Quick Navigation

Report Overview

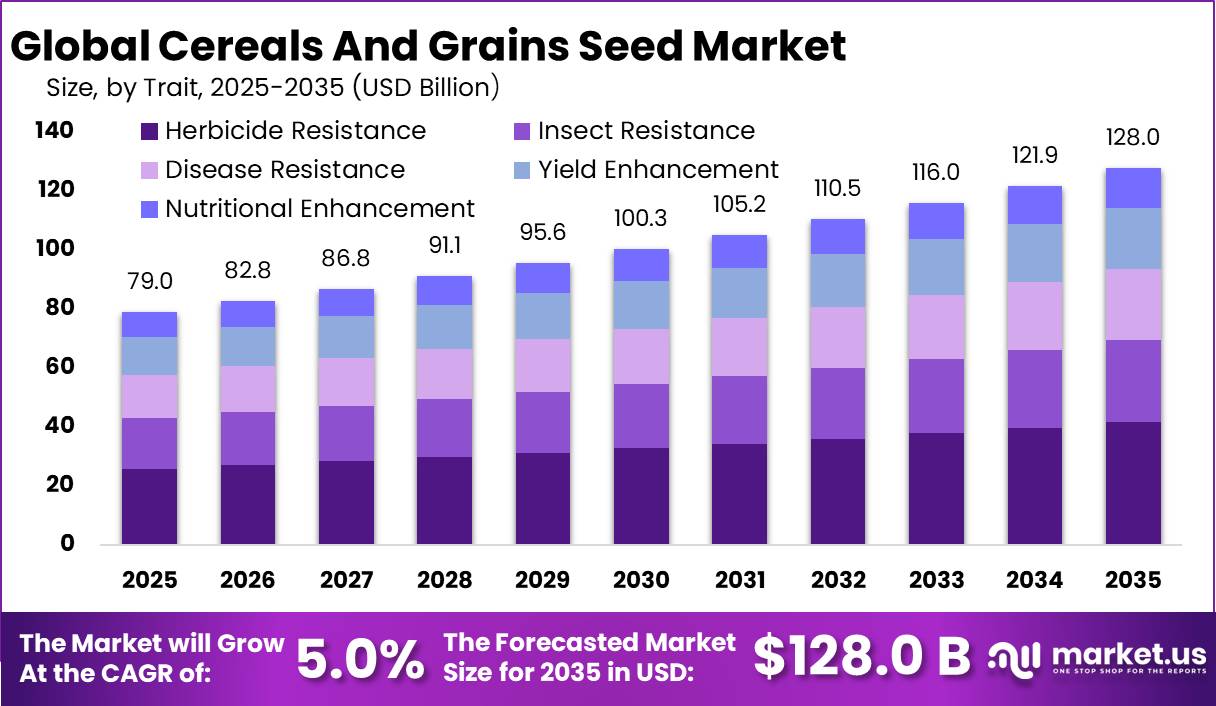

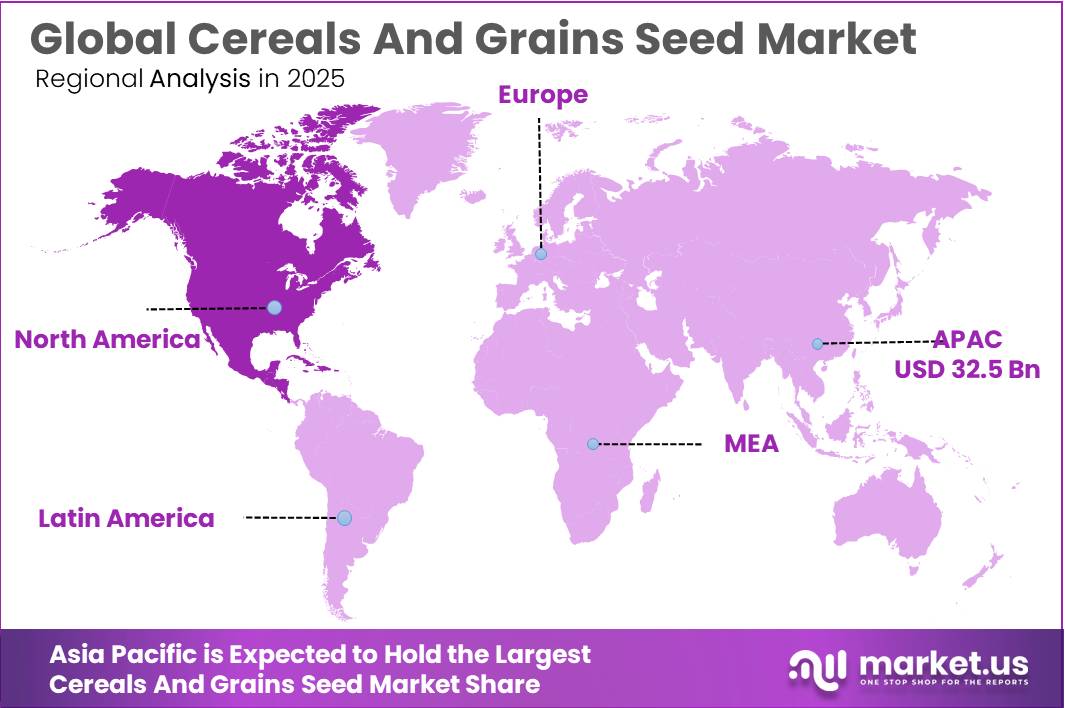

The Global Cereals And Grains Seed Market size is expected to be worth around USD 128.0 Billion by 2035, from USD 79.0 Billion in 2025, growing at a CAGR of 5.0% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 41.2% share, holding USD 32.5 Billion revenue.

Key Takeaways

- Cereals And Grains Seed Market size is expected to be worth around USD 128.0 Billion by 2035, from USD 79.0 Billion in 2025, growing at a CAGR of 5.0%.

- Industrial Grade held a dominant market position, capturing more than a 49.9% share of the Sodium Acetate market.

- Maize held a dominant market position, capturing more than a 34.8% share of the Cereals and Grains Seed market.

- Conventional Breeding held a dominant market position, capturing more than a 48.5% share of the Cereals and Grains Seed market.

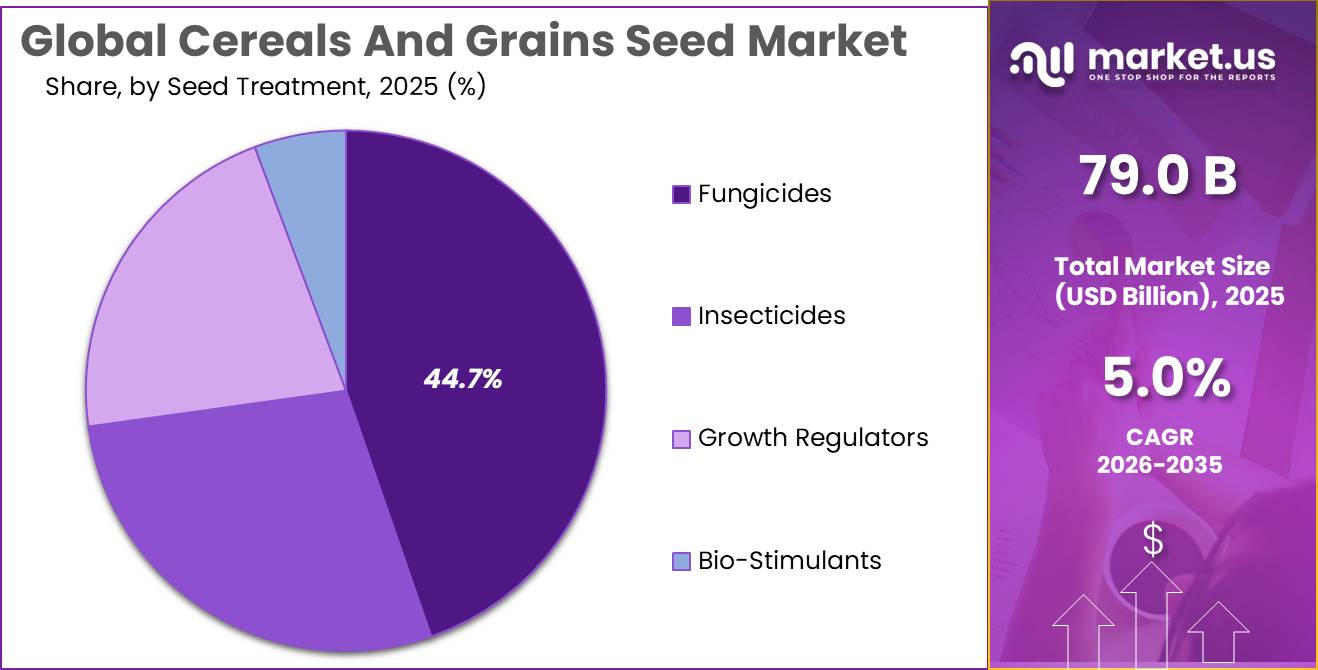

- Fungicides held a dominant market position, capturing more than a 44.7% share of the Cereals and Grains Seed market.

- Asia-Pacific held a dominant position in the global Cereals and Grains Seed market, accounting for 41.2% of the total market share and reaching a market value of nearly USD 32.5 Billion.

By Trait Analysis

Industrial Grade dominates with 49.9% share due to its wide use across chemical processing and manufacturing industries.

In 2025, Industrial Grade held a dominant market position, capturing more than a 49.9% share of the Sodium Acetate market. The segment maintained its strong presence because of rising demand from textile processing, leather treatment, construction chemicals, and industrial buffering applications. Many manufacturers preferred industrial grade sodium acetate due to its lower production cost and suitability for large-scale industrial operations where ultra-high purity was not required.

By Crop Type Analysis

Maize leads with 34.8% share driven by rising demand for high-yield and disease-resistant seed varieties.

In 2025, Maize held a dominant market position, capturing more than a 34.8% share of the Cereals and Grains Seed market. The segment showed strong growth due to the increasing global demand for maize as a food crop, animal feed ingredient, and biofuel source. Farmers continued to prefer maize seeds because of their high productivity, better adaptability across different climatic conditions, and growing availability of hybrid seed varieties. Demand remained particularly strong in regions with large-scale livestock farming, where maize is widely used in feed production.

By Technology Analysis

Conventional Breeding leads with 48.5% share as farmers continue to prefer reliable and cost-effective seed development methods.

In 2025, Conventional Breeding held a dominant market position, capturing more than a 48.5% share of the Cereals and Grains Seed market. The segment remained strong because conventional breeding methods are widely accepted across both developed and developing agricultural markets. Farmers continued to rely on these seeds due to their affordability, stable performance, and easier regulatory approval compared to advanced genetic technologies. Conventional breeding also remained popular among growers looking for crop varieties with improved yield, climate adaptability, and disease resistance without the use of complex biotechnology processes.

By Seed Treatment Analysis

Fungicides dominate with 44.7% share due to their strong role in protecting seeds from early-stage crop diseases.

In 2025, Fungicides held a dominant market position, capturing more than a 44.7% share of the Cereals and Grains Seed market. The segment experienced solid demand as farmers increasingly focused on improving seed protection and crop establishment during the early stages of cultivation. Fungicide seed treatments became widely used because they help prevent soil-borne and seed-borne fungal infections that can reduce germination rates and crop productivity. Their ability to support healthier plant growth and minimize yield losses made them an important part of cereal and grain farming practices.

Key Market Segments

By Trait

- Herbicide Resistance

- Insect Resistance

- Disease Resistance

- Yield Enhancement

- Nutritional Enhancement

By Crop Type

- Wheat

- Rice

- Maize

- Barley

- Dats

By Technology

- Conventional Breeding

- Genetic Engineering

- Hybrid Breeding

By Seed Treatment

- Fungicides

- Insecticides

- Growth Regulators

- Bio-Stimulants

Emerging Trends

Climate-Resilient and Digital Seed Technologies are Becoming the Biggest Trend in the Cereals and Grains Seed Market

One of the latest trends shaping the Cereals and Grains Seed market is the growing shift toward climate-resilient and digitally supported farming practices. Farmers are increasingly looking for seed varieties that can tolerate drought, extreme heat, and changing rainfall patterns while still maintaining stable yields. According to the Food and Agriculture Organization (FAO), climate-smart agriculture has become a major global focus as governments and agricultural institutions work to improve food security and reduce climate-related crop losses.

Seed producers are responding by developing improved cereal and grain seed varieties with stronger disease resistance and better adaptability to difficult growing environments. Climate-smart crops such as drought-tolerant maize and stress-resistant wheat are gaining wider acceptance in regions facing water shortages and unstable weather. Governments in Asia, Africa, and North America are also supporting sustainable agriculture programs that encourage the use of certified and resilient seeds.

Precision Farming and Smart Agriculture Tools are Increasing Demand for Advanced Seed Varieties

Another important trend in the Cereals and Grains Seed market is the rapid adoption of precision agriculture technologies. Farmers are using GPS-based equipment, yield monitoring systems, digital crop management tools, and AI-supported farming platforms to improve productivity and reduce operational costs.

- According to USDA-supported research, more than 50% of farms in some Midwestern U.S. states are already using precision agriculture practices, while a recent Midwest farmer survey showed that 93% of respondents used some form of digital agricultural technology.

Governments and agricultural agencies are also investing heavily in precision agriculture research and technology expansion. The U.S. Government Accountability Office reported that USDA and NSF together provided nearly US$200 million for precision agriculture research and development between 2017 and 2021.

Drivers

Rising Global Food Demand is Increasing the Need for High-Quality Grain Seeds

The growing demand for food across the world is one of the biggest driving factors for the Cereals and Grains Seed market. Countries are focusing heavily on improving crop productivity as population growth continues to put pressure on food supplies.

- According to the Food and Agriculture Organization (FAO), global cereal production is expected to reach around 3.04 billion tonnes in 2025/26, showing strong growth compared to previous years.

Farmers are increasingly adopting hybrid and treated seeds to improve harvest quality and reduce crop losses caused by changing climate conditions. Governments in many countries are also supporting cereal production through subsidies, irrigation programs, and seed distribution initiatives. In Asia and Africa, food security programs are encouraging farmers to use certified seeds to increase productivity per hectare.

Expanding Use of Cereals in Feed and Biofuel Industries Supporting Seed Demand

The increasing use of cereals in animal feed and biofuel production is also pushing demand for cereals and grains seeds. Maize especially has become an important crop for ethanol production and livestock nutrition. According to USDA estimates, around 5.6 billion bushels of corn are expected to be used for ethanol production during the 2025–26 period.

The OECD-FAO Agricultural Outlook 2025-2034 states that global cereal use is projected to increase from 2.8 billion tonnes to 3.2 billion tonnes by 2034, mainly due to higher food and feed demand. The report also highlights that nearly 33% of cereals will be used for animal feed while industrial and biofuel applications will continue to grow steadily. This rising industrial dependence on cereals is motivating seed producers to develop drought-tolerant and high-yield seed varieties suitable for large-scale farming.

Restraints

Rising Climate Stress and Unpredictable Weather are Limiting Stable Grain Production

One of the major restraining factors for the Cereals and Grains Seed market is the increasing impact of climate change on agricultural productivity. Unpredictable rainfall, droughts, floods, and rising temperatures are creating serious challenges for farmers across major grain-producing regions. According to the Food and Agriculture Organization (FAO), nearly 3.8 trillion calories in crop production have been lost globally over the last three decades due to drought conditions alone.

Many farmers are becoming cautious about investing in premium or hybrid seeds because extreme weather increases the risk of crop failure. In several developing countries, limited irrigation systems and poor access to climate-resilient farming technologies further add pressure on cereal cultivation. Governments are introducing climate adaptation programs and drought-resistant seed initiatives, but adoption remains uneven in rural areas.

High Seed Costs and Limited Farmer Purchasing Power are Slowing Adoption

The increasing cost of certified and hybrid cereal seeds is another major factor restricting market expansion, especially in low-income agricultural regions. Advanced seed varieties often require higher investment because of research, breeding, seed treatment, and storage costs.

- According to the International Maize and Wheat Improvement Center (CIMMYT), many smallholder farmers in developing economies still rely on saved seeds due to financial limitations, despite the productivity advantages of improved seed varieties. Small farms account for nearly 84% of global farms, and many operate with very limited annual agricultural budgets.

Opportunity

Rising Demand for Climate-Resilient Crops is Creating New Growth Opportunities for Seed Producers

One of the biggest growth opportunities in the Cereals and Grains Seed market is the rising demand for climate-resilient and high-yield crop varieties. Farmers across the world are facing increasing pressure from droughts, soil degradation, irregular rainfall, and pest attacks. This has created strong demand for seeds that can survive difficult growing conditions while maintaining stable crop output.

According to the Food and Agriculture Organization (FAO), global food production must increase by nearly 60% by 2050 to meet the needs of the growing population. This target is encouraging governments and agricultural organizations to invest heavily in improved seed technologies and sustainable farming practices.

Expansion of Precision Farming and Modern Agriculture Supporting Seed Innovation

The growing use of precision farming and modern agricultural equipment is creating another major opportunity for the Cereals and Grains Seed market. Farmers are increasingly using technologies such as GPS-guided tractors, smart irrigation systems, and digital crop monitoring tools to improve productivity and reduce wastage. According to the United States Department of Agriculture (USDA), precision agriculture technologies are now used on more than 60% of large-scale farms in the United States, especially for maize and wheat cultivation.

This shift toward technology-driven farming is increasing the demand for high-performance seeds that can deliver consistent yields under managed farming conditions. Seed developers are focusing on varieties with improved nutrient efficiency, faster growth cycles, and stronger resistance to climate stress. Governments in Europe, North America, and Asia are also supporting digital agriculture programs through funding and farmer training initiatives.

Regional Insights

Asia-Pacific dominates the Cereals and Grains Seed market with a 41.2% share valued at USD 32.5 Billion due to strong agricultural production and rising food demand.

In 2025, Asia-Pacific held a dominant position in the global Cereals and Grains Seed market, accounting for 41.2% of the total market share and reaching a market value of nearly USD 32.5 Billion. The region’s leadership is mainly supported by its large agricultural base, growing population, and high dependence on cereals such as rice, wheat, and maize as staple food crops.

China remains one of the world’s largest grain producers, while India continues to expand seed replacement programs and hybrid seed adoption through government-backed agricultural initiatives. The region also benefits from favorable climatic conditions and large cultivation areas for cereals and grains. Rising awareness among farmers regarding disease-resistant and climate-tolerant seeds is further supporting market growth across both developed and developing economies in Asia-Pacific.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE continues to strengthen its cereals and grains seed business through investments in seed treatment technologies and crop protection solutions. In 2025, the company allocated over €900 million toward agricultural research and development activities, supporting innovation in seed quality and disease resistance. BASF operates in more than 90 countries and serves millions of hectares of cultivated farmland globally.

Bayer AG remains one of the leading participants in the cereals and grains seed market through its Crop Science division. In 2025, the company invested nearly €2.4 billion in research and development across agriculture and seed technologies. Bayer’s seed portfolio includes maize, wheat, and rice seed solutions designed for high yield and disease tolerance. The company operates across more than 140 countries and continues expanding digital farming platforms to support precision agriculture.

Syngenta Crop Protection AG plays an important role in the cereals and grains seed market through advanced seed genetics and crop enhancement technologies. In 2025, the company expanded its seed research programs across Asia and Latin America to improve stress-resistant cereal varieties. Syngenta invests more than US$1.4 billion annually in agricultural innovation and biotechnology. The company supplies seeds and crop solutions to farmers in over 100 countries.

Top Key Players Outlook

- BASF SE

- Bayer AG

- Syngenta Crop Protection AG

- KWS SAAT SE & Co. KGaA

- Corteva Inc.

- Land O’Lakes, Inc.

- Limagrain

- UPL

- DLF

- Rallis India Limited

- TAKII & CO., LTD.

- Barenbrug South Africa (Pty) Ltd

Recent Industry Developments

In 2025, BASF SE remained active in the cereals and grains seed sector through its Agricultural Solutions business, which offers seeds, traits, seed treatment, crop protection and digital tools. The division reported €9,587 million in sales, including €2,026 million from Seeds & Traits and €575 million from Seed Treatment, while R&D spending reached €990 million.

In 2025, Corteva Inc. strengthened its cereals and grains seed work through corn and grain seed technologies, reporting Seed net sales of US$8.16 billion in the first 9 months of 2025, up 5%, with Seed operating EBITDA at US$2.51 billion, up 18%. Seed growth was supported by higher corn area, share gains in North America, early safrinha deliveries in Brazil, and recovery of corn acres in Argentina.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 79.0 Bn |

| Forecast Revenue (2035) | USD 128.0 Bn |

| CAGR (2026-2035) | 5.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Trait (Herbicide Resistance, Insect Resistance, Disease Resistance, Yield Enhancement, Nutritional Enhancement), By Crop Type (Wheat, Rice, Maize, Barley, Dats), By Technology (Conventional Breeding, Genetic Engineering, Hybrid Breeding), By Seed Treatment (Fungicides, Insecticides, Growth Regulators, Bio-Stimulants) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | BASF SE, Bayer AG, Syngenta Crop Protection AG, KWS SAAT SE & Co. KGaA, Corteva Inc., Land O’Lakes, Inc., Limagrain, UPL, DLF, Rallis India Limited, TAKII & CO., LTD., Barenbrug South Africa (Pty) Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |