipments of silicone intermediates and finished elastomers passing through key maritime chokepoints have faced higher insurance premiums, rerouting requirements, and delays, with some corridors reporting transit-time extensions of around 10–20% along with additional compliance and documentation burdens.

Trade restrictions and export-control measures between certain countries have also disrupted normal trade flows of silicone-chemistry products. In response, at least one major European silicone rubber producer has reported that approximately 10–15% of its previous export volumes were redirected to alternative markets or held in regional warehouses, leading to higher inventory requirements of several hundred metric tons per quarter.

Conflict-linked energy infrastructure disruptions and transport network instability have also affected production continuity in some regions, occasionally reducing local conversion-capacity utilization by single-digit percentage points for short periods. As a result, downstream industries have increased safety-stock levels of silicone rubber components to maintain supply security. Overall, these geopolitical pressures are increasing operational costs and reinforcing the shift toward more regionalized and resilient supply-chain structures in the silicone rubber market.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Silicone Rubber Market

Asia Pacific remains the leading regional market for silicone rubber, holding a 35.1%, anchored by China’s large-scale manufacturing and electronics production base. In October 2025, according to the World Bank, China’s economy grew by 5.0% in 2025, continuing to reinforce the region’s position as the world’s primary hub for silicone rubber consumption across automotive, electronics, and construction applications .

Middle East & Africa is emerging as the fastest-growing regional market, supported by expanding industrial and infrastructure activity. In November 2025, according to the African Development Bank, Africa’s real GDP growth reached 4.2% in 2025, up from 3.5% in 2024, reflecting improved macroeconomic conditions and rising private investment across the continent

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Silicone rubber manufacturers are prioritising specialty grade expansion, application-specific compound development, and regional capacity investment as the primary mechanisms for maintaining margin differentiation against commodity-grade competition from Chinese producers. A central focus is the development of high-performance silicone rubber formulations targeting electric vehicle thermal management, medical implant, and semiconductor manufacturing applications, where material purity, certifications, and processing consistency create qualification barriers that price-competitive producers cannot easily overcome.

Leading players are simultaneously investing in liquid silicone rubber capacity expansion to serve high-growth injection molding applications in automotive sealing, infant care, and healthcare, where LSR’s biocompatibility and cycle time advantages over high-temperature vulcanised grades are driving accelerated specification uptake. Vertical integration into upstream siloxane and silicon metal supply is becoming a strategic priority as platinum catalyst cost volatility, evidenced by Wacker Chemie’s January 2026 price adjustment of up to 25% on addition-curing silicone rubber grades, compresses margins across the converter tier.

The Major Players In The Industry

- Dow Inc.

- Wacker Chemie AG

- Shin Etsu Chemical Co Ltd

- Elkem ASA Elkem Silicones

- Momentive Performance Materials Inc

- KCC Corporation

- Henkel AG and Co KGaA

- Evonik Industries AG

- CHT Group

- Wynca Group

- Hesheng Silicon Industry Co Ltd

- Zhejiang Xinan Chemical Industrial Group Co Ltd

- Reiss Manufacturing Inc

- Specialty Silicone Products Inc

- Kaneka Corporation

- Other companies

Key Development

- September, 2025, Dow launched DOWSIL EG-4175 Silicone Gel, a protective solution for next-generation insulated gate bipolar transistor modules operating at higher voltages, targeting electric vehicle power electronics and renewable energy technology applications requiring high-reliability silicone encapsulation under demanding thermal and electrical stress conditions.

- January, 2026, Wacker Chemie announced a price increase of up to 25% on selected addition-curing silicone rubber products effective February 1, 2026, driven by a sharp rise in platinum catalyst commodity costs, with customers across the automotive, medical, paper, electrical engineering, and pharmaceutical sectors directly affected by the adjustment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 5.7 Bn |

| Forecast Revenue (2035) | USD 9.8 Bn |

| CAGR (2026-2035) | 5.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (High temperature vulcanized (HTV), Room temperature vulcanized (RTV), Liquid silicone rubber (LSR), and Fluorosilicone rubber), By Technology (Extrusion., Injection molding, Compression molding., and Other processes), By End-user Industry (Automotive & transportation, Building & construction, Electrical & electronics, Medical & healthcare, and Industrial and consumer products) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Dow Inc., Wacker Chemie AG, Shin Etsu Chemical Co Ltd, Elkem ASA Elkem Silicones, Momentive Performance Materials Inc, KCC Corporation, Henkel AG and Co KGaA, Evonik Industries AG, CHT Group, Wynca Group, Hesheng Silicon Industry Co Ltd, Zhejiang Xinan Chemical Industrial Group Co, Reiss Manufacturing Inc, Specialty Silicone Products Inc, Kaneka Corporation, Other companies |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |