Quick Navigation

Report Overview

The Radioimmunoassay Market size is expected to be worth around US$ 1.2 billion by 2034 from US$ 0.7 billion in 2024, growing at a CAGR of 5.4% during the forecast period 2025 to 2034. Increasing demand for highly sensitive and specific diagnostic tools is driving the growth of the radioimmunoassay (RIA) market.

Radioimmunoassay is a powerful technique used to measure concentrations of antigens, hormones, and other biomarkers in blood and other bodily fluids. It plays a critical role in detecting diseases such as cancer, HIV, thyroid disorders, and cardiovascular conditions by offering highly accurate results at low concentrations. The rising prevalence of chronic diseases and the need for effective diagnostic methods to monitor conditions like diabetes and endocrine disorders is significantly contributing to the demand for RIA.

In July 2022, the World Health Organization reported that by the end of 2021, around 38.4 million people globally were living with HIV, with an estimated 1.5 million new cases diagnosed that year, underscoring the continued need for awareness, treatment, and prevention efforts. Recent trends indicate increasing use of RIA in both clinical and research settings for drug discovery and monitoring therapeutic efficacy.

Additionally, the growing focus on personalized medicine and the integration of RIA with advanced technologies, such as automation and high-throughput screening, presents opportunities for further market growth. As the demand for more precise diagnostic tools and improved treatment monitoring solutions rises, the RIA market is poised for continued innovation and expansion.

Key Takeaways

- In 2024, the market for Radioimmunoassay generated a revenue of US$ 0.7 billion, with a CAGR of 5.4%, and is expected to reach US$ 1.2 billion by the year 2034.

- The product type segment is divided into radiobinding assay, immunoradiometric assay, and radioreceptor assay, with immunoradiometric assay taking the lead in 2024 with a market share of 47.6%.

- Considering application, the market is divided into oncology, endocrinology, infectious disease, and immunology. Among these, oncology held a significant share of 42.3%.

- Furthermore, concerning the detection method segment, the market is segregated into solid-phase and liquid-phase. The solid-phase sector stands out as the dominant player, holding the largest revenue share of 63.5% in the Radioimmunoassay market.

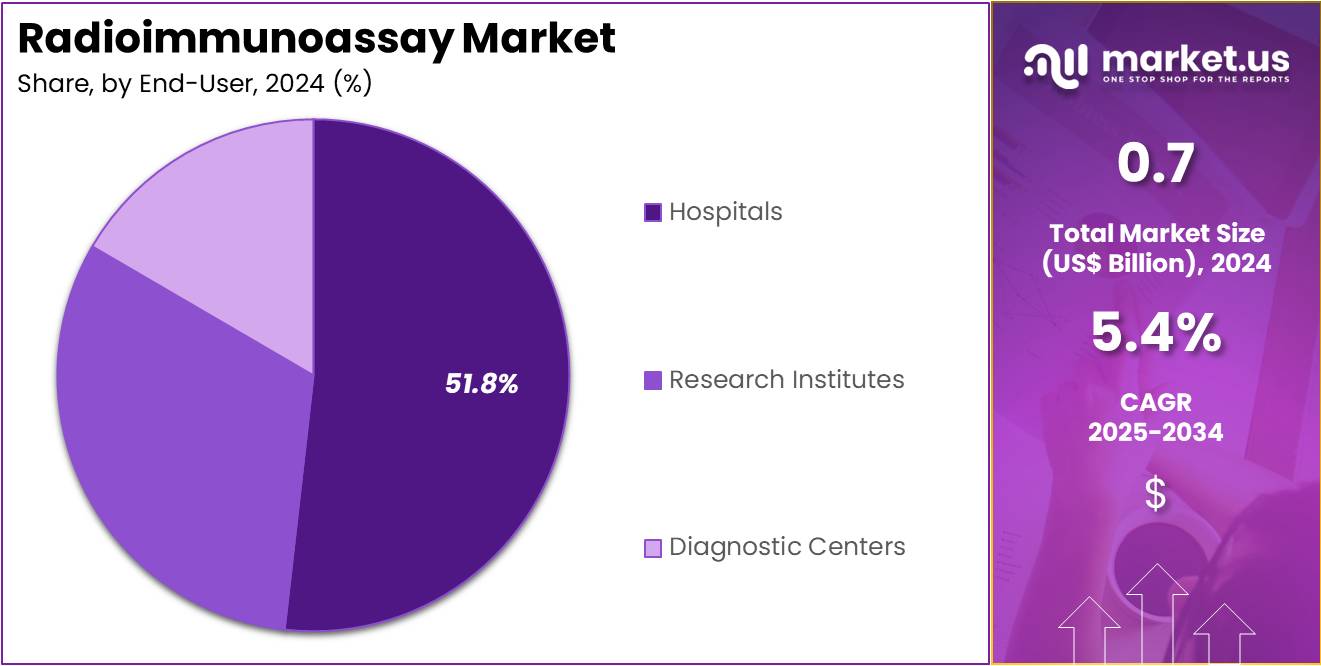

- The end-user segment is segregated into hospitals, research institutes, and diagnostic centers, with the hospitals segment leading the market, holding a revenue share of 51.8%.

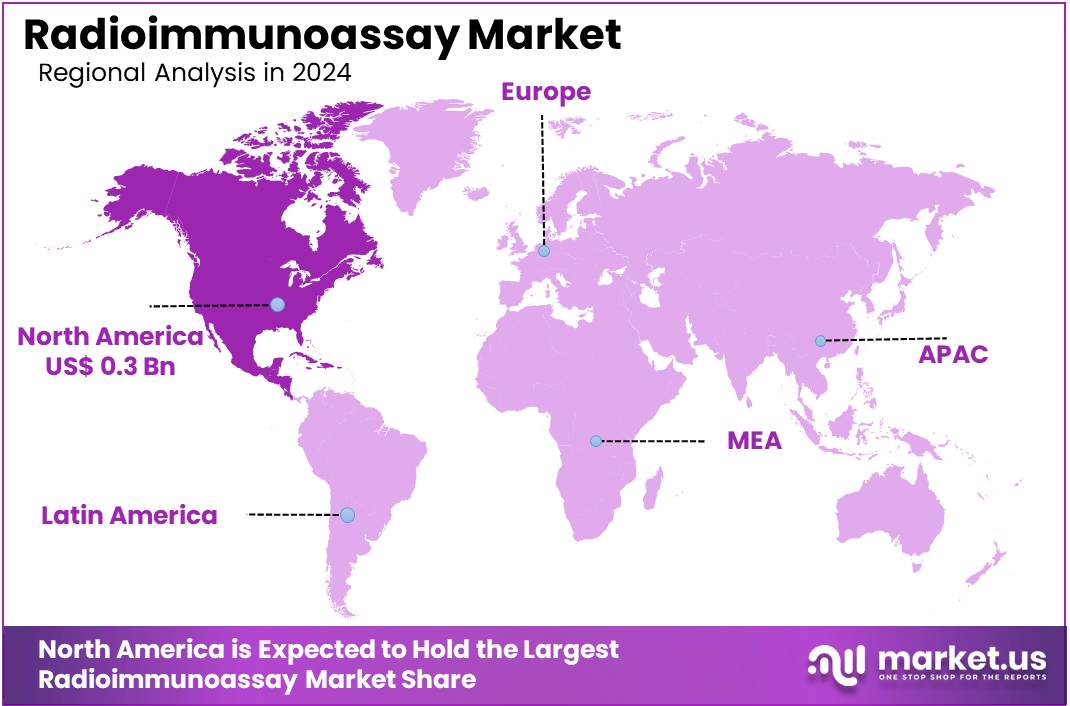

- North America led the market by securing a market share of 40.5% in 2024.

Product Type Analysis

The immunoradiometric assay segment led in 2024, claiming a market share of 47.6% owing to its increasing application in clinical diagnostics and research. This growth is driven by the assay’s high sensitivity and ability to detect low levels of target antigens, making it suitable for detecting diseases such as cancer, autoimmune disorders, and infectious diseases. The immunoradiometric assay is anticipated to benefit from advancements in technology, which enhance its accuracy, speed, and ease of use.

As the demand for early disease detection and personalized medicine increases, the need for precise diagnostic tools, like immunoradiometric assays, is projected to rise. Furthermore, the growing focus on molecular diagnostics and the integration of immunoradiometric assays into automated diagnostic platforms are likely to propel market growth.

Application Analysis

The oncology held a significant share of 42.3% due to the rising global incidence of cancer and the increasing demand for precise diagnostic and therapeutic solutions. Radioimmunoassay techniques, particularly those used in oncology, offer high specificity and sensitivity for detecting biomarkers associated with various cancers, such as breast, prostate, and lung cancer. These techniques are anticipated to improve cancer diagnosis and monitoring, enabling earlier intervention and more personalized treatment approaches.

The growth of the oncology segment is also driven by the continued adoption of immuno-oncology therapies, which require advanced diagnostic tools to assess the effectiveness of treatments. As healthcare providers and researchers increasingly rely on radioimmunoassay to support oncology clinical trials, this segment is expected to experience substantial growth.

Detection Method Analysis

The solid-phase segment had a tremendous growth rate, with a revenue share of 63.5% owing to its advantages in terms of sensitivity, reproducibility, and ease of automation. Solid-phase assays use a solid substrate to immobilize the antigen or antibody, facilitating better signal detection and higher accuracy compared to liquid-phase assays. This method is particularly beneficial in high-throughput testing, which is increasingly in demand in clinical diagnostics and pharmaceutical research.

The solid-phase segment is anticipated to benefit from advancements in materials and technology that improve assay performance and efficiency. As healthcare and research institutions continue to prioritize cost-effective, reliable diagnostic solutions, the solid-phase detection method is projected to see substantial growth.

End-user Analysis

The hospitals segment showed significant growth, contributing 51.8% of the revenue. This rise is due to the increasing demand for precise diagnostic tools in hospital settings. Hospitals are adopting radioimmunoassay techniques to enhance patient care, especially in oncology, immunology, and infectious diseases. The growing need for rapid and accurate testing is pushing hospitals to integrate these platforms into their laboratories. Additionally, the focus on personalized medicine is increasing, making radioimmunoassay a crucial tool for delivering targeted treatments and improving diagnostic accuracy.

The expansion of hospital-based research and clinical trials is fueling demand for advanced diagnostic technologies. Hospitals are becoming hubs for high-complexity diagnostics, boosting the adoption of radioimmunoassay. These techniques enable quicker and more reliable test results, enhancing clinical decision-making.

With rising investments in healthcare infrastructure, hospitals are expected to further integrate these methods. As precision medicine advances, radioimmunoassay will remain essential for hospitals looking to improve diagnostic efficiency and patient outcomes, ensuring continued market growth.

Key Market Segments

By Product Type

- Radiobinding Assay

- Immunoradiometric Assay

- Radioreceptor Assay

By Application

- Oncology

- Endocrinology

- Infectious Disease

- Immunology

By Detection Method

- Solid-Phase

- Liquid-Phase

By End-user

- Hospitals

- Research Institutes

- Diagnostic Centers

Drivers

Growing Prevalence of Cancer Driving the Radioimmunoassay Market

Rising cancer prevalence is expected to drive the radioimmunoassay market as demand for precise diagnostic tools continues to grow. A February 2022 report from the World Health Organization revealed that approximately 400,000 children are diagnosed with cancer worldwide each year, emphasizing the need for improved pediatric cancer care and treatment access. Early detection plays a crucial role in improving survival rates, and radioimmunoassay offers highly sensitive biomarker analysis for accurate diagnosis.

Healthcare providers are increasingly using this technique to measure hormone levels, tumor markers, and antigens in cancer patients. Advanced laboratory automation is improving efficiency, enabling faster test processing and higher throughput. Pharmaceutical companies rely on radioimmunoassay for drug development and therapeutic monitoring, strengthening its role in oncology research. Increased investment in personalized medicine is further fueling the need for advanced diagnostic methods.

Expanding cancer screening programs in hospitals and diagnostic laboratories are promoting wider adoption of radioimmunoassay. The integration of AI-driven analytics is enhancing data interpretation, allowing for more accurate clinical decisions. Government initiatives supporting early cancer detection are expected to boost market growth. Collaborations between research institutions and diagnostic manufacturers are accelerating the development of innovative radioimmunoassay applications. These factors contribute to the rising demand for precise and efficient cancer diagnostics.

Restraints

High Costs Are Restraining the Radioimmunoassay Market

High costs are limiting the widespread adoption of radioimmunoassay, particularly in resource-constrained healthcare settings. The use of radioactive isotopes in testing requires specialized facilities, increasing operational expenses for laboratories. Strict regulatory requirements for handling radioactive materials add complexity and delay approval processes. The disposal of radioactive waste incurs additional costs, making compliance with environmental safety regulations challenging.

Many hospitals and diagnostic centers opt for alternative immunoassay methods that offer similar accuracy without requiring radiolabeled reagents. Limited availability of trained professionals to conduct and interpret radioimmunoassay tests further restricts its use. The high price of radioimmunoassay kits and reagents adds financial strain, particularly for smaller laboratories and developing markets. Overcoming these cost barriers through technological advancements and regulatory support could improve accessibility and market growth.

Opportunities

Increasing Diagnostic Capabilities as an Opportunity for the Radioimmunoassay Market

Growing advancements in diagnostic capabilities are anticipated to create new opportunities in the radioimmunoassay market. In June 2023, DiaSorin introduced the LIAISON B·R·A·H·M·S MR-proADM immunodiagnostic assay, making it available in regions recognizing the CE Mark. This launch highlights the industry’s focus on expanding diagnostic precision for various medical conditions.

Advanced radioimmunoassay techniques are improving the detection of low-concentration biomarkers, enhancing early disease diagnosis. Integration with automation platforms is streamlining workflows, reducing manual errors, and increasing efficiency in laboratories. AI-powered diagnostic software is enhancing data interpretation, supporting faster and more accurate clinical decisions.

Growing adoption in pharmaceutical research is strengthening radioimmunoassay’s role in drug development and biomarker validation. Increased investment in precision medicine is driving demand for highly sensitive immunoassays in personalized treatment strategies. Expanding healthcare infrastructure in emerging markets is creating new growth avenues, enabling broader access to advanced diagnostic solutions. These developments are expected to accelerate the adoption of radioimmunoassay in clinical and research applications.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly affect the radioimmunoassay market. On the positive side, increasing healthcare investments and growing demand for accurate diagnostic solutions, particularly in cancer detection, drive market growth. The rising prevalence of chronic diseases, especially cancer, necessitates the development of more effective diagnostic tools, contributing to the expansion of radioimmunoassay techniques. However, economic downturns or healthcare budget cuts may reduce spending on diagnostic technologies, especially in resource-constrained regions.

Geopolitical tensions, trade restrictions, and regulatory discrepancies between countries can disrupt the supply chains for essential reagents and equipment, potentially delaying product availability or increasing costs. Moreover, stringent regulations and approval processes for new diagnostics can limit market entry for innovative technologies. Despite these challenges, the continued advancements in diagnostic accuracy, the growing focus on personalized medicine, and the increasing demand for non-invasive diagnostic methods ensure a positive outlook for the market’s future growth.

Latest Trends

Rise in Mergers and Acquisitions Driving the Radioimmunoassay Market

Rising mergers and acquisitions are becoming a significant trend driving the radioimmunoassay market. High demand for innovative and accurate diagnostic solutions, coupled with the need to expand market reach, is expected to encourage companies to merge or acquire specialized firms. These strategic moves enable companies to integrate advanced technologies, expand their product portfolios, and improve their service offerings.

The ability to leverage expertise from various sectors enhances the development of cutting-edge diagnostic solutions, improving both the accuracy and efficiency of radioimmunoassay techniques. Increasing mergers and acquisitions are likely to foster further innovation, ensuring faster commercialization of novel technologies.

In May 2023, Freenome, a private biotechnology company, completed the acquisition of Oncimmune Ltd, a UK-based firm specializing in immunodiagnostics. This acquisition strengthens Freenome’s clinical and commercial capabilities, advancing its early cancer detection and screening programs. As mergers and acquisitions continue to rise, the market is expected to benefit from more integrated and advanced diagnostic solutions, driving its continued expansion.

Regional Analysis

North America is leading the Radioimmunoassay Market

North America dominated the market with the highest revenue share of 40.5% owing to increasing demand for highly sensitive diagnostic techniques and expanding applications in endocrinology, oncology, and infectious disease testing. The rising prevalence of chronic diseases such as diabetes, thyroid disorders, and hormone-related conditions fueled the need for precise and reliable diagnostic methods.

Advancements in immunoassay technologies, including improved automation and enhanced sensitivity, contributed to the widespread adoption of radioimmunoassay in clinical laboratories and research institutions. Strong investments in pharmaceutical and biotechnology research further drove demand, particularly in drug development and therapeutic monitoring.

Regulatory support for advanced diagnostic tools and favorable reimbursement policies facilitated market expansion. Additionally, collaborations between academic institutions and healthcare companies strengthened innovation and accessibility. The presence of well-established healthcare infrastructure and a growing focus on early disease detection reinforced North America’s leadership in the market.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to increasing demand for cost-effective diagnostic solutions and expanding healthcare infrastructure. The Indian government’s implementation of a 5% import duty on Hepatitis B and HIV diagnostic kits since February 2022 reflects the region’s focus on boosting domestic manufacturing and reducing reliance on imported diagnostic tools.

Expanding pharmaceutical research and growing investments in biotechnology are anticipated to drive demand for advanced immunoassay techniques. Increasing prevalence of infectious diseases and endocrine disorders is likely to support adoption in hospitals, diagnostic laboratories, and research facilities. Collaborations between local manufacturers and global diagnostic firms are projected to enhance product availability and affordability.

Rising awareness of early disease detection and government-backed healthcare initiatives are expected to improve access to advanced diagnostics. Additionally, technological advancements in automated immunoassay systems and radioisotope-based testing methods are anticipated to strengthen market growth across Asia Pacific.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the radioimmunoassay market focus on advancing assay sensitivity and automation to improve diagnostic accuracy in detecting hormones, cancer markers, and infectious diseases. Companies invest in research and development to enhance radioisotope labeling techniques and ensure compliance with evolving regulatory standards.

Strategic collaborations with healthcare institutions and research laboratories help expand market reach and accelerate the adoption of advanced immunoassay solutions. Geographic expansion into regions with increasing demand for precise diagnostic tools supports further growth. Many players also prioritize cost-effective solutions and improved laboratory workflow integration to enhance efficiency and accessibility.

Beckman Coulter is a leading company in this market, offering high-quality immunoassay solutions tailored for clinical and research applications. The company focuses on innovation by integrating automation and advanced detection technologies to improve diagnostic reliability. Beckman Coulter’s commitment to scientific excellence and global expansion strengthens its position as a key player in the radioimmunoassay industry.

Top Key Players in the Radioimmunoassay Market

- Thermo Fisher Scientific

- Roche

- QuidelOrtho Corporation

- Ortho Clinical Diagnostics

- EKF Diagnostics Holdings plc

- DiaSorin

- Becton, Dickinson and Company

- Abbott Laboratories

Recent Developments

- In July 2021, DiaSorin finalized its acquisition of Luminex Corporation, expanding its molecular diagnostics and radioimmunoassay portfolio. By integrating Luminex’s multiplexing technology, DiaSorin strengthened its immunodiagnostics capabilities, positioning itself as a key player in advanced diagnostic solutions.

- In March 2021, Roche, a Swiss-based healthcare company, introduced an upgraded version of its Cobas pro-integrated solutions analyzer, launching eight new configurations in CE-certified regions. The enhanced model significantly boosts efficiency, delivering up to 4,400 tests per hour.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 0.7 billion |

| Forecast Revenue (2034) | US$ 1.2 billion |

| CAGR (2025-2034) | 5.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Radiobinding Assay, Immunoradiometric Assay, and Radioreceptor Assay), By Application (Oncology, Endocrinology, Infectious Disease, and Immunology), By Detection Method (Solid-Phase and Liquid-Phase), By End-user (Hospitals, Research Institutes, and Diagnostic Centers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Thermo Fisher Scientific, Roche, QuidelOrtho Corporation, Ortho Clinical Diagnostics, EKF Diagnostics Holdings plc, DiaSorin, Becton, Dickinson and Company, and Abbott Laboratories. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |