Quick Navigation

Report Overview

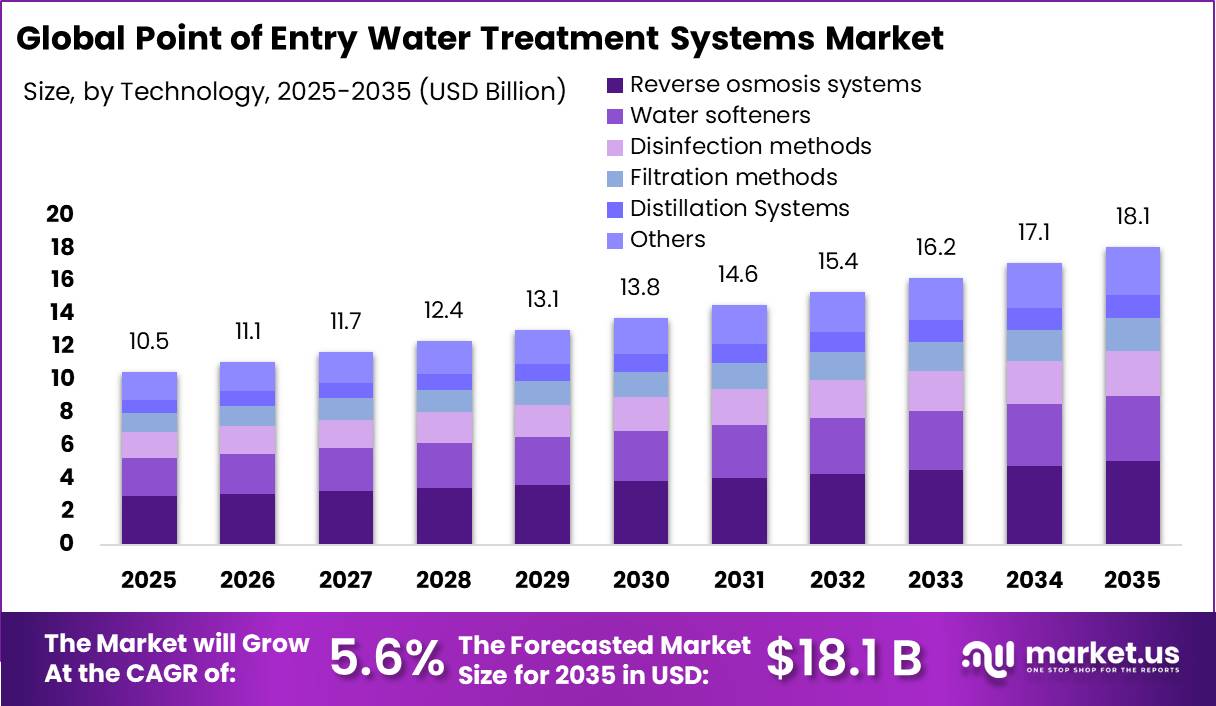

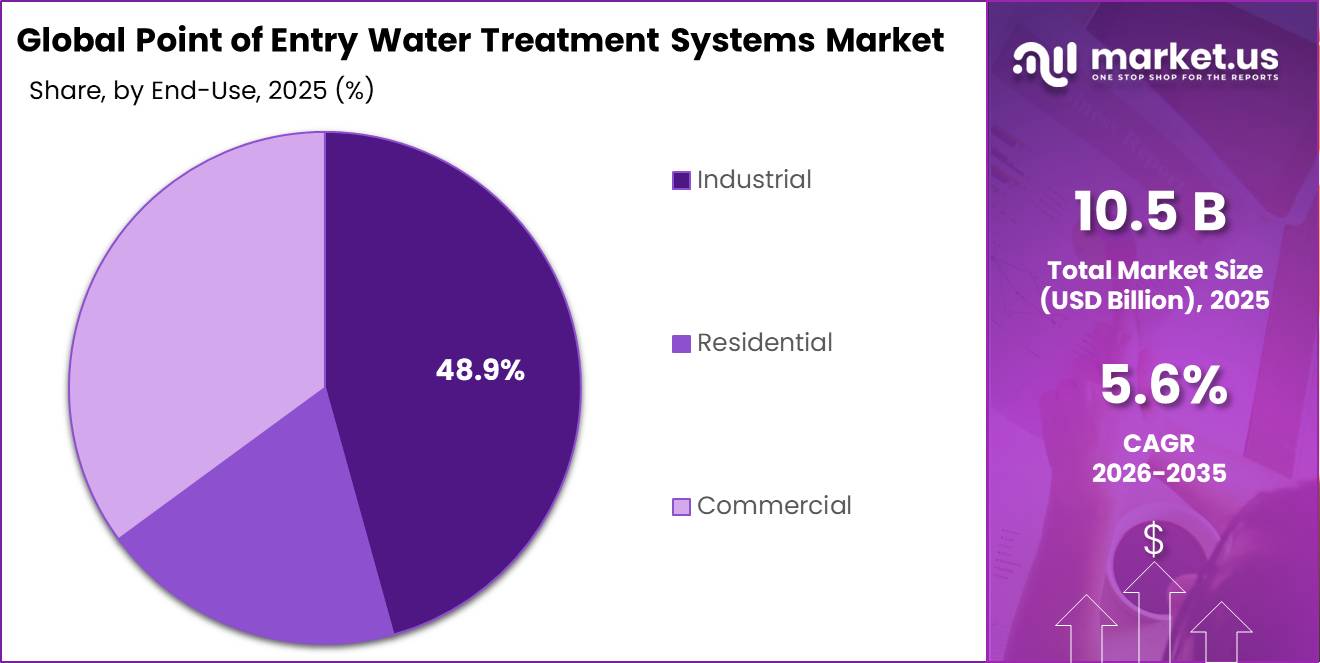

In 2025, the Global Point of Entry Water Treatment Systems Market was valued at US$10.5 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 5.6%, reaching about US$18.1 billion by 2035.

A point-of-entry (POE) water treatment system, commonly known as a whole-house water filter, is a purification system installed where the main water line enters a home or building. The POE water treatment systems market is shaped by rising water-quality concerns, infrastructure gaps, and evolving regulatory standards.

- According to a report by the World Health Organization (WHO), in 2022, globally, at least 1.7 billion people used a drinking water source contaminated with faeces.

Persistent contamination, such as heavy metals, high total dissolved solids, and microbial risks, drives demand for whole-house treatment solutions capable of addressing multiple pollutants simultaneously. Reverse osmosis-based systems are widely adopted due to their broad contaminant removal capability, while alternatives are often used in combination for specific needs.

- According to a study by the US Centers for Disease Control and Prevention, at least 1.1 million individuals, about 1 in every 300 individuals, in the United States alone get sick every year from germs in drinking water.

Infrastructure expansion and urbanization increase the number of connected households, but inconsistent supply quality and aging distribution networks sustain demand for decentralized treatment at the entry point. At the same time, high upfront and maintenance costs remain a barrier, particularly in residential segments. Industrial users represent a major adoption base due to stringent process requirements and regulatory compliance obligations. Meanwhile, technological trends, such as smart monitoring and IoT-enabled systems, are enhancing operational efficiency and reliability.

Key Takeaways

- The global point-of-entry water treatment systems market was valued at USD 10.5 billion in 2025.

- The global point of entry water treatment systems market is projected to grow at a CAGR of 5.6% and is estimated to reach USD 18.1 billion by 2035.

- Based on the technology of point-of-entry water treatment systems, reverse osmosis systems dominated the market, with a market share of around 27.6%.

- Among the end-uses of point of entry water treatment systems, the industrial uses held a major share in the market, 48.9% of the market share.

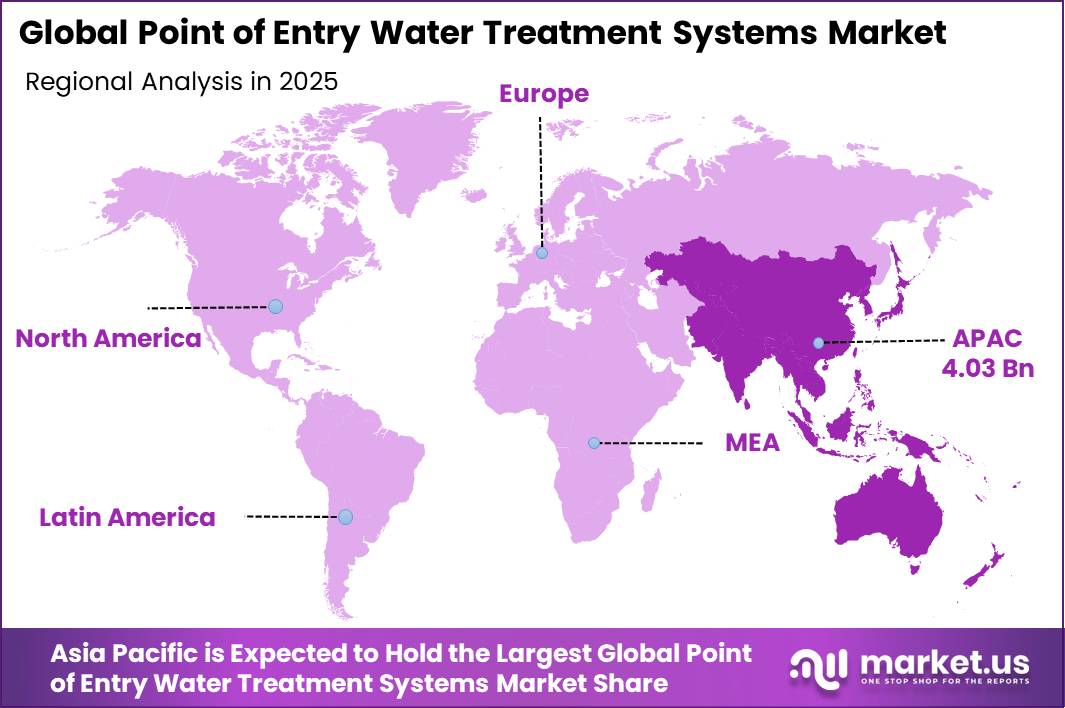

- In 2025, the Asia Pacific was the most dominant region in the point of entry water treatment systems market, accounting for around 38.6% of the total global consumption.

Technology Analysis

Reverse Osmosis Systems Held the Largest Share in the Point of Entry Water Treatment Systems Market.

The point of entry water treatment systems market is segmented based on technology into reverse osmosis systems, water softeners, disinfection methods, filtration methods, distillation systems, and others. The reverse osmosis systems dominated the point-of-entry water treatment systems market, comprising around 27.6% of the market share, as they provide broad-spectrum contaminant removal within a single integrated process. RO membranes can reject dissolved inorganic solids, heavy metals, nitrates, and certain organic compounds, addressing both chemical and aesthetic water-quality concerns simultaneously.

In contrast, water softeners primarily remove hardness, while disinfection methods, such as chlorination or UV, target microbial contaminants but do not eliminate dissolved solids. Conventional filtration is generally limited to particulates and some organics, and distillation, although effective, is energy-intensive and less practical for whole-house applications. Regulatory frameworks for drinking water emphasize limits on total dissolved solids and toxic ions, which RO systems are specifically designed to meet.

End-Use Analysis

Point of Entry Water Treatment Systems Are Mostly Utilized for Industrial Uses.

Based on the end uses of point-of-entry water treatment systems, the market is divided into industrial, residential, and commercial. The industrial uses dominated the point of entry water treatment systems market, with a market share of 48.9%, as water quality directly affects process integrity, equipment lifespan, and regulatory compliance. Industrial operations, such as food processing, pharmaceuticals, power generation, and electronics manufacturing, require strict control over parameters such as total dissolved solids, hardness, microbial load, and specific ions.

Additionally, industries consume large volumes of water, making centralized, entry-point treatment more efficient than multiple point-of-use systems. Regulatory frameworks governing discharge and processed water further necessitate robust treatment at intake. In contrast, residential and commercial users often tolerate variability in non-critical applications and may rely on point-of-use devices due to lower volume needs and cost sensitivity.

Key Market Segments

By Technology

- Reverse osmosis systems

- Water softeners

- Disinfection methods

- Filtration methods

- Sediment Filters

- Granular Activated Carbon (GAC) Filters

- Carbon Block Filters

- Ion Exchange Filters

- Distillation Systems

- Others

By End-Use

- Industrial

- Food & Beverage

- Electronics & Semiconductor

- Pharmaceuticals & Biotechnology

- Chemical & Petrochemical

- Power Generation

- Others

- Residential

- Commercial

- Offices

- HoReCa

- Hospitals

- Schools

- Other

Drivers

Growing Contamination Concerns Drive the Point of Entry Water Treatment Systems Market.

Growing contamination concerns, quantified through regulatory thresholds and field measurements, are a primary structural driver for point-of-entry water treatment adoption. Emerging contaminants include pharmaceuticals, hormones, industrial chemicals, detergents, cyanotoxins, and nanomaterials. In a study of 258 of the world’s rivers in 2022, over a quarter of these were found to have concentrations of active pharmaceutical ingredients that exceeded safe limits. The WHO suggests that, whilst the exact effects on human health and biodiversity are not fully known, this will likely augment antibiotic resistance.

Similarly, the World Health Organization guideline for arsenic in drinking water is 10 µg/L, yet concentrations above this level are reported across multiple aquifers and regions globally. In India, government-linked assessments identify arsenic contamination across several states, with localized sampling showing up to 59.06% of water sources exceeding 50 µg/L, which is five times the WHO guideline.

Contamination is not isolated, as heavy metals affect an estimated 100 million people worldwide, reflecting systemic groundwater quality degradation. The household studies further show untreated well water arsenic ranging from less than 10 to 640 µg/L, with statistically significant exposure reductions, up to 59% in adults, when point-of-use/entry treatment is applied.

The contamination sources include geogenic leaching and anthropogenic runoff, while regulatory tightening, such as progressive lowering of permissible arsenic limits, reinforces compliance pressure. Consequently, persistent exceedances, health-linked exposure data, and stricter standards create sustained demand for POE systems as a risk-mitigation response.

Restraints

High Initial Investment and Operating Costs Might Hamper the Demand for Point of Entry Water Treatment Systems.

High initial investment and recurring operating costs constitute a material constraint on the adoption of point-of-entry water treatment systems, particularly for residential users. Cost structures are multi-layered, comprising capital equipment, installation, and lifecycle maintenance, as reflected in engineering cost frameworks used by the U.S. Environmental Protection Agency for drinking-water treatment systems.

Additionally, operating and maintenance (O&M) costs represent a continuous financial burden. The primary O&M components include regular replacement of filters and membranes. Similarly, energy consumption for advanced systems and chemicals, such as sodium hypochlorite or chlorine, can increase unit production costs by approximately 0.18 EUR/m³.

The California State Water Resources Control Board highlights that for small or at-risk systems, these cumulative costs often exceed local funding capabilities, making centralized alternatives or simpler point-of-use devices more viable despite the comprehensive protection offered by POE solutions. The higher contaminant loads increase both capital intensity, via pre-treatment needs, and maintenance frequency, reinforcing cost barriers and slowing adoption despite demonstrated treatment efficacy.

Opportunity

Infrastructure and Urbanization Create Opportunities in the Point of Entry Water Treatment Systems Market.

Infrastructure expansion and rapid urbanization create a structural opportunity for point-of-entry water treatment systems by increasing exposure to a centralized yet inconsistent water supply. The urban tap-water coverage in India rose from 49% in 2011 to about 77% by 2025-26, adding over 22.8 million household connections under national programs. However, service reliability and quality remain uneven, as no Indian city provides a continuous 24/7 supply, and distribution is often limited to a few hours per day.

Urbanization intensifies this gap, as global assessments show cities absorbing nearly all population growth, while infrastructure expansion lags, leaving many urban residents without safely managed water services. Even where piped access exists, quality constraints persist, as only 6% of surveyed urban households report receiving drinkable water directly, and 62% already rely on filtration systems.

The infrastructure scale-up increases last-mile contamination risks due to aging pipes, intermittent supply, and wastewater intrusion, while expanding the addressable base of connected households. This combination, rising network penetration alongside quality variability, creates a sustained, infrastructure-linked opportunity for POE systems as decentralized treatment complements centralized supply.

Trends

Adoption of Smart and Connected Point of Entry Water Treatment Systems.

The adoption of smart and connected point-of-entry water treatment systems is emerging as a technology-driven trend, anchored in the integration of Internet of Things (IoT)-based monitoring and control capabilities. The IoT-enabled systems can continuously measure multiple water-quality parameters, such as pH, turbidity, conductivity, and dissolved solids, in real time, replacing periodic manual testing.

The experimental deployments demonstrate near-real-time monitoring frequencies, such as measurements at two-hour intervals, and high operational reliability, with sensor-based systems achieving up to 96% accuracy and about 1.2-second response times for anomaly detection. These systems further enable automated alerts when parameters deviate from predefined safety thresholds, reducing response latency compared to conventional sampling methods.

The smart water architectures combine sensors, controllers, and cloud platforms to support remote monitoring, predictive maintenance, and automated control of treatment processes. This functionality is particularly relevant under rising water-quality variability driven by urbanization and pollution, which challenges fixed-parameter treatment systems. The shift toward real-time data acquisition, automated alerts, and remote operability is transforming POE systems from passive filtration units into adaptive, connected infrastructure, supporting improved compliance and operational efficiency.

Geopolitical Impact Analysis

Geopolitical Volatility and Infrastructure Resilience in the POE Water Treatment Sector.

The geopolitical tensions impact the point-of-entry (POE) water treatment sector through supply chain volatility and resource insecurity. According to the U.S. Department of Commerce, trade restrictions and tariffs on aluminum and steel, critical materials for pressure vessels and housing components, have increased raw material lead times. Furthermore, the European Commission notes that energy supply disruptions in the Eurozone have increased the cost of energy-intensive components such as UV lamps and specialized membranes.

The Federal Maritime Commission reports that rerouting cargo due to maritime insecurity in Red Sea tensions has added 10-15 days to transit times for components sourced from Asia, impacting assembly schedules for POE systems. Additionally, trade barriers on rare earth elements and specialized resins used in ion exchange systems have led to price fluctuations. For instance, Pentair’s technical disclosures acknowledge that global supply chain constraints necessitated inventory build-ups to mitigate parts shortages.

Similarly, the Cybersecurity and Infrastructure Security Agency (CISA) issued alerts regarding threats to decentralized water infrastructure. This has mandated a shift toward secure-by-design smart POE systems with encrypted remote monitoring to protect against cross-border cyberattacks. Furthermore, governments are responding with friend-shoring initiatives. The U.S. Environmental Protection Agency (EPA) encourages the use of American-made components through Build America, Buy America (BABA) requirements for federally funded water projects, prioritizing domestic manufacturing of filtration media and hardware.

Moreover, the geopolitical tensions are increasingly linked to water scarcity itself. The transboundary water disputes, such as the Nile and Brahmaputra basins, and upstream control of river systems can alter downstream water quality and availability. These dynamics elevate contamination risks and supply unreliability at the point of use.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Point of Entry Water Treatment Systems Market.

In 2025, the Asia Pacific dominated the global point-of-entry water treatment systems market, holding about 38.6% of the total global consumption, due to its scale of population exposure, infrastructure gaps, and persistent water-quality deficits.

- In East Asia and the Pacific alone, an estimated 116 million people still lack basic drinking water services, while about 910 million lack safe sanitation.

- Across the Asia-Pacific more broadly, over 1.7 billion people do not have access to modern sanitation, indicating systemic water-quality risks at the household level.

The region’s combination of dense population, rapid urbanization, and uneven water infrastructure creates high exposure to last-mile contamination. This expands reliance on household-level treatment. Consequently, Asia Pacific represents the largest installed base and adoption environment for POE systems, driven by scale, infrastructure heterogeneity, and persistent water-quality uncertainty.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of point-of-entry water treatment systems focus on a combination of technology, compliance, and service-led strategies. A primary emphasis is on product innovation, integrating multi-stage filtration and sensor-based monitoring to address diverse contaminant profiles and enable real-time performance tracking. Regulatory alignment is another key activity, with systems designed to meet evolving drinking-water standards set by public authorities, ensuring acceptance in both residential and institutional applications.

Companies further invest in modular and scalable system designs to reduce installation complexity and adapt to varying household or building requirements. After-sales service models, such as maintenance contracts, filter replacement programs, and remote diagnostics, are used to improve lifecycle reliability and customer retention. Additionally, manufacturers pursue localization of production and supply chains to manage input variability and enhance responsiveness to region-specific water conditions.

The Major Players in The Industry

- 3M

- DuPont

- Pentair plc

- BWT Holding GmbH

- Culligan

- Watts

- Veolia

- Calgon Carbon Corporation

- EcoWater Systems LLC

- Watch Water

- O. Smith

- Haier Smart Home (GE Appliances)

- Xylem

- Newterra

- Filtrine

- Other Key Players

Key Development

- In March 2023, DuPont announced the commercial launch of its next-generation DuPont Multibore PRO ultrafiltration membranes, enabling water treatment systems to use fewer modules while improving efficiency across desalination, municipal drinking water, and industrial water purification applications.

- In May 2025, Culligan International launched Culligan with ZeroWater Technology, a range of pitchers and dispensers featuring advanced five-stage filtration, certified to remove more contaminants, including lead, pharmaceuticals, and PFAS, delivering safer, cleaner, and better-tasting drinking water.

Report Scope

| Report Features | Description |

| Market Value (2025) | US$10.5 Bn |

| Forecast Revenue (2035) | US$18.1 Bn |

| CAGR (2026-2035) | 5.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Reverse osmosis systems, Water softeners, Disinfection methods, Filtration methods, Distillation Systems, and Others), By End-Use (Industrial, Residential, and Commercial) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | 3M, DuPont, Pentair plc, BWT Holding GmbH, Culligan, Watts, Veolia, Calgon Carbon Corporation, EcoWater Systems LLC, Watch Water, A. O. Smith, Haier Smart Home (GE Appliances), Xylem, Newterra, Filtrine, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |