Quick Navigation

Report Overview

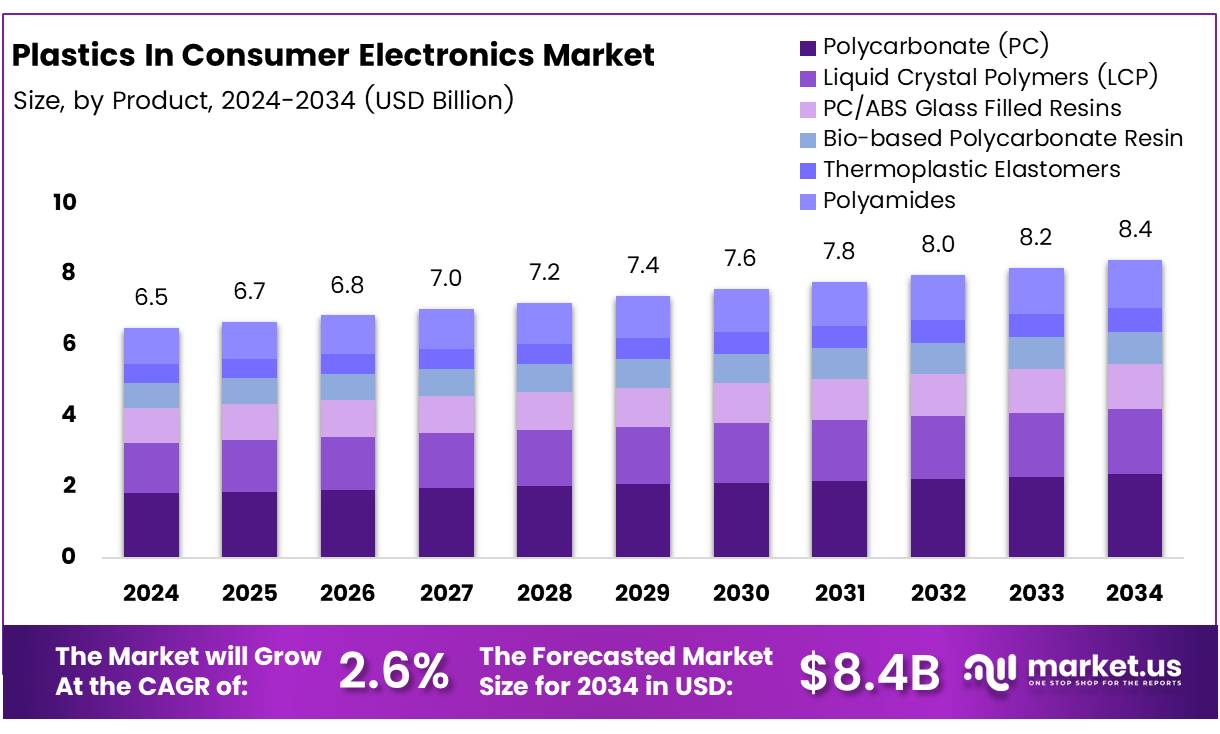

The Global Plastics In Consumer Electronics Market size is expected to be worth around USD 8.4 Billion by 2034, from USD 6.5 Billion in 2024, growing at a CAGR of 2.6% during the forecast period from 2025 to 2034.

The plastics in consumer electronics market encompasses the utilization of various plastic materials in the manufacturing of electronic devices such as smartphones, computers, televisions, and other gadgets. Plastics, valued for their versatility, affordability, and lightweight properties, play a crucial role in shaping the aesthetic, durability, and functionality of these devices.

According to P2Infohouse, plastics represent about 17% of the materials found in end-of-life consumer electronics, illustrating their significant but limited use relative to other materials which constitute the remaining 83%.

the role of plastics in consumer electronics is poised for transformative growth. The inherent properties of plastics such as flexibility, moldability, and resistance to corrosion make them indispensable in the evolving electronics sector.

Moreover, advancements in polymer science are continually enhancing the performance characteristics of plastics, thus broadening their applications within this industry. However, the environmental impact and the push for sustainability pose challenges to the use of traditional plastics, prompting a shift towards biodegradable and recycled plastics.

The market dynamics of plastics in consumer electronics are influenced by several growth factors. The surge in plastic production, which escalated to approximately 400 million tonnes in 2021 and is projected to reach 800 million by 2050, underscores the expanding scale of plastic usage as per Statistics. This growth trajectory is supported by the continuous demand for new and upgraded electronic devices, driven by technological advancements and consumer preferences.

Opportunities within this market are largely tied to innovations in eco-friendly plastics and the integration of high-performance polymers that can replace traditional materials without compromising on quality or functionality.

Additionally, government investments and regulations are increasingly pivotal. They not only mandate the recycling and reduction of plastic waste but also incentivize research in sustainable materials, thus shaping market strategies and competitive dynamics.

Governmental bodies worldwide are intensifying their focus on the environmental impact of consumer electronics, specifically targeting the reduction of plastic waste. Regulations are becoming stricter, requiring manufacturers to adopt more sustainable practices and to participate in the circular economy.

This regulatory environment is complemented by substantial investments in recycling technologies and the development of new materials that align with environmental standards. These initiatives not only support sustainability but also open new avenues for growth and innovation within the plastics market in the consumer electronics sector.

Key Takeaways

- The global plastics in consumer electronics market is projected to grow from USD 6.5 billion in 2024 to USD 8.4 billion by 2034, with a CAGR of 2.6%.

- Polycarbonate (PC) leads the product segment with a 33.2% market share in 2024, favored for its durability and heat resistance.

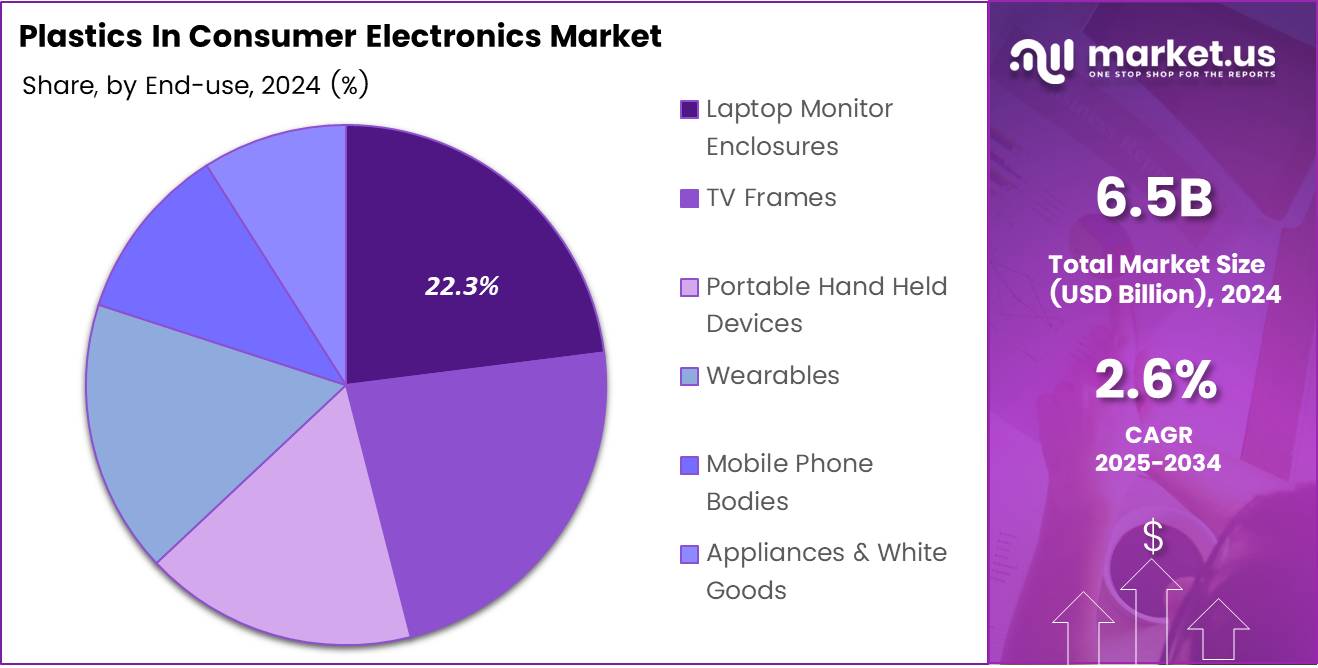

- Laptop monitor enclosures hold a significant 22.3% market share in the end use segment.

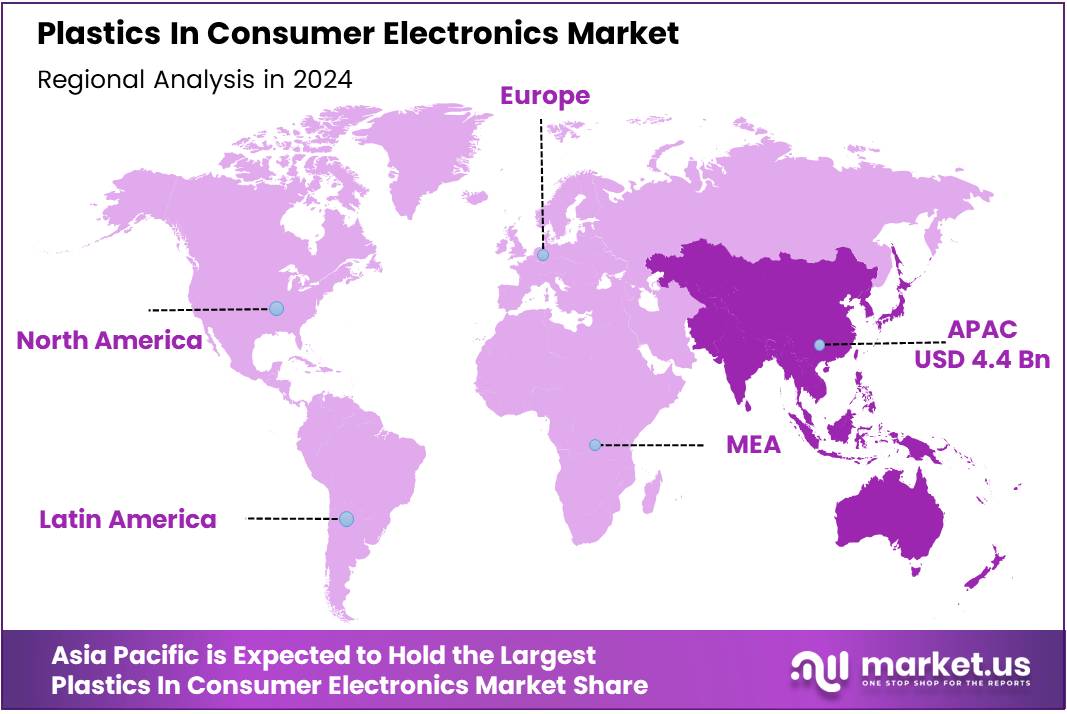

- Asia Pacific is the largest market, commanding a 68.2% share, driven by strong manufacturing bases in China, South Korea, and Taiwan.

Product Analysis

Polycarbonate Leads the Pack in Plastics for Consumer Electronics, Claiming a 33.2% Market Share

In 2024, the plastics in consumer electronics market observed a notable trend in the By Product Analysis segment. Polycarbonate (PC) emerged as the frontrunner, holding a dominant 33.2% market share, largely due to its superior durability and heat resistance which are essential for electronic devices. Following PC, Liquid Crystal Polymers (LCP) have also made significant inroads, particularly valued for their high thermal stability in ultra-thin components.

PC/ABS Glass Filled Resins are another key contender, offering an optimal blend of properties from both PC and ABS plastics, making them ideal for more robust electronic casings. Meanwhile, the shift towards sustainability has boosted the demand for Bio-based Polycarbonate Resin, though its market penetration is still in the early stages compared to synthetic counterparts.

Thermoplastic Elastomers and Polyamides are also pivotal, with the former appreciated for its flexibility and soft touch, which is perfect for consumer electronics that require ergonomic design features. Polyamides stand out for their high mechanical strength and thermal capabilities, supporting components that undergo high thermal cycles within electronic devices.

Collectively, these materials are shaping the dynamics of the plastics in consumer electronics market, each offering distinct advantages that cater to the evolving demands of technology and consumer preferences.

End Use Analysis

Laptop Monitor Enclosures Lead in Consumer Electronics Plastics with 22.3% Market Share

In 2024, the plastics in consumer electronics market witnessed a prominent trend in its By End Use Analysis segment. Laptop Monitor Enclosures emerged as the frontrunner, securing a substantial 22.3% share of the market. This segment’s dominance is primarily due to the ongoing surge in remote work and digital learning, driving the demand for durable and aesthetically pleasing laptops.

As consumers increasingly prioritize portability and design, manufacturers have leveraged advanced plastic materials that offer robustness without adding significant weight, thus enhancing the appeal of laptop monitor enclosures.

Following closely are TV Frames, which capitalize on the rising consumer inclination towards sleek, large-screen displays for enhanced home entertainment experiences. Portable Hand Held Devices also held a significant portion of the market, supported by the continuous innovation in smartphones and tablets that demand lightweight and high-strength materials.

Wearables and Mobile Phone Bodies further contributed to the market dynamics, with each segment adapting to consumer preferences for functionality merged with fashion.

Lastly, Appliances & White Goods segment showcased a steady demand for plastics, driven by the consumer shift towards energy-efficient and smarter home appliances, which require versatile plastic solutions to accommodate complex designs and functionalities.

Key Market Segments

By Product

- Polycarbonate (PC)

- Liquid Crystal Polymers (LCP)

- PC/ABS Glass Filled Resins

- Bio-based Polycarbonate Resin

- Thermoplastic Elastomers

- Polyamides

By End Use

- Laptop Monitor Enclosures

- TV Frames

- Portable Hand Held Devices

- Wearables

- Mobile Phone Bodies

- Appliances & White Goods

Drivers

Lightweight Plastics Enhance Portability and Appeal in Consumer Electronics

In the dynamic realm of consumer electronics, plastics play a pivotal role, primarily driven by their lightweight yet robust characteristics. This inherent property of plastics significantly reduces the weight of devices, ranging from smartphones to laptops, making them notably more portable and user-friendly.

Beyond just lightening the load, plastics offer unparalleled design flexibility, allowing manufacturers to push the boundaries of innovation to produce sleek, modern, and compact designs that attract consumers. Additionally, the cost-effectiveness of plastics stands out in an industry where pricing can be a critical competitive edge.

Manufacturers favor plastics over more expensive materials like metals, as they help keep production costs down while meeting design and durability requirements. Furthermore, plastics excel in electrical insulation, essential for ensuring the safety and functionality of electronic devices. This feature is crucial for components such as connectors, casings, and circuit boards, safeguarding them against electrical hazards and enhancing the product’s overall reliability.

Restraints

Increasing Regulations Impact Plastics in Consumer Electronics

The consumer electronics market faces significant restraints due to increasing government regulations and bans on specific plastic materials. Materials such as PVC and phthalates, commonly used in electronic devices, are now under scrutiny and subject to strict regulatory controls. This shift is driven by environmental concerns and health issues related to these plastics.

Additionally, the consumer electronics industry is highly sensitive to the fluctuations in material costs, particularly because plastics used are often petroleum-based. These materials are inherently volatile in price due to their dependency on the global oil market.

This volatility complicates budgeting and operational planning for manufacturers, who must adapt to both the changing regulatory landscape and the unpredictable cost of key raw materials. As regulations tighten and material costs remain uncertain, companies in the consumer electronics market must innovate and possibly shift towards more sustainable and stable alternatives to maintain competitiveness and comply with global standards.

Growth Factors

Rising Smart Home Device Adoption Fuels Plastics Opportunities in Consumer Electronics

The consumer electronics sector is experiencing a notable expansion in the use of plastics, primarily driven by the increasing adoption of smart home devices. These devices, including smart speakers, home security systems, and IoT-enabled appliances, demand materials that are not only lightweight and cost-effective but also durable and aesthetically versatile.

Plastics meet these criteria perfectly, making them ideal for both external casings and internal components. The trend towards smart homes is accelerating, propelled by consumer interest in automation and enhanced connectivity. As more households adopt these technologies, the demand for plastics in this sector will likely see substantial growth.

This is further supported by plastics’ ability to be engineered to specific needs, such as improved heat resistance and electrical insulation, which are critical for safety and functionality in consumer electronics. Therefore, this surge in smart home devices presents a lucrative growth opportunity for the plastics industry within the realm of consumer electronics, promising increased market share and new product development avenues.

Emerging Trends

3D Printing of Plastic Components Enhances Consumer Electronics Manufacturing

In the consumer electronics sector, a notable trend is the increasing adoption of 3D printing technologies for plastic components. This trend is revolutionizing the industry by offering unprecedented flexibility in designing and prototyping. Manufacturers now have the capability to create custom, complex plastic parts quickly and cost-effectively, which accelerates the development cycle and brings products to market faster.

Additionally, the shift towards smart packaging solutions is gaining momentum, with plastics playing a crucial role in the development of RFID-enabled and interactive packaging that enhances user engagement and product security.

Another significant development is the integration of advanced plastics with cutting-edge technologies like graphene and conductive plastics, which are paving the way for the creation of high-performance, durable materials suitable for the latest electronic gadgets.

Furthermore, the ongoing drive towards miniaturization in consumer electronics continues to boost the demand for thin, lightweight plastics that are essential for the production of smaller, yet powerful devices such as smartphones and laptops. These advancements in plastic use within the electronics industry highlight a dynamic evolution towards more innovative, efficient, and tailored manufacturing solutions.

Regional Analysis

Asia Pacific Leads Global Market for Plastics in Consumer Electronics with 68.2% Share, Valued at $4.42 Billion

The global plastics in consumer electronics market is segmented into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America, each displaying unique growth dynamics and market opportunities.

Asia Pacific dominates the market with a commanding 68.2% share, valued at USD 4.42 billion. This region’s prominence is bolstered by its robust electronics manufacturing base, particularly in countries like China, South Korea, and Taiwan.

The proliferation of manufacturing facilities, coupled with high consumer electronics consumption, drives significant demand for plastics used in smartphones, laptops, and other gadgets. The region’s dominance is further supported by favorable government policies encouraging electronics production, leading to an increased intake of high-performance plastics for advanced consumer electronics.

Regional Mentions:

In North America, the market is driven by technological advancements and the high adoption rate of new-generation telecommunication networks, such as 5G, which require sophisticated consumer electronics. The United States leads in the region, leveraging its strong technological infrastructure and presence of major electronics giants like Apple and HP, which extensively use plastics in product design and aesthetics.

Europe follows a similar pattern with a strong emphasis on sustainability. The European market is keen on adopting eco-friendly plastics to align with stringent regulatory standards, promoting the use of recycled plastics in consumer electronics manufacturing. Countries such as Germany and the UK are at the forefront, integrating innovation with environmental considerations.

The Middle East & Africa, and Latin America regions, though smaller in market size, are rapidly growing. Increased urbanization and rising disposable incomes in these regions contribute to a growing consumer base for electronics, subsequently increasing the demand for plastics in these products. The market in these regions is expected to expand significantly due to the ongoing digital transformation and the increasing penetration of internet-based services.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2024, the global plastics in consumer electronics market is driven by several key players, each contributing to technological innovations and sustainability initiatives in the use of plastics.

Trinseo PLC is strategically focusing on sustainable solutions, aiming to incorporate recycled materials into their plastic production processes. This aligns with the increasing demand for eco-friendly consumer electronics.

Covestro AG continues to be at the forefront of material innovation, with their development of high-performance polycarbonates designed for electronics. These materials are not only durable but also lighter, which is critical for portable devices.

Celanese Corporation has been enhancing its portfolio of engineered materials, providing high thermal resistance plastics that are crucial for devices requiring heat management.

SABIC has been a leader in the market by providing a wide range of resin solutions that cater to the electronics industry’s need for customizable and high-strength materials.

Lotte Chemical Corp and LG Chem are key players in the South Korean market, driving innovation with their advanced polymers tailored for consumer electronics, focusing on enhancing the aesthetic appeal and functionality of devices.

Mitsubishi Chemical Group Corporation emphasizes R&D in developing sustainable plastic solutions that contribute to reducing the environmental impact of electronic products.

SAMSUNG SDI Co., Ltd., primarily known for its battery technologies, also invests in developing polymers that improve battery casings, contributing to safer and more reliable consumer electronics.

Top Key Players in the Market

- Trinseo PLC

- Covestro AG

- Celanese Corporation

- SABIC

- Lotte Chemical Corp.

- LG Chem

- Mitsubishi Chemical Group Corporation

- SAMSUNG SDI Co., Ltd.

- DSM-firmenich

- Kuraray Co. Ltd.

- Qingdao GON Science & Technology Co., Ltd.

Recent Developments

- In December 2024, Cadstrom successfully raised $6.8 million in seed funding to enhance the validation processes for electronic hardware design, aiming to improve efficiency and accuracy in the industry.

- In November 2024, TactoTek® secured a substantial $60 million in funding, with the investment round led by Virala Group, to advance their innovative molded structural electronics technology.

- In September 2024, Morphotonics announced the first closing of their Series B funding round, successfully raising over $10 million to expand their roll-to-plate nanoimprint technology for large-area optical applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 6.5 Billion |

| Forecast Revenue (2034) | USD 8.4 Billion |

| CAGR (2025-2034) | 2.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Polycarbonate, Liquid Crystal Polymers, PC/ABS Glass Filled Resins, Bio-based Polycarbonate Resin, Thermoplastic Elastomers, Polyamides), By End Use (Laptop Monitor Enclosures, TV Frames, Portable Hand Held Devices, Wearables, Mobile Phone Bodies, Appliances & White Goods) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Trinseo PLC, Covestro AG, Celanese Corporation, SABIC, Lotte Chemical Corp., LG Chem, Mitsubishi Chemical Group Corporation, SAMSUNG SDI Co., Ltd., DSM-firmenich, Kuraray Co. Ltd., Qingdao GON Science & Technology Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |