Quick Navigation

- Report Overview

- Key Takeaways

- Analysts’ Viewpoint

- China Power Amplifier Market

- Analyst’s Viewpoint

- Product Analysis

- Class Analysis

- Technology Analysis

- Vertical Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Top Opportunities for Players

- Recent Developments

- Report Scope

Report Overview

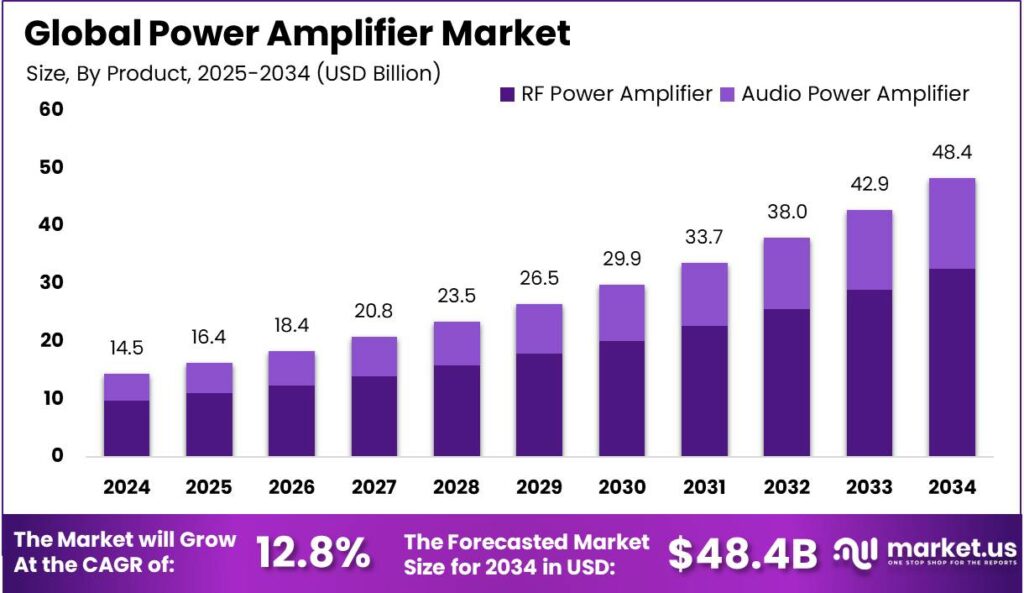

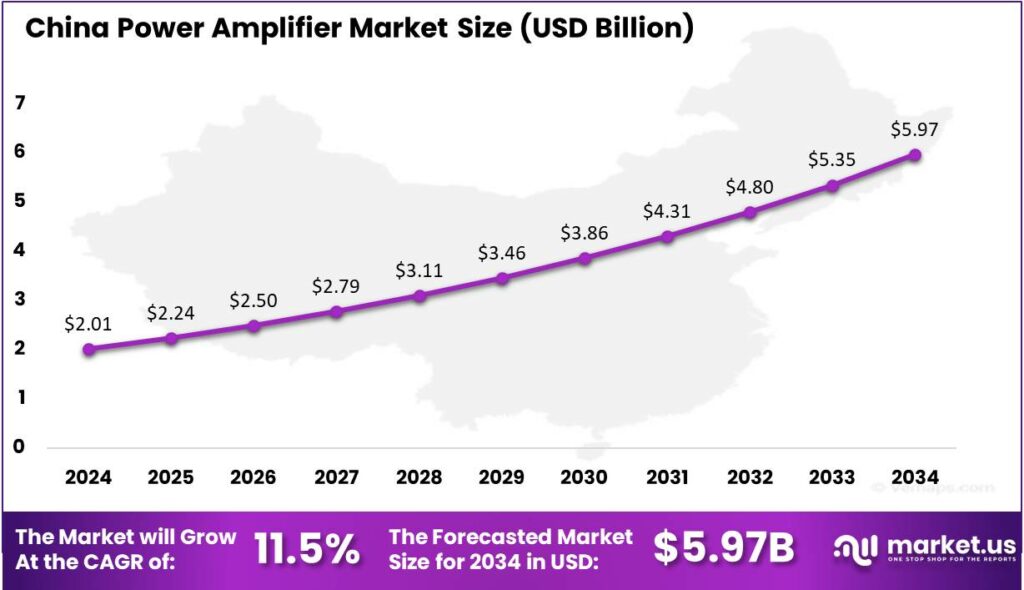

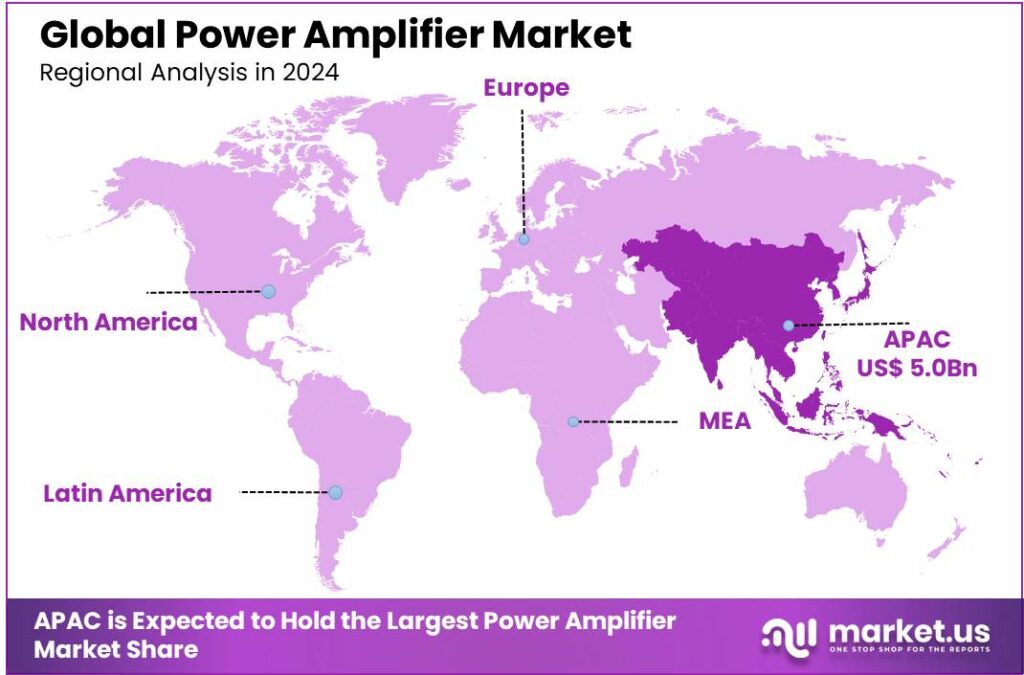

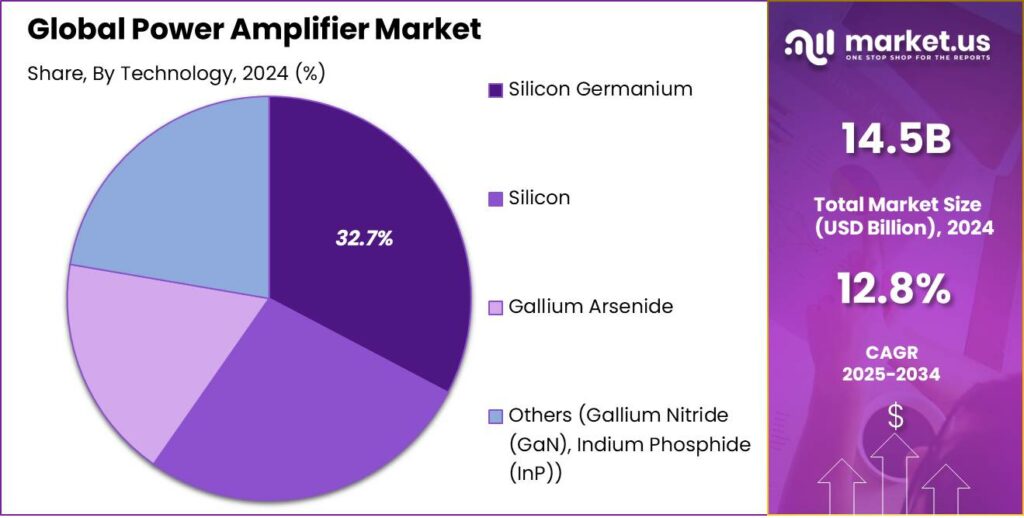

The Global Power Amplifier Market size is expected to be worth around USD 48.4 Billion By 2034, from USD 14.5 Billion in 2024, growing at a CAGR of 12.80% during the forecast period from 2025 to 2034. In 2024, the Asia-Pacific region dominated the global power amplifier market with over 34.8% market share, translating to approximately USD 5.0 bn in revenue. The power amplifier market in China was valued at USD 2.01 bn, with a projected CAGR of 11.5%.

The market for power amplifiers plays a critical role in various industries, ranging from telecommunications to automotive and consumer electronics. These devices are essential for amplifying electrical signals to drive loads and achieve higher output power in applications such as wireless communications and audio systems.

The growth of the power amplifier market is primarily fueled by the expanding adoption of new technologies such as machine-to-machine (M2M) communication and the Internet of Things (IoT). These technologies demand high power output for efficient data transmission, thus propelling the demand for advanced power amplifiers.

Advanced materials like gallium nitride (GaN) and silicon carbide (SiC) are increasingly being adopted in the manufacturing of power amplifiers due to their superior performance characteristics, which include higher power densities and greater efficiency. These materials are particularly vital in applications demanding high power efficiency and compactness, such as in electric vehicles and renewable energy systems.

The demand for power amplifiers is strong, driven by the growing telecommunications sector and the rise of smart devices. The push for 5G technology and better connectivity solutions has highlighted the need for advanced power amplifiers. Additionally, the growing popularity of high-fidelity audio systems has further boosted demand in the audio equipment market.

The rise of high-quality audio systems in consumer electronics drives advancements in PA technology. The automotive sector also fuels market growth as vehicles adopt advanced infotainment systems. Additionally, improvements in efficiency and integration capabilities support market expansion across various applications, from military to personal electronics.

Key benefits of power amplifiers include improved signal quality and extended transmission range, essential for modern communication infrastructures. They also elevate audio experiences with superior sound quality. Moreover, advancements in design and technology have led to more energy-efficient amplifiers, aiding industries in meeting sustainability goals by reducing energy consumption and heat generation.

Key Takeaways

- The Global Power Amplifier Market size is expected to reach USD 48.4 Billion by 2034, growing from USD 14.5 Billion in 2024, with a CAGR of 12.80% during the forecast period from 2025 to 2034.

- In 2024, the RF Power Amplifier segment held a dominant market position, capturing more than 67.6% of the global market share.

- In 2024, the Class A segment held a dominant position within the power amplifier market, capturing more than 28.7% of the market share.

- In 2024, the Silicon Germanium (SiGe) segment held a dominant position in the power amplifier market, capturing more than 32.7% of the market share.

- In 2024, the Consumer Electronics segment dominated the Power Amplifier Market, capturing more than 38.4% of the market share.

- In 2024, the Asia-Pacific region held a dominant position in the global power amplifier market, capturing more than 34.8% of the market share, which translated to approximately USD 5.0 billion in revenue.

- In 2024, the market for power amplifiers in China was estimated at USD 2.01 billion and is projected to grow at a CAGR of 11.5%.

Analysts’ Viewpoint

Significant investment opportunities lie in developing innovative power amplifier solutions tailored for emerging applications like 5G technology, where there is a need for amplifiers that can operate at higher frequencies and support increased data rates.

There is a trend towards the integration of power amplifiers with other semiconductor components to form more compact and efficient modules. This integration is particularly prevalent in mobile and communication applications, driving the market towards more integrated solutions.

For businesses, investing in advanced power amplifier technologies can lead to benefits such as reduced operational costs, enhanced product performance, and the ability to meet diverse customer needs effectively. These advantages are critical for maintaining competitiveness in the fast-evolving tech landscape.

The regulatory environment for power amplifiers is increasingly focusing on energy efficiency and environmental impact. This has led to tighter controls and standards that manufacturers must comply with, influencing the design and functionality of new power amplifiers.

China Power Amplifier Market

In 2024, the market for power amplifiers in China was estimated to be valued at USD 2.01 billion. It is projected to grow at a compound annual growth rate (CAGR) of 11.5%. The significant growth in the power amplifier market in China can be attributed to several factors.

The increasing demand for high-performance audio devices and wireless communication systems plays a crucial role in this expansion. Advancements in technology and the growing adoption of 4G and 5G networks have increased the demand for power amplifiers that offer higher efficiency and better performance in telecommunications.

Furthermore, the expansion of the consumer electronics sector in China, including smartphones, tablets, and home entertainment systems, is also driving the market. The integration of power amplifiers is crucial for improving audio outputs and connectivity in devices. With the Chinese government’s supportive policies and initiatives to boost technological innovations in electronics manufacturing, the power amplifier market is expected to continue its strong growth in the coming years.

In 2024, the Asia-Pacific region held a dominant position in the global power amplifier market, capturing more than 34.8% of the market share, which translated to approximately USD 5.0 billion in revenue. This leadership can be attributed to several pivotal factors that are unique to the Asia-Pacific area.

Asia-Pacific’s dominance in the power amplifier market is driven by strong manufacturing capabilities and the presence of key industry players in China, South Korea, and Japan. These countries lead in consumer electronics, telecommunications, and technological innovation, with the expansion of 5G networks boosting demand for advanced power amplifiers for high-speed data transmission.

Moreover, the Asia-Pacific market benefits from the increasing consumption of electronic devices such as smartphones, tablets, and smart home devices among its vast population. The growth in these consumer electronics directly boosts the power amplifier market, as these devices require efficient and high-quality signal amplification to deliver enhanced audio and connectivity features.

Government initiatives in the Asia-Pacific region promoting industrial growth and technological advancement have bolstered the power amplifier market. These policies encourage R&D, attract foreign investments, and support the expansion of manufacturing facilities, driving the growth of the power amplifier industry in the region.

Analyst’s Viewpoint

The power amplifier market is set for strong growth, fueled by rising demand for high-quality audio in consumer electronics, the global shift to 5G technology, and advancements in automotive entertainment systems. These sectors are driving the need for more sophisticated amplification solutions.

The power amplifier market faces challenges such as regulatory hurdles on electromagnetic interference and safety standards, intense competition driving pricing pressures, and the technological challenge of creating efficient amplifiers that meet modern power and frequency demands while minimizing energy use and heat.

Innovations like Class-D and Class-G amplification are boosting efficiency and reducing heat, popular in consumer electronics and audio systems. Gallium Nitride (GaN) is enhancing performance in high-frequency applications like satellite communications, while smart, IoT-enabled amplifiers are optimizing performance and energy use.

Product Analysis

In 2024, the RF Power Amplifier segment held a dominant market position, capturing more than a 67.6% share of the global market. This dominance is primarily driven by the extensive application of RF power amplifiers in diverse industries, including telecommunications, military, and broadcasting.

The RF Power Amplifier segment is mainly driven by Traveling-Wave Tube Amplifiers (TWTA) and Solid State Power Amplifiers (SSPA). TWTA is crucial for high power and broadband applications like satellite communications and radar systems, thanks to its efficiency at high frequencies and reliability in performance.

SSPAs are gaining momentum due to their reliability, efficiency, and compact size, making them ideal for applications like terrestrial broadband and space communications. The shift to solid-state technology in traditional TWTA applications is driven by SSPAs’ superior power efficiency and lower operational costs, fueling growth in this segment.

Advancements in technology that enhance power output, efficiency, and heat dissipation reinforce the market leadership of the RF Power Amplifier segment. These improvements are vital for meeting the demands of modern communication and broadcasting systems, supporting the segment’s continued growth.

Class Analysis

In 2024, the Class A segment held a dominant market position within the power amplifier market, capturing more than a 28.7% share. Class A amplifiers are highly regarded for their ability to deliver superior sound quality due to their linear amplification characteristics and minimal signal distortion.

The predominance of Class A amplifiers also stems from their simplicity in design, which appeals to both manufacturers and audiophiles. Unlike more complex designs, Class A amplifiers operate with their output transistors always in the “on” state, which eliminates crossover distortion and ensures a purer waveform reproduction.

Despite their superior sound quality, Class A amplifiers are less energy-efficient than other types, like Class D, due to higher power consumption and heat generation. While this can be a drawback for portable or battery-powered applications, Class A amplifiers maintain a strong market share in settings where audio quality is prioritized over power efficiency.

Class A amplifiers enjoy a strong, niche demand, especially in markets where audio performance is prioritized over energy efficiency. The ongoing commitment to high-quality audio output drives their market dominance. Despite operational and efficiency challenges, the Class A segment maintains leadership in the power amplifier market, thanks to its superior sound fidelity and design simplicity.

Technology Analysis

In 2024, the Silicon Germanium (SiGe) segment held a dominant position in the power amplifier market, capturing more than a 32.7% share. This prominence can be attributed to several strategic advantages that SiGe offers over other semiconductor materials.

SiGe power amplifiers are highly favored in applications requiring high-frequency performance combined with low power consumption. The inherent properties of SiGe allow for better performance at high frequencies, making it ideal for wireless communications and radar applications. Its capacity to operate efficiently in these critical applications underpins the significant market share it holds.

The integration of SiGe technology boosts the efficiency of power amplifiers by reducing noise figures and improving linearity, which are essential for high-performance telecommunications infrastructure. As demand for better data transmission quality grows, SiGe-based power amplifiers have seen increased adoption.

The manufacturing process for SiGe components aligns with existing silicon-based fabrication technologies, enabling cost-effective production without significant investments in new equipment. This economic advantage has driven widespread adoption and fueled the growth of the SiGe segment in the power amplifier market.

Vertical Analysis

In 2024, the Consumer Electronics segment held a dominant position in the Power Amplifier Market, capturing more than a 38.4% share. This segment’s leadership is primarily attributed to the widespread adoption of consumer electronics devices such as smartphones, tablets, and home entertainment systems, which extensively utilize power amplifiers to enhance audio and signal quality.

The rise of IoT and connected devices has greatly expanded the Consumer Electronics segment. As manufacturers incorporate advanced communication features into everyday devices, the demand for power amplifiers that support these capabilities has increased. This trend is expected to continue, further strengthening the segment’s market dominance.

Technological advancements in wireless technologies and the rollout of 5G networks have driven a surge in demand for power amplifiers that are more efficient, compact, and capable of handling higher frequencies. This need is especially prominent in the consumer electronics sector, where improving device connectivity and performance is a key priority.

The market dynamics of the Consumer Electronics segment are influenced by consumer preferences for portable and high-performance electronics. The increasing consumer spending on audio and visual entertainment products is directly boosting the need for power amplifiers, thus driving the segment’s growth.

Key Market Segments

By Product

- Audio Power Amplifier

- RF Power Amplifier

- Traveling-Wave Tube Amplifier (TWTA)

- Solid State Power Amplifier (SSPA)

By Class

- Class A

- Class B

- Class AB

- Class C

- Class D

- Others (G, H, DG, K)

By Technology

- Silicon

- Silicon Germanium

- Gallium Arsenide

- Others (Gallium Nitride (GaN), Indium Phosphide (InP))

By Vertical

- Consumer Electronics

- Industrial

- Telecommunication

- Automotive

- Military & Defense

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Increasing Demand for Wireless Communication

The growing demand for wireless communication technologies drives the power amplifier market. Devices like smartphones, tablets, and laptops rely on robust wireless connectivity, with power amplifiers playing a key role in boosting signal strength and ensuring reliable data transmission.

The proliferation of technologies like 4G and the ongoing deployment of 5G networks further amplify this demand. 5G technology, in particular, promises ultra-fast data speeds and low latency, enabling applications such as autonomous vehicles, augmented reality, and the Internet of Things (IoT).

These advancements require sophisticated power amplifiers capable of operating at higher frequencies and delivering greater efficiency. Consequently, manufacturers are investing in research and development to produce power amplifiers that meet these evolving requirements, thereby fueling market growth.

Restraint

High Production Costs

Despite the positive growth trajectory, the power amplifier market faces the significant restraint of high production costs. Developing advanced power amplifiers involves substantial investment in research and development, sophisticated manufacturing processes, and the use of high-quality materials.

These factors contribute to elevated production expenses, which can lead to higher prices for end-users and potentially limit market adoption. The complexity of designing power amplifiers for modern applications increases development costs and time-to-market. Manufacturers must navigate these financial challenges while delivering cost-effective solutions that do not compromise on performance or reliability.

Opportunity

Expansion of Electric Vehicles (EVs)

The burgeoning electric vehicle market presents a substantial opportunity for the power amplifier industry. EVs rely heavily on electronic components for various functions, including powertrain control, infotainment systems, and advanced driver-assistance systems (ADAS).

Power amplifiers play a crucial role in these applications by ensuring efficient power management and signal amplification. As the global push towards sustainable transportation intensifies, the demand for EVs is expected to rise significantly.

This trend offers power amplifier manufacturers the chance to develop specialized products tailored to automotive applications, focusing on factors such as power efficiency, compactness, and thermal management. By aligning product development strategies with the specific needs of the EV sector, companies can tap into this growing market segment and drive revenue growth.

Challenge

Heat Dissipation in High-Power Applications

Effective heat dissipation remains a critical challenge in the design and operation of high-power amplifiers. These devices generate substantial amounts of heat during operation, and inadequate thermal management can lead to performance degradation, reduced lifespan, and even device failure.

In continuous or high-power applications like telecommunications and industrial equipment, effective heat management is essential. Engineers must design amplifiers with efficient cooling systems, choose materials with high thermal conductivity, and employ innovative circuit designs to reduce heat-related issues. Addressing these thermal challenges is essential to ensure the reliability and longevity of power amplifiers in demanding applications.

Emerging Trends

A key trend is the development of high-frequency, high-efficiency, and high-linearity power amplifiers, driven by the demand for better performance in modern applications. Envelope tracking, which adjusts the power supply voltage to maintain peak efficiency during transmission, is an emerging technique to further enhance efficiency.

Another notable advancement is the integration of Gallium Nitride (GaN) technology into Monolithic Microwave Integrated Circuit (MMIC) power amplifiers. GaN’s superior efficiency and frequency response make it ideal for high-power and high-frequency applications, leading to its increased adoption in telecommunications, aerospace, and defense sectors.

The rise of Class-D amplifiers is also noteworthy. These amplifiers offer higher efficiency compared to traditional analog amplifiers by operating their output stages as electronic switches rather than linear gain devices. This efficiency makes them particularly suitable for portable and battery-powered devices.

Business Benefits

Power amplifiers offer key business benefits by enhancing sound quality. They efficiently handle high currents and voltages separately from delicate pre-amplification functions, reducing signal path lengths. This design allows for the use of larger amplifier modules, which boosts audio clarity, dynamics, and power handling capabilities, leading to superior performance in audio systems.

Power amplifiers are versatile tools used across a wide range of industries including telecommunications, broadcasting, and medical equipment. Power amplifiers are crucial for robust signal amplification in applications like driving loudspeakers, transmitting broadcast signals, and powering medical devices such as MRI and ultrasound machines.

A dedicated unit for power amplification improves component quality, handling more power and heat without impacting other electronics. This separation boosts component longevity, ensuring sustained performance and potentially lowering long-term costs by reducing replacements and repairs.

Key Player Analysis

The key players in the power amplifier market dominate due to their technological advancements, global presence, and strong product portfolios.

Infineon Technologies stands as one of the top players in the power amplifier market, providing innovative solutions in the field of power management. The company’s power amplifiers are widely used in automotive, industrial, and communication sectors. Infineon is known for its strong focus on energy efficiency and high performance, providing products that meet the growing demand for greener solutions.

Texas Instruments (TI) is another prominent player in the power amplifier space, offering a diverse range of products catering to both consumer and industrial sectors. TI’s power amplifiers are known for their precision, efficiency, and high-performance capabilities, serving key applications in wireless communication, audio equipment, and automotive systems.

Broadcom is a significant contributor to the power amplifier market, providing solutions that are central to wireless communication systems. The company’s power amplifiers are widely used in mobile devices, networking equipment, and broadband infrastructure.

Top Key Players in the Market

- Infineon Technologies

- Texas Instruments

- Broadcom

- Toshiba

- STMicroelectronics

- Maxim Integrated

- Yamaha

- Qorvo

- NXP Semiconductors

- Analog Devices

- Skyworks

- QSC Audio Products

- Peavey Electronics

- Qualcomm

- Macom

- Bonn Elektronik

- Renesas Electronics

- ETL System

- Ophir RF

- Others

Top Opportunities for Players

The power amplifier market is poised for substantial growth, driven by several emerging opportunities across various industries.

- Internet of Things (IoT) Devices: The proliferation of IoT devices, which are expected to exceed 29 billion units by 2027, represents a significant driver for the power amplifier market. These devices often require low-power, battery-powered amplifiers capable of operating across various frequency bands, essential for wireless connectivity and data exchange in IoT ecosystems.

- Wearable Technology: The demand for wearable devices is on the rise, with an expected market reach of 520 million units in 2023. Power amplifiers in this segment need to be highly efficient, small, and consume minimal power to be viable for health and fitness tracking, remote patient monitoring, and personal productivity applications.

- Electric Vehicles and Renewable Energy Systems: Emerging applications in electric vehicles (EVs) and renewable energy systems present significant growth opportunities. Power amplifiers in these sectors are crucial for motor drives, battery management, and efficient energy conversion, demanding high efficiency and compact designs to meet the specific needs of these industries.

- Expansion in 5G Infrastructure: The ongoing rollout and expansion of 5G networks are crucial for the power amplifier market. These networks require advanced power amplifiers that support higher data rates and improved coverage, driving demand particularly in telecommunications and wireless networks.

- Consumer Electronics: The market for consumer electronics continues to demand high-quality audio and video experiences, which are reliant on advanced power amplifiers. This segment includes applications such as soundbars, home theaters, and portable speakers, where power amplifiers play a vital role in delivering enhanced audio fidelity.

Recent Developments

- In January 2024, Qorvo reached a definitive agreement to acquire Anokiwave, a supplier of high-performance silicon integrated circuits for intelligent active array antennas used in defense, SATCOM, and 5G applications.

- In June 2024, Analog Devices released the ADPA1116, a gallium nitride (GaN) power amplifier operating across 0.3 GHz to 6 GHz, enhancing RF and microwave applications.

- In September 2024, MACOM highlighted its diverse product offerings, including a 300W X-band GaN-on-SiC matched power amplifier suitable for pulsed radar applications such as marine, defense and weather radar.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 14.5 Bn |

| Forecast Revenue (2034) | USD 48.4 Bn |

| CAGR (2025-2034) | 12.80% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Product (Audio Power Amplifier, RF Power Amplifier (Traveling-Wave Tube Amplifier (TWTA), Solid State Power Amplifier (SSPA)), By Class (Class A, Class B, Class AB, Class C, Class D, Others (G, H, DG, K)), By Technology (Silicon, Silicon Germanium, Gallium Arsenide, Others (Gallium Nitride (GaN), Indium Phosphide (InP))), By Vertical (Consumer Electronics, Industrial, Telecommunication, Automotive, Military & Defense, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Infineon Technologies, Texas Instruments, Broadcom, Toshiba, STMicroelectronics, Maxim Integrated, Yamaha, Qorvo, NXP Semiconductors, Analog Devices , Skyworks, QSC Audio Products, Peavey Electronics, Qualcomm, Macom, Bonn Elektronik, Renesas Electronics, ETL System, Ophir RF, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |