Quick Navigation

Report Overview

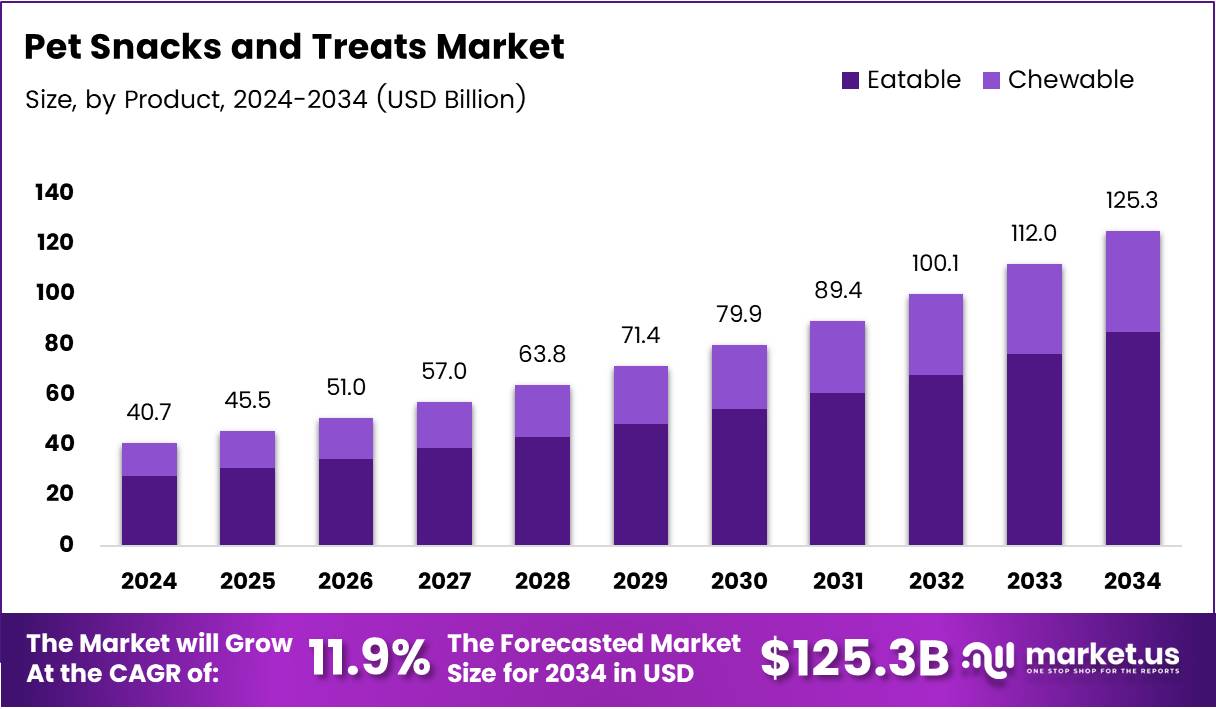

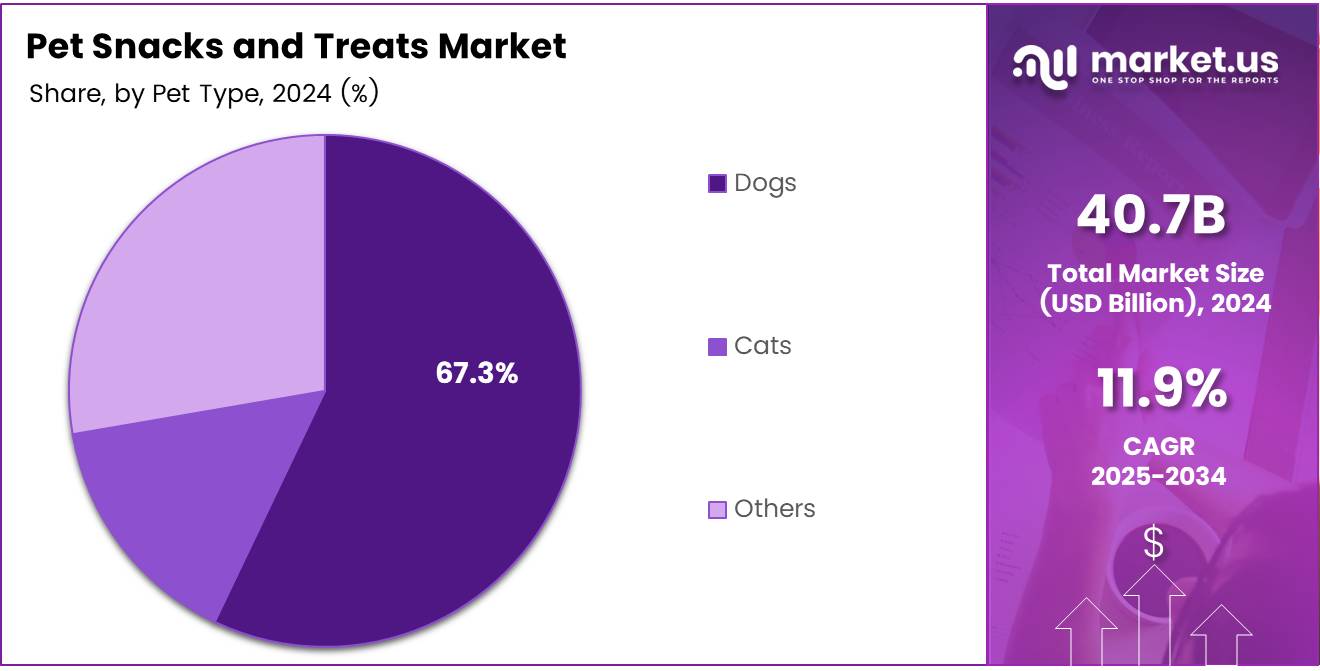

The Global Pet Snacks and Treats Market size is expected to be worth around USD 125.3 Billion by 2034, from USD 40.7 Billion in 2024, growing at a CAGR of 11.9% during the forecast period from 2025 to 2034. This growth is primarily fueled by increasing pet humanization, rising demand for premium and functional treats, and expanding e-commerce penetration.

Key Takeaways

- The Global Pet Snacks and Treats Market is projected to reach USD 125.3 Billion by 2034, growing at a CAGR of 11.9% from 2025 to 2034.

- Eatable products dominated the market in 2024, holding a 67.5% share due to their palatability and compatibility with daily routines.

- Pet Specialty Stores led the distribution channel segment in 2024, with a 42.3% market share, thanks to personalized service and specialized products.

- Dogs accounted for 67.3% of the pet snacks and treats market in 2024, driven by their prevalence in households and use of treats for various purposes.

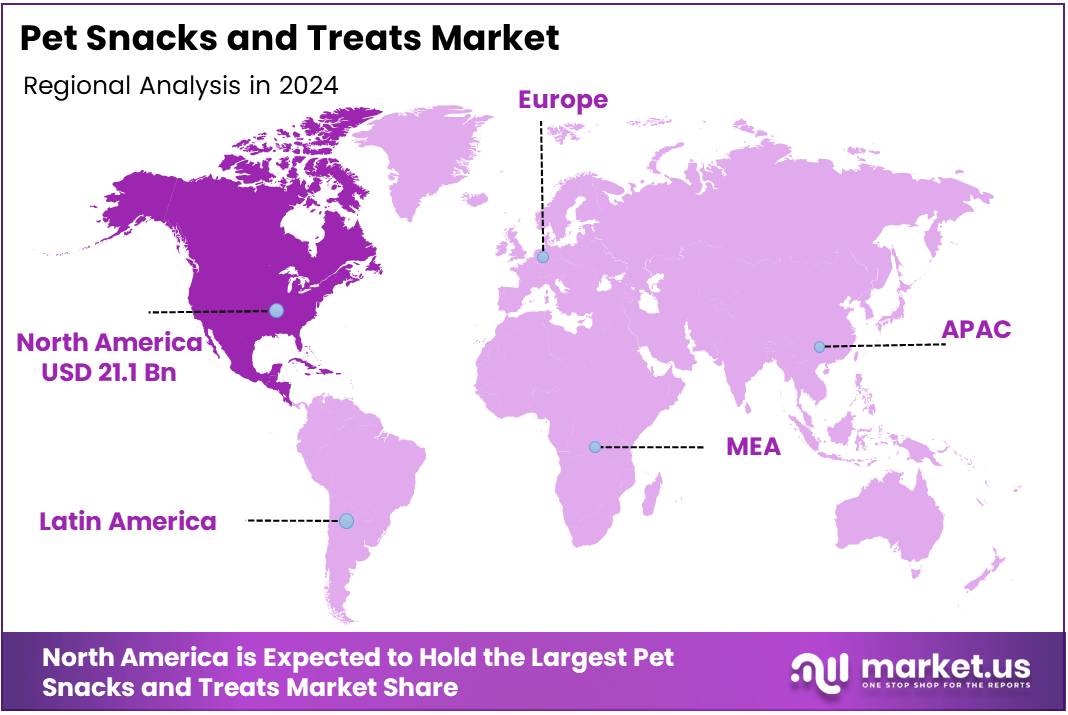

- North America held the leading market share of 52.7% in 2024, valued at USD 21.1 Billion, driven by high pet ownership and a preference for premium-grade snacks.

The pet snacks and treats market is a fast-evolving segment within the broader pet care industry, primarily driven by rising pet ownership, humanization of pets, and a shift toward premium and functional nutrition. With owners treating pets as family, demand for indulgent and health-oriented treats has surged globally.

According to Forbes, 66% of U.S. households, amounting to 86.9 million homes, own a pet—creating a massive consumer base. Dogs lead the ownership charts with 65.1 million U.S. households, followed by 46.5 million owning cats and 11.1 million keeping freshwater fish. This broad adoption continues to drive consistent demand for pet snacks.

Notably, pet treats are not just indulgent products—they often serve functional purposes such as dental health, anxiety relief, and nutritional supplementation. As consumers increasingly seek personalized pet products, this has opened up white spaces for organic, clean-label, and protein-enriched treats in both developed and emerging markets.

The U.S. holds a significant share of the global pet snacks market, but Europe is steadily gaining ground. According to GlobalPetIndustry, Europe accounts for 45% of total units sold in the pet treats category, while the U.S. represents 36% of worldwide sales, indicating a slight but impactful shift in consumer demand and market leadership.

Government support for animal welfare and pet nutrition regulations in Europe and North America has further professionalized this segment. Regulatory clarity has led to rising investments in clean ingredients, safety, and transparent labelling, offering consumers confidence and boosting premium treat adoption.

Simultaneously, growth opportunities are emerging in Asia-Pacific and Latin America as urbanization and middle-class income expansion fuel pet ownership. Manufacturers are targeting these regions through region-specific flavors, smaller pack sizes, and affordability-based segmentation, capitalizing on rising disposable incomes.

Innovation also plays a vital role. Brands are launching baked snacks, freeze-dried treats, and breed-specific formulations. This diversified offering not only increases shelf turnover but also helps brands build emotional loyalty with pet parents—a key market differentiator in this highly emotive segment.

E-commerce expansion has redefined purchase behavior, enabling direct-to-consumer (D2C) pet treat brands to gain momentum. With product personalization and subscription models, companies are leveraging data to deliver better user experiences and recurring revenue.

The pet snacks and treats market is clearly poised for steady long-term growth. By aligning with consumer expectations for health, sustainability, and convenience, businesses have ample runway to innovate and scale across multiple geographies.

Product Analysis

Eatable dominates with 67.5% due to strong consumer preference and versatility in formulations.

In 2024, Eatable held a dominant market position in By Product Analysis segment of Pet Snacks and Treats Market, with a 67.5% share. The popularity of these products is driven by their palatability, ease of portioning, and compatibility with both training and daily feeding routines.

Pet owners are increasingly choosing eatable treats as a functional food option, integrating vitamins and supplements into snacks, which further boosts demand in this segment. Their availability in various textures and flavors makes them more appealing to a wider range of pet types and preferences.

Chewable treats, while accounting for the remaining share, are still valued for their dental health benefits. However, their market penetration is limited compared to eatables due to fewer variations and use-case scenarios.

Distribution Channel Analysis

Pet Specialty Stores dominate with 42.3% due to targeted offerings and expert guidance.

In 2024, Pet Specialty Stores held a dominant market position in By Distribution Channel Analysis segment of Pet Snacks and Treats Market, with a 42.3% share. These outlets attract pet owners seeking personalized advice and specialized products, which has elevated trust and loyalty within this channel.

The stores often carry premium and niche snack brands not found in general retailers, enabling deeper market differentiation. Their tailored service approach also fosters repeat business and higher spending per visit.

Supermarkets and Hypermarkets continue to offer convenience and competitive pricing, while online platforms are rapidly growing due to doorstep delivery and subscription-based purchases.

Pet Type Analysis

Dogs dominate with 67.3% owing to their higher ownership rate and frequent treat usage.

In 2024, Dogs held a dominant market position in By Pet Type Analysis segment of Pet Snacks and Treats Market, with a 67.3% share. The segment’s strength comes from the sheer number of dog-owning households and their habitual use of treats for training, bonding, and health supplementation.

Dogs are also more likely to receive daily snacks compared to other pets, amplifying their demand in the market. This has prompted brands to launch an array of dog-specific flavors, formats, and nutritional profiles.

Cats account for a smaller portion due to their selective eating behavior, while the ‘Others’ category includes niche species, which although growing, have limited scale in comparison.

Key Market Segments

By Product

- Eatable

- Chewable

By Distribution Channel

- Pet Specialty Stores

- Supermarkets & Hypermarkets

- Online

- Others

By Pet Type

- Dogs

- Cats

- Others

Drivers

Rise in Humanization of Pets Influencing Purchase Behavior

Pet owners are increasingly treating their pets like family members, which is leading to higher spending on quality snacks and treats. This humanization trend encourages buyers to look for products that resemble human food in taste, texture, and nutrition, making premium options more popular.

Premiumization of pet snacks is becoming a key driver, with pet parents willing to pay more for treats that have added health benefits. Functional ingredients such as probiotics, omega-3 fatty acids, and vitamins are gaining traction as they support digestion, joint health, and overall wellness.

Urbanization and the rise in single-person households are also expanding pet ownership. These consumers often have higher disposable incomes and treat their pets as companions, contributing to a growing demand for convenient, high-quality snack options.

The market is also seeing rapid diversification with the introduction of novel protein sources such as insect protein, duck, and fish. These alternatives cater to pets with allergies or special dietary needs while appealing to sustainability-focused buyers.

Restraints

Limited Shelf Life of Organic and Natural Snack Variants

Organic and natural pet treats, while growing in popularity, often have a shorter shelf life due to the absence of preservatives. This can limit their distribution and make retailers cautious about stocking them in bulk.

High import duties on specialized or premium pet snacks can raise costs significantly. This makes these products less competitive in price-sensitive markets and can deter consumers from frequent purchases.

Consumers are also becoming more aware of artificial ingredients in pet treats, leading to skepticism around products that include preservatives, artificial colors, or flavors. This mistrust can slow down sales of non-natural options.

Global supply chains are facing disruptions due to geopolitical and economic factors. These issues affect the availability of key ingredients, particularly for specialized and health-focused pet snacks, limiting consistent product availability.

Growth Factors

Growth in Subscription-Based Pet Treat Delivery Models

Subscription-based delivery services for pet snacks are growing quickly. These services provide convenience, consistent supply, and customization, which appeals to busy pet owners and helps brands build loyalty.

There’s increasing demand for breed-specific nutrition, with pet owners now looking for treats that are tailored to their pets’ size, age, or health needs. Companies that offer customized formulations stand to gain a competitive edge.

Expanding into emerging markets in Asia and Latin America presents major growth opportunities. As pet ownership grows in these regions, so does the demand for high-quality treats, especially among younger and urban consumers.

Innovation in snack preparation methods—like freeze-drying and air-drying—is becoming a strong growth area. These methods preserve nutrients and improve shelf life, making the products more appealing to health-conscious buyers.

Emerging Trends

Incorporation of CBD and Adaptogens in Pet Edibles

The inclusion of CBD and adaptogens in pet snacks is a rising trend. These ingredients are believed to support anxiety relief, stress management, and overall pet wellness, appealing to owners who seek natural health solutions.

Transparency in sourcing and labeling is becoming a key focus. Consumers are increasingly choosing brands that clearly disclose where ingredients come from and how snacks are made, driving demand for cleaner labels.

Sustainability is another trending factor, with more brands investing in eco-friendly packaging. Zero-waste and biodegradable solutions are helping companies align with the values of environmentally conscious consumers.

Personalized and DNA-based snacks are an emerging innovation. These products use pet genetic data to create custom formulations, targeting specific health needs and increasing buyer confidence in product effectiveness.

Regional Analysis

North America Dominates the Pet Snacks and Treats Market with a Market Share of 52.7%, Valued at USD 21.1 Billion

North America held the leading position in the pet snacks and treats market, driven by high pet ownership rates and the growing trend of pet humanization. Consumers in the region increasingly opt for functional and premium-grade snacks, contributing to the region’s market dominance. In North America, the market was valued at USD 21.1 Billion, accounting for a 52.7% share, reflecting its robust consumption patterns and advanced retail infrastructure.

Europe Pet Snacks and Treats Market Insights

Europe continues to show steady growth, supported by rising awareness of pet nutrition and a strong preference for natural and organic pet products. Government regulations promoting pet welfare and the presence of mature pet food markets in Western Europe have further reinforced demand across the region.

Asia Pacific Pet Snacks and Treats Market Trends

Asia Pacific is emerging as a fast-growing region due to expanding pet adoption and increasing disposable incomes in countries like China, India, and Japan. Urbanization and shifting cultural attitudes toward pets are also contributing to rising expenditure on pet care and nutrition, especially in metropolitan areas.

Middle East and Africa Pet Snacks and Treats Market Overview

The Middle East and Africa region is gradually evolving, with growing awareness of pet care among the urban population. Although the market is still in its nascent stage, the increasing demand for premium pet snacks in countries with rising pet ownership is laying the groundwork for future growth.

Latin America Pet Snacks and Treats Market Outlook

Latin America shows moderate growth, supported by a rising number of middle-class pet owners and increased availability of pet snacks across retail channels. The region’s market is being shaped by economic developments and the growing influence of western pet care trends.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Pet Snacks and Treats Company Insights

In the rapidly growing global Pet Snacks and Treats Market in 2024, Merrick Pet Care stands out as a leading player, renowned for its premium, natural ingredients that appeal to health-conscious pet owners. Their commitment to high-quality, grain-free treats has made them a favored choice in the market.

Spectrum Brands, Inc. has a significant footprint in the industry, primarily through its brands such as Tetra and Dingo. The company focuses on providing a broad range of pet snacks that cater to various pet sizes and dietary preferences, ensuring strong brand loyalty across its customer base.

VAFO Group a.s. has become a prominent force, known for its innovative approach to creating natural, nutritious snacks for pets. With its focus on sustainable practices and high-quality production, VAFO continues to gain traction in global markets, especially in Europe.

Off-Leash Pet Treats is a rising player, making waves with their focus on all-natural, preservative-free treats that emphasize health and well-being. Their growth is largely driven by their strong commitment to eco-friendly packaging and a transparent production process, which resonates with increasingly conscientious consumers.

Each of these companies brings unique strengths to the pet snacks and treats sector, ensuring that the market remains competitive, dynamic, and attuned to consumer demands for quality and sustainability.

Top Key Players in the Market

- Merrick Pet Care

- Spectrum Brands, Inc.

- VAFO Group a.s.

- Off-Leash Pet Treats

- Colgate Palmolive Company

- Mars, Incorporated

- The J.M. Smucker Company

- Wellness Pet, LLC

- Nestlé S.A.

- General Mills Inc.

Recent Developments

- In February 2025, natural pet treat brand Dogsee Chew raised $8 million in a Series B funding round to expand its production capacity and strengthen its distribution network across global markets. The investment is expected to accelerate innovation in healthy, Himalayan cheese-based pet treats.

- In January 2024, pet-food start-up TABPS secured Rs 6.5 Crores in seed funding to scale its operations, enhance its research capabilities, and introduce functional nutrition products tailored for Indian pet owners. The funds will also support expansion into tier-2 and tier-3 cities.

- In September 2024, a fresh, insect-based dog food startup received $1.46 million in funding to boost eco-friendly pet nutrition solutions. The capital will be used to increase production, improve sustainable packaging, and broaden its market presence.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 40.7 Billion |

| Forecast Revenue (2034) | USD 125.3 Billion |

| CAGR (2025-2034) | 11.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Eatable, Chewable), By Distribution Channel (Pet Specialty Stores, Supermarkets & Hypermarkets, Online, Others), By Pet Type (Dogs, Cats, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Merrick Pet Care, Spectrum Brands, Inc., VAFO Group a.s., Off-Leash Pet Treats, Colgate Palmolive Company, Mars, Incorporated, The J.M. Smucker Company, Wellness Pet, LLC, Nestlé S.A., General Mills Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |