Quick Navigation

Report Overview

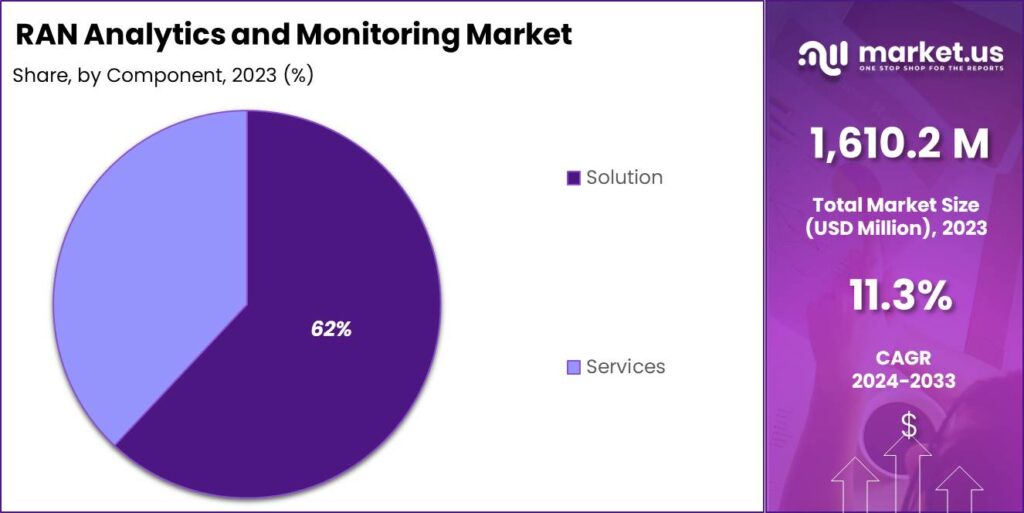

The Global RAN Analytics and Monitoring Market size is expected to be worth around USD 4,697.1 Million by 2033, from USD 1,610.2 Million in 2023, growing at a CAGR of 11.3% during the forecast period from 2024 to 2033. In 2023, North America held a dominant market position, capturing more than a 36% share, holding USD 597.7 Million revenue.

RAN Analytics and Monitoring refers to the processes and technologies used to analyze and oversee the operations of Radio Access Networks (RAN). RAN forms a vital part of mobile telecommunication systems, linking mobile devices to other parts of a network through radio connections. The analytics part focuses on extracting insights from data generated by RAN components to enhance performance, optimize resource allocation, and improve user experience.

The RAN Analytics and Monitoring market is experiencing significant growth, driven by the increasing demand for efficient and reliable wireless networks. Factors such as the adoption of 5G technology, the proliferation of connected devices, and the need for improved network efficiency are contributing to this expansion. The market is expected to witness substantial growth in the coming years, presenting lucrative opportunities for industry participants and stakeholders.

Several factors are propelling the growth of the RAN Analytics and Monitoring market. The widespread deployment of 5G networks necessitates sophisticated monitoring solutions to ensure seamless connectivity and high data rates. Additionally, the rising number of connected devices, including IoT gadgets, requires efficient network resource management.

Operators are also focusing on enhancing user experience and reducing operational costs, further driving the adoption of analytics and monitoring tools. The demand for RAN Analytics and Monitoring solutions is escalating as operators strive to maintain high-quality network performance amid growing user expectations.

The increasing reliance on wireless connectivity for various applications has made it imperative for operators to promptly identify and address network issues. Furthermore, the complexity of modern radio access networks requires advanced tools to manage and troubleshoot effectively, contributing to the rising market demand.

The evolving telecommunications landscape presents numerous opportunities for the RAN Analytics and Monitoring market. The emergence of new applications, such as smart cities and autonomous vehicles, demands real-time network monitoring and optimization. Additionally, the growing preference for cloud-based solutions offers scalability and flexibility, making advanced analytics tools more accessible to operators and service providers.

Technological advancements are at the forefront of the RAN Analytics and Monitoring market’s evolution. The integration of artificial intelligence (AI) and machine learning (ML) enables more accurate analysis of network data, allowing operators to predict and mitigate potential issues proactively. Moreover, the development of cloud-based analytics platforms provides scalable solutions that can handle the increasing data volumes generated by modern networks.

Key Takeaways

- The Global RAN Analytics and Monitoring Market is on a strong growth trajectory, with its value projected to reach USD 4,697.1 million by 2033, up from USD 1,610.2 million in 2023. This impressive expansion reflects a compound annual growth rate (CAGR) of 11.3% from 2024 to 2033.

- In 2023, the Solution segment emerged as the frontrunner, dominating the market with over 62% of the total share. This highlights the growing demand for advanced solutions that optimize RAN performance and operational efficiency.

- The 4G segment also held a commanding position, capturing more than 51% of the market share in 2023. Despite the ongoing 5G rollout, 4G networks remain crucial for many operators, driving significant investments in analytics and monitoring tools for this technology.

- Among end-use industries, the Telecommunications sector led the charge, accounting for over 48% of the market in 2023. This dominance is fueled by the need for telcos to enhance network quality, reduce operational costs, and improve user experiences.

- Regionally, North America stood out as the largest market, holding more than 36% of the global share in 2023. The region’s leadership is driven by its advanced telecom infrastructure and high adoption of cutting-edge RAN analytics technologies.

Component Segment Analysis

In 2023, the Solution segment held a dominant market position within the RAN Analytics and Monitoring market, capturing more than a 62% share. This substantial market share can be attributed to the increasing demand for robust network performance and real-time analytics in the telecommunications industry.

As telecom operators and service providers strive to enhance network reliability and efficiency, the deployment of advanced RAN solutions has become imperative. These solutions enable effective monitoring and management of network operations, leading to improved service quality and customer satisfaction. The prominence of the Solution segment is further bolstered by the rapid deployment of 5G networks globally, which requires sophisticated analytics to optimize network functions and reduce operational costs.

RAN solutions provide critical insights into network behavior, allowing operators to make data-driven decisions that enhance network performance and scalability. Moreover, these solutions support the implementation of automated processes and AI-driven analytics, which are vital for managing the complexity of modern radio access networks.

Furthermore, the integration of AI and machine learning technologies into RAN solutions has revolutionized the way network data is analyzed and utilized. These technologies enable predictive maintenance, capacity planning, and anomaly detection, which are crucial for maintaining high network availability and performance. The ability to predict and mitigate network issues before they affect users contributes significantly to the segment’s growth, as it directly impacts customer retention and satisfaction.

The services associated with RAN analytics and monitoring also play a supportive role in the market, although they hold a smaller share compared to solutions. These services include professional services like consulting, implementation, and support, which are essential for the successful deployment of RAN analytics solutions. As the complexity of networks increases, the demand for specialized services that offer expert guidance and ongoing support will likely continue to grow, complementing the solutions segment and driving the overall market forward.

Application Segment Analysis

In 2023, the 4G segment held a dominant market position, capturing more than a 51% share of the Global RAN Analytics and Monitoring Market. The dominance of the 4G segment in the market is driven by its widespread adoption and infrastructure maturity. 4G meets the growing demand for mobile internet, streaming and online services across urban and rural areas.

This dominance can be attributed to the mature infrastructure of 4G networks which continue to underpin a vast array of mobile communication deployments globally. Despite the rapid advancement and rollout of 5G technologies, 4G remains indispensable, primarily due to its widespread coverage and reliability which ensures continued consumer and enterprise connectivity.

The sustained preference for 4G is driven by its established ecosystem and the extensive penetration of 4G-enabled devices, which outweigh the current global adoption rates of newer network technologies. Furthermore, the technological stability of 4G networks allows telecom operators to deliver consistent service quality, meeting the ongoing demand for high-speed mobile internet and supporting the backbone of numerous critical communication applications in both urban and rural settings.

Additionally, the integration of advanced analytics and real-time monitoring solutions into 4G networks enhances operational efficiencies. These technologies enable operators to swiftly identify and rectify network performance bottlenecks, thereby reducing downtime and improving user experiences. This capability is vital as it supports the vast volume of data traffic handled by 4G networks and aids in maintaining robust network performance amid increasing data consumption and connectivity demands.

Looking ahead, while the market anticipates a gradual shift towards more 5G deployments, the role of 4G will remain foundational. Operators continue to leverage 4G networks to ensure a seamless transition and integration with emerging 5G infrastructures, thereby safeguarding ongoing investments and maximizing the utility of existing network assets

End User Segment Analysis

In 2024, the Telecommunications segment held a dominant market position within the RAN Analytics and Monitoring sector, capturing more than a 48% share. This substantial market share can be primarily attributed to the critical need for sophisticated analytics and monitoring solutions within this sector.

Telecommunications providers are increasingly reliant on these solutions to effectively manage network performance, optimize network usage, and enhance overall customer experience. The pivotal role of telecommunications in RAN analytics and monitoring is further underscored by the sector’s requirements to handle vast amounts of data traffic and maintain service quality across extensive network infrastructures.

As networks evolve, particularly with the rollout of 5G technologies, the complexity and scale of managing these networks increase significantly. This drives the demand for advanced analytics solutions that can provide real-time insights into network performance and user engagement, thus enabling proactive management and optimization of network resources.

Moreover, the telecommunications industry’s investment in RAN analytics is not merely about sustaining existing infrastructure but is also driven by the strategic need to reduce operational costs and enhance service delivery. The integration of AI and machine learning technologies into RAN solutions is particularly notable, enabling more predictive capabilities in network management and maintenance.

This technological integration helps telecommunications providers not only to anticipate and swiftly address potential issues but also to improve the overall quality of experience for their customers, thereby solidifying their market position and ensuring customer retention in a highly competitive market.

Key Market Segments

By Component

- Solution

- Services

By Application

- 4G

- 5G

- 3G & 2G

By End-User

- Telecommunications

- IT

- Healthcare

- BFSI

- Retail

- Manufacturing

- Others

Driver

Integration of AI and Machine Learning

The RAN Analytics and Monitoring market is experiencing substantial growth, significantly driven by the integration of artificial intelligence (AI) and machine learning (ML) technologies. These technologies are transforming the telecommunications industry by enabling more sophisticated analytics capabilities.

AI and ML not only enhance the ability to monitor and optimize network performance in real-time but also facilitate predictive maintenance and anomaly detection. This technological advancement supports the increasingly complex network architectures associated with 5G and IoT deployments, where traditional monitoring methods fall short.

The ability to predict and prevent faults before they affect users significantly improves the reliability and efficiency of telecom networks, leading to enhanced customer satisfaction and reduced operational costs. This trend is expected to continue driving the demand for advanced RAN analytics solutions as network operators seek to manage the growing scale and complexity of their networks efficiently.

Restraint

Complexity of Network Environments

One of the primary restraints facing the RAN Analytics and Monitoring market is the complexity of modern network environments. As networks become denser and more complex, integrating and managing advanced analytics solutions becomes increasingly challenging. The rapid pace of technological advancements necessitates frequent updates and upgrades to analytics systems, which can be resource-intensive.

Moreover, the heterogeneity of network technologies often leads to interoperability issues, adding another layer of complexity to the deployment and operationalization of analytics solutions. These factors can slow down the adoption of RAN analytics and monitoring technologies, limiting market growth. Organizations must navigate these complexities to deploy effective solutions that can keep up with the continuous evolution of network technologies.

Opportunity

Adoption of Cloud-Based Solutions

The shift towards cloud-based RAN analytics and monitoring solutions presents a significant opportunity for market growth. Cloud-based platforms offer scalability and flexibility, which are crucial in managing the increasing volume of data and the growing complexity of network infrastructures. These platforms enable telecom operators and enterprises to deploy advanced analytics without the need for substantial upfront investments in infrastructure.

Additionally, cloud-based solutions support rapid deployment and innovation, allowing organizations to adapt quickly to changing market needs and technological advancements. The adoption of cloud computing technologies and the focus on digital transformation are likely to propel the growth of cloud-based RAN analytics solutions, making them a pivotal area of development in the telecommunications sector.

Challenge

Data Privacy and Security Concerns

Data privacy and security emerge as significant challenges in the RAN Analytics and Monitoring market. With the increasing reliance on network data for operational decision-making, ensuring the security and integrity of this data becomes paramount. The growing concerns about data breaches and cyber-attacks require robust security measures, including advanced encryption and strict compliance with data protection regulations.

These security measures need to be integrated into RAN analytics solutions without compromising the performance or scalability of the network. Addressing these security concerns is crucial for maintaining trust and ensuring the reliability of network services, especially as regulations and threats evolve continuously.

Growth Factors

The RAN Analytics and Monitoring market is experiencing robust growth, driven by several pivotal factors. Chief among these is the accelerating deployment of 5G networks, which necessitates advanced analytics to manage the increased complexity and ensure optimal performance. The rising number of connected devices, which intensifies network traffic and complexity, also pushes the demand for more sophisticated monitoring and management solutions.

Furthermore, the shift towards digital transformation across various industries amplifies the need for robust network infrastructure, making RAN analytics an essential tool for businesses aiming to leverage new technologies and improve operational efficiency. This trend is coupled with a growing emphasis on enhancing the Quality of Experience (QoE) for network users, which directly benefits from improvements in network analytics capabilities.

Impact of AI on Market

Artificial Intelligence (AI) is revolutionizing the RAN Analytics and Monitoring market by introducing capabilities that allow for more precise and predictive network management. AI technologies facilitate the automation of complex processes such as network optimization, fault management, and predictive maintenance.

These advancements are crucial for handling modern networks that are not only larger but also more dynamic due to the variability in traffic and the array of services they support. AI enhances the ability of network operators to detect and rectify issues before they impact users, thereby improving the reliability and efficiency of network services. The integration of AI is not just a trend but a core component in the evolution of RAN analytics, driving the industry towards more proactive and less reactive management paradigms.

Emerging Trends

Several emerging trends are shaping the RAN Analytics and Monitoring market. The migration towards cloud-based solutions reflects a broader move within telecommunications to embrace cloud technologies, offering scalability and flexibility in network management. Another significant trend is the increased use of machine learning algorithms for deeper insights into network operations, which enables more effective decision-making and operational enhancements.

Additionally, the adoption of virtualized network functions continues to grow, which integrates well with advanced analytics to improve network agility and cost-efficiency. These trends collectively contribute to a more adaptive, responsive, and efficient networking environment, catering to the increasing demands of modern digital communications.

Business Benefits

Adopting RAN Analytics and Monitoring solutions offers substantial business benefits, primarily by enhancing network performance and user experience. For telecommunications providers, these tools are crucial in managing the ever-growing data traffic and network complexity, ensuring that service quality remains high. This capability directly contributes to customer satisfaction and retention, key metrics for business success in competitive markets.

Additionally, RAN analytics helps in optimizing operational expenditures by pinpointing inefficiencies and preventing revenue loss due to downtime or suboptimal performance. For businesses across various sectors, such as healthcare, BFSI, and manufacturing, RAN analytics ensures that their network infrastructures are robust, secure, and capable of supporting critical operations, thus enabling them to focus on core business activities without the overhead of network-related issues.

Regional Analysis

In 2024, North America held a dominant market position in the RAN Analytics and Monitoring market, capturing more than a 36% share with revenues amounting to USD 597.7 million. This leadership can be attributed to several key factors that distinguish the region in the global landscape.

Firstly, the rapid deployment of advanced telecommunications infrastructure, particularly 5G networks, across the region has been a significant driver. North America’s early and aggressive rollout of 5G has necessitated robust RAN analytics and monitoring solutions to manage the increased complexity and ensure optimal network performance.

This has spurred demand for advanced analytics solutions that can provide real-time insights into network operations and user experiences, thus enhancing the overall efficiency and reliability of telecommunications services. Moreover, North America is home to many of the leading players in the telecommunications and technology sectors, such as Cisco Systems, Intel Corporation, and Qualcomm.

These companies are not only major users of RAN analytics solutions but also contribute to the region’s leadership through their innovations in the field. Their continuous research and development efforts have led to the creation of more sophisticated analytics tools that cater to the evolving needs of modern networks, further propelling the market’s growth in the region.

Additionally, the presence of a highly developed IT infrastructure and a strong emphasis on regulatory compliance for data protection in North America have made it essential for network operators to invest in reliable and effective RAN analytics and monitoring systems. These systems help ensure that networks are not only efficient but also secure and compliant with stringent data security standards, thus boosting the adoption of these solutions across the region.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the highly competitive RAN Analytics and Monitoring market, three key players—Ericsson, Nokia, and Huawei – stand out due to their strategic initiatives, including acquisitions, new product launches, and mergers.

Ericsson has been proactive in launching new RAN analytics and monitoring solutions that leverage AI and machine learning to enhance network performance and efficiency. This strategy not only strengthens their product offerings but also consolidates their position in the market by addressing the growing demand for sophisticated network management tools necessary for modern telecommunications infrastructure.

Nokia continues to push the boundaries of RAN analytics through both development and strategic partnerships. Their focus has been on integrating analytics capabilities that enhance the performance and reliability of 5G networks. Nokia’s efforts are aimed at providing operators with advanced tools for network troubleshooting and optimization, which are critical for maintaining high-quality service in the rapidly evolving telecom sector.

Huawei, similarly, has expanded its RAN analytics solutions by incorporating AI technologies to improve network operations and customer experience. Their products are designed to support telecom operators in managing complex networks efficiently, ensuring optimal performance across various regions and network types.

Top Key Players in the Market

- Ericsson

- Nokia

- Huawei Technologies

- ZTE Corporation

- Cisco Systems

- NEC Corporation

- Samsung Electronics

- Juniper Networks

- Viavi Solutions

- Anritsu Corporation

- Spirent Communications

- Keysight Technologies

- Rohde & Schwarz

- Infovista

- Radcom Ltd.

- Teoco Corporation

- NetScout Systems

- Other Key Players

Recent Developments

- In 2024, Nokia introduced the concept of RAN Intelligent Agents to enhance 5.5G networks with intelligence. This innovation includes a telecom foundation model, RAN digital twins system, and intelligent computing power to improve network productivity.

- Huawei proposed the idea of RAN Intelligent Agents at their 2024 Analyst Summit. This technology aims to reshape network operations, experience, and service models to help operators achieve significant improvements in network productivity for 5.5G.

- At Mobile World Congress 2024, Samsung showcased its latest innovations in virtualized RAN (vRAN) and Open RAN. The company announced it has deployed over 38,000 O-RAN compliant vRAN commercial sites globally with Tier 1 operators.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1,610.2 Mn |

| Forecast Revenue (2033) | USD 4,697.1 Mn |

| CAGR (2024-2033) | 11.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Solution, Services), By Application (5G, 4G, 3G & 2G), By End-User (Telecommunications, IT, Healthcare, BFSI, Retail, Manufacturing, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Ericsson, Nokia, Huawei Technologies, ZTE Corporation, Cisco Systems, NEC Corporation, Samsung Electronics, Juniper Networks, Viavi Solutions, Anritsu Corporation, Spirent Communications, Keysight Technologies, Rohde & Schwarz, Infovista, Radcom Ltd., Teoco Corporation, NetScout Systems, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |