Quick Navigation

Report Overview

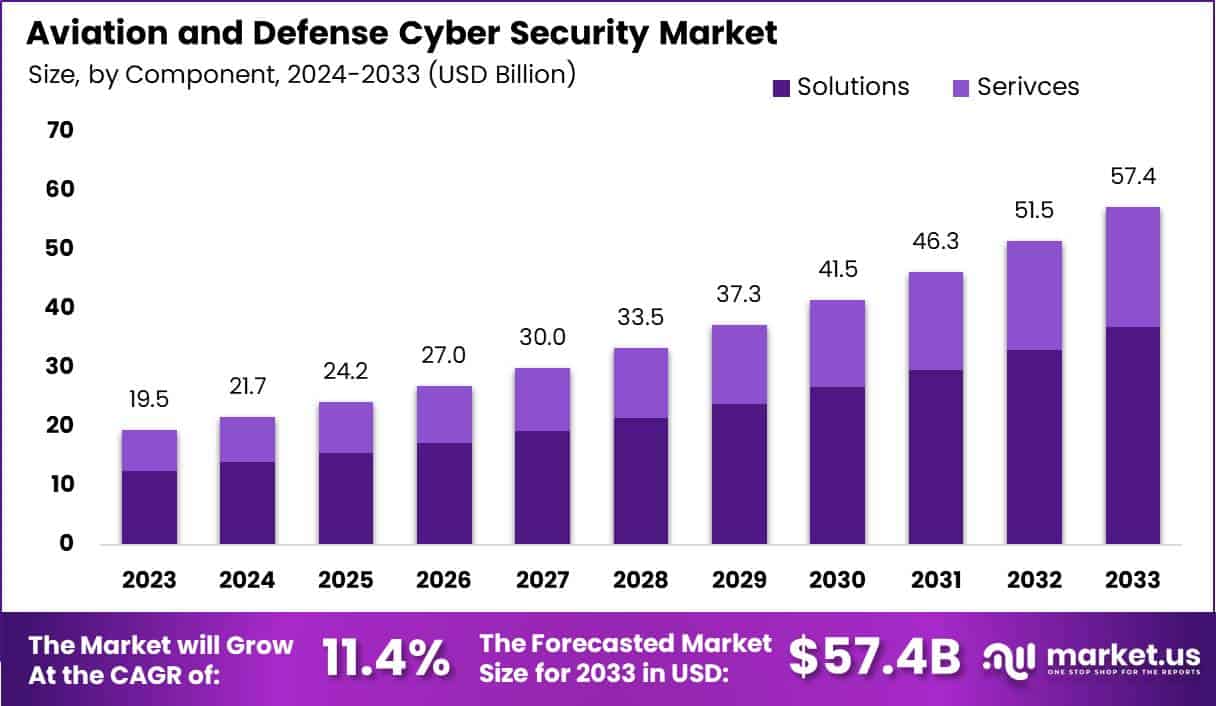

The Global Aviation and Defense Cyber Security Market size is expected to be worth around USD 57.4 Billion By 2033, from USD 19.5 Billion in 2023, growing at a CAGR of 11.40% during the forecast period from 2024 to 2033. In 2023, North America led the Aviation and Defense Cyber Security market, capturing over 42% of the market share and generating USD 8.2 billion in revenues.

Aviation and Defense Cyber Security encompasses a wide range of protective measures and technologies designed to safeguard the digital and physical infrastructure integral to both civil and military aviation sectors. This field aims to counter cyber threats that target aircraft, air traffic control systems, and other critical components of the aviation industry. It encompasses various security measures including network security, data protection, and threat intelligence, crucial for maintaining the integrity and functionality of aviation operations.

The market for aviation and defense cybersecurity is expanding significantly, driven by the increasing incidence of cyber threats, government regulations, and the growing complexity of cyber attacks. The global nature of the aviation industry necessitates a coordinated approach to cybersecurity, encompassing a wide range of practices from basic network hygiene to advanced threat detection and mitigation strategies.

Market growth is bolstered by continuous advancements in technology and the increasing digitalization of operations, requiring constant vigilance and updates to cybersecurity measures.The aviation and defense cyber security market’s growth is primarily driven by the rising incidents of cyber-attacks and the expanding digitalization within the industry. The integration of connected systems in aircraft and airports has opened new avenues for cyber threats, necessitating robust cyber security measures.

The demand within the aviation and defense cyber security market is fueled by the need to protect against potential cyber-attacks that could jeopardize safety, operational security, and data integrity. As the aviation industry continues to evolve with technological advancements like the Internet of Things (IoT) and connected devices, the importance of implementing comprehensive cyber security solutions has become paramount.

There are significant opportunities for growth in the aviation and defense cyber security market, particularly in developing regions like Asia-Pacific, which is expected to be the fastest-growing market in the coming years. The expansion in these regions is driven by increasing air traffic, advancements in aviation infrastructure, and heightened awareness of cyber security risks.

For instance, In April 2023, Rebellion Defense secured a key partnership with the U.S. Department of Energy’s National Nuclear Security Administration (NNSA). The agreement focuses on enhancing NNSA’s cybersecurity through Rebellion Nova, a cutting-edge simulation platform designed to mimic real-world adversarial attacks. This move highlights NNSA’s commitment to bolstering its cyber defenses against emerging threats.

Furthermore, the ongoing development of more sophisticated cyber security solutions, such as real-time threat detection and AI-driven security protocols, provides additional growth avenues for market players. Innovative technologies are at the forefront of driving changes in the aviation and defense cyber security landscape.

Recent advancements include the development of advanced authentication methods, real-time security monitoring platforms, and the integration of artificial intelligence and machine learning in cyber security solutions. These technologies enhance the ability to detect and respond to threats swiftly and effectively. For example, new tools like the Viper Memory Loader Verifier II have been developed specifically to protect military aircraft from cyber threats.

Key Takeaways

- The Global Aviation and Defense Cyber Security Market is projected to reach USD 57.4 billion by 2033, growing from USD 19.5 billion in 2023, at a CAGR of 11.40% during the forecast period from 2024 to 2033.

- In 2023, the Solution segment dominated the Aviation and Defense Cyber Security market, accounting for over 64.3% of the market share.

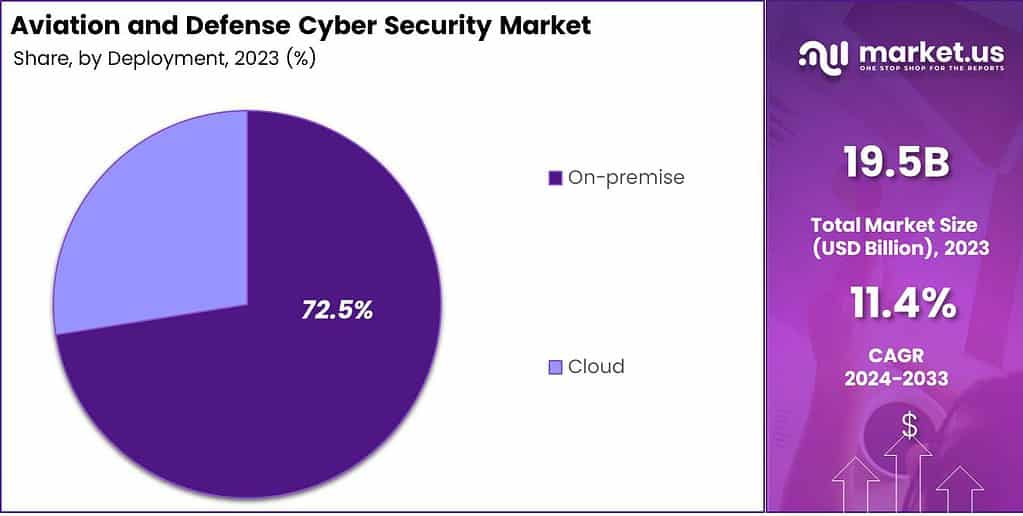

- The On-premise segment held a dominant position in 2023, capturing more than 72.5% of the market share within the Aviation and Defense Cyber Security sector.

- The Commercial Aviation segment was the largest in 2023, representing more than 36.4% of the market share in the Aviation and Defense Cyber Security market.

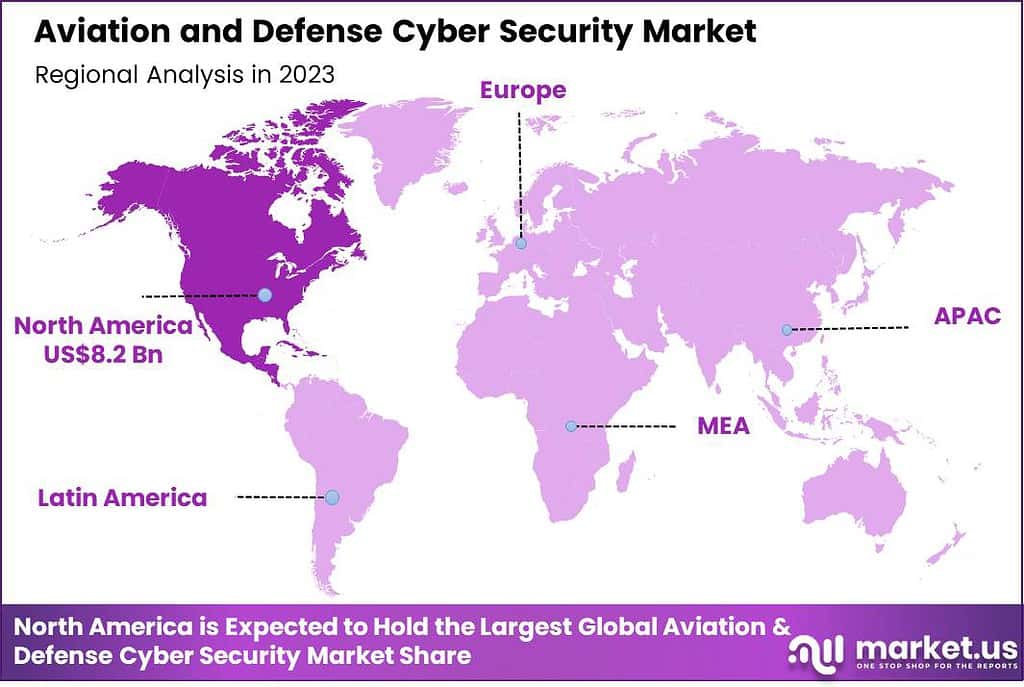

- North America led the Aviation and Defense Cyber Security market in 2023, holding more than 42% of the market share and generating USD 8.2 billion in revenues.

Component Analysis

In 2023, the Solution segment held a dominant market position within the Aviation and Defense Cyber Security market, capturing more than a 64.3% share. This segment’s leadership can be attributed to several critical factors.

The increasing complexity and frequency of cyber threats specifically targeting the aviation and defense sectors necessitate robust cybersecurity solutions. These solutions include advanced threat detection systems, firewall management, intrusion detection systems, and other security software designed to protect sensitive data and operations from cyber-attacks.

Growing emphasis on securing critical infrastructure has led to significant investments in cybersecurity solutions by both government and private entities in the aviation and defense industries. These investments are driven by the need to adhere to stringent regulatory requirements and to safeguard against potential security breaches.

The adoption of IoT, cloud computing, and AI in these sectors has expanded the attack surface, rendering traditional security measures inadequate. This has led to a demand for advanced, integrated security solutions that can adapt to new threats and provide comprehensive protection against various cyber risks.

Deployment Analysis

In 2023, the On-premise segment held a dominant market position in the Aviation and Defense Cyber Security market, capturing more than a 72.5% share. This leadership stems primarily from the stringent security requirements and sensitive nature of data handled within these sectors.

On-premise solutions are preferred because they offer enhanced control over security measures and data management, a critical factor for military and aviation operations where data confidentiality and integrity are paramount.

The reliance on on-premise cyber security solutions in aviation and defense is also driven by regulatory compliance demands. Many regulations specific to these industries mandate strict data residency and protection guidelines, which are more reliably met through on-premise architectures.

Additionally, the on-premise deployment model is favored due to its ability to be customized to specific organizational needs. Aviation and defense entities often operate under unique operational conditions and face specific threat vectors that might not be effectively addressed by cloud-based solutions.

Application Analysis

In 2023, the Commercial Aviation segment held a dominant market position in the Aviation and Defense Cyber Security Market, capturing more than a 36.4% share. This leadership can be attributed to several pivotal factors that underscore the critical nature of cyber security in this sector.

The increase in digitalization of operations in commercial aviation has expanded the cyber attack surface. Airlines, airports, and service providers have increasingly integrated digital technologies for everything from booking systems and passenger data management to flight operations and crew scheduling. The evolving nature of cyber threats, such as ransomware and phishing attacks, specifically targeting the aviation sector, has put additional pressure on commercial aviation companies.

Financial repercussions of cyber attacks in commercial aviation are substantial. Incidents of data breaches or system disruptions can lead to severe financial losses due to operational downtime, legal penalties, and compromised customer trust. The high cost of potential breaches incentivizes investment in advanced cyber security solutions, further propelling the dominance of this segment.

Key Market Segments

By Component

- Solution

- Services

By Deployment

- Cloud

- On-premise

By Application

- Commercial Aviation

- Military Aviation

- Defence Contractors

- Government Agencies

Driver

Escalating Cyber Threats

The aviation and defense sectors are increasingly targeted by sophisticated cyberattacks, including ransomware, data breaches, and advanced persistent threats (APTs). These attacks aim to disrupt operations, steal sensitive information, and compromise national security. The aviation industry has witnessed a rise in cybercrimes, such as ransomware attacks on airlines and data breaches involving passenger information.

Also, defense organizations face threats from state-sponsored actors seeking to infiltrate critical systems. This growing threat landscape necessitates robust cybersecurity measures to protect vital infrastructure and maintain operational integrity.

Restraint

Integration Challenges

Implementing comprehensive cybersecurity solutions in aviation and defense is complex due to the integration of advanced technologies like IoT, AI, and cloud computing. These technologies, while enhancing operational efficiency, introduce new vulnerabilities.

The Internet of Military Things (IoMT) connects various devices, increasing the attack surface and potential entry points for adversaries. Ensuring seamless integration without compromising security requires significant investment in time, resources, and expertise, posing a restraint on rapid cybersecurity advancements.

Opportunity

Developing Advanced Intrusion Detection Systems (IDS)

A significant opportunity lies in developing advanced intrusion detection systems (IDS) tailored to the unique architectures of aviation and defense networks. Traditional IDS often fall short in these environments due to specialized communication protocols and stringent real-time performance requirements.

By creating IDS solutions that integrate seamlessly with existing systems and address specific vulnerabilities, organizations can enhance their cyber resilience. This approach not only mitigates potential threats but also aligns with the sectors’ operational demands, ensuring both security and efficiency. Investing in such specialized cybersecurity solutions is essential for safeguarding critical infrastructure against evolving cyber adversaries.

Challenge

Evolving Cyber Threats and Advanced Persistent Threats (APTs)

A significant challenge in aviation and defense cybersecurity is the rise of advanced persistent threats (APTs). These threats are often state-sponsored or highly sophisticated groups that continuously target systems with the intent of stealing sensitive data or disrupting operations over a long period. Unlike typical cyberattacks, APTs can bypass traditional security defenses, making them harder to detect.

This poses a major concern for both industries, as it could jeopardize critical infrastructure like flight control systems in aviation or military command networks in defense. The challenge lies not only in defending against these sophisticated attacks but also in the ability to adapt to rapidly evolving tactics used by attackers.

Emerging Trends

The aviation and defense sectors are increasingly integrating advanced technologies, leading to a heightened focus on cybersecurity.

Emerging technologies such as machine learning, 5G telecommunications, electric vertical takeoff and landing (eVTOL) aircraft, autonomous systems, and increased space utilization are contributing to this complexity. As these technologies become more prevalent, the aviation industry’s cybersecurity risk management is on rise, becoming more intricate.

The adoption of cloud computing, Internet of Things (IoT) devices, and artificial intelligence (AI) has led to an increased reliance on technology in the aerospace and defense industries. While these advancements offer significant benefits, they also present opportunities for disruption through a larger attack surface and an increased potential for cyberattacks.

A value-driven approach focuses on aligning cybersecurity initiatives with business value and strategic goals, thereby making cybersecurity a core business enabler rather than a burden. This approach emphasizes the importance of self-innovation within organizations to address the evolving cyber threat landscape effectively.

Business Benefits

- Enhanced Operational Safety: Implementing cybersecurity measures ensures the integrity of critical systems, reducing risk of disruptions that could compromise safety. This proactive approach helps prevent incidents that might endanger lives and assets.

- Protection of Sensitive Information: Safeguarding data from unauthorized access is crucial. Effective cybersecurity prevents breaches that could lead to the loss of intellectual property or sensitive information, thereby maintaining trust with stakeholders.

- Regulatory Compliance: Adhering to cybersecurity standards and regulations is essential to avoid legal penalties and maintain operational licenses. Compliance demonstrates a commitment to security and can enhance an organization’s reputation.

- Financial Stability: Investing in cybersecurity can prevent costly incidents such as data breaches or system outages, which might lead to financial losses. By mitigating these risks, organizations protect their bottom line.

- Competitive Advantage: Companies known for strong cybersecurity practices are more attractive to partners and customers. This reputation can lead to increased business opportunities and a stronger position in the market.

Regional Analysis

In 2023, North America held a dominant market position in the Aviation and Defense Cyber Security market, capturing more than a 42% share and generating revenues of USD 8.2 billion. This region’s leadership can be attributed to several pivotal factors that reinforce its top standing in the global market.

North America is home to some of the world’s largest defense contractors and aviation companies, which invest heavily in cybersecurity to protect critical military and commercial aviation systems. The high concentration of these technologically advanced enterprises drives substantial demand for cybersecurity solutions, ensuring robust market growth.

The United States government enforces stringent cybersecurity regulations and standards that govern both the defense and aviation sectors. These regulations mandate security measures to safeguard sensitive data and infrastructure from cyber threats, thus driving the adoption of advanced cybersecurity solutions.

Agencies such as the Department of Defense (DoD) and the Federal Aviation Administration (FAA) continuously update these standards to address emerging cyber threats, which in turn propels the market growth.The region’s commitment to national security and the defense sector’s heavy reliance on cyber technologies further amplify this need.

The high level of technological adoption in North America, including the integration of IoT, AI, and cloud technologies in defense and aviation systems, contributes to an expanded threat landscape that requires enhanced cybersecurity measures. This technological advancement, coupled with ongoing R&D activities in cybersecurity, supports the sustained investment and innovation within this region.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

In the Aviation and Defense Cyber Security market, several key players stand out for their contributions and innovations.

IBM has established itself as a powerhouse in the cyber security sector, especially within aviation and defense. Known for its advanced analytics and integrated security solutions, IBM provides a range of services that help protect critical infrastructure and sensitive data.

Honeywell International is another major player, renowned for its expertise in creating secure environments for aerospace operations. Honeywell’s cyber security solutions are integral to its broader automation and control technologies, offering layered security that encompasses network solutions and endpoint security.

CACI International Inc. specializes in providing information solutions and services to the defense and intelligence sectors. Their cyber security solutions focus on securing sensitive information against a wide array of cyber threats. CACI’s strength lies in its deep understanding of national security needs and its ability to tailor solutions that enhance operational capabilities while ensuring security compliance.

Top Key Players in the Market

- IBM

- Honeywell International

- CACI International Inc

- Collins Aerospace

- Leidos

- Palo Alto Networks

- BAE Systems PLC

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Harris Corporation

- Other Key Players

Recent Developments

- United Electronic Industries (UEI) made a significant move in July 2023 by launching new cybersecurity solutions tailored for its data collection, testing, and control equipment. These tools are built to meet the stringent security demands of aerospace and defense industries, including advanced applications like Unmanned Aerial Vehicles (UAVs). This launch highlights UEI’s commitment to addressing the growing cybersecurity concerns in critical sectors.

- In the same month, Honeywell acquired SCADAfence, a leader in Operational Technology (OT) and IoT cybersecurity. SCADAfence brings cutting-edge expertise in asset discovery, threat detection, and security governance, all crucial for managing cybersecurity in industrial operations and large-scale building systems. This acquisition strengthens Honeywell’s position in the industrial cybersecurity market, reinforcing its ability to protect critical infrastructure.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 19.5 Bn |

| Forecast Revenue (2033) | USD 57.4 Bn |

| CAGR (2024-2033) | 11.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Solution , Services), By Deployment (Cloud, On-premise), By Application (Commercial Aviation, Military Aviation, Defence Contractors, Government Agencies) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | IBM, Honeywell International, CACI International Inc, Collins Aerospace, Leidos, Palo Alto Networks, BAE Systems PLC, Lockheed Martin Corporation, Northrop Grumman Corporation, Harris Corporation, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |