Quick Navigation

Report Overview

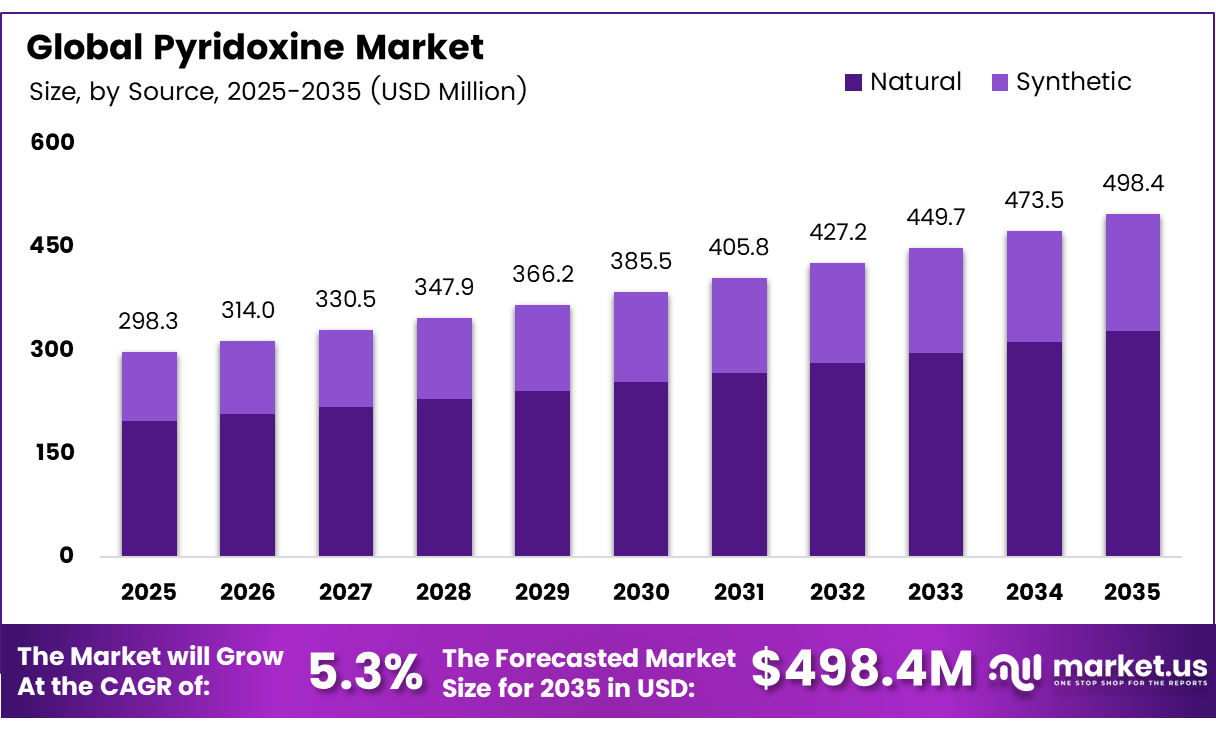

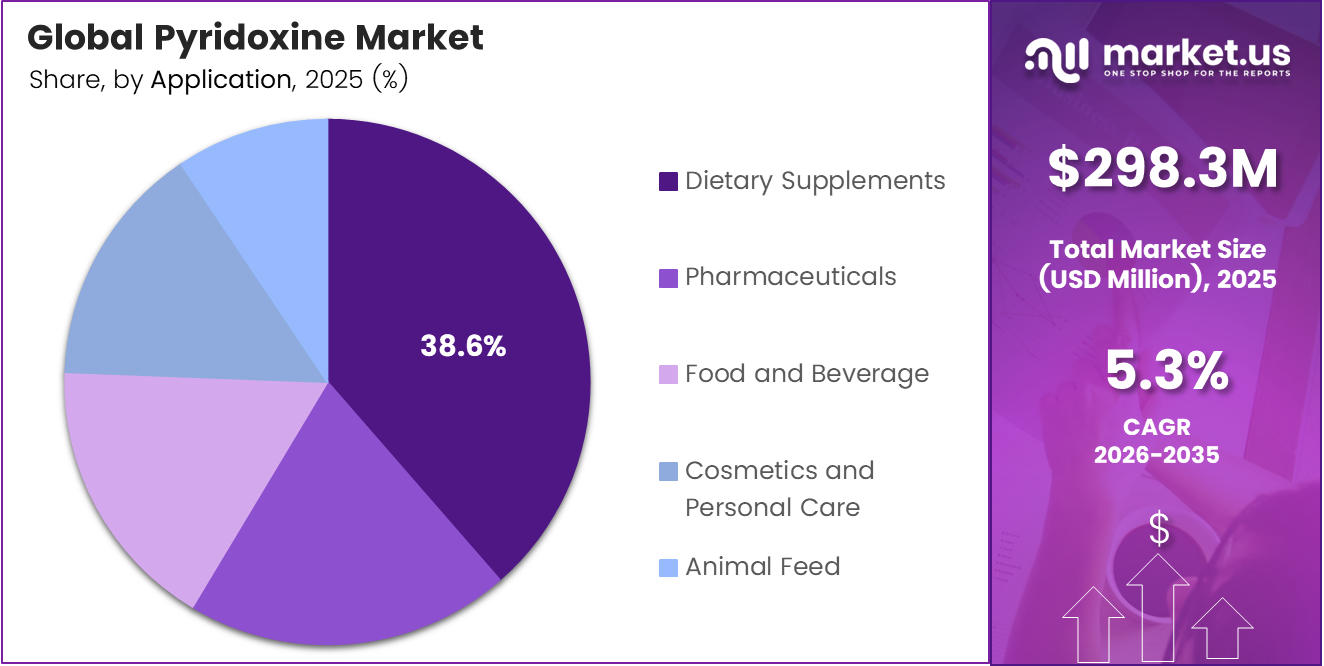

The Global Pyridoxine Market size is expected to be worth around USD 498.4 million by 2035 from USD 298.3 million in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

Pyridoxine, the primary commercial form of Vitamin B6, functions as a coenzyme in over 100 enzymatic reactions involving amino acid metabolism, neurotransmitter synthesis, and immune regulation. Its broad biochemical role makes it indispensable across dietary supplements, pharmaceuticals, fortified foods, and animal feed applications. This functional versatility directly explains why demand persists across consumer, clinical, and industrial channels simultaneously.

The pharmaceutical segment uses pyridoxine in neurological disorder management and metabolic disease treatment. Clinicians prescribe it for conditions including pyridoxine-dependent epilepsy, nausea in pregnancy, and peripheral neuropathy. This clinical anchoring creates a stable, non-discretionary demand base, which differentiates pyridoxine from purely lifestyle-driven supplement categories that are more vulnerable to consumer sentiment shifts.

Feed-grade pyridoxine hydrochloride must comply with a 99.0%–101.0% assay specification and maintain a 48-month shelf life in sealed original packaging, highlighting the industry’s increasing focus on reliable and traceable ingredient quality. For tablet formulations, at least 75% of the labeled pyridoxine hydrochloride must dissolve within 45 minutes, establishing a pharmaceutical-grade standard for bioavailability and strengthening the market position of suppliers that consistently achieve these quality benchmarks.

The animal feed industry adds another structural demand layer. Livestock producers use pyridoxine supplementation to optimize poultry and swine health, particularly for growth performance and feed conversion efficiency. As protein consumption rises globally, feed additive demand scales proportionally — creating a parallel commercial channel that insulates the overall market from weakness in any single end-use category.

Functional food and beverage manufacturers actively fortify products with Vitamin B6 to meet consumer interest in preventive nutrition. Cereal producers, sports drink brands, and energy supplement makers incorporate pyridoxine into formulations targeting immune support, cognitive performance, and metabolic efficiency. This broadens the addressable market well beyond pharmacy channels and into fast-moving consumer goods retail.

Key Takeaways

- The Global Pyridoxine Market is valued at USD 298.3 million in 2025 and is forecast to reach USD 498.4 million by 2035 at a CAGR of 5.3% from 2026 to 2035.

- Tablets hold the dominant share at 41.2% of total market revenue.

- Dietary Supplements account for the largest share at 38.6%.

- Natural-sourced pyridoxine commands 64.7% of the market.

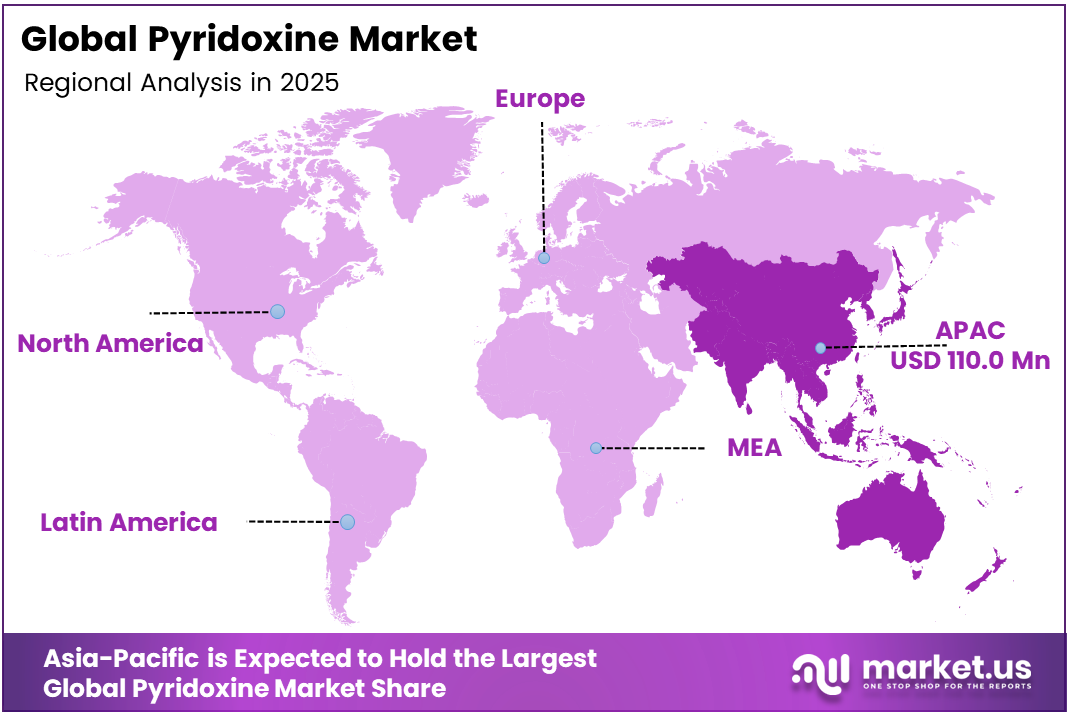

- Asia-Pacific leads all regions with a 36.9% market share, valued at USD 110.0 million.

Product Analysis

Tablets dominate with 41.2% due to dosage precision and broad retail accessibility.

In 2025, Tablets held a dominant market position in the By Product segment of the Pyridoxine Market, with a 41.2% share. Tablets deliver measured pyridoxine doses that meet USP-NF pharmaceutical standards, making them the preferred format for both clinical and retail supplement buyers. Their long shelf stability and low manufacturing cost reinforce procurement preference across institutional and consumer channels.

Capsules serve buyers who prioritize faster dissolution and formulation flexibility over tablets. Capsule formats allow combination with other B-complex vitamins or bioavailability-enhancing excipients, making them attractive to premium supplement brands. However, higher per-unit production costs restrict their penetration in price-sensitive markets, positioning capsules as a mid-to-premium segment play.

Application Analysis

Dietary Supplements dominate with 38.6% due to high consumer adoption in preventive nutrition.

In 2025, Dietary Supplements held a dominant market position in the By Application segment of the Pyridoxine Market, with a 38.6% share. Consumer self-medication trends and preventive health awareness drive consistent retail demand for standalone B6 and B-complex formulations. This segment also benefits from lower regulatory barriers compared to pharmaceuticals, enabling faster product launches and broader retail distribution.

Pharmaceuticals anchor pyridoxine demand in regulated clinical settings. Neurologists and obstetricians prescribe pyridoxine for conditions including neuropathy, pyridoxine-dependent epilepsy, and pregnancy-related nausea, creating a stable, non-discretionary revenue base. Pharmaceutical-grade requirements enforce strict quality compliance, which concentrates supply toward producers with validated manufacturing capabilities.

Source Analysis

Natural-sourced pyridoxine dominates with 64.7% due to clean-label consumer preference and regulatory alignment.

In 2025, Natural source pyridoxine held a dominant market position in the By Source segment of the Pyridoxine Market, with a 64.7% share. Buyers across dietary supplements, functional foods, and cosmetics increasingly specify natural-origin Vitamin B6 to meet clean-label certification requirements and consumer transparency expectations. This preference creates a procurement premium that natural-source suppliers can sustain even at higher production costs.

Synthetic pyridoxine retains significant commercial relevance in pharmaceutical and animal feed applications where cost efficiency outweighs origin claims. Chemical synthesis delivers high-purity, specification-controlled pyridoxine hydrochloride at scale — a requirement for pharmaceutical tablet manufacturing and bulk feed premix production. However, growing clean-label scrutiny in food and supplement channels continues to redirect volume toward natural alternatives over time.

Key Market Segments

By Product

- Tablets

- Capsules

- Powders

- Fortified Foods

- Liquids

By Application

- Dietary Supplements

- Pharmaceuticals

- Food and Beverage

- Cosmetics and Personal Care

- Animal Feed

By Source

- Natural

- Synthetic

Emerging Trends

Microencapsulation and High-Potency Complex Formats Reshape Pyridoxine Product Development

Supplement brands shift from single-vitamin tablets toward high-potency B-complex formulations that combine pyridoxine with B12 and folate for immune and cognitive health positioning. This bundling strategy raises average selling prices per unit while reducing consumer reliance on standalone B6 products. Manufacturers with multi-nutrient blending capacity gain a clear commercial advantage in premium retail channels.

Microencapsulation technology improves pyridoxine stability, extends shelf life, and enhances bioavailability in food and supplement matrices. Vitamin B6 Typ 1 limits total plate count to fewer than 100 CFU/g and requires Salmonella to be negative in 25 g samples. These microbial benchmarks reflect tightening formulation quality standards that microencapsulation processes help manufacturers consistently meet.

Sports nutrition brands actively incorporate pyridoxine into pre-workout, energy, and recovery formulations targeting active lifestyle consumers. This positions Vitamin B6 as a performance ingredient rather than a basic nutritional supplement, unlocking higher-margin retail segments. Brands that successfully anchor pyridoxine within sports science claims differentiate their products from commodity B-vitamin offerings and command stronger shelf placement.

Drivers

Clinical Demand, Fortification Mandates, and Livestock Health Programs Collectively Sustain Pyridoxine Volume Growth

Physicians and clinical nutrition protocols actively prescribe pyridoxine for neurological disorder management, including peripheral neuropathy and metabolic disease treatment. Australia’s Therapeutic Goods Administration reported 250 Vitamin B6-related neuropathy adverse-event reports, reflecting both widespread clinical use and growing regulatory attention on dosage safety. This dual signal accelerates pharmaceutical-grade procurement and tightens formulation quality expectations.

Food manufacturers fortify cereals, infant formula, and functional beverages with pyridoxine to comply with national nutrition standards. These regulatory fortification requirements convert discretionary purchasing into mandatory ingredient inclusion, insulating demand from consumer sentiment fluctuations. Manufacturers who supply specification-compliant pyridoxine to food producers benefit from long-term supply agreements tied to production volumes rather than retail trends.

The global livestock industry uses pyridoxine supplementation to improve amino acid metabolism, feed conversion efficiency, and immune function in poultry and swine. As global meat protein consumption rises, feed additive volumes scale proportionally. This animal nutrition channel provides a structurally separate demand base that buffers pyridoxine producers against softness in human health segments during cyclical slowdowns.

Restraints

Regulatory Compliance Costs and Raw Material Volatility Compress Manufacturer Margins

Chemical synthesis of pyridoxine requires multi-step reaction processes using price-volatile raw materials, including 3-hydroxy-4-methyl pyridine precursors. Input cost swings directly compress manufacturer margins because long-term supply contracts with food and feed buyers typically fix pricing in advance. Producers without backward integration into precursor chemistry carry the highest margin exposure during periods of feedstock price pressure.

Regulatory authorities enforce increasingly detailed compliance requirements for vitamin formulations across pharmaceutical, food, and feed applications. Pyridoxine hydrochloride tablets must contain 95.0%–115.0% of the labeled content, and dissolution testing requires no less than 75% dissolution within 45 minutes using 900 mL of water at 50 rpm. Meeting these standards demands a validated analytical testing infrastructure, raising the capital threshold for new market entrants.

International market entry adds further compliance complexity as each jurisdiction enforces distinct registration timelines, documentation requirements, and maximum dosage limits. Smaller pyridoxine producers targeting export markets face product approval delays that extend time-to-revenue by months or years. This regulatory friction concentrates global trade volume among larger, compliance-resourced suppliers who can absorb registration costs across multiple markets simultaneously.

Growth Factors

Personalized Nutrition, Clean-Label Ingredients, and Developing Market Expansion Unlock New Pyridoxine Revenue Streams

Precision healthcare platforms and personalized nutrition brands develop customized supplement formulations calibrated to individual metabolic profiles. At least 125 Australian medicines deliver more than 50 mg to 200 mg of Vitamin B6 per maximum daily dose, including 116 listed complementary medicines. This volume of registered products signals a mature supplement market, creating demand templates that developing economies will replicate as healthcare infrastructure expands.

Consumer preference for clean-label and plant-based vitamin ingredients creates product development opportunities for natural-origin pyridoxine suppliers. Supplement and food brands reformulating toward recognizable, non-synthetic ingredient lists are willing to pay a premium for traceable, plant-derived B6. Suppliers with natural-source extraction capabilities and third-party certification can capture a margin advantage in this segment that synthetic producers cannot directly match.

Strategic collaborations between pharmaceutical companies and nutraceutical manufacturers accelerate the development of advanced pyridoxine delivery systems. Joint ventures combine pharmaceutical-grade quality infrastructure with nutraceutical distribution networks, enabling faster commercial scaling. Markets in Southeast Asia, South Asia, and Latin America present the clearest near-term expansion potential as rising healthcare awareness converts unaddressed nutritional deficiencies into structured supplement purchasing.

Regional Analysis

Asia-Pacific Dominates the Pyridoxine Market with a Market Share of 36.9%, Valued at USD 110.0 Million

Asia-Pacific commands 36.9% of the global Pyridoxine Market, valued at USD 110.0 million. China anchors this dominance through large-scale chemical synthesis capacity and cost-competitive manufacturing infrastructure. The region supplies both domestic demand from its own rapidly expanding supplement and food sectors and a substantial share of global export volumes to North America and Europe.

North America represents a high-value consumption market for pharmaceutical and premium supplement-grade pyridoxine. Stringent FDA and USP standards drive procurement toward specification-verified suppliers, which shifts competitive advantage toward quality-consistent producers. Strong retail supplement culture and clinical prescription volumes sustain predictable baseline demand across both pharmaceutical and consumer health channels.

Europe enforces strict maximum dosage limits for Vitamin B6 in food supplements through European Food Safety Authority guidance, directly shaping formulation decisions by regional manufacturers. Regulatory alignment across EU member states creates a unified compliance environment that benefits large suppliers with EU-approved facilities. Germany and France lead regional demand, driven by established pharmaceutical manufacturing and functional food industries.

Latin America shows expanding nutraceutical consumption as middle-class populations in Brazil and Mexico increase spending on preventive health products. Domestic supplement manufacturing remains limited, leaving the region dependent on imported pyridoxine ingredients, primarily from the Asia-Pacific region. This import dependency creates supply chain vulnerability but simultaneously signals an opportunity for suppliers capable of building regional distribution infrastructure.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Analysis

BASF SE positions itself as a vertically integrated supplier of vitamin ingredients, offering pharmaceutical- and food-grade pyridoxine across global markets. Its strength lies in combining large-scale production with multi-jurisdictional regulatory approvals, giving institutional buyers a single qualified supplier for high-volume contracts. This compliance infrastructure creates switching costs that protect long-term supply relationships even against lower-cost regional competitors.

DSM differentiates through its science-led nutrition platform, integrating pyridoxine within broader human and animal nutrition portfolios. Its ability to combine multiple B-vitamins into premix solutions for food manufacturers reduces procurement complexity for buyers, increasing the share of wallet per customer. DSM’s research investment in bioavailability and formulation stability reinforces premium positioning in markets where technical performance justifies price premiums.

HuiSheng Pharma operates as a cost-competitive Chinese manufacturer with a production scale that supports high-volume feed and food-grade pyridoxine supply. Its competitive advantage is concentrated in bulk commodity markets where price drives procurement decisions. However, rising global quality scrutiny on Chinese-origin pharmaceutical ingredients creates pressure to invest in GMP certification to maintain access to regulated Western markets.

Xinfa Pharmaceutical leverages integrated chemical synthesis capabilities to control production economics across the pyridoxine value chain. Its presence in both feed-grade and pharmaceutical-grade segments allows flexible production allocation based on demand signals. This production flexibility provides a margin management advantage during periods of segment-specific demand softness that single-channel producers cannot replicate.

Key Players

- BASF SE

- DSM

- HuiSheng Pharma

- Xinfa Pharmaceutical

- Huazhong Pharmaceutical

- Tianxin Pharmaceutical

- Torrent Pharmaceuticals Ltd.

- Rochem International Inc.

- Acebright Pharmaceuticals Group

- Hegno

- Nanjing Pharmaceutical Factory

Recent Developments

- In 2025, BASF SE continues to maintain an active presence in the global vitamins and animal nutrition market through its nutrition and health portfolio, including feed vitamin formulations connected to pyridoxine (Vitamin B6). Recent Indian government customs records from 2026 indicate continued imports of BASF-linked vitamin products under the “Lutavit” brand into India, reflecting the company’s ongoing participation in feed additive supply chains.

- In 2025, DSM-Firmenich remains one of the most recognized global suppliers of vitamins, including pyridoxine, for pharmaceutical, nutritional, and feed applications. DSM-Firmenich published several official vitamin market outlooks, noting that Vitamin B6 pricing has stabilized after earlier oversupply conditions and market softness.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 298.3 Million |

| Forecast Revenue (2035) | USD 498.4 Million |

| CAGR (2026-2035) | 5.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Tablets, Capsules, Powders, Fortified Foods, Liquids), By Application (Dietary Supplements, Pharmaceuticals, Food and Beverage, Cosmetics and Personal Care, Animal Feed), By Source (Natural, Synthetic) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | BASF SE, DSM, HuiSheng Pharma, Xinfa Pharmaceutical, Huazhong Pharmaceutical, Tianxin Pharmaceutical, Torrent Pharmaceuticals Ltd., Rochem International Inc., Acebright Pharmaceuticals Group, Hegno, Nanjing Pharmaceutical Factory |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |