Quick Navigation

- Report Overview

- Key Takeaways

- Vector Type Analysis

- Workflow Analysis

- Application Analysis

- Disease Analysis

- End-user Analysis

- Key Market Segments

- Drivers

- Restraints

- Opportunities

- Impact of Macroeconomic / Geopolitical Factors

- Trends

- Regional Analysis

- Key Regions and Countries

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

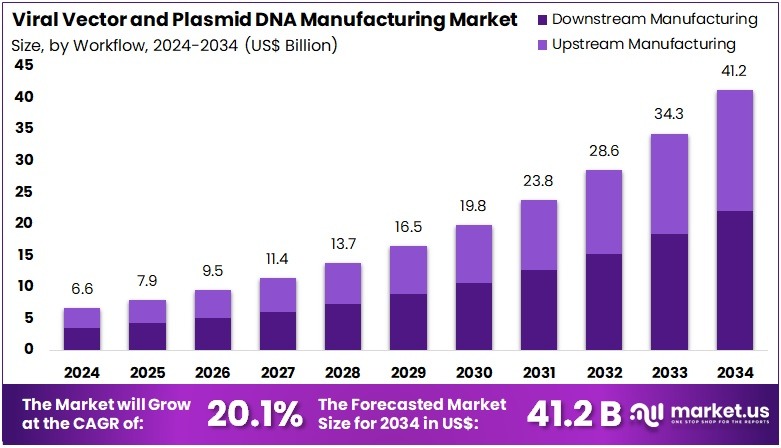

The Viral Vector and Plasmid DNA Manufacturing Market Size is expected to be worth around US$ 41.2 billion by 2034 from US$ 6.6 billion in 2024, growing at a CAGR of 20.1% during the forecast period 2025 to 2034.

Growing demand for advanced gene therapies and vaccines is driving the expansion of the viral vector and plasmid DNA manufacturing market. Viral vectors and plasmid DNA are essential components in the development and production of gene therapies, DNA vaccines, and cell therapies. Rising investments in biotechnology and pharmaceutical sectors, along with an increasing focus on personalized medicine, are fueling the growth of this market. Viral vectors are particularly important in the delivery of therapeutic genes, while plasmid DNA is a key component in vaccine development and gene editing applications.

In April 2022, FUJIFILM Corporation, through its subsidiary FUJIFILM Diosynth Biotechnologies, acquired a cell therapy manufacturing facility from Atara Biotherapeutics in Thousand Oaks, California, boosting its cell therapy production capabilities. The growing prevalence of genetic disorders, cancer, and infectious diseases is accelerating the need for scalable viral vector and plasmid DNA production.

Additionally, the rapid development of mRNA vaccines, particularly in response to the COVID-19 pandemic, has significantly increased the demand for efficient manufacturing solutions. The emergence of new technologies such as CRISPR and gene editing further propels market growth by creating new opportunities for viral vector applications in research and clinical settings. As the regulatory landscape becomes more supportive of gene therapies and vaccines, the market for viral vector and plasmid DNA manufacturing is set to continue its expansion, offering considerable opportunities for companies specializing in these manufacturing processes.

Key Takeaways

- In 2024, the market for viral vector and plasmid DNA manufacturing generated a revenue of US$ 6.6 billion, with a CAGR of 20.1%, and is expected to reach US$ 41.2 billion by the year 2034.

- The vector type segment is divided into adenovirus, retrovirus, plasmids, lentivirus, adeno-associated virus (AAV), and others, with adeno-associated virus (AAV) taking the lead in 2024 with a market share of 24.6%.

- Considering workflow, the market is divided into upstream manufacturing and downstream manufacturing. Among these, downstream manufacturing held a significant share of 53.5%.

- Furthermore, concerning the application segment, the market is segregated into antisense & RNAi therapy, vaccinology, research applications, gene therapy, and cell therapy. The vaccinology sector stands out as the dominant player, holding the largest revenue share of 42.3% in the viral vector and plasmid DNA manufacturing market.

- The disease segment is segregated into cancer, infectious diseases, genetic disorders, and others, with the cancer segment leading the market, holding a revenue share of 48.9%.

- Considering end-user, the market is divided into pharmaceutical and biopharmaceutical companies and research institutes. Among these, research institutes held a significant share of 59.3%.

- North America led the market by securing a market share of 46.9% in 2024.

Vector Type Analysis

The adeno-associated virus (AAV) segment led in 2024, claiming a market share of 24.6% owing to its increasing application in gene therapy. AAV vectors are highly regarded for their ability to deliver genes to a wide variety of tissues with minimal immune response, making them ideal for long-term gene expression. The rising number of gene therapies aimed at treating genetic disorders, particularly rare diseases, is anticipated to drive this segment’s expansion.

Furthermore, advances in AAV manufacturing technologies, which offer improved yields and quality, are likely to support market growth. The growing number of clinical trials using AAV vectors for gene therapies is projected to further increase demand, making AAV one of the most preferred viral vectors in the market.

Workflow Analysis

The downstream manufacturing held a significant share of 53.5%. As gene therapies become more prevalent, the demand for efficient and scalable downstream processing technologies is expected to rise. Downstream manufacturing is critical for purifying and formulating viral vectors and plasmid DNA, ensuring that they meet stringent quality standards required for clinical and commercial applications.

Innovations in purification techniques and the need for large-scale production of high-quality vectors are projected to drive the growth of this segment. Additionally, the increasing focus on viral vector-based gene therapies is likely to contribute to the heightened demand for optimized downstream manufacturing processes, ensuring the safety and efficacy of therapeutic products.

Application Analysis

The vaccinology segment had a tremendous growth rate, with a revenue share of 42.3% owing to the increasing demand for viral vector-based vaccines. The global rise in infectious diseases, such as the COVID-19 pandemic, has underscored the need for rapid vaccine development, with viral vectors playing a critical role in creating effective and safe vaccines.

As viral vectors offer several advantages, such as the ability to induce both humoral and cellular immune responses, the demand for these vaccines is expected to grow. The success of viral vector-based vaccines in clinical trials is anticipated to drive further investments in this segment. Moreover, the ability of viral vectors to target specific cells and induce durable immunity is likely to spur the development of new vaccines, further driving the growth of the vaccinology segment.

Disease Analysis

The cancer segment grew at a substantial rate, generating a revenue portion of 48.9% due to the increasing application of gene therapies in oncology. Viral vectors are increasingly being used to deliver therapeutic genes directly to cancer cells, offering a targeted treatment approach with the potential for higher efficacy and fewer side effects. The growing number of cancer gene therapy trials, particularly those focusing on immunotherapies and oncolytic viruses, is anticipated to drive market growth.

Additionally, advancements in viral vector manufacturing techniques that improve vector stability and scalability are likely to contribute to the expansion of this segment. As cancer continues to be a leading cause of death worldwide, the demand for effective gene therapies is projected to rise, boosting the cancer segment’s growth.

End-user Analysis

The research institutes held a significant share of 59.3% due to the increasing focus on academic and clinical research in gene therapy and genomics. Research institutions play a crucial role in the development of new viral vector technologies and therapeutic applications. The rise in funding for gene-based research, particularly in the fields of genetic disorders, cancer, and infectious diseases, is expected to drive demand for viral vectors and plasmid DNA in these settings.

Moreover, the growing number of collaborations between academic institutions and pharmaceutical companies is likely to further boost the demand for viral vectors. As research institutes continue to focus on advancing gene therapy techniques, the need for high-quality viral vectors and plasmid DNA will likely contribute to the growth of this segment.

Key Market Segments

By Vector Type

- Adenovirus

- Retrovirus

- Plasmids

- Lentivirus

- Adeno-Associated Virus (AAV)

- Others

By Workflow

- Upstream Manufacturing

- Vector Amplification & Expansion

- Vector Recovery/Harvesting

- Downstream Manufacturing

- Purification

- Fill Finish

By Application

- Antisense & RNAi Therapy

- Vaccinology

- Research Applications

- Gene Therapy

- Cell Therapy

By Disease

- Cancer

- Infectious Diseases

- Genetic Disorders

- Others

By End-user

- Pharmaceutical and Biopharmaceutical Companies

- Research Institutes

Drivers

Increasing gene and cell therapy clinical trials and approvals is driving the market

Increasing gene and cell therapy clinical trials and approvals is driving the viral vector and plasmid DNA manufacturing market. Viral vectors and plasmid DNA are fundamental components for delivering genetic material in these advanced therapies. As more gene and cell therapies demonstrate promising results in clinical trials and gain regulatory approval, the demand for high-quality manufacturing of these vectors and plasmids escalates.

Each new therapy progressing through the pipeline requires reliable and scalable production of its specific vector or plasmid. The American Society of Gene & Cell Therapy (ASGCT) reported that the gene, cell, and RNA therapy pipeline landscape grew by 7% in 2024, consistent with the growth seen in 2022 and 2023, indicating a sustained expansion of therapeutic candidates requiring manufacturing support.

Restraints

The high cost and complexity of manufacturing is restraining the market

The high cost and complexity of manufacturing is restraining the viral vector and plasmid DNA manufacturing market. Producing clinical-grade viral vectors and plasmid DNA involves intricate processes, specialized equipment, and stringent quality control measures to ensure safety and efficacy. Scaling up production from research-grade to commercial quantities while maintaining consistency and purity presents significant technical and financial challenges. These complexities contribute to high manufacturing costs per dose, which can impact the overall affordability and accessibility of gene and cell therapies.

Organizations like the National Institute for Innovation in Manufacturing Biopharmaceuticals (NIIMBL), a public-private partnership, are investing in projects aimed at improving manufacturing efficiency; for instance, NIIMBL reported an US$ 11 Million investment in new technology projects in areas such as mRNA vaccines, cell processing, and critical quality attribute measurement during 2022-2023, highlighting the ongoing need to address manufacturing hurdles.

Opportunities

Advancements in manufacturing technologies and emergence of new vector types is creating growth opportunities

Advancements in manufacturing technologies and emergence of new vector types is creating growth opportunities in the viral vector and plasmid DNA manufacturing market. Innovations in cell culture techniques, upstream and downstream processing, and analytical methods are improving the efficiency, scalability, and cost-effectiveness of producing viral vectors and plasmid DNA.

The development of novel vector platforms with improved safety profiles and tissue targeting capabilities also expands the potential applications of gene and cell therapies, consequently increasing the demand for their manufacturing. These technological advancements open new avenues for market players to offer improved manufacturing solutions.

Government initiatives supporting biomanufacturing research and development, such as those outlined in the US government’s fact sheet on actions to advance biotechnology and biomanufacturing, which notes over US$29 billion in public and private sector biomanufacturing investments since the start of the Biden-Harris Administration, foster the development of these advanced manufacturing technologies.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the market for viral vector and plasmid DNA manufacturing. Global economic conditions impact the availability of venture capital and other funding crucial for biotechnology companies developing gene and cell therapies, directly affecting the demand for manufacturing services. Inflation increases the cost of raw materials, reagents, and energy required for complex manufacturing processes.

Geopolitical tensions can disrupt international supply chains for specialized materials, equipment, and skilled labor needed in manufacturing facilities. For instance, the US government’s 2021-2024 Quadrennial Supply Chain Review highlighted vulnerabilities in healthcare and other critical supply chains. Despite these challenges, a heightened focus on national biosecurity and securing domestic biomanufacturing capabilities, often a response to geopolitical instability, drives government investment and incentives to build resilient manufacturing infrastructure within the US.

Current US tariff policies also impact the market for viral vector and plasmid DNA manufacturing. Tariffs on imported manufacturing equipment, such as bioreactors, chromatography systems, and purification equipment, as well as on certain raw materials like specialized chemicals or cell culture media components, can increase the cost of establishing and operating manufacturing facilities in the US. These increased costs can potentially affect the competitiveness of domestic manufacturing and influence pricing for vectors and plasmids.

While the impact varies depending on specific tariff codes, duties on essential manufacturing inputs can create financial burdens. According to a survey conducted in February 2025, nearly 90% of US biotech companies relied on imported components, indicating the potential for tariffs to increase manufacturing costs. However, these tariffs can also incentivize domestic production of manufacturing equipment and materials, fostering a more robust and secure national manufacturing ecosystem for these critical components of advanced therapies.

Trends

Growing focus on in-house manufacturing capabilities by therapeutic developers is a recent development in the market

Growing focus on in-house manufacturing capabilities by therapeutic developers is a recent development in the viral vector and plasmid DNA manufacturing market. To gain greater control over the manufacturing process, quality, and supply chain security for their gene and cell therapies, a number of therapeutic development companies are investing in building or expanding their own manufacturing facilities. This strategic shift reduces reliance on contract manufacturing organizations and allows companies to tailor production specifically to their proprietary processes and product needs.

While this represents a change in the market dynamic, it also drives investment in manufacturing equipment, technologies, and skilled personnel within the therapeutic development sector. According to J.P. Morgan’s Q4 2024 Biopharma Industry Insights report, biopharma venture dollar volume reached US$ 26.0 billion in 2024 through December 9, indicating substantial investment flowing into therapeutic developers, which often includes funding for manufacturing capabilities.

Regional Analysis

North America is leading the Viral Vector and Plasmid DNA Manufacturing Market

North America dominated the market with the highest revenue share of 46.9% owing to the expanding clinical applications of gene therapies. The FDA has approved an increasing number of gene therapies, fueling demand for the vectors and DNA used in their production. For instance, the FDA approved 3 gene therapy products in 2022 and 2 in 2023, as documented on their website. Each of these approvals necessitates significant quantities of high-quality vectors.

Furthermore, the substantial funding from the National Institutes of Health (NIH) for gene therapy research supports market growth. The NIH Data Book indicates that in fiscal year 2023, the NIH awarded over US$ 1.3 billion in grants related to gene therapy research. Specifically, within that funding, a significant portion was allocated to research projects focused on developing and improving viral vector technologies, which are critical for gene delivery in these therapies.

This commitment is evident in the NIH’s increasing funding for research programs focused on gene therapy. The ongoing progress in gene editing technologies, which often utilize viral vectors for delivery, also contributes to the increased demand for their manufacture.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is projected to witness the fastest CAGR due to growing investments in biotechnology and biopharmaceutical research. Countries like China are expanding their R&D budgets significantly. According to China’s National Bureau of Statistics, R&D expenditure reached 2.54% of GDP in 2022. A major portion of this was directed toward biotechnology, including gene therapy innovations. These developments are supported by regional initiatives to advance healthcare technologies. As gene therapy research progresses, the demand for supporting technologies such as vector and plasmid DNA manufacturing is expected to rise steadily.

The increasing prevalence of genetic disorders in Asia Pacific is further accelerating the need for advanced therapies. Improved healthcare infrastructure in nations like India, China, and South Korea is enabling faster clinical adoption. Moreover, regulatory bodies across the region are working to establish clear guidelines for gene therapy development and approval. These evolving frameworks are anticipated to provide greater confidence to manufacturers and researchers. Collectively, these factors are fostering a robust environment for market growth in gene therapy and its supporting industries.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the viral vector and plasmid DNA manufacturing market focus on increasing production capacity, optimizing manufacturing processes, and expanding their service offerings to meet the growing demand for gene therapies and vaccines. They invest heavily in technological advancements to enhance the efficiency and scalability of production systems. Strategic collaborations with biopharma companies, academic institutions, and contract development and manufacturing organizations (CDMOs) are key to their growth strategies.

Geographical expansion, particularly in emerging markets, allows these companies to capture new opportunities. Additionally, they prioritize regulatory compliance and quality control to ensure consistent product performance across global markets. Lonza Group is a leading player in the viral vector and plasmid DNA manufacturing market, specializing in cell and gene therapy solutions. The company provides integrated services from process development to large-scale manufacturing for the production of viral vectors and plasmid DNA.

Lonza has established itself as a key partner for biopharmaceutical companies by leveraging its state-of-the-art facilities and expertise. With a focus on innovation, quality, and scalability, Lonza continues to expand its capacity and deepen its collaborations with leading biotech firms to support the rapidly evolving gene therapy industry.

Top Key Players in the Viral Vector and Plasmid DNA Manufacturing Market

- Wuxi Biologics

- Thermo Fisher Scientific

- Merck KGaA

- Lonza

- FUJIFILM Diosynth Biotechnologies

- Cobra Biologics

- BioNTech SE

- AGC Biologics

Recent Developments

- In October 2023, AGC Biologics enhanced its plasmid DNA (pDNA) and messenger RNA (mRNA) production capabilities at its Heidelberg, Germany facility. This expansion, completed in October 2023, introduced a new production line with advanced technology, allowing for increased pDNA and mRNA manufacturing.

- In February 2023, BioNTech SE finalized its first proprietary pDNA manufacturing facility in Marburg, Germany. This facility aims to independently produce pDNA for both clinical trials and commercial products related to cancer and infectious diseases.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 6.6 billion |

| Forecast Revenue (2034) | US$ 41.2 billion |

| CAGR (2025-2034) | 20.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Vector Type (Adenovirus, Retrovirus, Plasmids, Lentivirus, Adeno-Associated Virus (AAV), and Others), By Workflow (Upstream Manufacturing (Vector Amplification & Expansion, and Vector Recovery/Harvesting), Downstream Manufacturing (Purification, and Fill Finish)), By Application (Antisense & RNAi Therapy, Vaccinology, Research Applications, Gene Therapy, and Cell Therapy), By Disease (Cancer, Infectious Diseases, Genetic Disorders, and Others), By End-user (Pharmaceutical and Biopharmaceutical Companies, and Research Institutes) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Wuxi Biologics, Thermo Fisher Scientific, Merck KGaA, Lonza, FUJIFILM Diosynth Biotechnologies, Cobra Biologics, BioNTech SE, and AGC Biologics. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |