Global Pre-Harvest Equipment Market Size, Share, And Industry Analysis Report By Equipment Type (Seed Drills, Plows, Harrows, Cultivators, Planters, Sprayers), By Power Source (Tractor-mounted, Self-propelled, PTO-driven Implements, Manual/Animal-draft), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables), By End User (Large-scale Farmers, Small and Medium Farmers, Agricultural Contractors, Cooperatives), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181151

- Number of Pages: 344

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

The Global Pre-Harvest Equipment Market size is expected to be worth around USD 124.4 billion by 2035 from USD 68.8 billion in 2025, growing at a CAGR of 6.1% during the forecast period 2026 to 2035.

Pre-harvest equipment includes machinery and tools used to prepare land, plant seeds, and maintain crops before harvesting. This category covers seed drills, plows, harrows, cultivators, planters, and sprayers. These machines help farmers increase crop yields while reducing manual labor. Consequently, demand for such equipment continues to rise globally.

The market benefits from growing food demand driven by a rising global population. Farmers increasingly adopt mechanized solutions to improve productivity and reduce input costs. Moreover, government initiatives in developing nations actively promote agricultural mechanization. This creates favorable conditions for sustained market growth across all major regions.

Regulatory support and subsidy programs in countries like India, China, and Brazil expand equipment access. Governments recognize that mechanization improves food security and farm income. CNH Industrial reported full-year 2025 consolidated revenues of USD 18.10 billion, reflecting how major players continue to scale despite regional demand shifts.

- Mahindra Farm Equipment captured a market share of 43.3% in India during FY2025, up 170 basis points year over year. This reflects the strong demand momentum in the Asia Pacific region, which leads global pre-harvest equipment adoption.

Europe registered 204,500 tractors in 2024, including 144,400 agricultural tractors. This data highlights continued equipment investment across established markets, reinforcing stable long-term demand. However, affordability and land fragmentation remain key challenges limiting growth in smaller farm economies.

Precision agriculture and smart farming practices further accelerate adoption. Farmers now use GPS-guided seed drills and variable-rate planters to optimize seed placement and spacing. Therefore, equipment manufacturers invest heavily in integrating digital tools into pre-harvest machinery. These advancements attract large-scale farms and progressive smallholders alike.

Key Takeaways

- The Global Pre-Harvest Equipment Market was valued at USD 68.8 billion in 2025 and is projected to reach USD 124.4 billion by 2035 at a CAGR of 6.1% during the forecast period from 2026 to 2035.

- Seed Drills dominate with a 21.4% market share in 2025.

- Tractor-mounted equipment leads the segment with a 49.1% share.

- Cereals and Grains represent the largest segment at 44.8%.

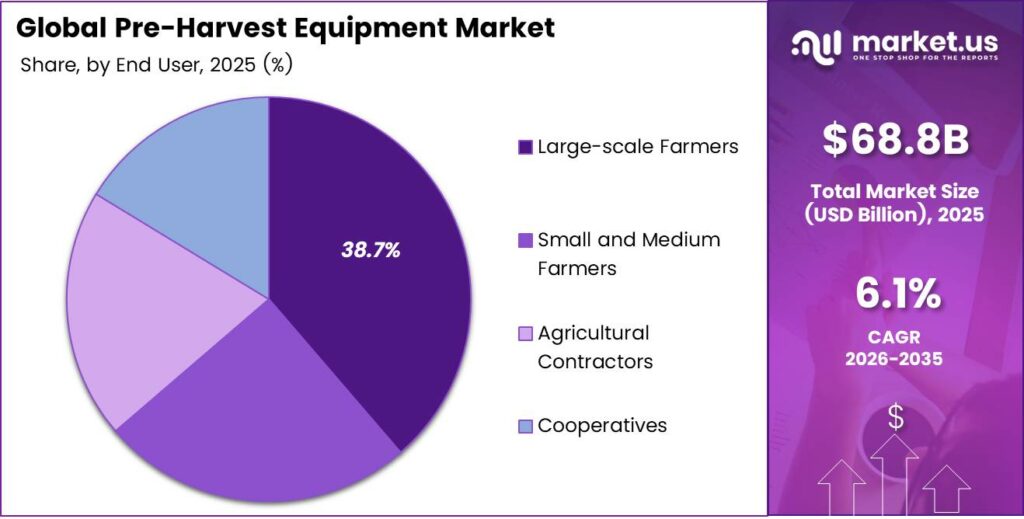

- Large-scale Farmers hold the dominant position with a 38.7% share.

- Asia Pacific dominates the regional landscape with a 41.2% market share, valued at USD 28.2 billion.

Equipment Type Analysis

Seed Drills dominate with 21.4% due to their critical role in precision seeding and higher crop yield outcomes.

In 2025, Seed Drills held a dominant market position in the By Equipment Type segment of the Pre-Harvest Equipment Market, with a 21.4% share. Seed drills deliver seeds at precise depths and spacing, directly improving germination rates. Consequently, large-scale farms and precision agriculture operators prioritize seed drill adoption across cereal and oilseed crop production systems.

Plows remain essential tools for primary tillage across global farmlands. These implements break and turn soil layers, improving aeration and root penetration. Moreover, plow demand stays consistent in regions with heavy clay soils and large grain-producing farms. Tractor-mounted versions remain the preferred choice for efficiency and compatibility with existing farm fleets.

Harrows serve a vital secondary tillage function by breaking soil clods and creating fine seedbeds. Farmers commonly use harrows after plowing to prepare optimal planting conditions. Additionally, disc and chain harrow variants support multiple crop types, making them versatile across diverse agricultural settings worldwide.

Cultivators help manage weeds and aerate soil between crop rows without disturbing plant roots. Farmers value cultivators for reducing herbicide dependence while maintaining soil health. Therefore, cultivator demand grows alongside organic farming trends and integrated pest management practices in both developed and emerging markets.

Sprayers complete the pre-harvest equipment portfolio by enabling precise application of fertilizers and crop protection products. Self-propelled and boom sprayer models dominate commercial farms. Additionally, drone-integrated spraying solutions are gaining traction in the Asia Pacific, supporting sustainable and technology-driven farming practices.

Power Source Analysis

Tractor-mounted equipment dominates with 49.1% due to its versatility and compatibility with existing farm infrastructure.

In 2025, Tractor-mounted equipment held a dominant market position in the By Power Source segment of the Pre-Harvest Equipment Market, with a 49.1% share. Farmers prefer tractor-mounted implements because they offer flexibility across multiple field tasks. Moreover, compatibility with standard tractor hitches lowers the total cost of farm mechanization significantly.

Self-propelled equipment delivers higher operational speed and output for large commercial operations. These machines integrate engines, GPS systems, and precision controls for autonomous field coverage. Consequently, self-propelled sprayers and planters are gaining adoption among large-scale farms focused on reducing labor dependency and operational time.

PTO-driven implements draw power directly from the tractor’s power take-off shaft, offering reliable torque for demanding tillage tasks. These implements are cost-effective alternatives to fully motorized machinery. Therefore, PTO-driven options remain popular in mid-size farming operations across North America, Europe, and South Asia.

Manual/Animal-draft equipment continues to serve smallholder farmers in low-income rural regions of Sub-Saharan Africa and South Asia. These tools require minimal investment and no fuel. However, productivity limitations and labor intensity push farmers to transition toward motorized options as rural incomes and government support improve.

Crop Type Analysis

Cereals and Grains dominate with 44.8% due to their status as the world’s primary staple food crops.

In 2025, Cereals and Grains held a dominant market position in the By Crop Type segment of the Pre-Harvest Equipment Market, with a 44.8% share. Wheat, rice, corn, and barley drive massive equipment demand globally. Moreover, large planted acreages in Asia, North America, and Europe ensure consistent investment in seed drills, plows, and planters for grain production.

Oilseeds and Pulses represent a fast-growing segment driven by rising demand for edible oils, protein crops, and biofuels. Soybean and canola production in Brazil, Argentina, and Canada creates strong demand for specialized planters and sprayers. Consequently, equipment manufacturers develop purpose-built solutions for oilseed row-crop planting and cultivation systems.

Fruits and Vegetables require specialized pre-harvest equipment suited for raised-bed planting, inter-row cultivation, and precision spraying. The horticulture sector increasingly adopts compact and GPS-enabled equipment. Additionally, rising consumer demand for fresh produce worldwide encourages greater mechanization investment in this traditionally labor-intensive crop category.

Others include specialty crops, forage, sugar cane, and industrial crops. These segments use niche equipment configurations adapted to specific planting methods. Therefore, equipment makers serving these segments focus on modular and customizable machinery to address the highly varied requirements of specialty agriculture operations globally.

End User Analysis

Large-scale Farmers dominate with 38.7% due to their purchasing power and need for high-capacity mechanization solutions.

In 2025, Large-scale Farmers held a dominant market position in the By End User segment of the Pre-Harvest Equipment Market, with a 38.7% share. These operators manage extensive land holdings that demand high-capacity, technology-integrated machinery. Moreover, large farms typically have access to financing and subsidy programs that support premium equipment purchases.

Small and Medium Farmers represent the largest population segment globally but face affordability constraints. Rising equipment costs limit access to modern pre-harvest tools. However, government rental schemes, cooperative buying programs, and micro-financing initiatives increasingly help smaller operators access mechanized solutions in Asia and Africa.

Agricultural Contractors provide equipment services to farmers on a contract basis, enabling mechanization without direct ownership costs. This model grows in regions where individual farm sizes are too small to justify full equipment investment. Consequently, contractor fleets expand rapidly in India, Southeast Asia, and parts of Eastern Europe.

Cooperatives pool resources among multiple farmer members to collectively purchase and operate pre-harvest machinery. This model reduces per-unit equipment costs and improves overall farm productivity. Therefore, cooperative adoption of shared machinery is expanding in sub-Saharan Africa and Central Asia, supported by development agencies and government programs.

Key Market Segments

By Equipment Type

- Seed Drills

- Plows

- Harrows

- Cultivators

- Planters

- Sprayers

By Power Source

- Tractor-mounted

- Self-propelled

- PTO-driven Implements

- Manual/Animal-draft

By Crop Type

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Others

By End User

- Large-scale Farmers

- Small and Medium Farmers

- Agricultural Contractors

- Cooperatives

Emerging Trends

Autonomous Technology and Digital Innovation Reshape the Pre-Harvest Equipment Landscape

Major equipment manufacturers now focus on autonomous solutions for specialty crops like vineyards and orchards. Robotic platforms navigate complex row structures without human operators. Additionally, digital twin technology enables farmers to simulate crop growth and predict harvest timing, helping optimize planting decisions and equipment utilization well before field operations begin.

- Turkey recorded 63,546 tractor registrations in 2024, down 18% year over year. This significant decline signals a market correction phase, creating buyer-favorable conditions across established equipment markets. Consequently, manufacturers respond by accelerating innovation and offering more flexible financing to sustain demand during market downturns.

Brazil’s 2023/24 grain harvest fell by 23 million tonnes to 298 million tonnes, reducing agricultural machinery demand in that cycle. This highlights how crop output directly influences equipment purchasing decisions. Therefore, equipment makers increasingly align product launches and inventory strategies with regional harvest performance forecasts to manage exposure during weak agricultural seasons.

Drivers

Rising Food Demand and Technology Adoption Drive Pre-Harvest Equipment Market Growth

A growing global population creates rising pressure on food production systems worldwide. Farmers need to produce more food on the same or shrinking arable land. Consequently, the adoption of advanced pre-harvest equipment accelerates as mechanization becomes essential for maintaining yield targets and meeting food security goals set by governments and international bodies.

- Deere Production and Precision Agriculture net sales reached USD 3.163 billion, up 3% from USD 3.067 billion in Q1 FY2025. This growth reflects sustained demand for high-technology farm equipment despite market volatility. Moreover, companies adopting precision agriculture tools report measurable improvements in input efficiency and overall farm profitability.

Government subsidies and mechanization support programs further strengthen market demand. Countries across Asia, Africa, and Latin America actively fund equipment purchase schemes for rural farmers. Additionally, a broad shift toward data-driven precision agriculture encourages farmers to invest in smart seed drills, GPS-guided planters, and variable-rate sprayers to enhance both productivity and profitability.

Restraints

High Equipment Costs and Fragmented Land Holdings Limit Pre-Harvest Equipment Market Adoption

Advanced pre-harvest equipment carries high upfront costs that many small-scale farmers cannot afford. Modern seed drills, self-propelled sprayers, and precision planters require significant capital investment. Consequently, affordability barriers prevent widespread mechanization in low-income agricultural regions, particularly across Sub-Saharan Africa, South Asia, and parts of Southeast Asia.

- Brazil’s wholesale agricultural machinery sales fell to 48.9 thousand units in 2024, down 19.8% from 61.0 thousand units in 2023. This sharp decline reflects how weak harvest seasons and tight credit conditions directly reduce equipment purchasing power among farmers. The AMAZONE Group reported turnover of €763 million in FY2024, down 10.4% from the record €852 million in FY2023, confirming broader market softness.

Small and fragmented land holdings also complicate the adoption of large-scale machinery. Wide-body planters and high-capacity sprayers require minimum field sizes to operate efficiently. Therefore, farmers with plots under two hectares often find conventional mechanized equipment impractical and economically unviable without cooperative access arrangements or government-supported rental programs.

Growth Factors

Smart Farming Adoption and Expansion in Developing Regions Accelerate Market Growth

Smart farming practices, including automation, robotics, and IoT-connected machinery, create strong new growth avenues for equipment manufacturers. Farmers increasingly deploy sensor-equipped planters and autonomous sprayers that adjust operations in real time. Moreover, equipment companies investing in AI-integrated platforms report higher customer retention and recurring aftermarket revenue streams from software and data subscriptions.

- India produced 107,089 tractors in October 2025 alone, with total monthly sales of 173,635 units including exports. This demonstrates exceptional market scale in the Asia Pacific. Additionally, Kubota’s FY2025 Farm Equipment and Engines segment generated revenue of ¥2,003.307 billion, up 0.7% year over year, reflecting resilient demand in key Asia Pacific markets.

Developing regions in Africa, Southeast Asia, and South America offer significant untapped growth potential. Government mechanization programs, rural electrification, and expanding dealer networks lower equipment access barriers. Therefore, manufacturers expanding into these markets through local assembly partnerships and customized product lines position themselves to capture long-term growth as smallholder farm incomes rise steadily.

Regional Analysis

Asia Pacific Dominates the Pre-Harvest Equipment Market with a Market Share of 41.2%, Valued at USD 28.2 Billion

Asia Pacific leads the global pre-harvest equipment market, commanding a 41.2% share valued at USD 28.2 billion in 2025. Countries like India, China, and Japan drive this dominance through large farming populations and robust government mechanization programs. India’s tractor market remains one of the world’s most active, with monthly production volumes exceeding 100,000 units in peak seasons.

North America maintains a mature and technology-driven pre-harvest equipment market. Large commercial farms in the United States and Canada invest consistently in precision planters, GPS-guided seed drills, and high-capacity sprayers. However, recent data indicate retail tractor sales declined in 2024, reflecting inventory corrections and cautious buyer sentiment after years of elevated post-pandemic demand.

Europe represents a sophisticated market with strong demand for sustainable and high-efficiency pre-harvest solutions. Germany, France, and Italy lead regional equipment adoption among key agricultural producers. Additionally, tractor registrations across major European markets declined modestly in 2024, signaling a market normalization phase following previous years of above-average equipment investment cycles.

The Middle East and Africa region represents an emerging growth frontier for pre-harvest equipment suppliers. Food security concerns drive government investment in farm mechanization across GCC countries and Sub-Saharan Africa. Therefore, international manufacturers and development finance institutions actively support equipment access programs targeting smallholder farmers and cooperative farming organizations in this region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Deere and Company stands as the global leader in pre-harvest equipment, known for its John Deere-branded tractors, planters, and precision farming systems. The company invests heavily in digital agriculture platforms and autonomous equipment development. Its Production and Precision Agriculture segment demonstrates consistent revenue performance, supported by a broad dealer network spanning over 100 countries worldwide.

CNH Industrial N.V. operates leading agricultural equipment brands serving farmers across all major global markets. The company focuses on integrated smart farming solutions, connectivity tools, and sustainable machinery development. CNH’s Agriculture segment serves both large commercial operations and mid-size farms, leveraging global manufacturing and a diversified brand portfolio to address varied regional equipment requirements effectively.

Kubota Corporation holds a strong position in compact and mid-range pre-harvest equipment, particularly across the Asia Pacific and North America. Kubota’s Farm Equipment and Engines division delivers consistent revenue backed by loyal customer relationships and an expanding product lineup. The company continuously invests in precision agriculture technology and global dealer infrastructure to strengthen its international market presence further.

Mahindra and Mahindra Ltd dominates the Indian tractor market and maintains a growing international footprint in pre-harvest equipment. The company’s farm equipment division benefits from India’s large and expanding agricultural sector. Mahindra operates multiple large-scale manufacturing facilities across India and actively exports equipment to markets in Africa, Southeast Asia, and the Americas, broadening its global reach.

Top Key Players in the Market

- Deere and Company

- CNH Industrial N.V.

- BAGCO Corporation

- Kubota Corporation

- Mahindra and Mahindra Ltd

- CLAAS KGaA mbH

- Kuhn Group

- Yanmar Holdings Co., Ltd.

- Salford Group

- Amazon H. Dreyer GmbH

- Kinze Manufacturing

- Hardi International

- Máquinas Agrícolas Jacto S.A.

- LEMKEN GmbH

- TAFE

Recent Developments

- In 2025, Deere is expanding its See and Spray targeted spraying system to be compatible with small grains like wheat, barley, and canola for the 2027 model year. The second-generation system (Gen 2) features improved camera placement to reduce dust interference, a lighter design with fewer processors, and new four-wheel steering options for sprayers

- In 2025, CNH has designated India as its fifth standalone global region, underpinned by a strategy called India for India, India for Global. The company announced plans to debut a refreshed lineup of New Holland and Case IH equipment for the 2026 model year. Due to U.S. tariffs, these new models, along with current inventory, will see price increases, specifically in the North American market.

Report Scope

Report Features Description Market Value (2025) USD 68.8 Billion Forecast Revenue (2035) USD 124.4 Billion CAGR (2026-2035) 6.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Equipment Type (Seed Drills, Plows, Harrows, Cultivators, Planters, Sprayers), By Power Source (Tractor-mounted, Self-propelled, PTO-driven Implements, Manual/Animal-draft), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Others), By End User (Large-scale Farmers, Small and Medium Farmers, Agricultural Contractors, Cooperatives) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Deere and Company, CNH Industrial N.V., BAGCO Corporation, Kubota Corporation, Mahindra and Mahindra Ltd, CLAAS KGaA mbH, Kuhn Group, Yanmar Holdings Co., Ltd., Salford Group, Amazone H. Dreyer GmbH, Kinze Manufacturing, Hardi International, Maquinas Agricolas Jacto S.A., LEMKEN GmbH, TAFE Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Pre-Harvest Equipment MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Pre-Harvest Equipment MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Deere and Company

- CNH Industrial N.V.

- BAGCO Corporation

- Kubota Corporation

- Mahindra and Mahindra Ltd

- CLAAS KGaA mbH

- Kuhn Group

- Yanmar Holdings Co., Ltd.

- Salford Group

- Amazon H. Dreyer GmbH

- Kinze Manufacturing

- Hardi International

- Máquinas Agrícolas Jacto S.A.

- LEMKEN GmbH

- TAFE

Our Clients

- 181151

- March 2026