Quick Navigation

Report Overview

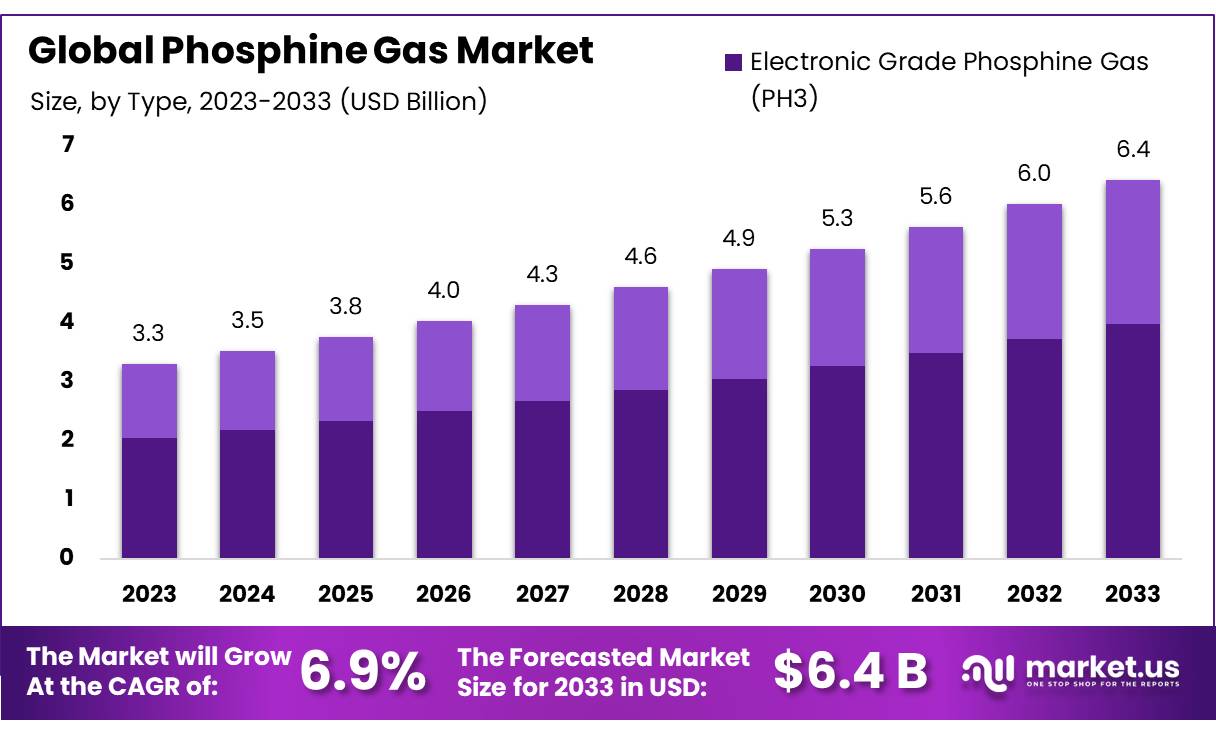

The Global Phosphine Gas Market size is expected to be worth around USD 6.4 Bn by 2033, from USD 3.3 Bn in 2023, growing at a CAGR of 6.9% during the forecast period from 2024 to 2033.

Phosphine gas (PH₃) is a colorless, flammable, and toxic compound primarily used in agriculture, electronics, and chemical industries. Its high reactivity and reducing properties make it an essential fumigant, semiconductor dopant, and intermediate for chemical synthesis. Derived from the reaction of phosphorus with strong bases or acids, phosphine gas plays a crucial role in pest control, particularly in grain storage, and advanced manufacturing processes such as semiconductors and LEDs.

The agriculture sector is the largest consumer of phosphine gas, accounting for over 65% of its demand due to its use as a fumigant to protect stored grains and prevent pest infestations. Meanwhile, the electronics industry is rapidly expanding its use of phosphine as a doping agent in semiconductor manufacturing, driven by the global shift toward advanced electronic devices.

The primary growth driver for the phosphine gas market is the increasing need for efficient pest control solutions in agriculture. With global grain production exceeding 2.8 billion metric tons in 2022, the importance of safe storage and protection from pests has surged. Phosphine gas offers a cost-effective and residue-free alternative to traditional pesticides, aligning with stringent regulatory standards.

Additionally, the booming electronics industry, with global semiconductor sales reaching over USD 600 billion in 2022, has propelled the demand for high-purity phosphine gas. The rising adoption of electric vehicles (EVs), smart devices, and renewable energy technologies further contributes to the growth of this segment.

A significant trend in the phosphine gas market is the development of advanced fumigation technologies. Innovations in controlled-release formulations and portable fumigation systems enhance efficiency and safety, reducing risks associated with handling this toxic gas. The integration of phosphine in eco-friendly pest control solutions is also gaining traction.

Key Takeaways

- Phosphine Gas Market Market size is expected to be worth around USD 6.4 Bn by 2033, from USD 3.3 Bn in 2023, growing at a CAGR of 6.9%.

- Electronic Grade Phosphine Gas (PH₃) held a dominant market position, capturing more than a 62.1% share of the overall market.

- 5N (99.999% purity) held a dominant market position, capturing more than a 47.1% share.

- Electronic-grade phosphine gas held a dominant market position, capturing more than a 53.1% share.

- Semiconductor applications held a dominant market position, capturing more than a 38.4% share.

- Electronic Use held a dominant market position, capturing more than a 68.3% share of the total phosphine gas market.

- North America dominated the global phosphine gas market, holding a substantial share of 35.3%, valued at approximately USD 1.1 billion.

Business Environment Analysis

The business environment for phosphine gas is significantly influenced by regulatory measures aimed at ensuring safe handling, storage, and application. Governments and international agencies impose stringent guidelines, especially in its use as a fumigant for grain storage.

These regulations, such as those under the Food and Agriculture Organization (FAO) and regional pesticide control boards, have increased compliance costs for manufacturers but also ensured the market’s credibility and sustainability. The growing emphasis on environmentally friendly pest control methods has further pushed companies to innovate residue-free fumigation solutions.

Global economic growth, particularly in developing regions, has boosted grain production and storage needs, directly impacting phosphine gas demand. With global grain production exceeding 2.8 billion metric tons in 2022, effective pest control has become a priority. Simultaneously, the electronics industry’s rapid growth, driven by increasing semiconductor production and the adoption of renewable energy technologies, has expanded the use of high-purity phosphine in advanced manufacturing processes.

Technological advancements are reshaping the phosphine gas market, particularly in its applications. Innovations in fumigation methods, such as controlled-release formulations and automated systems, are enhancing operational safety and efficiency. In the electronics sector, developments in doping technologies for semiconductors and photovoltaic cells have expanded phosphine’s application scope.

Rising food security concerns and global population growth are key socio-political factors influencing the phosphine gas market. Governments and industries are investing in advanced pest management solutions to reduce post-harvest losses. Additionally, geopolitical tensions and trade regulations can affect the supply chain, particularly for raw materials like phosphorus.

By Type

In 2023, Electronic Grade Phosphine Gas (PH₃) held a dominant market position, capturing more than a 62.1% share of the overall market. This strong position can be attributed to its widespread use in the semiconductor and electronics industries. Electronic Grade Phosphine Gas is critical in the production of semiconductor devices, such as integrated circuits, where high purity is essential for the manufacturing process. The increasing demand for advanced electronics and the growth of the semiconductor market have contributed to the steady rise in the demand for this grade of phosphine gas.

Technical Grade Phosphine Gas (PH₃), on the other hand, accounted for the remaining share of the market in 2023. It held a significant portion of the market as well, primarily driven by its application in agricultural fumigation, metal and chemical industries, and certain manufacturing processes. The demand for Technical Grade Phosphine Gas has remained steady, with growth attributed to its use as a fumigant for pest control in stored grain and other agricultural products. Moreover, it is employed in the production of chemicals and as a reducing agent in the metal industry.

By Product Type

In 2023, 5N (99.999% purity) held a dominant market position, capturing more than a 47.1% share of the overall phosphine gas market. This grade of phosphine gas is highly sought after for its superior purity, making it ideal for industries where high precision is required, such as semiconductor manufacturing and specialized electronics. The rise in demand for high-quality components in these sectors, along with technological advancements, has fueled the growth of 5N phosphine gas. As the semiconductor industry continues to expand globally, particularly in regions like Asia-Pacific, 5N phosphine gas is expected to maintain its leading position in the coming years.

In contrast, 4N (99.99% purity) and 6N (99.9999% purity) have also carved out specific niches within the market. In 2023, 4N phosphine gas accounted for a notable share, driven by its cost-effectiveness for industrial applications where ultra-high purity is not a strict requirement. It is commonly used in agricultural fumigation and some chemical processes, which helped maintain its steady demand. However, the market share of 4N is expected to gradually decline as the focus on higher purity grades, particularly 5N and 6N, continues to grow.

6N phosphine gas, despite being the highest purity grade, held a smaller portion of the market in 2023. This is primarily due to its high cost, which limits its use to niche applications in research and highly specialized industrial processes. The demand for 6N phosphine gas is expected to grow modestly over the next few years, driven by increasing research activities and advancements in nanotechnology and materials science. However, its share will likely remain smaller compared to 5N, given the broader application range and more cost-effective nature of the latter.

By Grade

In 2023, Electronic-grade phosphine gas held a dominant market position, capturing more than a 53.1% share of the total market. This grade is highly valued for its exceptional purity, making it essential for high-precision applications in industries like semiconductor manufacturing and advanced electronics. As the demand for smaller, more powerful electronic devices continues to grow, particularly in regions with a strong presence of tech companies such as North America and Asia-Pacific, the use of Electronic-grade phosphine gas has risen steadily. The growing trend of miniaturization in electronics, coupled with innovations in semiconductor technologies, has driven the increased adoption of this high-purity gas in the production of microchips and integrated circuits.

In comparison, Technical-grade phosphine gas captured a significant share of the market in 2023, serving a wide range of industrial applications. It is commonly used in agriculture as a fumigant, as well as in the production of specialty chemicals and pharmaceuticals. While it does not match the purity of electronic-grade phosphine, Technical-grade phosphine offers sufficient quality for these applications and remains in demand due to its versatility and cost-effectiveness.

Industrial-grade phosphine gas, while accounting for a smaller share, also plays an important role in industries like metalworking, oil refining, and the manufacture of phosphorous-based chemicals. This grade is typically used in processes that do not require the high purity levels needed in electronics or specialized manufacturing, making it a more affordable alternative for large-scale industrial operations.

By Application

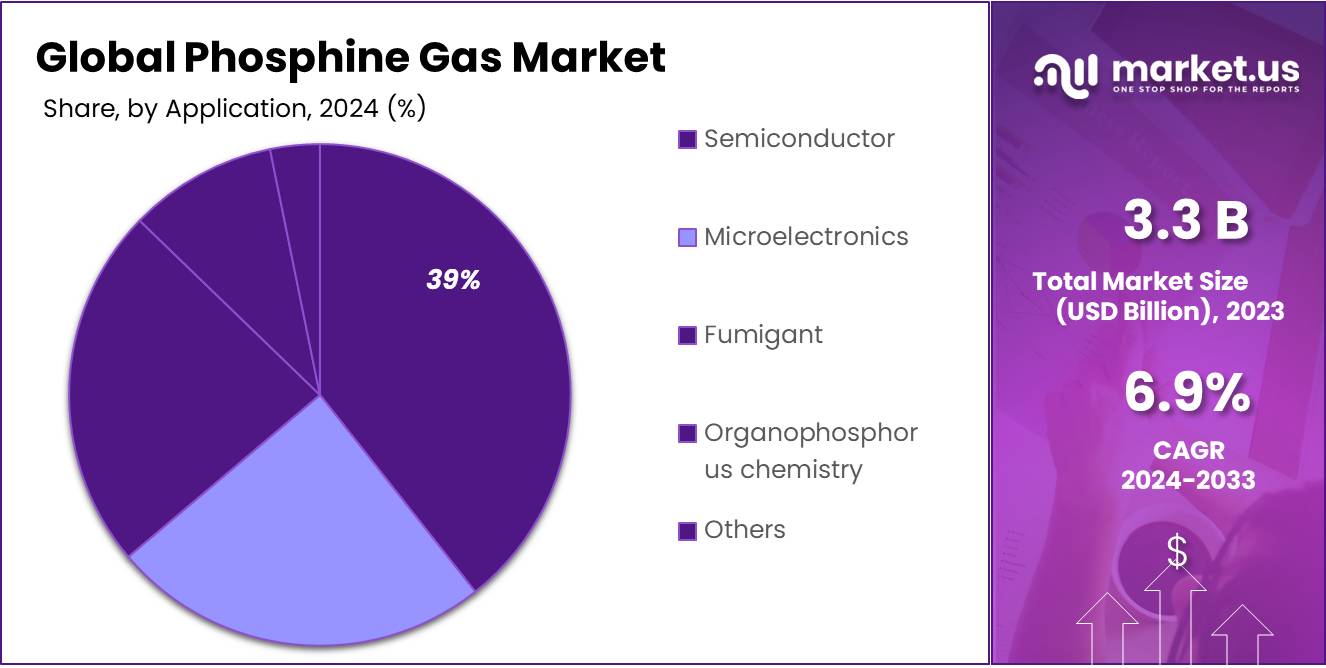

In 2023, Semiconductor applications held a dominant market position, capturing more than a 38.4% share of the overall phosphine gas market. This significant share is driven by the increasing demand for high-performance semiconductors in various electronic devices, such as smartphones, computers, and consumer electronics. Phosphine gas, particularly in high-purity forms, plays a crucial role in the production of semiconductor components, including the deposition of thin films and the etching process. As global semiconductor manufacturing continues to expand, especially in emerging markets and technologically advanced regions, the demand for phosphine gas in this sector has been steadily increasing.

Following semiconductor applications, the fumigant sector accounted for a considerable portion of the market in 2023, with a steady rise in demand driven by its effectiveness in pest control in agriculture and storage. The application of phosphine as a fumigant is crucial in ensuring the safety and longevity of stored grains, fruits, and other commodities. Additionally, sectors like organophosphorus chemistry, which involve the production of chemical compounds for agrochemicals and pharmaceuticals, continue to show a steady need for phosphine gas, contributing to its growing role in global chemical production.

Microelectronics and other niche applications also make up smaller but significant segments of the market, with each experiencing gradual growth as technologies evolve and diversify. Overall, as the range of applications for phosphine gas broadens, it is expected that the semiconductor sector will continue to maintain a leading role in the market.

By End Users

In 2023, Electronic Use held a dominant market position, capturing more than a 68.3% share of the total phosphine gas market. This dominance is primarily due to the widespread use of phosphine gas in the electronics and semiconductor industries, where it is used for processes such as chemical vapor deposition (CVD), doping of semiconductor materials, and other precision manufacturing techniques.

As the demand for more advanced and smaller electronic devices continues to rise, especially in sectors like consumer electronics, telecommunications, and computing, the need for high-purity phosphine gas has increased significantly. The growing trend of miniaturization and the need for faster, more efficient electronic devices are key factors fueling the strong demand in this segment.

Non-Electronic Use, while a smaller segment, also plays a crucial role in various industries, including agriculture and chemical manufacturing. However, its market share remains significantly lower compared to Electronic Use, with growth driven mainly by applications such as fumigation and pesticide production. Despite this, the Non-Electronic Use sector is expected to maintain steady growth in line with agricultural demand, particularly in regions focused on crop protection.

Key Market Segments

By Type

- Electronic Grade Phosphine Gas (PH3)

- Technical Grade Phosphine Gas (PH3)

By Product Type

- 4N

- 5N

- 6N

By Grade

- Electronic

- Technical

- Industrial

By Application

- Organophosphorus chemistry

- Microelectronics

- Fumigant

- Semiconductor

- Others

By End Users

- Non Electronic Use

- Electronic Use

Drivers

Growing Demand for Phosphine Gas in Fumigation

One of the major driving factors behind the increased demand for phosphine gas is its critical role in the fumigation of grains and other stored food products. The global need for effective pest control in the food supply chain, especially in grain storage and transportation, has led to a steady rise in the consumption of phosphine gas, which is recognized for its ability to effectively kill a broad range of pests, including insects and rodents, without leaving harmful residues.

Phosphine gas is primarily used in the form of pellets or tablets in sealed environments, such as storage silos, shipping containers, and warehouses, to safeguard the quality of stored grains. It’s highly effective because it diffuses easily and penetrates through stored goods, making it ideal for fumigating bulk commodities like wheat, rice, and maize. This method has become the standard in pest control in global agricultural markets, as it offers a reliable and cost-effective way to preserve the integrity of the food supply chain.

In 2023, global grain production reached approximately 2.8 billion metric tons, according to the Food and Agriculture Organization (FAO). This enormous volume of grain requires efficient pest management systems to prevent significant losses. The World Health Organization (WHO) states that between 5% to 10% of global food production is lost due to pest damage, particularly during storage. This alarming statistic underscores the importance of fumigation and, by extension, phosphine gas, as it plays a key role in preventing such losses and maintaining the quality of food products.

Government initiatives also contribute to the increased use of phosphine gas in agriculture. For instance, in many countries, agriculture and food safety regulators have established guidelines for the use of phosphine gas to ensure food safety and minimize pesticide residues. In the United States, the Environmental Protection Agency (EPA) provides specific recommendations on how to safely use phosphine for grain fumigation, including safety standards for both workers and consumers. These regulations help bolster the adoption of phosphine in agricultural settings, making it a preferred choice for fumigation.

Furthermore, organizations such as the Food and Agriculture Organization (FAO) and the International Plant Protection Convention (IPPC) have also recognized the importance of phosphine gas in global food security efforts. The FAO has highlighted the need for effective pest management systems to ensure that grain reserves are not compromised by infestations, particularly in countries with large-scale agricultural outputs, such as the United States, India, and Brazil. These organizations have consistently emphasized the critical role of phosphine in achieving food security, especially for developing nations with large agricultural sectors.

Additionally, emerging markets in Asia, Latin America, and Africa, where grain production is steadily increasing, are seeing a rising demand for phosphine as a fumigant. For instance, in India, one of the world’s largest producers of wheat and rice, the government has implemented widespread fumigation programs to protect stored grains from pests. According to the Indian Ministry of Agriculture and Farmers Welfare, India produces approximately 106 million metric tons of wheat annually, a significant portion of which is fumigated using phosphine gas to prevent pest damage.

The effectiveness of phosphine gas in pest control, coupled with its regulatory support, has made it the go-to solution for post-harvest pest management in the food industry. It ensures the safe transport and storage of food products, ultimately contributing to global food security. As agricultural production continues to grow to meet the demands of a rising global population, the reliance on phosphine for fumigation is expected to keep expanding.

Restraints

Health and Environmental Concerns

Despite its effectiveness as a fumigant, one of the key restraining factors for the growth of the phosphine gas market is the growing concern over its potential health and environmental risks. Phosphine is a highly toxic gas that can pose significant risks to human health if not handled properly. Exposure to high concentrations of phosphine can lead to severe symptoms, including respiratory distress, nausea, dizziness, and in extreme cases, death. As a result, stricter regulations and safety standards are being imposed globally, which could limit the widespread use of phosphine gas in industries like agriculture and food storage.

The food industry, particularly in grain storage, has become increasingly aware of the risks associated with phosphine fumigation. Although phosphine is highly effective in pest control, the fact that it is toxic to humans and animals has led many organizations to seek safer alternatives. For instance, the U.S. Environmental Protection Agency (EPA) has set regulations on the use of phosphine gas in food storage, citing its toxicity and potential long-term environmental impact. In 2020, the EPA issued a report indicating that the use of fumigants, including phosphine, in grain storage facilities had to comply with stringent guidelines to ensure the safety of both workers and the environment. The report emphasized that exposure levels must be minimized, and proper protective equipment should always be worn by those handling the gas.

Moreover, several international food safety organizations, such as the Food and Agriculture Organization (FAO) and the World Health Organization (WHO), have raised concerns over the long-term effects of phosphine use in the food supply chain. However, the report also stresses the need for more research into alternative, safer methods of pest control that don’t involve toxic chemicals like phosphine. The increasing awareness and concerns surrounding this issue are prompting governments and industry players to explore safer alternatives, such as heat treatment and carbon dioxide fumigation.

The restrictions on the use of phosphine gas also extend to environmental considerations. Phosphine can contribute to air pollution if released into the atmosphere during fumigation processes. This is a growing concern in agricultural regions where large-scale fumigation is common.

For example, in Australia, where grain exports are a major part of the economy, there have been calls for reduced phosphine usage due to its potential environmental impact. The Australian Pesticides and Veterinary Medicines Authority (APVMA) has been working closely with industry stakeholders to develop guidelines that minimize the release of phosphine gas into the environment.

In addition to these regulations, public pressure on companies and governments to ensure more sustainable agricultural practices is also increasing. According to the Food and Agriculture Organization (FAO), the environmental impact of chemicals used in agriculture, including phosphine, is one of the main reasons for the adoption of organic farming practices in several regions.

Organic farming, which avoids synthetic pesticides and fumigants, is becoming more popular as consumers increasingly demand cleaner, safer food. The FAO reports that the area under organic certification has grown significantly over the past decade, particularly in Europe and North America, as part of a broader trend towards sustainability in agriculture.

Phosphine gas, due to its toxic and environmental risks, faces growing pressure from regulatory bodies and food safety organizations to be phased out or replaced with safer alternatives. In 2021, the International Code of Conduct on Pesticide Management, a framework supported by the FAO, WHO, and the World Trade Organization (WTO), emphasized the need for pest control methods that minimize harm to human health and the environment. This reflects a broader push towards reducing chemical dependency in agriculture and food storage.

Opportunity

Rising Demand for Food Security and Grain Storage

One of the major growth opportunities for phosphine gas lies in its application within the food security sector, particularly in grain storage and fumigation. The global population continues to grow at a rapid pace, and with it, the demand for food, especially staple crops like grains.

According to the Food and Agriculture Organization (FAO), food production will need to increase by 60% by 2050 to meet the nutritional needs of an estimated 9.7 billion people. This presents a significant challenge, particularly in regions where food storage practices are not optimal, leading to post-harvest losses due to pests and insects.

Phosphine gas has long been a go-to solution for fumigating stored grains like wheat, rice, and corn, ensuring that pests do not ruin crops while they are in storage. As demand for grain and other agricultural products increases, the need for effective pest management strategies becomes even more critical. Phosphine remains one of the most widely used fumigants due to its efficacy in controlling pests at various stages of their life cycle. Additionally, it leaves no chemical residues on the crops, which makes it an attractive option for food safety.

According to a report by the FAO, about 25% of the world’s harvested food is lost or wasted annually, and a large portion of this loss is attributed to pest infestations during storage. As countries work to address these challenges and improve food security, they are turning to more effective and environmentally sustainable solutions like phosphine gas for pest control in storage facilities.

In addition, many government initiatives and regulations are pushing for improvements in food storage, which could further stimulate the demand for phosphine. For example, in the United States, the Department of Agriculture (USDA) has been promoting better storage practices to reduce food waste, with particular focus on grain storage. The USDA’s National Institute of Food and Agriculture (NIFA) supports research into improving grain storage technologies and pest management, which includes the safe use of fumigants like phosphine.

The use of phosphine is also expanding in developing countries where grain storage and pest management practices are less developed. In regions such as Africa and Southeast Asia, where post-harvest losses can reach up to 30-40%, the introduction of better pest control methods, including phosphine fumigation, presents a significant opportunity for growth. In fact, a study by the United Nations Conference on Trade and Development (UNCTAD) found that post-harvest losses could be reduced by 10-20% with the proper implementation of pest control methods, including fumigation with phosphine gas.

Trends

Increasing Adoption of Phosphine Gas for Sustainable Fumigation Practices

A major trend shaping the phosphine gas market today is the increasing adoption of more sustainable and eco-friendly fumigation practices in agriculture. Phosphine, once known for its toxic properties, is now being recognized as a more environmentally viable alternative compared to other chemical fumigants. This shift is driven by the growing emphasis on reducing the environmental impact of agricultural practices while maintaining food security.

The adoption of sustainable fumigation practices using phosphine gas is becoming more prevalent, particularly in regions with significant agricultural output, such as Asia-Pacific and North America.

According to the Food and Agriculture Organization (FAO), more than 1.5 billion tons of grain are produced annually worldwide, with a large portion being stored for months or even years. The need for efficient pest control during this storage period is paramount, but the agricultural industry is under increasing pressure to balance the benefits of pest control with the need to minimize environmental harm.

One key factor driving this trend is the increasing regulations surrounding the use of hazardous chemicals in agriculture. In response to growing concerns about the toxicity and environmental impact of traditional fumigants like methyl bromide, several governments and industry groups have moved toward promoting safer alternatives, including phosphine gas.

The International Plant Protection Convention (IPPC), a global body that works under the FAO, has set guidelines encouraging the use of phosphine as a safer, more sustainable fumigant. This has contributed to its growing popularity in grain storage, as it provides an effective method to control pests without leaving harmful residues that can contaminate food.

Another contributing factor is the rising demand for organic food and the pressure to reduce pesticide use. According to the Research Institute of Organic Agriculture (FiBL), the global organic food market reached a value of over USD 120 billion in 2020, and it continues to grow. This trend has pushed the agriculture industry to seek fumigation alternatives that are compatible with organic farming standards, and phosphine gas has become an increasingly popular choice. It is used in organic grain storage practices to ensure pest-free products without compromising the integrity of organic certification.

In terms of sustainability, phosphine gas also offers a significant reduction in the carbon footprint compared to other fumigants. For example, methyl bromide, which has been widely used in the past, is a potent ozone-depleting substance that contributes to climate change. The Montreal Protocol, an international treaty aimed at protecting the ozone layer, has led to the phasing out of methyl bromide, further encouraging the use of phosphine gas as a more environmentally friendly option.

Governments are supporting this transition through various initiatives. In the U.S., the Environmental Protection Agency (EPA) has endorsed phosphine as a safe alternative for use in grain storage, provided it is used according to recommended safety guidelines. In the European Union, regulations on pesticide use have become stricter, pushing the industry toward adopting alternatives like phosphine gas for pest control in grain storage facilities.

Regional Analysis

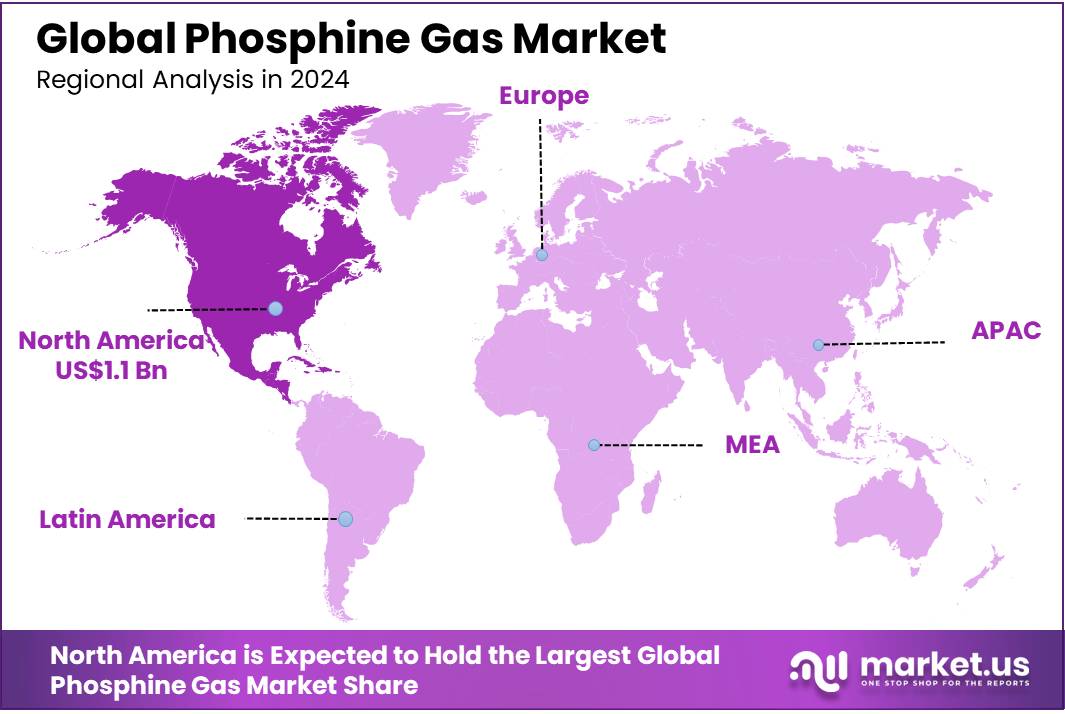

In 2023, North America dominated the global phosphine gas market, holding a substantial share of 35.3%, valued at approximately USD 1.1 billion. This region’s strong market position can be attributed to its well-established agricultural and food industries, where phosphine gas is widely used for grain fumigation. The demand for high-quality food storage solutions and pest control is projected to grow as North America continues to focus on improving food security and minimizing post-harvest losses. The presence of major agricultural producers, especially in the U.S. and Canada, further strengthens the market potential for phosphine gas in this region.

Europe follows closely, contributing a significant share to the global market. The region’s stringent food safety and environmental regulations have led to the adoption of more effective and sustainable fumigation methods, including phosphine gas. With robust agricultural practices and an increasing focus on organic and residue-free pest control, Europe is expected to maintain steady growth in demand.

In the Asia Pacific region, the phosphine gas market is rapidly expanding, driven by the rising demand for food storage in countries like India and China. These nations are major producers and consumers of grains, and the need for efficient fumigation solutions to prevent post-harvest losses is creating strong market growth. Asia-Pacific’s large population and agricultural sector are expected to contribute significantly to the global market share.

The Middle East & Africa and Latin America regions, while smaller in market size, are showing positive growth trends due to increasing agricultural practices and the need for pest control solutions in food production and storage.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The phosphine gas market is characterized by the presence of several key players who are driving innovation and competition in this sector. Air Products, a global leader in industrial gases, plays a significant role with its wide portfolio of products, including high-purity phosphine gas for semiconductor and industrial applications. BASF SE, another major player, offers a range of chemical solutions, including phosphine gas, primarily used in the fumigation and agricultural sectors. The company’s strong R&D capabilities and wide-reaching global presence enhance its position in the market.

Other prominent companies, such as Praxair Inc. and The Linde Group, are also significant contributors to the phosphine gas industry. Both companies are key players in the industrial gas market, offering various gases, including phosphine, to support sectors such as food preservation, semiconductor manufacturing, and agriculture.

Additionally, CYTEC SOLVAY GROUP and Gasco are active in supplying phosphine to industries focused on pest control and food security. Meanwhile, ATCO Atmospheric and Speciality Gases Private Limited and Nippon Chemical Industrial Co. Ltd. focus on providing high-purity phosphine for use in specialized applications, such as electronics and chemical processes.

Top Key Players

- Air Products

- Gas Detector Tubes

- ATCO Atmospheric And Speciality Gases Private Limited

- BASF SE

- Bhagwati Chemicals

- Chemicals Inc

- CYTEC SOLVAY GROUP

- FUGRAN

- Gasco

- Industrial Scientific

- Nippon Chemical Industrial CO. Ltd.

- Pentagon Chemicals

- Praxair Inc

- The Linde Group

Recent Developments

In 2023 Air Products revenue from gases and chemicals was around USD 11 billion, with a significant portion attributed to growth in the semiconductor and agricultural sectors, where phosphine gas is increasingly in demand.

In 2023 Gas Detector Tubes has seen a steady increase in demand for their products due to stricter safety guidelines and growing concerns about the toxic nature of phosphine.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 3.3 Bn |

| Forecast Revenue (2033) | USD 6.4 Bn |

| CAGR (2024-2033) | 6.9% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Electronic Grade Phosphine Gas (PH3), Technical Grade Phosphine Gas (PH3)), By Product Type (4N, 5N, 6N), By Grade (Electronic, Technical, Industrial), By Application (Organophosphorus chemistry, Microelectronics, Fumigant, Semiconductor, Others), By End Users (Non Electronic Use, Electronic Use) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Air Products, Gas Detector Tubes, ATCO Atmospheric And Speciality Gases Private Limited, BASF SE, Bhagwati Chemicals, Chemicals Inc, CYTEC SOLVAY GROUP, FUGRAN, Gasco, Industrial Scientific, Nippon Chemical Industrial CO. Ltd., Pentagon Chemicals, Praxair Inc, The Linde Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |