Quick Navigation

- Report Overview

- Key Takeaways

- Analysts’ Viewpoint

- China Rigid Flex Pcb Market

- Product Type Analysis

- Layer Count Analysis

- Flexibility Type Analysis

- Materials Analysis

- End-Use Industry Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Emerging Trends

- Business Benefits

- Key Regions and Countries

- Key Player Analysis

- Top Opportunities for Players

- Recent Developments

- Report Scope

Report Overview

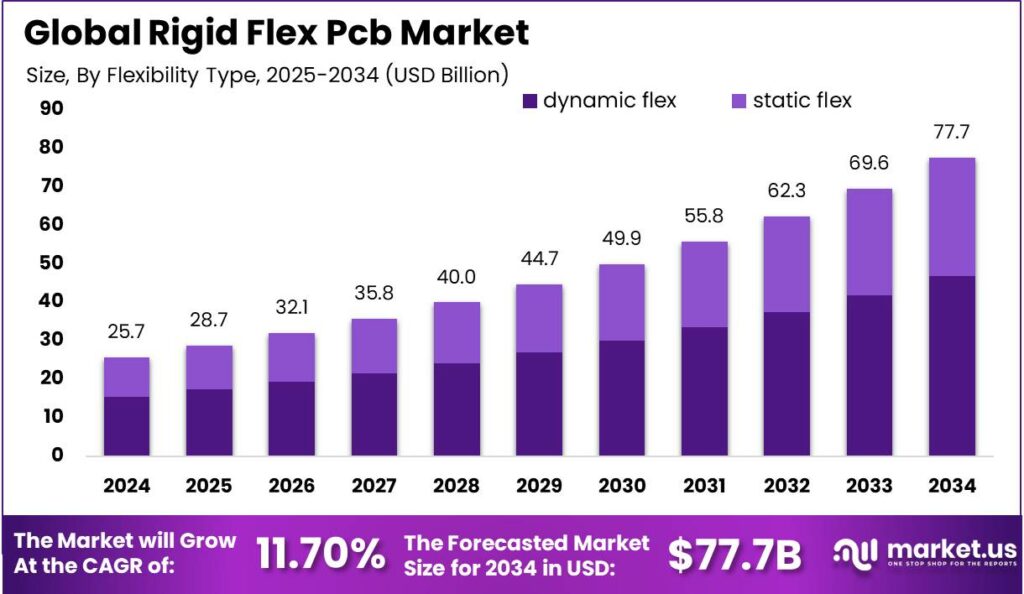

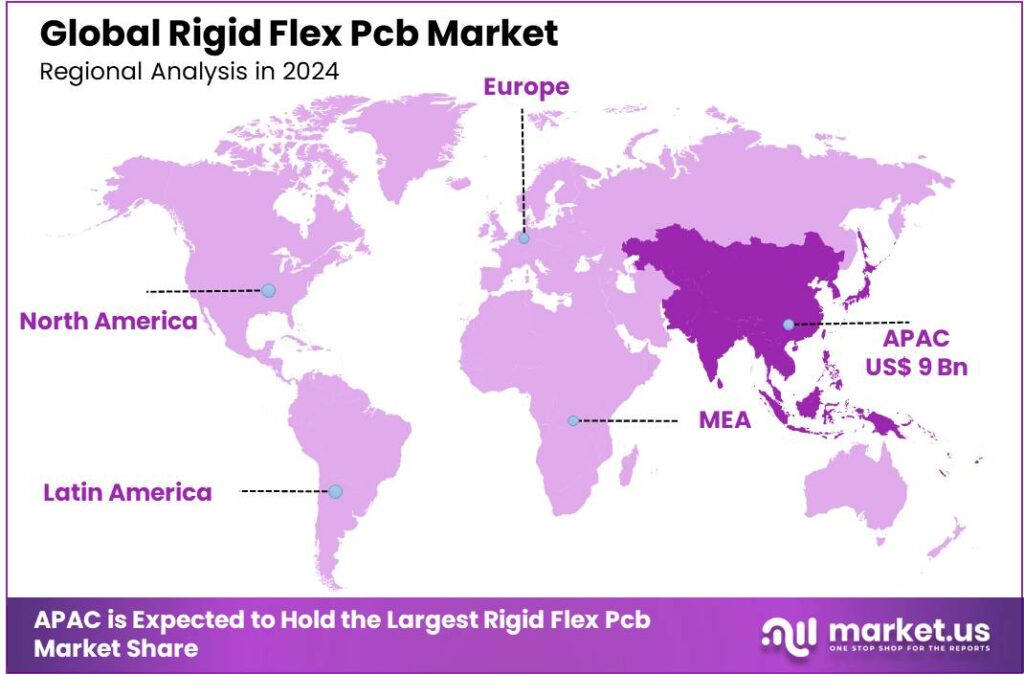

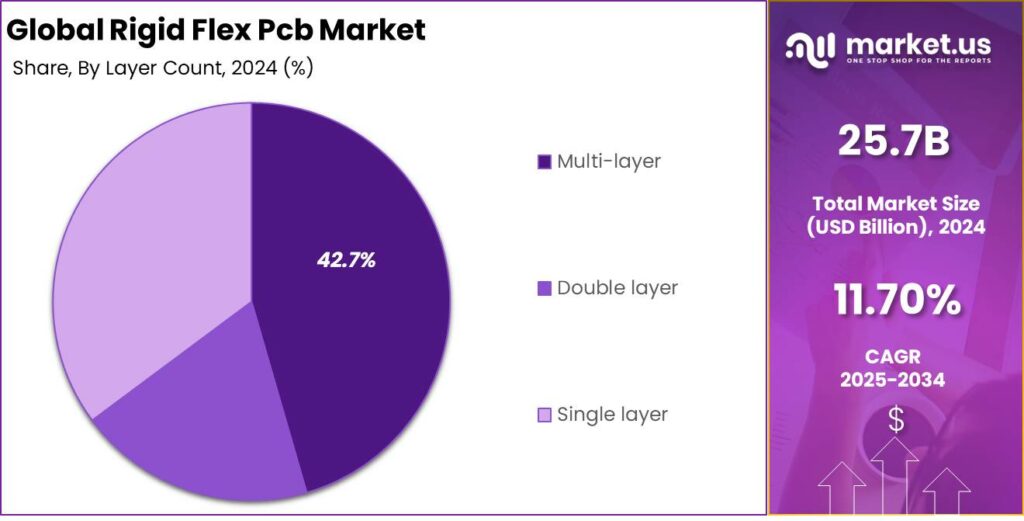

The Global Rigid Flex PCB Market size is expected to be worth around USD 77.7 Billion By 2034, from USD 25.7 Billion in 2024, growing at a CAGR of 11.70% during the forecast period from 2025 to 2034. In 2024, the Asia-Pacific region dominated the rigid flex PCB market, accounting for more than 35.3% of the global market, translating to approximately USD 9 billion in revenue.

The Rigid Flex PCB market is expanding, driven by the demand for more compact and reliable electronics across various sectors including automotive, aerospace, consumer electronics, and medical devices. The unique properties of Rigid Flex PCBs, such as their ability to reduce spatial constraints and improve reliability by minimizing interconnects, make them increasingly favorable in high-density and high-reliability applications.

Key drivers of the Rigid Flex PCB market include the ongoing miniaturization of electronic devices, increased need for durable and reliable electronics in harsh environments, and the growing trend towards sophisticated wearable technology. Automation and AI integration in various industries also push forward the demand for this versatile technology, as it can be designed to fit irregular shapes and automate assembly processes, thereby reducing costs and improving efficiency.

The demand for Rigid Flex PCBs is robust, attributed to their critical role in enabling modern high-tech applications. Industries such as aerospace, automotive, and healthcare rely heavily on these PCBs for applications that require high reliability under dynamic conditions, including vibration and thermal cycling.

Adopting Rigid Flex PCB technology brings several business benefits, including reduced assembly costs, enhanced reliability, and improved design flexibility. These PCBs reduce the need for additional connectors and wiring harnesses, which not only cuts down on material costs but also on labor. Their high reliability decreases maintenance and warranty costs, leading to improved customer satisfaction and reduced service expenses.

Rigid flex PCBs have gained popularity as manufacturers recognize their benefits in terms of design freedom, reliability, and performance in harsh environments. Their ability to reduce the assembly time and enhance the durability of electronic products also adds to their appeal, making them a popular choice across various industries.

In some regions, government initiatives aimed at boosting the local electronics manufacturing sector have led to increased investments in advanced PCB technologies, including rigid flex PCBs. These investments often come in the form of grants, tax incentives, or public-private partnerships, aimed at fostering innovation and technological advancement.

The market is poised for expansion, with technological advancements driving growth. As electronic devices continue to evolve towards more integrated and compact designs, the role of rigid flex PCBs becomes more critical. The push for sustainable electronics production will likely drive future market developments, aligning with global sustainability goals.

Key Takeaways

- The Global Rigid Flex PCB Market is projected to reach USD 77.7 Billion by 2034, up from USD 25.7 Billion in 2024, reflecting a CAGR of 11.70% from 2025 to 2034.

- In 2024, the Multi-layer flex segment held a dominant market position, accounting for more than 30.7% of the global market.

- The multi-layer segment in the rigid flex PCB market maintained a dominant position in 2024, with a market share exceeding 42.7%.

- The dynamic flex segment led the market in 2024, capturing more than 60.3% of the rigid flex PCB market.

- The FR4 segment dominated the rigid flex PCB market in 2024, commanding a share of over 33.4%.

- The Automotive segment held a dominant position in the rigid flex PCB market in 2024, with a share exceeding 28.7%.

- In 2024, the Asia-Pacific region dominated the rigid flex PCB market, accounting for more than 35.3% of the global market, translating to approximately USD 9 billion in revenue.

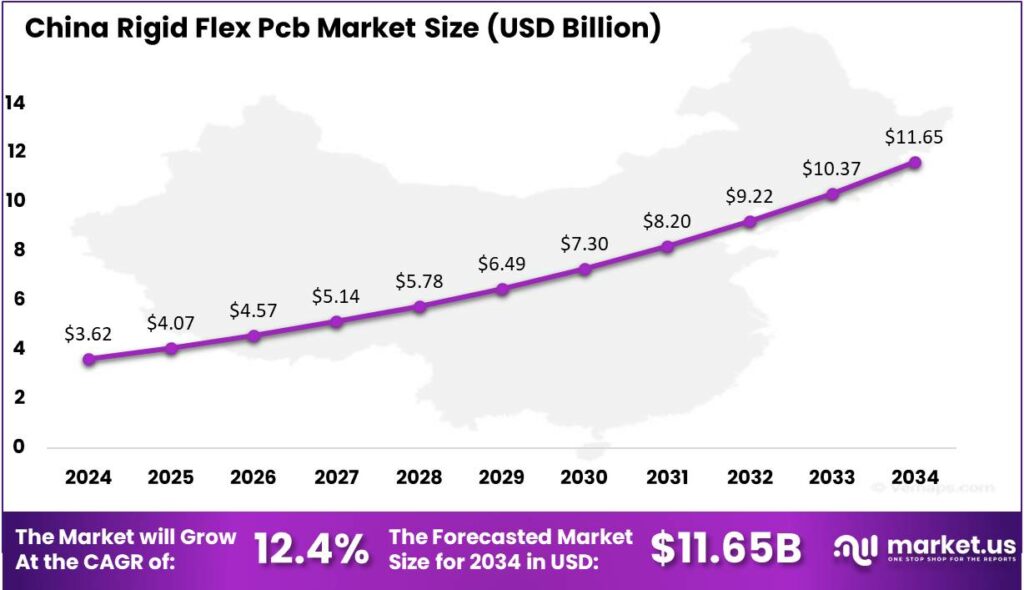

- In 2024, the market for rigid flex PCBs in China was valued at USD 3.62 billion and is projected to grow at a CAGR of 12.4%.

Analysts’ Viewpoint

From an investment perspective, the Rigid Flex PCB market presents numerous opportunities due to its expanding application base and the technological advancements driving its adoption. Analysts highlight the importance of partnering with manufacturers who can navigate the complexities of Rigid Flex PCB design and production to leverage these opportunities fully.

Regulatory environments focusing on sustainability and advancements in green technology are also influencing the market, suggesting a shift towards more environmentally friendly manufacturing processes and materials.

Moreover, as industries continue to demand more sophisticated electronic solutions, the technological advancements in Rigid Flex PCB manufacturing are expected to keep pace, offering significant investment opportunities in the near future.

China Rigid Flex Pcb Market

In 2024, the market for rigid flex PCBs in China was valued at USD 3.62 billion. It is projected to grow at a compound annual growth rate (CAGR) of 12.4%. Rigid-flex PCBs blend the benefits of rigid and flexible circuit boards, offering improved reliability and versatility, especially in space- and weight-sensitive electronic applications.

The growth of this market in China can be attributed to increasing demands in sectors such as consumer electronics, automotive, and healthcare, where technological advancements are continuously evolving. China’s prominent role in electronic manufacturing, coupled with its technological innovation, supports the expansion of the rigid flex PCB market.

Moreover, government initiatives aimed at boosting the domestic production capabilities of high-tech components have positively impacted the market. Investments in 5G and smart infrastructure are boosting the demand for advanced components like rigid-flex PCBs. As industries adopt more compact designs, China’s rigid-flex PCB market is poised for significant growth, driven by technological advancements and supportive policies.

In 2024, Asia-Pacific held a dominant market position in the rigid flex PCB market, capturing more than a 35.3% share, which translated into revenue of approximately USD 9 billion. The region’s market leadership is driven by its strong electronics manufacturing sector and growing adoption of advanced technologies across industries.

Asia-Pacific dominates the rigid-flex PCB market due to its leading electronics manufacturing countries, including China, South Korea, and Taiwan. These nations’ large-scale production facilities for consumer electronics, automotive components, and high-tech products drive the demand for rigid-flex PCBs, positioning the region as a market leader.

Government policies in the region, such as China’s “Made in China 2025” plan and South Korea’s semiconductor investments, are driving the growth of high-tech industries. These initiatives enhance the production of advanced electronic components, including rigid-flex PCBs, boosting the region’s manufacturing capacity.

The growing demand for wearable tech, smart devices, and IoT products in Asia-Pacific is driving the rigid-flex PCB market. These devices require the durability and flexibility of rigid-flex PCBs. With the expansion of consumer electronics and trends toward miniaturization, the market is set for significant growth, supported by strong infrastructure and future opportunities.

Product Type Analysis

In 2024, the Multi-layer flex segment held a dominant market position, capturing more than a 30.7% share of the global market. The multi-layer flex segment leads due to its superior functionality in complex devices, offering enhanced connectivity, higher circuit density, and greater flexibility than single-sided and double-sided circuits.

Single-sided and double-sided flex PCBs are key market segments. Single-sided flex PCBs are cost-effective for simpler applications, while double-sided flex PCBs offer a balance of flexibility and connectivity for moderate complexity. However, they lack the circuit density and miniaturization potential of multi-layer flex PCBs, limiting their use in advanced technologies.

The Multilayer PCB and Quick Turn Rigid Flex PCB segments serve niche but essential markets. Multilayer PCBs, with multiple rigid layers and flexible interconnections, are key for high-performance applications requiring strong structural integrity and complex circuits, particularly in high-speed data transmission and high-frequency operations.

Quick turn rigid-flex PCBs cater to urgent development needs with rapid prototyping and fast production cycles. Valued in industries like automotive and consumer electronics, this segment is smaller due to its time-sensitive market demand.

Layer Count Analysis

In 2024, the multi-layer segment of the rigid flex PCB market held a dominant position, capturing more than a 42.7% share. This segment’s leadership is largely attributable to its critical role in complex electronic applications where multiple circuit connections are necessary within a constrained space.

The demand for multi-layer rigid-flex PCBs is driven by their enhanced reliability and connectivity, making them ideal for high-speed data transmission. Their durability and flexibility also make them suitable for harsh environments, expanding their use in military and aerospace sectors where reliability is crucial.

The rise of multi-layer rigid-flex PCBs is driven by advancements in electronic technology, which require more components on a single chip. As devices become smarter and more integrated, these PCBs support complex functions while maintaining a compact size, aligning with the trend toward more efficient and compact devices.

Furthermore, the production processes for multi-layer rigid flex PCBs have seen significant improvements, reducing costs and enhancing production efficiency. Innovations in manufacturing technologies have made it more feasible for companies to produce complex multi-layer designs at a larger scale, thereby meeting the growing market demand.

Flexibility Type Analysis

In 2024, the dynamic flex segment held a dominant market position in the rigid flex PCB market, capturing more than a 60.3% share. This segment’s leadership is primarily driven by its extensive application in industries where durability and repeated movement are crucial.

Dynamic flex PCBs are designed to withstand constant and repetitive motion, making them ideal for use in sectors such as consumer electronics, automotive, and industrial machinery. For instance, in consumer electronics, these PCBs are essential for products that require frequent flexing or bending, like foldable smartphones and laptops.

Furthermore, the automotive industry heavily relies on dynamic flex PCBs due to their ability to resist vibrations and thermal stress. As vehicles become more advanced, the integration of electronic components increases, necessitating the use of dynamic flex PCBs for connections that require movement or are subject to harsh environments.

The trend toward miniaturization in electronics demands more compact solutions, with dynamic flex PCBs playing a vital role. Their ability to fit into small spaces while ensuring strong performance drives their demand. As technology advances, the dynamic flex PCB segment is set to remain a market leader due to its essential role in modern electronics.

Materials Analysis

In 2024, the FR4 segment held a dominant market position in the rigid flex PCB market, capturing more than a 33.4% share. This leadership can be attributed to FR4’s comprehensive set of properties, including high dielectric strength, thermal resistance, and mechanical durability, making it highly suitable for a broad range of applications in electronics.

The robustness of FR4 in diverse environmental conditions also contributes to its leading status in the market. It demonstrates excellent performance in both high and low temperature environments, which is crucial for the reliability of electronic devices across various industries, including automotive, aerospace, and consumer electronics.

The global electronics industry’s growth has increased demand for FR4 materials. As devices become more compact and integrated, the need for reliable PCB materials has risen. FR4’s compatibility with complex circuit designs and dense component layouts makes it ideal for supporting intricate electronic assemblies without compromising electrical integrity.

Technological advancements in PCB manufacturing have improved FR4’s qualities, expanding its applications. Enhancements like better thermal management and dielectric properties enable FR4 to meet stricter requirements in high-frequency applications, strengthening its market dominance by evolving with industry needs and trends.

End-Use Industry Analysis

In 2024, the Automotive segment held a dominant market position in the rigid flex PCB market, capturing more than a 28.7% share. This leadership is primarily driven by the increasing integration of advanced electronics in vehicles, including connectivity solutions, autonomous driving systems, and energy-efficient lighting.

The demand for rigid flex PCBs in the automotive sector is further bolstered by the global shift towards electric vehicles (EVs) and hybrid systems. These modern vehicle architectures require more sophisticated electronic control systems, which rely heavily on the unique capabilities of rigid flex PCBs to handle high power and high-speed signal transmissions efficiently.

The need for compact, lightweight components in vehicles drives the adoption of rigid-flex PCBs. These PCBs fit into smaller spaces, reducing weight and volume, which is especially beneficial in automotive design to enhance fuel efficiency and performance.

Furthermore, technological advancements in automotive safety and infotainment systems have created additional demand for rigid flex PCBs. As manufacturers develop more advanced safety features, such as collision avoidance systems and emergency braking systems, and more sophisticated infotainment units, the precision and reliability provided by rigid flex PCBs become indispensable.

Key Market Segments

By Product Type

- Single-sided flex

- Double-sided flex

- Multi-layer flex

- Multilayer PCB

- Quick turn rigid flex PCB

By Layer Count

- Single layer

- Double layer

- Multi-layer

By Flexibility Type

- static flex

- dynamic flex

By Materials

- FR4

- Kapton

- Rogers

- Others

By End-Use Industry

- Aerospace and defense

- Automotive

- Consumer electronics

- Industrial

- IT and telecommunications

- Healthcare

- Others (e.g., Energy, Transportation)

Driver

Growing Demand in Consumer Electronics

The increasing miniaturization and multifunctionality of consumer electronics have significantly propelled the adoption of rigid-flex printed circuit boards (PCBs). Devices such as smartphones, tablets, and wearable technology require compact, lightweight, and reliable interconnect solutions.

Rigid-flex PCBs, by integrating flexible and rigid substrates, enable complex circuitry within constrained spaces, thereby meeting these stringent design requirements.

Integrating rigid-flex PCBs reduces device footprint while boosting performance and durability, meeting consumer demand for sleek, durable products. As the consumer electronics industry evolves, the adoption of rigid-flex PCBs is expected to grow, fueled by ongoing innovation and the drive for better user experiences.

Restraint

High Production Costs

Despite their advantages, the widespread adoption of rigid-flex PCBs is hindered by elevated production costs compared to traditional rigid PCBs. The manufacturing process involves complex design rules, meticulous material selection, and precise assembly techniques, all contributing to increased expenses.

For instance, determining appropriate bend radii in flexible sections and ensuring seamless layer transitions necessitate advanced engineering expertise and sophisticated equipment. The limited availability of high-quality materials for both rigid and flexible sections raises costs, which could discourage manufacturers—especially those with strict budget constraints from incorporating rigid-flex PCBs, ultimately hindering market growth.

Opportunity

Expansion in Medical Devices

The medical device industry presents a significant opportunity for the application of rigid-flex PCBs. Advanced medical equipment, including diagnostic imaging systems, patient monitoring devices, and implantable technologies, demands compact, reliable, and high-performance electronic components.

Rigid-flex PCBs fulfill these requirements by offering enhanced durability and flexibility, essential for devices that must conform to various form factors or endure repetitive movements. As healthcare technology advances towards more portable and minimally invasive solutions, the demand for rigid-flex PCBs is expected to escalate, providing manufacturers with avenues for diversification and growth within this critical sector.

Challenge

Design and Manufacturing Complexity

The intricate design and manufacturing processes associated with rigid-flex PCBs pose substantial challenges. Engineers must navigate complex design rules, such as accommodating specific bend radii to prevent mechanical failures and maintaining signal integrity across flexible sections.

Material selection is critical, requiring compatibility between rigid and flexible substrates to ensure consistent performance under varying thermal and mechanical stresses. Furthermore, the assembly process demands precise alignment and integration of components, increasing the potential for errors and rework.

Addressing these complexities necessitates continuous investment in specialized design software, skilled personnel, and advanced manufacturing technologies, which can be resource-intensive for companies aiming to maintain competitiveness in the rigid-flex PCB market.

Emerging Trends

As electronic devices become more compact and feature-rich, there’s an increasing need for PCBs that are both thinner and capable of higher circuit densities. Rigid-flex PCBs are evolving to meet these requirements, facilitating the development of smaller and more powerful gadgets.

The adoption of materials like gallium nitride (GaN) and silicon carbide (SiC) is enhancing the performance and reliability of rigid-flex PCBs. Innovations in manufacturing techniques, such as laser drilling and chemical copper plating, are improving precision and efficiency.

The incorporation of HDI technology allows for more intricate circuitry within compact spaces, improving signal integrity and reducing electromagnetic interference. This advancement is particularly beneficial for high-performance applications in consumer electronics and telecommunications.

Business Benefits

- Space Efficiency: By integrating rigid and flexible sections, these PCBs can be folded or bent to fit into compact spaces, eliminating the need for connectors and additional interconnects. This design is particularly beneficial for compact and densely packed electronic devices.

- Enhanced Reliability: With fewer connectors and solder joints, rigid-flex PCBs reduce potential points of failure, leading to improved system reliability. Their design minimizes connector-related issues, making them suitable for high-vibration environments.

- Cost Reduction: Although the initial manufacturing process may be complex, the overall assembly costs are often reduced due to fewer components and manual assembly steps. The elimination of connectors and reduced assembly errors contribute to cost savings.

- Durability in Harsh Conditions: Rigid-flex PCBs are designed to withstand mechanical stress and temperature variations, making them suitable for applications in harsh environments. Their robust construction ensures longevity and performance stability.

- Design Flexibility: These PCBs enable the creation of complex geometries and three-dimensional configurations that are challenging to achieve with traditional rigid PCBs. This flexibility allows designers to develop innovative and compact electronic products.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

In this competitive market, several key players have emerged as leaders, driving growth and technological innovation.

Zhen Ding Technology Holding Limited, a major player in the rigid-flex PCB market, is known for its innovation and technological advancements. Zhen Ding, based in Taiwan, specializes in rigid and flexible PCBs, offering high-performance solutions for industries such as consumer electronics, automotive, and telecommunications.

Nippon Mektron, a Japanese company, stands as one of the world’s largest manufacturers of flexible printed circuits. Its contribution to the rigid-flex PCB market is significant, with a focus on advanced manufacturing techniques and a commitment to innovation. Nippon Mektron’s products are known for their precision and durability, serving industries such as automotive, medical, and consumer electronics.

Sumitomo Electric Industries, based in Japan, is a key player in the rigid-flex PCB market due to its advanced technology and comprehensive portfolio. The company’s rigid-flex PCBs are known for their high reliability and high performance, especially in industries that require high-speed and high-frequency electronic devices.

Top Key Players in the Market

- Zhen Ding Technology Holding Limited

- Nippon Mektron, Ltd.

- Sumitomo Electric Industries, Ltd.

- Unimicron Technology Corporation

- Interflex Co., Ltd.

- Young Poong Electronics Co., Ltd.

- TTM Technologies, Inc.

- Multek (a Flex Company)

- Shengyi Technology Co., Ltd.

- AT&S Austria Technologie & Systemtechnik AG

- Meiko Electronics Co., Ltd.

- Kinwong Electronic Co., Ltd.

- Sierra Circuits, Inc.

- Eltek Ltd.

- Jabil Circuit, Inc.

- Samsung Electro-Mechanics

- Würth Elektronik GmbH & Co. KG

- Shenzhen Kinwong Electronic Co., Ltd.

- Flex PCB (Printed Circuits LLC)

- Others

Top Opportunities for Players

The rigid-flex PCB market presents several promising opportunities for industry players and investors, driven by its expanding application across various sectors.

- Expansion into Emerging Technologies: The rigid-flex PCBs are increasingly crucial in cutting-edge technologies such as wearables, IoT devices, and smart devices, where their flexibility and durability are essential. The drive towards miniaturization and higher performance in consumer electronics also propels the demand for these PCBs.

- Growth in the Automotive Sector: Advanced driver-assistance systems (ADAS) and electric vehicles (EVs) are becoming more prevalent, necessitating robust and space-efficient PCB solutions. This trend is set to continue as the automotive industry evolves, highlighting a significant growth area for rigid-flex PCBs.

- Healthcare and Medical Applications: There is an increasing demand for compact, reliable medical devices such as wearables and implantable devices, which require the unique capabilities of rigid-flex PCBs. This sector offers substantial opportunities due to the critical nature and rapid growth of medical technologies.

- Technological Advancements in PCB Materials: Innovations in materials and manufacturing processes for rigid-flex PCBs can lead to enhanced performance and durability. Players in the PCB market can gain a competitive edge by investing in R&D to develop superior flex layers and adhesives.

- Geographical Expansion: Markets in Asia-Pacific, particularly China and India, are rapidly growing due to the surge in electronics manufacturing and adoption of advanced technologies. Companies can leverage these markets by expanding their manufacturing capabilities or forming strategic partnerships in the region.

Recent Developments

- In June 2024, AdvancedPCB was formally launched as a unified entity combining the capabilities of Advanced Printed Circuit Technology (APCT), Advanced Circuits, Inc. (ACI), and San Diego PCB Design (SDPCB). This strategic consolidation aims to strengthen PCB manufacturing across critical industries such as healthcare, aerospace, and defense.

- April 2024: DuPont has unveiled the Pyralux ML Series, a new range of double-sided metal-clad laminates crafted for superior thermal management in flexible and rigid-flex PCBs. Designed for demanding sectors like aerospace, defense, EVs, and AI networking, these laminates excel in complex circuit applications such as sensors, heaters, and thermocouples.

- May 2024: Flex Ltd., a global electronics manufacturing services company, acquired FreeFlow, a Texas-based firm, enhancing its capabilities in the PCB sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 25.7 Bn |

| Forecast Revenue (2034) | USD 77.7 Bn |

| CAGR (2025-2034) | 11.70% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Product Type (Single-sided flex, Double-sided flex, Multi-layer flex, Multilayer PCB, Quick turn rigid flex PCB), By Layer Count (Single layer, Double layer, Multi-layer), By Flexibility Type (static flex, dynamic flex), By Materials (FR4, Kapton, Rogers, Others), By End-Use Industry (Aerospace and defense, Automotive, Consumer electronics, Industrial, IT and telecommunications, Healthcare, Others (e.g., Energy, Transportation)) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Zhen Ding Technology Holding Limited, Nippon Mektron, Ltd., Sumitomo Electric Industries, Ltd., Unimicron Technology Corporation, Interflex Co., Ltd., Young Poong Electronics Co., Ltd., TTM Technologies, Inc., Multek (a Flex Company), Shengyi Technology Co., Ltd., AT&S Austria Technologie & Systemtechnik AG, Meiko Electronics Co., Ltd., Kinwong Electronic Co., Ltd., Sierra Circuits, Inc., Eltek Ltd., Jabil Circuit, Inc., Samsung Electro-Mechanics, Würth Elektronik GmbH & Co. KG, Shenzhen Kinwong Electronic Co., Ltd., Flex PCB (Printed Circuits LLC), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |