Quick Navigation

Report Overview

The Global Power Electronic Testing Market size is expected to be worth around USD 25 Billion By 2034, from USD 6.4 Billion in 2024, growing at a CAGR of 14.60% during the forecast period from 2025 to 2034. In 2024, the Asia-Pacific region dominated the Power Electronic Testing Market with a 38.6% share and USD 2.4 billion in revenue. China’s market was valued at USD 0.98 billion, projected to grow at a 11.2% CAGR.

Power electronic testing evaluates the performance, safety, and efficiency of electronic components and systems that manage the flow of power. This includes testing various components like inverters, converters, batteries, and semiconductor devices to ensure they operate efficiently and meet regulatory standards.

The power electronic testing market is driven by the need for advanced energy systems in rapidly urbanizing areas, supportive government policies for renewable energy and electric vehicles, and innovations in semiconductor materials like silicon carbide (SiC) and gallium nitride (GaN). These factors contribute to the demand for robust testing solutions that can handle the complexities of modern power electronics.

Key drivers of the power electronic testing market include technological advancements that push the limits of power efficiency and miniaturization, the global shift towards sustainable energy solutions, and the increasing complexity of electronic devices that require sophisticated testing to ensure performance and safety.

Innovations in materials and design, such as wide bandgap semiconductors, amplify these needs by introducing new testing challenges that are critical to address for market growth. There is a growing demand for power electronic testing services in industries such as automotive, telecommunications, and industrial automation.

These sectors require high standards for electronic components due to their critical roles in safety and functionality. The integration of advanced electronics in vehicles, renewable energy systems, and smart industrial equipment drives the need for detailed and rigorous testing protocols to prevent failures and ensure reliability over long periods

Power electronic testing has grown in importance as manufacturers and designers recognize the need for rigorous testing protocols. Regulatory demands enforcing strict safety and efficiency standards further fuel this trend. As a result, testing services have become essential in the power electronics production cycle, rather than just a precaution.

Investing in advanced power electronic testing facilities brings substantial business benefits, including enhanced product reliability, compliance with international safety standards, and the ability to innovate safely with new materials and technologies. Companies that can provide comprehensive testing services are better positioned to capitalize on the trends towards electrification and digitalization, securing a competitive edge in a technology-driven market.

Key Takeaways

- The Global Power Electronic Testing Market size is expected to reach USD 25 Billion by 2034, up from USD 6.4 Billion in 2024, growing at a CAGR of 14.60% during the forecast period from 2025 to 2034.

- In 2024, the Testing Equipment segment held a dominant market position within the Power Electronic Testing Market, capturing more than a 68.7% share.

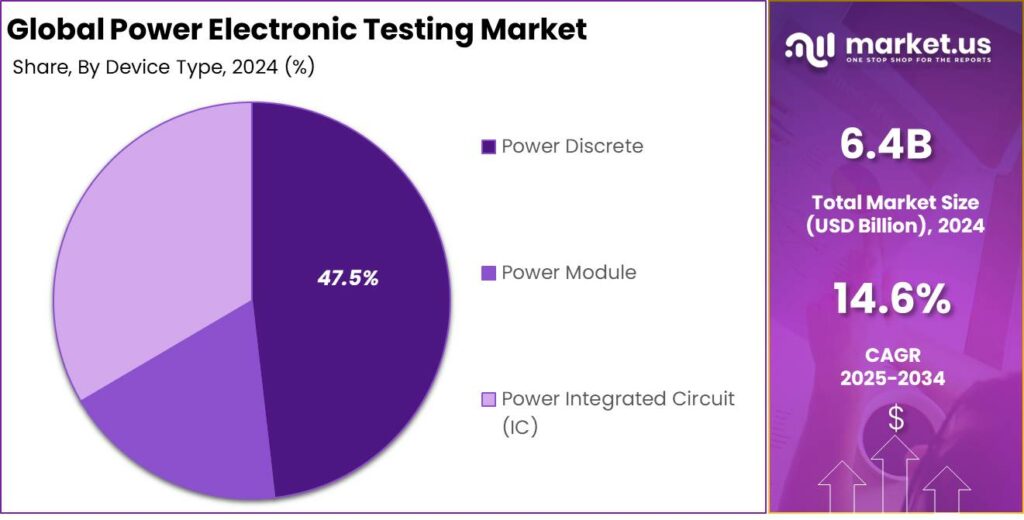

- The Power Discrete segment also held a dominant position in the power electronic testing market in 2024, capturing more than a 47.5% share.

- The ICT segment held a dominant market position within the power electronic testing market in 2024, capturing more than a 32.7% share.

- In 2024, the Asia-Pacific region held a dominant market position in the Power Electronic Testing Market, capturing more than a 38.6% share, with revenue amounting to USD 2.4 billion.

- The market for power electronic testing in China was valued at USD 0.98 billion in 2024 and is projected to grow at a CAGR of 11.2%.

Analysts’ Viewpoint

From an investment perspective, the power electronic testing market presents robust opportunities, particularly in adapting to and driving technological advancements and regulatory environments. Analysts emphasize the importance of embracing innovative testing technologies that can handle the higher power densities and efficiency demands of modern electronics.

The ability to quickly adapt to changing technologies and regulatory requirements is also seen as crucial for staying relevant and leading in the market. Additionally, the strategic collaborations with academic institutions and industry leaders are recommended to foster innovation and maintain technological leadership

China Market Size

In 2024, the market for power electronic testing in China was valued at USD 0.98 billion. It is projected to grow at a compound annual growth rate (CAGR) of 11.2%. This substantial growth can be attributed to several factors, including the rapid expansion of the power electronics sector within the region, driven by increasing investments in renewable energy and the automotive industry.

As the demand for more efficient energy solutions rises, so does the necessity for rigorous testing of power electronics to ensure reliability and safety in applications ranging from industrial machinery to consumer electronics and electric vehicles.

Government initiatives to enhance China’s technological infrastructure are key to market expansion. These initiatives promote advanced manufacturing techniques and local expertise in high-tech industries, driving demand for power electronic testing services. As a result, the market is poised for continued growth, fueled by technological advancements and a shift toward sustainable energy practices.

In 2024, Asia-Pacific held a dominant market position in the Power Electronic Testing Market, capturing more than a 38.6% share with revenue amounting to USD 2.4 billion. This significant market share can be attributed to several key factors that underscore the region’s leading position in this sector.

Asia-Pacific benefits from a robust manufacturing base, particularly in countries like China, Japan, and South Korea, where there are substantial investments in semiconductor and electronics industries. The demand for power electronic testing in these regions is fueled by the production of consumer electronics, automotive electronics, and renewable energy solutions, all of which require stringent quality checks and performance assessments.

Government policies supporting industrial growth and technology boost market dynamics by encouraging investment in research and development. Subsidies and tax incentives, particularly in the electronics manufacturing sector, drive advancements in power electronic devices, requiring stringent testing to manage emerging technologies.

The rapid growth of renewable energy projects, particularly in China and India, is pivotal to the dominance of the Asia-Pacific market. As these nations shift towards greener energy solutions, the demand for power electronic testing services to ensure the efficiency and safety of equipment in solar and wind installations has significantly increased.

Offering Analysis

In 2024, the Testing Equipment segment held a dominant market position within the Power Electronic Testing Market, capturing more than a 68.7% share. The leading position of this segment can be primarily attributed to the critical need for accurate, real-time testing and measurement to ensure the functionality and safety of power electronic devices across various applications.

The Testing Equipment segment holds a significant market share, driven by the growing complexity of power electronic systems. As devices become more integrated, the need for diverse testing equipment increases. Automated Test Equipment (ATE) plays a crucial role in streamlining complex tests, improving production efficiency and reliability in sectors like automotive and consumer electronics.

Technological advancements in renewable energy, automotive, and telecommunications drive the demand for advanced testing solutions like Oscilloscopes and Spectrum Analyzers. These tools help diagnose issues, ensure stability, and optimize performance. As these sectors evolve, the need for high-performance testing equipment to address emerging challenges becomes increasingly critical.

The global expansion of regulatory standards has strengthened the Testing Equipment segment, driven by the need for compliance with safety, quality, and environmental norms. The demand for advanced testing instruments in healthcare and aerospace fuels the segment’s leadership in the Power Electronic Testing Market, ensuring precise testing to meet evolving regulations.

Device Type Analysis

In 2024, the Power Discrete segment held a dominant position in the power electronic testing market, capturing more than a 47.5% share. This segment encompasses various components crucial for managing power at high efficiencies, such as diodes and transistors.

The Power Discrete segment’s leadership is driven by the widespread use of diodes and transistors in key applications. Diodes like Zener, Schottky, and rectifier diodes are essential for voltage regulation and power conversion in supply systems. Similarly, transistors such as FETs, BJTs, and IGBTs are crucial for switching and amplifying electronic signals, which are vital for modern electronic devices.

Advancements in materials like silicon carbide (SiC) and gallium nitride (GaN) have boosted the Power Discrete segment by improving diode and transistor performance under high-frequency and high-temperature conditions. These innovations surpass global efficiency standards, driving increased adoption in demanding applications.

The Power Discrete segment is set for continued growth, driven by the demand for energy-efficient, compact devices. As global electrification and renewable energy efforts increase, the need for reliable, efficient power components will ensure the segment’s ongoing dominance in the power electronic testing market.

Vertical Analysis

In 2024, the ICT segment held a dominant market position within the power electronic testing market, capturing more than a 32.7% share. This substantial market share can be attributed to the escalating demand for robust, high-speed, and efficient communication systems across various sectors.

The rise in cloud computing and data center operations has further propelled the ICT segment’s growth. Power electronic testing is essential for data centers, ensuring reliable, uninterrupted power supply systems and energy-efficient solutions capable of managing large data volumes. It verifies that these systems can handle high loads and perform optimally, driving the growth of the sector.

The growing focus on IoT and connected devices has heightened the demand for power electronic testing in the ICT sector. As device interconnectivity increases, power management complexity grows, requiring thorough testing to prevent failures and ensure interoperability. This shift towards a connected digital ecosystem positions the ICT sector as a key driver in the power electronic testing market.

Regulatory standards and environmental concerns are influencing market dynamics. Stricter rules on electronic waste and energy efficiency require thorough testing of ICT equipment before deployment. To comply with these regulations and reduce environmental impact, companies are investing in testing solutions, solidifying the ICT segment’s dominant role in the power electronic testing market.

Key Market Segments

By Offering

- Testing Equipment

- Automated Test Equipment

- Oscilloscopes

- Signal Generators

- Multimeters

- Logic Analyzers

- Spectrum Analyzers

- Bert Solutions

- Testing Services

- Electromagnetic Compatibility (EMC) Testing -Electrical Safety Testing

- Radio Frequency (RF) Testing -Energy Efficiency Testing

By Device Type

- Power Discrete

- Diode

- Mounting Type and Diode Packaging

- PIN Diode

- Zener Diode

- Schottky Diode

- Switching Diode

- Rectifier Diode

- Transistor

- Field-effect Transistor (FET)

- Bipolar Junction Transistor (BJT)

- Insulated Gate Bipolar Transistor (IGBT)

- Thyristors

- Diode

- Power Module

- Standard & Power Integrated Module

- IGBT Module

- FET

- Others

- IPM

- Standard & Power Integrated Module

- Power Integrated Circuit (IC)

- Power Management IC

- Application-Specific IC

By Vertical

- ICT

- Consumer Electronics

- Power

- Industrial

- Automotive

- Aerospace & Defence

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Surge in Electric Vehicle (EV) Adoption

The rapid growth of the electric vehicle (EV) market serves as a significant driver for the power electronic testing industry. As EVs become more prevalent, the demand for reliable and efficient power electronic components, such as inverters, converters, and battery management systems, has intensified.

The surge in electrified transportation highlights the need for manufacturers to invest in advanced testing solutions for power electronics. Effective testing is crucial to address challenges like thermal management, electromagnetic interference, and energy efficiency, ensuring the reliability and consumer acceptance of EVs.

Governments are enacting strict regulations and incentives to boost EV adoption, including performance and safety standards for automotive electronics. This has fueled growth in the power electronic testing market, as manufacturers must ensure components meet regulatory requirements and consumer expectations.

Restraint

High Costs of Testing Infrastructure

The advancement of power electronics necessitates sophisticated testing equipment capable of evaluating complex components like wide-bandgap semiconductors. However, acquiring and maintaining such advanced testing infrastructure entails substantial financial investment.

The cost of state-of-the-art testing equipment can range from tens of thousands to millions of dollars, posing a significant economic barrier, particularly for small and medium-sized enterprises (SMEs). This financial burden can limit the ability of SMEs to compete effectively, as they may struggle to access the necessary resources to conduct comprehensive testing.

Moreover, the rapid pace of technological innovation in power electronics means that testing equipment can become obsolete relatively quickly, leading to additional capital expenditures to stay current with industry standards.

Opportunity

Integration of Renewable Energy Systems

The global shift towards renewable energy sources presents a significant opportunity for the power electronic testing market. Renewable energy systems, such as solar photovoltaic installations and wind turbines, rely heavily on power electronic components to convert and manage energy efficiently.

As the adoption of renewable energy accelerates, the demand for testing services to ensure the reliability and efficiency of these components is expected to rise substantially. Comprehensive testing is crucial to validate the performance, safety, and durability of these devices under diverse environmental conditions.

Moreover, governments and regulatory bodies are implementing stringent standards and certifications for renewable energy equipment to ensure grid stability and safety. This regulatory landscape further amplifies the need for specialized testing services, creating a lucrative opportunity for companies operating in the power electronic testing market.

Challenge

Rapid Technological Evolution

The power electronics industry is evolving quickly with the rise of wide-bandgap semiconductors like SiC and GaN, which offer higher efficiency and better performance at elevated temperatures and voltages. However, their unique properties create new testing challenges, complicating the power electronic testing market.

Traditional testing methodologies may not be adequate to assess the performance and reliability of devices based on SiC and GaN technologies. Developing new testing protocols requires substantial investment in research and development, as well as the acquisition of specialized equipment.

Additionally, the lack of standardized testing procedures for these advanced materials can lead to inconsistencies in test results, complicating the certification process and potentially delaying time-to-market for new products.

Emerging Trends

One significant trend is the adoption of wide bandgap (WBG) semiconductors, such as gallium nitride (GaN) and silicon carbide (SiC). These materials enable higher efficiency and faster switching frequencies, necessitating the development of specialized testing methodologies to ensure device reliability and performance.

Another emerging trend is the integration of Internet of Things (IoT) capabilities into power electronics. This integration allows for enhanced communication between devices, leading to smarter and more responsive systems. Testing protocols are being updated to assess the reliability and security of these interconnected devices.

The complexity of modern power electronic systems has also led to the increased use of simulation-based testing methods, such as Hardware-in-the-Loop (HIL) simulations. HIL allows for real-time testing of control strategies and system responses without the need for physical prototypes, thereby reducing development time and costs.

Business Benefits

Thorough power electronic testing provides key business benefits, including improved product quality and reliability by detecting defects early in development. This proactive approach minimizes costly recalls and boosts customer confidence.

Rigorous testing ensures compliance with industry standards, facilitating smoother market entry and reducing the risk of legal issues. Products that meet established standards are more likely to be accepted globally, expanding potential market reach.

Additionally, comprehensive testing contributes to cost efficiency by mitigating risks associated with product failures. Identifying issues during the testing phase prevents expensive post-launch corrections and protects the company’s reputation. Investing in advanced testing methods gives companies a competitive edge by showcasing their commitment to quality, which boosts consumer trust, brand loyalty, and business opportunities.

Key Player Analysis

Several key players dominate this sector, providing specialized testing services that cater to various industries, including automotive, and consumer electronics.

SGS SA is a global leader in inspection, verification, testing, and certification. With a strong reputation for delivering high-quality testing services, SGS has become a trusted name in the power electronics testing market. The company offers a wide range of testing solutions that ensure the performance, safety, and compliance of power electronic devices.

Intertek Group plc is a leading provider of quality and safety services, specializing in testing and certification. Intertek plays an essential role in power electronics testing by offering services that help manufacturers and businesses verify the quality, functionality, and safety of their power devices.

TÜV SÜD is another major player in the power electronics testing sector. Based in Germany, TÜV SÜD provides testing and certification services that ensure the safety, reliability, and performance of power electronic products. The company offers specialized services in areas like high-voltage testing, battery testing, and energy efficiency assessment.

Top Key Players in the Market

- SGS SA

- Intertek Group plc

- TÜV SÜD

- TÜV Rheinland

- Eurofins Scientific

- Bureau Veritas

- DEKRA com

- The CSA Group

- Tektronix, Inc.

- Testilabs Oy

- Element Materials Technology

- Others

Top Opportunities for Players

In the power electronics testing market, several opportunities are emerging that can significantly benefit industry players.

- Regulatory Compliance and Standardization: With regions like Europe, the Middle East, and Africa adopting stringent regulatory frameworks, there is a substantial opportunity for growth in compliance testing services. These regions require high standards for power electronics to ensure safety and efficiency, creating demand for advanced testing services that can help companies meet these strict regulations.

- Technological Advancements in Testing Equipment: The market for Automated Test Equipment (ATE), oscilloscopes, and network analyzers is experiencing strong growth, driven by their ability to optimize testing workflows and enhance signal quality in industries like automotive and telecommunications. This demand is largely fueled by the increasing complexity of power electronics systems, particularly those used in electric vehicles and renewable energy technologies.

- Expansion in Emerging Markets: The Asia-Pacific region is experiencing rapid industrialization and technological adoption, leading to a growing demand for power electronics testing services. This is fueled by substantial investments in automation and digital transformation initiatives. Market players can capitalize on this by developing and offering testing solutions tailored to the unique needs of these emerging markets.

- Integration of Wide-Bandgap Semiconductors: There is a growing need for specific testing methodologies due to the development of wide-bandgap materials like Silicon Carbide (SiC) and Gallium Nitride (GaN). These materials are becoming crucial in the production of more efficient and compact devices. Testing services that can cater specifically to these advancements will be critical as the use of these semiconductors expands across various industries.

- Focus on Renewable Energy and Electric Vehicles: The global shift to renewable energy and the growing adoption of electric vehicles are fueling demand for robust testing frameworks to ensure the reliability and efficiency of power electronics. As a result, testing services for solar inverters, grid integration solutions, and EV battery management systems are expected to experience increased demand.

Recent Developments

- In November 2024, SGS acquired Beta Analytic, a leader in Carbon-14 testing, which supports the growing demand for bio-based product validation.

- TÜV SÜD expanded its laboratory in Frankfurt am Main on March 18, 2025. The new facilities will enhance testing capabilities for electromobility products, including car charging plugs and small batteries, addressing growing demands for safety and performance assessments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 6.4 Bn |

| Forecast Revenue (2034) | USD 25 Bn |

| CAGR (2025-2034) | 14.60% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Offering (Testing Equipment (Automated Test Equipment, Oscilloscopes, Signal Generators, Multimeters, Logic Analyzers, Spectrum Analyzers, Bert Solutions), Testing Services (Electromagnetic Compatibility (EMC) Testing -Electrical Safety Testing, Radio Frequency (RF) Testing -Energy Efficiency Testing)), By Device Type (Power Discrete (Diode, Mounting Type and Diode Packaging, PIN Diode, Zener Diode, Schottky Diode, Switching Diode, Rectifier Diode, Transistor, Field-effect Transistor (FET), Bipolar Junction Transistor (BJT), Insulated Gate Bipolar Transistor (IGBT), Thyristors), Power Module (Standard & Power Integrated Module, IGBT Module, FET, Others , IPM), Power Integrated Circuit (IC) (Power Management IC, Application-Specific IC), By Vertical (ICT, Consumer Electronics, Power, Industrial, Automotive, Aerospace & Defence, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | SGS SA, Intertek Group plc, TÜV SÜD, TÜV Rheinland, Eurofins Scientific, Bureau Veritas, DEKRA com, The CSA Group, Tektronix, Inc., Testilabs Oy, Element Materials Technology, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |