Quick Navigation

Report Overview

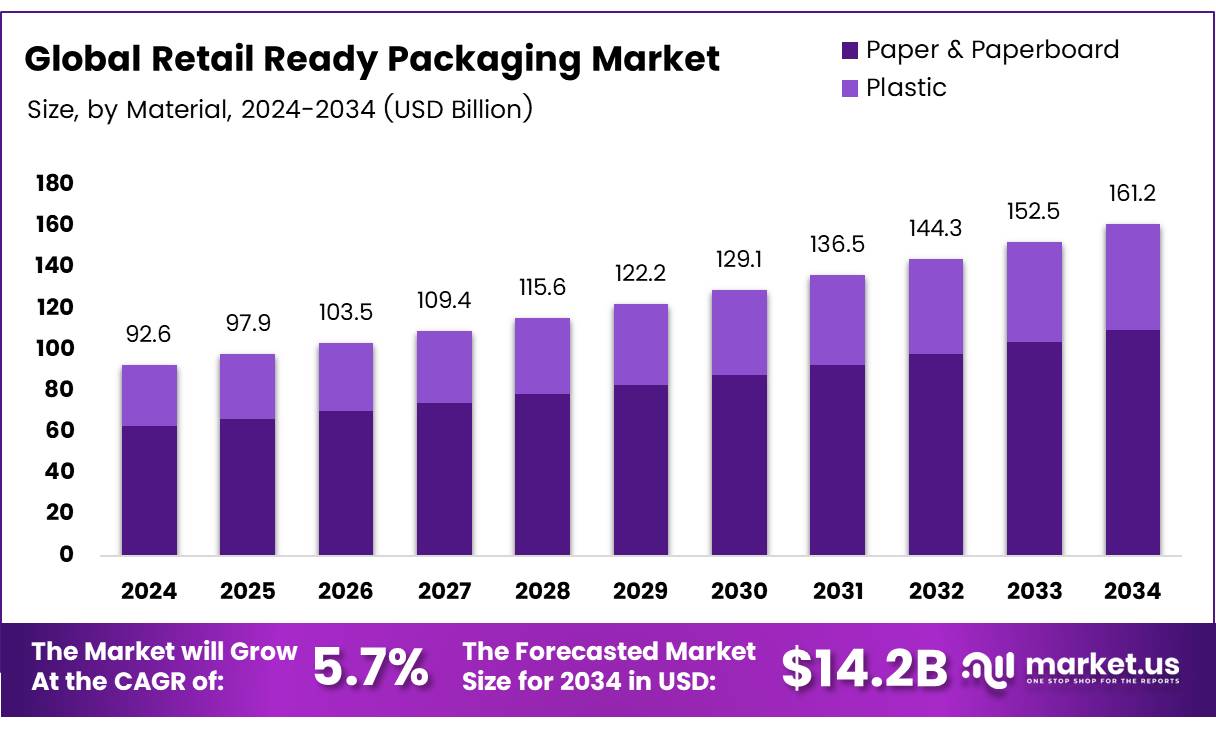

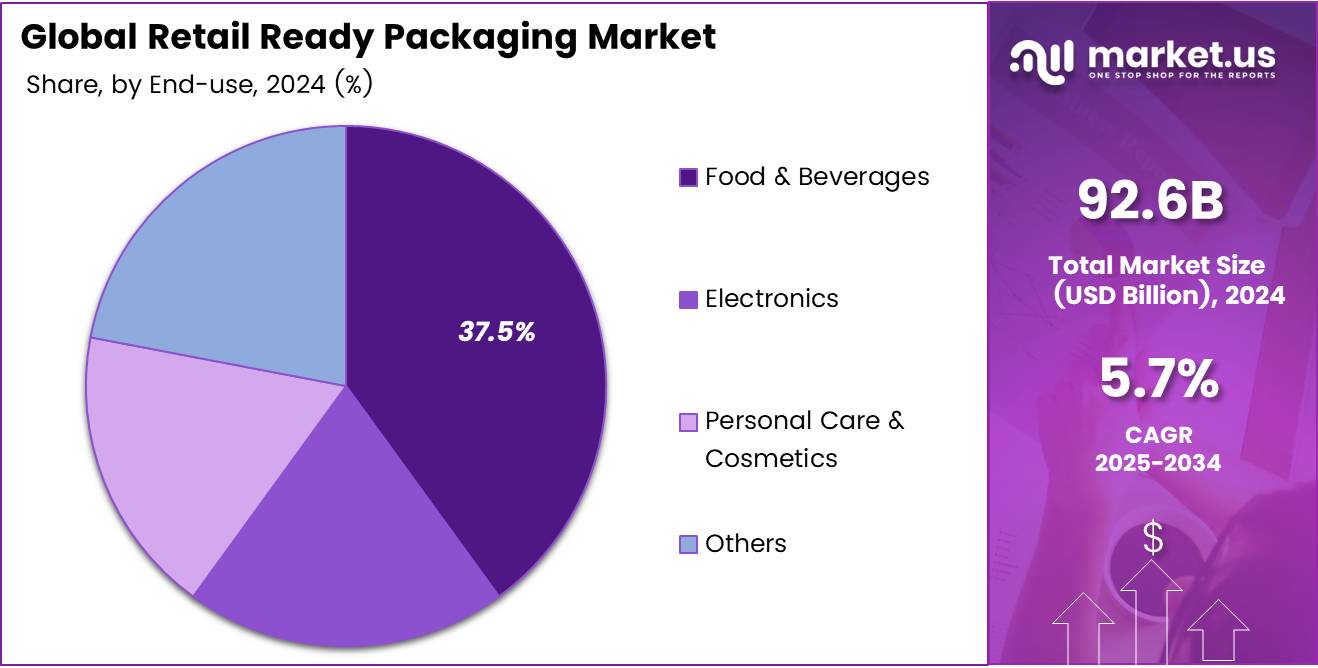

The Global Retail Ready Packaging Market size is expected to be worth around USD 161.2 Billion by 2034, from USD 92.6 Billion in 2024, growing at a CAGR of 5.7% during the forecast period from 2025 to 2034.

Retail Ready Packaging (RRP), also known as shelf-ready packaging, is designed to optimize the retail supply chain by allowing products to be ready for immediate sale or display upon arrival at retail stores.

This type of packaging not only reduces operational costs by minimizing the labor and time required for product handling and shelf stocking but also enhances product visibility and accessibility to boost consumer convenience.

The RRP market has gained significant traction as retailers and manufacturers aim to streamline logistics and enhance the shopping experience. The growth of the Retail Ready Packaging market is primarily driven by the increasing emphasis on reducing labor costs in retail settings and improving the efficiency of supply chains. With more than 70% of purchasing decisions made in-store, according to The Custom Pack, RRP can significantly influence sales by making products easy to locate and visually appealing.

This is critical as packaging that enhances product visibility can increase impulse purchases by up to 30%, suggests research from The Custom Pack. Furthermore, the adoption of sustainable practices in packaging solutions appeals to environmentally conscious consumers, presenting additional growth opportunities for the market.

Government regulations and investments are increasingly focusing on sustainability, which impacts the RRP market. Packaging solutions that reduce waste and are recyclable are being supported through various regulatory guidelines, which encourage manufacturers to adopt eco-friendly materials and designs.

Such regulations not only help in maintaining environmental standards but also resonate well with the consumers’ growing preference for green products. This regulatory environment, therefore, aids in shaping the strategies of companies in the RRP sector to align with governmental standards and consumer expectations.

Consumer behavior has shown a shift towards convenience and sustainability, which are pivotal factors driving the demand for Retail Ready Packaging. According to PakFactory, 52% of consumers have changed brands due to new packaging that better meets their needs in terms of convenience and environmental impact.

This highlights the significant influence of packaging on consumer choices and underscores the importance of innovative packaging solutions in today’s competitive market. The emphasis on visually appealing and easy-to-use packaging formats is likely to continue to dictate market trends and consumer preferences in the foreseeable future.

Key Takeaways

- Global Retail Ready Packaging Market projected to reach USD 161.2 Billion by 2034, growing at a CAGR of 5.7%.

- Paper & Paperboard holds 61.5% market share in 2024 due to sustainability and recycling advantages.

- Die cut display containers lead with 30.5% market share in 2024, favored for their design flexibility and aesthetic appeal.

- Food & Beverages sector dominates end-use segment with 37.5% market share in 2024.

- North America leads the market with a 26.3% share, valued at approximately USD 24 billion.

Material Analysis

Paper & Paperboard Leads with 61.5% in Retail Ready Packaging Materials

In 2024, the Retail Ready Packaging Market saw Paper & Paperboard capturing a commanding 61.5% market share within the By Material Analysis segment. This dominance is attributed to its sustainability features and widespread recycling practices, appealing to environmentally conscious consumers and businesses aiming for greener packaging solutions.

As retailers and manufacturers continue to prioritize sustainable and cost-effective packaging options, Paper & Paperboard has emerged as a preferred choice. Its versatility and adaptability allow for innovative designs that cater to a broad range of products, enhancing shelf presence and consumer convenience.

On the other hand, Plastic, while still a significant player in the market, faces increasing scrutiny due to environmental concerns. The shift towards more sustainable materials like Paper & Paperboard reflects broader industry trends where sustainability is becoming a key factor in material selection.

This transition is supported by advancements in paper technology and increased investment in recycling infrastructure, which bolster the material’s appeal by improving its durability and functionality without compromising environmental values.

Product Analysis

Die Cut Display Containers Lead with 30.5% Market Share in Retail Packaging

In 2024, die cut display containers maintained a dominant position in the By Product Analysis segment of the Retail Ready Packaging Market, securing a 30.5% share. This leadership is attributed to their flexibility in design and superior aesthetics, which enhance shelf presence and consumer appeal.

These containers easily accommodate complex cuts and folds without compromising structural integrity, making them ideal for both protective and promotional packaging solutions.

Following closely are corrugated cardboard boxes, known for their durability and recyclability, addressing the increasing demand for sustainable packaging solutions. Folding cartons also continue to be favored for their cost-effectiveness and ease of assembly, making them a practical choice for a variety of products.

Shrink wrapped trays, while lower in market share, are valued in sectors that prioritize product visibility and tamper evidence, such as food and pharmaceuticals.

The Others category, which includes assorted packaging types like plastic and foam trays, caters to niche market needs that require specific attributes such as lightweight and insulating properties.

End-use Analysis

Retail Ready Packaging Flourishes in Food & Beverages Sector

In 2024, the Retail Ready Packaging Market witnessed significant traction in the Food & Beverages sector, capturing a dominant 37.5% share in the By End-use Analysis segment. This sector’s lead is propelled by the escalating demand for convenient, sustainable packaging solutions that cater to the fast-paced lifestyle of consumers.

Retail ready packaging in this segment not only enhances shelf visibility but also streamlines stocking processes, making it an integral component in modern retail environments.

The Electronics segment, although smaller in comparison, shows promising growth due to the increasing consumer electronics sales and the need for secure packaging solutions that ensure product safety while maintaining consumer appeal.

Personal Care & Cosmetics is another notable segment where retail ready packaging is becoming increasingly prevalent. The emphasis on aesthetic appeal and brand differentiation in store aisles makes effective packaging critical in capturing consumer attention and driving purchase decisions.

Lastly, the ‘Others’ category, which encompasses various industries, continues to adopt retail ready packaging solutions to leverage their benefits of efficiency and enhanced visibility, tailoring them to diverse product needs and consumer expectations.

Key Market Segments

By Material

- Paper & Paperboard

- Plastic

By Product

- Die cut display containers

- Corrugated cardboard boxes

- Folding cartons

- Shrink wrapped trays

- Others

By End-use

- Food & Beverages

- Electronics

- Personal Care & Cosmetics

- Others

Drivers

Consumer Convenience Boosts Retail Ready Packaging Market

The retail ready packaging market is driven by several crucial factors. Consumer demand for convenience significantly propels the market as today’s shoppers prefer products that are easy to access and ready to display, streamlining their shopping experience.

Retail ready packaging also enhances operational efficiency by enabling quicker shelf stocking and reducing labor costs, making it highly attractive for stores aiming to optimize operations.

The push towards sustainability plays a vital role, with a growing demand for eco-friendly packaging solutions that align with broader environmental initiatives. Moreover, the expansion of modern retail formats like supermarkets and hypermarkets necessitates innovative packaging that serves practical purposes and acts as an effective marketing tool, collectively shaping the growth opportunities in this market.

Restraints

High Initial Investment Challenges Retail Ready Packaging Adoption

The adoption of retail ready packaging (RRP) is notably hindered by the considerable initial investment required. This financial barrier primarily affects smaller manufacturers who may find the upfront costs prohibitive.

Retail ready packaging demands a unique blend of aesthetic appeal and functionality to meet the diverse branding requirements of different retailers. Designing such packaging involves not only creative design but also extensive testing to ensure it meets specific retail standards, which can escalate costs further.

Additionally, the complexity involved in developing RRP that aligns seamlessly with retailer demands adds another layer of expense, complicating the design process and potentially lengthening the time to market. This complexity and high cost of entry can deter manufacturers from adopting retail ready packaging solutions, thereby restraining the growth of the market in this segment.

Growth Factors

Technological Advancements Propel Sustainability and Efficiency in Retail Ready Packaging

The retail ready packaging market is poised for significant growth, driven by technological advancements that focus on sustainability and operational efficiency. Innovations in material science and packaging design are enabling the development of more sustainable solutions, which are increasingly demanded by both retailers and consumers who are conscious of environmental impacts.

These advancements not only reduce waste but also improve the logistical efficiency of packaging, making it easier to transport, display, and dispose of products. Additionally, the integration of cutting-edge technologies, such as biodegradable materials and lightweight packaging, offers enhanced protection for products while minimizing environmental footprints. This shift towards innovative and sustainable packaging solutions is expected to open new avenues for growth, particularly as global markets move towards more eco-friendly consumption patterns.

By capitalizing on these technological innovations, companies in the retail ready packaging sector can not only meet the current market demands but also position themselves as leaders in a more sustainable and efficient future.

Emerging Trends

Shift Towards Sustainability Drives Retail Ready Packaging Trends

In the retail packaging sector, a prominent trend is the increasing shift towards sustainability, primarily through the adoption of biodegradable and recycled materials. This move is driven by stringent environmental regulations and a growing consumer preference for eco-friendly products. Manufacturers are innovating with materials that not only meet these standards but also enhance the overall consumer experience.

Such packaging solutions are designed to be easy to open, dispose of, or reuse, aligning with consumer demands for convenience and sustainability. Additionally, as retail automation becomes more prevalent, there is a heightened demand for packaging that seamlessly integrates with automated stocking and scanning systems. This includes designs that are both functional and automation-friendly, facilitating smoother operations in retail settings.

Regional Analysis

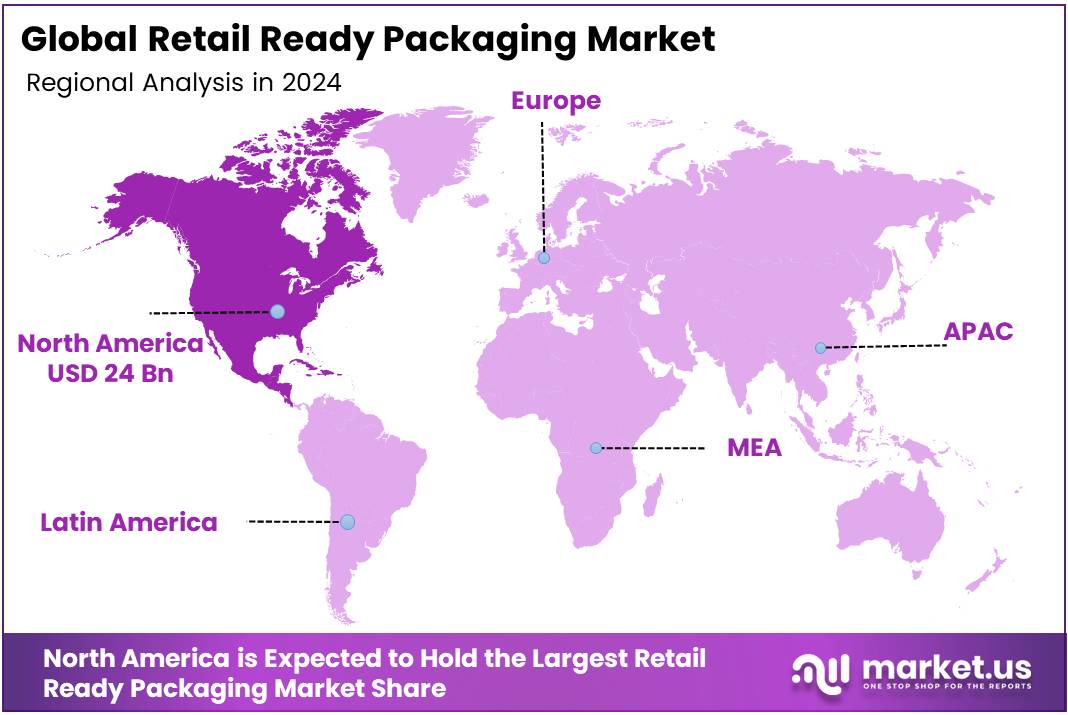

North America Leads Retail Ready Packaging Market with 26.3% Share, Valued at USD 24 Billion

North America emerges as a dominating region in the Retail Ready Packaging market, commanding a substantial market share of 26.3% with a market value of approximately USD 24 billion.

This dominance can be attributed to the region’s robust retail infrastructure and a high degree of manufacturer-retailer collaboration aimed at reducing stocking time and enhancing shelf visibility. The U.S. leads this region, driven by stringent efficiency requirements in retail operations and a strong push towards sustainable packaging solutions.

Regional Mentions:

Europe follows closely, characterized by advanced packaging innovations and strict regulations regarding packaging waste. Retailers in European countries, particularly in the UK, Germany, and France, are increasingly adopting RRP solutions to meet consumer demand for convenience and sustainability. The European market is further propelled by the growing emphasis on reducing logistics costs, enhancing product security, and improving the speed of product placements on shelves.

Asia Pacific is identified as the fastest-growing region in the RRP market, thanks to rising urbanization, increasing disposable incomes, and the expansion of organized retail sectors in countries like China, India, and Japan. The region’s growth is fueled by the burgeoning consumer goods sector and a shift towards modern retailing, which demands more sophisticated packaging solutions.

Middle East & Africa and Latin America are also showing promising growth. These regions benefit from rapid urban development and an increasing number of hypermarkets and supermarkets. The adoption of RRP in these regions is driven by the need for cost-effective and efficient packaging solutions that cater to the growing retail and consumer markets.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the burgeoning global Retail Ready Packaging (RRP) market of 2024, several key players are poised to redefine packaging norms and standards, driven by escalating demand from major retailers and consumer goods manufacturers. Among them, notable companies such as Smurfit Kappa, International Paper, DS Smith, and Mondi continue to dominate due to their comprehensive capabilities in innovation and sustainability.

Smurfit Kappa, with its vast global presence, is at the forefront, leveraging its experience to innovate with both structural and graphic design enhancements that optimize retail efficiency and shelf appeal. The company’s commitment to sustainability aligns with the growing consumer demand for environmentally friendly packaging solutions, making it a leader in the development of eco-conscious RRP solutions.

International Paper, renowned for its extensive range of packaging solutions, excels in the customization of RRP, catering to specific retailer needs. Their focus on integrating technology for improved logistics and inventory management allows retailers to enhance in-store efficiency and reduce operational costs.

DS Smith stands out with its focus on high-quality, sustainable materials and creative design. Their approach to RRP caters to the rapid changes in consumer preferences and the dynamic retail environment, which demands versatility and adaptability in packaging solutions.

Mondi’s strategy revolves around material innovation and process optimization. Their emphasis on creating lightweight yet durable packaging solutions not only appeals to retailers looking to reduce shipping costs but also aligns with global sustainability trends.

These companies, with their robust strategies and innovations in RRP, are not just shaping industry standards but are also significantly influencing retail operations and consumer experiences worldwide. Their ability to adapt and innovate ensures they remain at the forefront of the Retail Ready Packaging market.

Top Key Players in the Market

- Bennett

- The Cardboard Box Company

- Smurfit Kappa

- Weedon Group Ltd

- BoxesIndia

- International Paper

- DS Smith

- Vanguard Packaging, LLC

- WestRock Company

- STI – Gustav Stabernack GmbH

- Mondi

- Green Bay Packaging Inc.

- Graphic Packaging International, LLC

Recent Developments

- In June 2024, RetailReady successfully secured $3.3 million in seed funding aimed at enhancing its capabilities to reduce shipping errors. This financial boost is set to expand the firm’s operational effectiveness and technological advancements.

- In February 2025, Keychain celebrated its first anniversary with remarkable achievements, announcing $1 billion in monthly project postings. Simultaneously, it introduced new verticals in packaging and ingredients, bolstered by significant funding from a major European retailer.

- In January 2025, Package.ai announced a substantial $14 million Series A funding round led by Susquehanna Growth Equity (SGE). This capital injection is intended to propel the development and deployment of advanced AI-driven solutions in the packaging industry.

- In November 2024, Ukhi raised $1.2 million to scale its production of sustainable biomaterials for packaging. This funding is expected to accelerate the company’s innovative approaches to eco-friendly packaging solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 92.6 Billion |

| Forecast Revenue (2034) | USD 161.2 Billion |

| CAGR (2025-2034) | 5.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material (Paper & Paperboard, Plastic), By Product (Die cut display containers, Corrugated cardboard boxes, Folding cartons, Shrink wrapped trays, Others), By End-use (Food & Beverages, Electronics, Personal Care & Cosmetics, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Bennett, The Cardboard Box Company, Smurfit Kappa, Weedon Group Ltd, BoxesIndia, International Paper, DS Smith, Vanguard Packaging, LLC, WestRock Company, STI – Gustav Stabernack GmbH, Mondi, Green Bay Packaging Inc., Graphic Packaging International, LLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |