Global Pet Diabetes Care Market By Pet Type (Dogs, Cats and Others), By Product Type (Insulin, Glucose Monitoring Devices, Syringes and Pen Needles, Diabetic Food, Dietary Supplements and Others), By Distribution Channel (Veterinary Hospitals and Clinics, Retail Pharmacies, Online Pharmacies and Pet Specialty Stores), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182490

- Number of Pages: 378

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

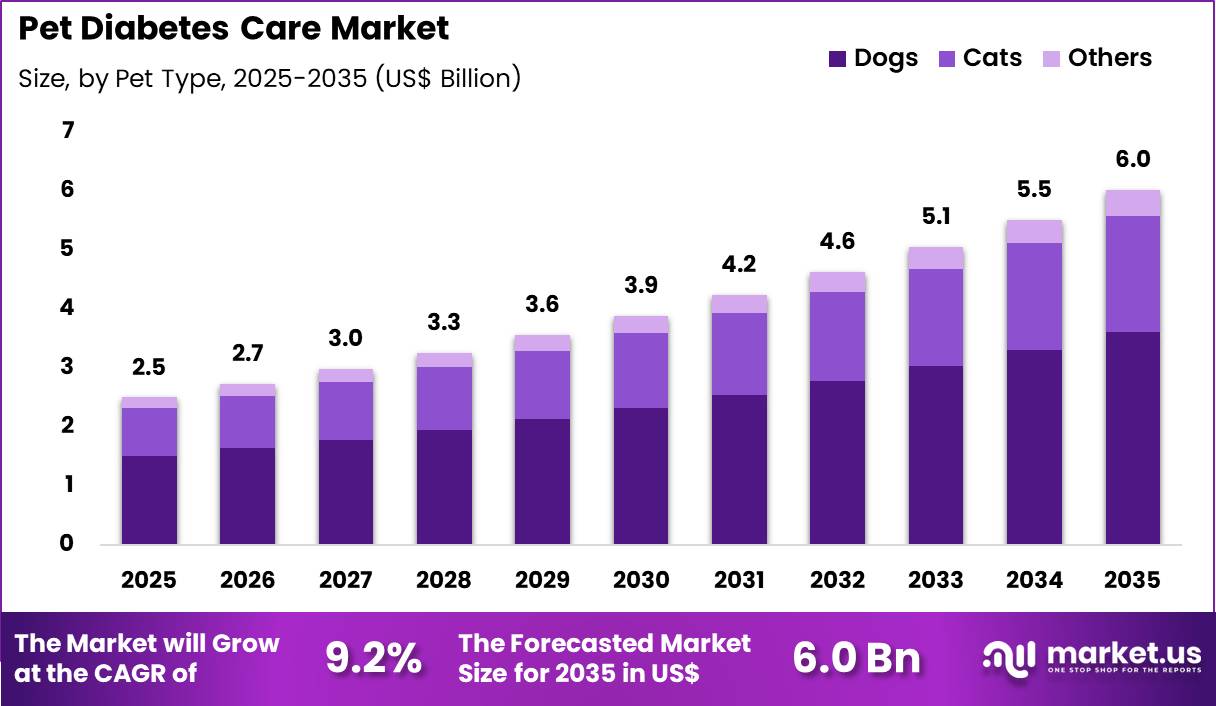

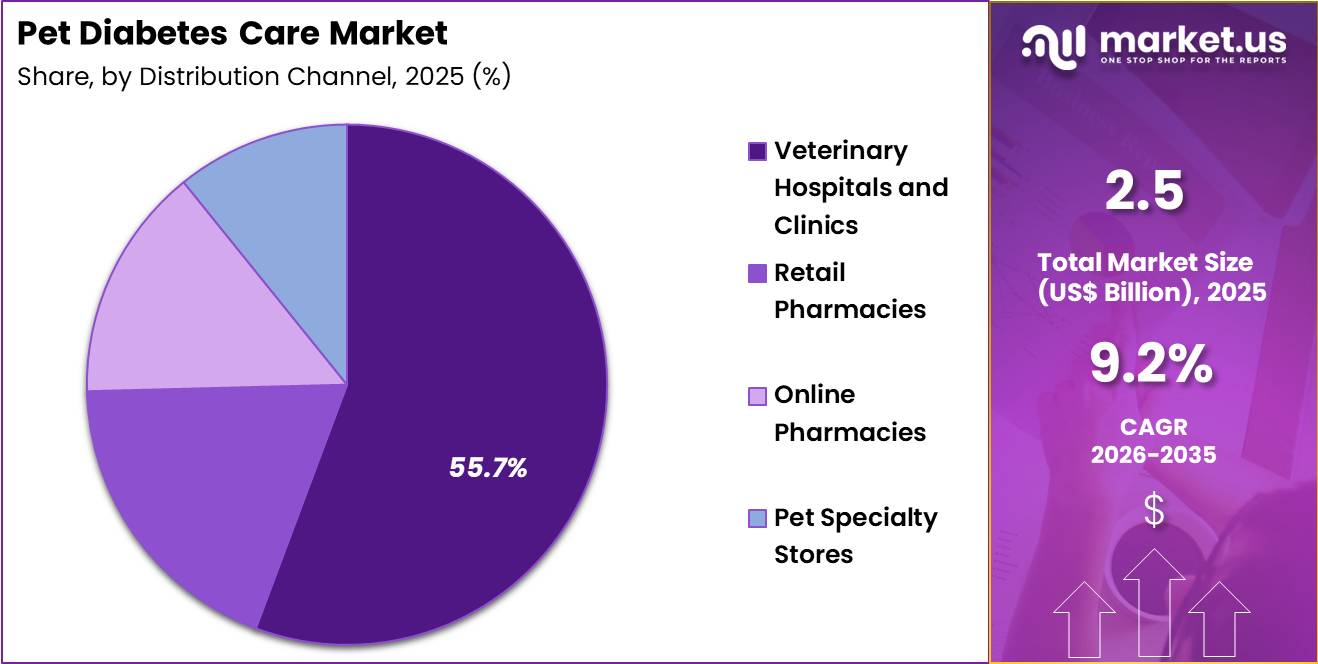

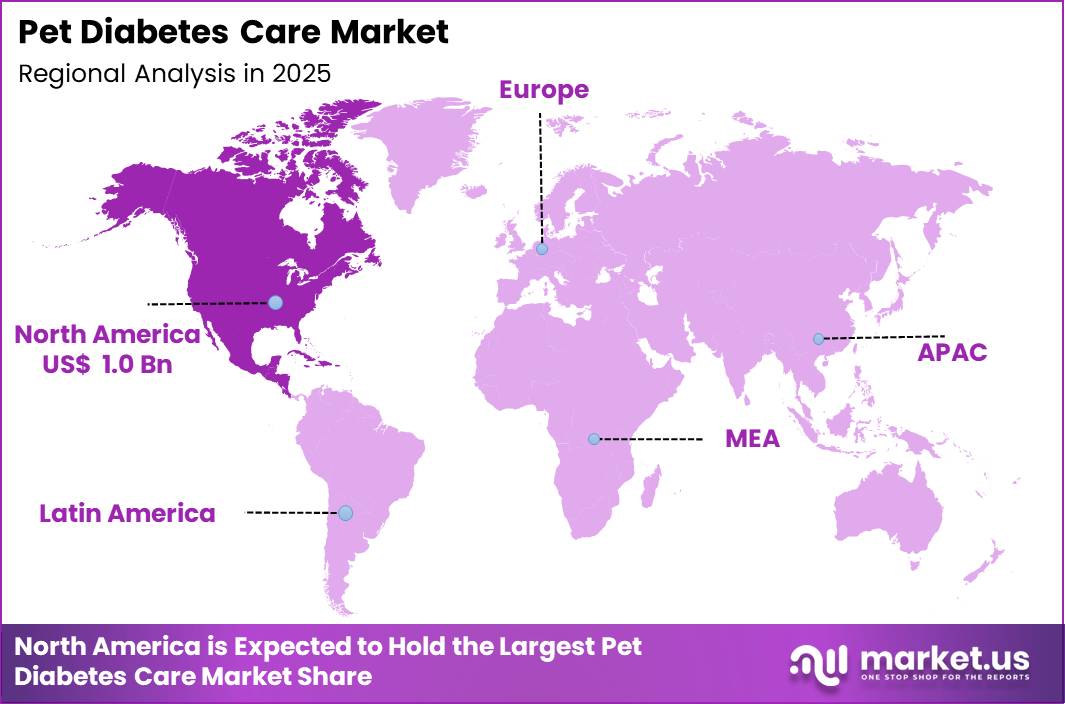

The Global Pet Diabetes Care Market size is expected to be worth around US$ 6.0 Billion by 2035 from US$ 2.5 Billion in 2025, growing at a CAGR of 9.2% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 39.4% share with a revenue of US$ 1.0 Billion.

Increasing prevalence of diabetes mellitus in companion animals, particularly dogs and cats, drives the Pet Diabetes Care market as pet owners and veterinarians prioritize effective monitoring and treatment to manage this chronic condition and prevent life-threatening complications.

Veterinarians increasingly prescribe insulin therapies such as protamine zinc insulin or glargine for diabetic dogs and cats, administering daily injections to stabilize blood glucose levels and alleviate clinical signs like polyuria, polydipsia, and weight loss.

These treatments support home glucose monitoring through portable glucometers and continuous glucose monitors that provide real-time interstitial glucose readings, enabling pet owners to adjust insulin doses based on daily trends and avoid hypoglycemia episodes.

Pet owners utilize these devices during routine home testing to track fasting and postprandial glucose curves, facilitating close collaboration with veterinarians for insulin dose titration and dietary management.

Nutritional interventions play a key role, with prescription diets formulated for low glycemic index and high fiber content helping stabilize blood glucose fluctuations in diabetic pets. Supportive care includes weight management programs and exercise regimens tailored to improve insulin sensitivity in overweight diabetic dogs.

Manufacturers pursue opportunities to develop integrated digital platforms that connect glucose monitors with mobile apps, expanding applications in long-term disease management where pet owners receive automated alerts for abnormal readings and share data directly with veterinarians for remote adjustments.

These advancements support predictive analytics that forecast glucose trends and recommend insulin dose modifications, reducing the risk of diabetic ketoacidosis and improving glycemic control in cats with concurrent conditions like pancreatitis or hyperthyroidism.

Opportunities emerge in non-invasive or minimally invasive monitoring technologies that minimize stress for pets during frequent testing. Companies invest in user-friendly, pet-specific glucometers with features like voice guidance and large displays to enhance owner compliance.

In February 2026, Zoetis reported continued expansion in its animal health diagnostics segment, with strong focus on point-of-care glucose monitoring solutions. The company is advancing integration of its diagnostic platforms with connected digital tools, enabling real-time data sharing between veterinarians and pet owners to support more effective disease management.

Recent trends emphasize connected devices, personalized insulin protocols, and remote veterinary oversight, positioning the market for growth in comprehensive, owner-empowered pet diabetes care focused on improved quality of life and reduced complications.

Key Takeaways

- In 2025, the market generated a revenue of US$ 2.5 Billion, with a CAGR of 9.2%, and is expected to reach US$ 6.0 Billion by the year 2035.

- The pet type segment is divided into dogs, cats and others, with dogs taking the lead with a market share of 59.9%.

- Considering product type, the market is divided into insulin, glucose monitoring devices, syringes and pen needles, diabetic food, dietary supplements and others. Among these, insulin held a significant share of 43.5%.

- Furthermore, concerning the distribution channel segment, the market is segregated into veterinary hospitals and clinics, retail pharmacies, online pharmacies and pet specialty stores. The veterinary hospitals and clinics sector stands out as the dominant player, holding the largest revenue share of 55.7% in the market.

- North America led the market by securing a market share of 39.4%.

Pet Type Analysis

Dogs accounted for 59.9% of growth within pet type and dominate the pet diabetes care market due to higher diagnosis rates, stronger clinical monitoring, and closer veterinary supervision compared to other companion animals.

Veterinary studies highlight that diabetes mellitus occurs more frequently in middle-aged and older dogs, particularly in certain breeds, which expands the treated population. Pet owners tend to observe behavioral and physical changes such as increased thirst, weight loss, and lethargy more easily in dogs, which supports earlier diagnosis and intervention.

Dogs are expected to remain the leading segment as routine veterinary checkups and preventive care become more common in companion animal healthcare. Owners also show higher willingness to invest in long-term treatment for dogs, including insulin therapy, dietary management, and regular glucose monitoring.

The segment benefits from structured treatment protocols that guide insulin dosing and lifestyle adjustments. Increasing pet humanization is projected to further strengthen spending on chronic disease management in dogs.

Veterinary professionals emphasize consistent monitoring in canine diabetes, which increases repeat purchases of related products. Rising obesity rates in pets are likely to contribute to growing diabetes incidence, particularly in urban environments.

As dog ownership continues to rise globally and awareness of chronic pet diseases improves, this segment is anticipated to maintain its dominant share in the pet diabetes care market.

Product Type Analysis

Insulin accounted for 43.5% of growth within product type and dominates the pet diabetes care market because it remains the primary and most essential treatment for managing diabetes in companion animals. Veterinarians prescribe insulin therapy as the standard of care for both canine and feline diabetes to regulate blood glucose levels and prevent complications.

Clinical guidance indicates that most diabetic dogs require lifelong insulin therapy, which drives continuous demand for this product category. Insulin is expected to retain its leading position as it directly addresses the core metabolic dysfunction associated with diabetes.

Pet owners rely on insulin to stabilize their pets’ health, improve quality of life, and reduce the risk of severe complications such as ketoacidosis. The segment benefits from advancements in insulin formulations and delivery systems that improve dosing accuracy and ease of administration.

Growing awareness of pet diabetes management is projected to support higher treatment adherence and regular insulin use. Veterinarians also provide detailed guidance on dosing schedules and monitoring, which reinforces consistent product demand.

Increasing diagnosis rates and improved access to veterinary care are likely to expand the number of pets receiving insulin therapy. As diabetes management requires ongoing and controlled treatment, insulin is estimated to remain the most critical and dominant product segment in this market.

Distribution Channel Analysis

Veterinary hospitals and clinics accounted for 55.7% of growth within distribution channel and dominate the pet diabetes care market due to their central role in diagnosis, treatment initiation, and long-term disease management.

Pet diabetes requires precise monitoring, individualized dosing, and continuous follow-up, which makes veterinary supervision essential throughout the treatment journey. Veterinarians conduct blood glucose testing, adjust in

sulin regimens, and recommend dietary changes, which strengthens the reliance on clinical settings for product distribution. Veterinary hospitals and clinics are expected to remain the primary channel as most diabetes treatments require professional prescription and monitoring.

The segment benefits from increasing pet healthcare spending and rising awareness of chronic disease management in animals. Clinics also offer education to pet owners on insulin administration, diet control, and symptom monitoring, which improves treatment adherence.

The growing number of veterinary facilities in urban and semi-urban areas is projected to enhance accessibility to diabetes care. Pet owners often trust veterinarians for product authenticity and proper usage guidance, which influences purchasing behavior.

Repeat visits for monitoring and follow-up care are likely to drive consistent product demand through this channel. As structured veterinary care continues to expand globally, veterinary hospitals and clinics are anticipated to maintain their dominant position in the pet diabetes care market.

Key Market Segments

By Pet Type

- Dogs

- Cats

- Others

By Product Type

- Insulin

- Glucose Monitoring Devices

- Syringes and Pen Needles

- Diabetic Food

- Dietary Supplements

- Others

By Distribution Channel

- Veterinary Hospitals and Clinics

- Retail Pharmacies

- Online Pharmacies

- Pet Specialty Stores

Drivers

Rising companion animal diabetes prevalence and diagnostic testing is driving the market.

Veterinary practices report sustained increases in confirmed canine and feline diabetes mellitus cases requiring ongoing management. The condition necessitates regular blood glucose monitoring and insulin administration protocols.

Pet owners demonstrate greater willingness to pursue long-term therapy following diagnosis through improved screening practices. The driver aligns with expanded use of point-of-care analyzers and continuous glucose monitors in veterinary clinics.

Facilities achieve more accurate titration of insulin doses through frequent home and in-clinic measurements. The trend supports higher compliance with veterinary recommendations for dietary management and exercise regimens. Enhanced owner education programs contribute to earlier detection and intervention.

The expansion reflects broader recognition of diabetes as a manageable chronic disease in companion animals. Sustained case identification maintains demand for monitoring devices and insulin products. This factor reinforces consistent market growth through essential diagnostic and therapeutic requirements.

Restraints

Increasing cost of insulin products and monitoring supplies is restraining the market.

Veterinary insulin formulations and compatible syringes remain subject to periodic price adjustments driven by raw material and manufacturing expenses. Pet owners frequently encounter higher out-of-pocket costs for ongoing therapy compared to human analogs.

The restraint limits adherence in households with constrained budgets for chronic care. Practices observe reduced refill rates when monthly expenses exceed owner financial capacity. The factor contributes to selective use of less expensive alternatives with potentially variable efficacy.

Providers must navigate insurance coverage gaps for veterinary-specific products. The dynamic moderates demand for premium continuous glucose monitoring systems. This constraint tempers broader adoption of advanced management tools in certain demographic segments.

The limitation persists in influencing treatment decisions and long-term compliance patterns. Economic pressures continue to shape accessibility within the pet diabetes care segment.

Opportunities

Development of longer-acting veterinary insulin formulations is creating growth opportunities.

Pharmaceutical developers are advancing insulin analogs with extended duration of action specifically formulated for canine and feline physiology. These preparations aim to reduce injection frequency while maintaining glycemic control. Opportunities emerge for improved owner compliance through simplified administration schedules.

The framework supports reduced risk of hypoglycemic episodes in patients with variable routines. Manufacturers can pursue regulatory pathways for differentiated product claims. The development facilitates integration with existing monitoring technologies for optimized dose adjustments.

Such advancements attract partnerships with veterinary endocrinology specialists for clinical validation. The opportunity fosters differentiation through superior convenience and safety profiles. Stakeholders anticipate enhanced therapeutic outcomes in refractory cases. This progression positions participants for expansion in chronic diabetes management solutions.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic pressure is reshaping the pet diabetes care market because inflation lifts veterinary bills, consumable prices, and day-to-day treatment costs, which can push some owners to delay nonessential upgrades or reduce monitoring frequency.

Treatment demand still holds up better than many other pet care categories because diabetes management often requires ongoing insulin use and regular blood-glucose monitoring at home.

Geopolitical tension adds further strain by unsettling cross-border sourcing for pharmaceutical ingredients, plastics, and electronic parts tied to diabetes care products, and that can create procurement gaps for clinics and distributors.

Those pressures hurt margins and can make syringes, strips, and monitoring tools less affordable for end users. The current US reciprocal tariff order issued in April 2025 excludes pharmaceuticals, so insulin therapies do not face the same direct tariff burden under that framework.

However, the US continues to impose Section 301 duties on key Chinese inputs, including a 100% tariff on syringes and needles and a 50% tariff on semiconductors, which can raise the landed cost of injection supplies and some glucose-monitoring hardware.

Even so, these trade actions are also pushing companies to diversify suppliers, localize more production, and build more resilient inventory strategies. In practical terms, the market faces near-term cost pressure, but essential care demand and stronger regional supply planning should keep the long-term outlook favorable.

Latest Trends

Increased availability of veterinary-specific continuous glucose monitors is driving the market.

Multiple manufacturers expanded distribution of continuous glucose monitoring systems designed for companion animals during 2024-2025. These devices provide real-time interstitial glucose readings with extended sensor life suitable for canine and feline patients.

The 2024-2025 availability addresses previous limitations in sensor durability and species-specific calibration. Veterinarians benefit from detailed glycemic profiles that guide precise insulin adjustments. The development aligns with growing demand for home-based monitoring to minimize clinic visits.

Facilities integrate data downloads into electronic medical records for longitudinal trend analysis. The trend supports remote consultation capabilities through cloud-based platforms.

Early clinical experience demonstrates reliable performance in outpatient settings. The increased deployment accelerates adoption in specialist and general practice environments. Overall, this technological advancement elevates standards for glycemic control in pet diabetes care.

Regional Analysis

North America is leading the Pet Diabetes Care Market

North America accounted for 39.4% of the pet diabetes care market in 2025 as veterinary clinics and pet owners increased focus on long-term management of chronic metabolic disorders in companion animals. Rising obesity levels among pets and improved diagnostic practices have led to higher identification of diabetes cases in both dogs and cats.

According to the American Veterinary Medical Association, approximately 45% of dogs in the United States were classified as overweight or obese in recent years, significantly increasing the risk of diabetes and related metabolic conditions.

Veterinarians across the United States and Canada are therefore emphasizing routine screening, blood glucose monitoring, and early intervention strategies. Pet owners are increasingly adopting insulin therapies, continuous glucose monitoring devices, and specialized diabetic diets to manage the condition effectively.

Growth in veterinary specialty clinics and endocrinology services has improved access to advanced treatment options. Pharmaceutical companies are developing pet-specific insulin formulations and monitoring solutions that enhance treatment compliance.

Digital health tools and mobile applications are also helping pet owners track glucose levels and treatment schedules. These developments collectively supported steady expansion of diabetes management solutions across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience strong growth during the forecast period as pet ownership increases and awareness of chronic animal health conditions improves across the region. Countries such as China, India, Japan, and South Korea are witnessing rapid growth in companion animal populations, particularly in urban households.

The World Health Organization reported that global obesity rates have risen significantly in recent decades, a trend that is also influencing pet health due to lifestyle similarities between owners and animals.

Veterinary clinics across the region are expanding diagnostic capabilities to detect metabolic disorders earlier in companion animals. Pet owners are increasingly seeking professional veterinary care and adopting specialized diets and treatment plans for chronic conditions.

Governments and veterinary associations are strengthening animal healthcare infrastructure and promoting preventive care practices. Pharmaceutical companies are expanding access to insulin therapies and glucose monitoring products tailored for regional markets.

Veterinary training institutions are improving education in animal endocrinology and chronic disease management. These developments are expected to accelerate adoption of diabetes care solutions for companion animals across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Pet Diabetes Care Market expand growth by developing advanced insulin therapies, smart glucose monitoring devices, and digital health tools that support continuous disease management in companion animals.

Companies collaborate with veterinary clinics and diagnostic laboratories to improve early detection and long-term treatment adherence for diabetic pets. They also invest in user-friendly monitoring systems and mobile applications that allow pet owners to track glucose levels and adjust treatment routines effectively.

Merck Animal Health represents a prominent participant in the Pet Diabetes Care Market and operates as a global animal health division of Merck & Co. that develops veterinary pharmaceuticals, vaccines, and monitoring solutions for companion animals and livestock.

The company focuses on innovation in metabolic disorder management and veterinary care technologies. Industry competitors continue to introduce improved insulin formulations, expand veterinary partnerships, and enhance digital monitoring capabilities to strengthen treatment outcomes and support sustained market growth.

Top Key Players

- Merck & Co., Inc. (Merck Animal Health)

- Zoetis

- BD (Becton, Dickinson and Company)

- Boehringer Ingelheim International GmbH

- Nova Biomedical

- Allison Medical, Inc.

- AccuBioTech Co., Ltd

- i-SENS, Inc.

- TaiDoc Technology Corporation

Recent Developments

- In February 2025, Boehringer Ingelheim introduced Senvelgo, an oral liquid therapy for managing diabetes in cats. The product is designed for once-daily use and offers an alternative to injectable insulin in suitable cases, improving ease of administration for pet owners and supporting wider adoption in newly diagnosed feline patients.

- In September 2025, Merck Animal Health collaborated with Zoetis and Purina Pro Plan Veterinary Diets to establish the Diabetes PetCare Alliance. The initiative provides veterinary clinics with structured starter kits and guidance tools to support pet owners during the early stages of diabetes management, helping improve treatment adherence and outcomes.

Report Scope

Report Features Description Market Value (2025) US$ 2.5 Billion Forecast Revenue (2035) US$ 6.0 Billion CAGR (2026-2035) 9.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Pet Type (Dogs, Cats and Others), By Product Type (Insulin, Glucose Monitoring Devices, Syringes and Pen Needles, Diabetic Food, Dietary Supplements and Others), By Distribution Channel (Veterinary Hospitals and Clinics, Retail Pharmacies, Online Pharmacies and Pet Specialty Stores) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, 9.2%Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Merck & Co., Inc., Zoetis, BD, Boehringer Ingelheim International GmbH, Nova Biomedical, Allison Medical, Inc., AccuBioTech Co., Ltd, i-SENS, Inc., TaiDoc Technology Corporation. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Merck & Co., Inc. (Merck Animal Health)

- Zoetis

- BD (Becton, Dickinson and Company)

- Boehringer Ingelheim International GmbH

- Nova Biomedical

- Allison Medical, Inc.

- AccuBioTech Co., Ltd

- i-SENS, Inc.

- TaiDoc Technology Corporation

Our Clients

- 182490

- March 2026