Global Perishable Prepared Food Market Size, Share, And Business Benefits By Product Type (Salads, Sandwiches, Fresh-Cut Fruits and Vegetables, Meals and Snacks), By Distribution Channel (Supermarkets, Convenience Stores, Online Retail, Foodservice), By End User (Residential Customers, Restaurants, Hotels and Catering Businesses), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: November 2025

- Report ID: 165739

- Number of Pages: 318

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

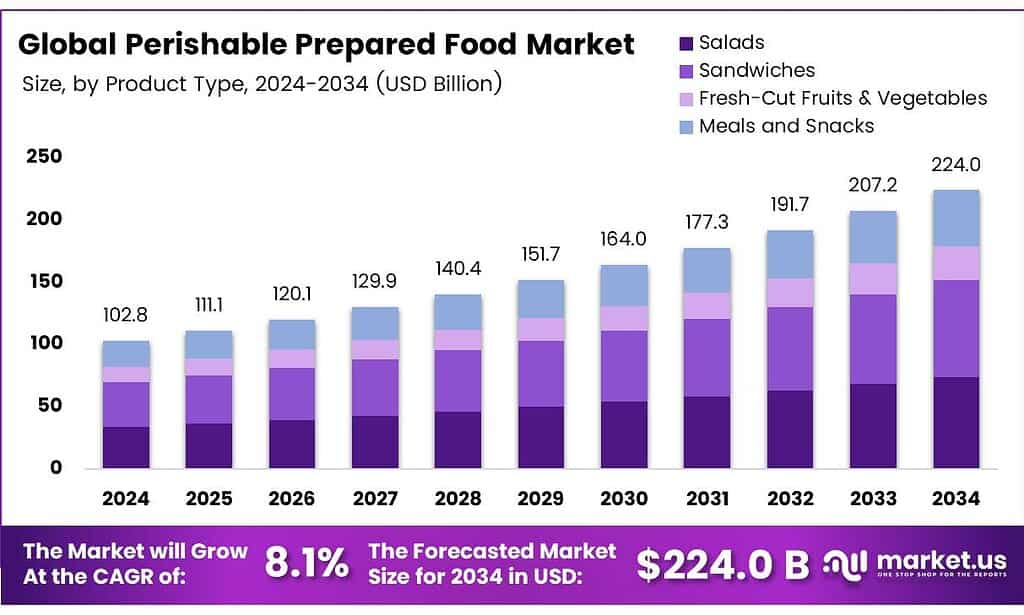

The Global Perishable Prepared Food Market size is expected to be worth around USD 224.0 Billion by 2034, from USD 102.8 Billion in 2024, growing at a CAGR of 8.1% during the forecast period from 2025 to 2034.

Perishable foods can spoil or grow harmful bacteria if not stored in a refrigerator or freezer. These items require prompt cooking or consumption to avoid going bad, making it essential to track expiration dates. Defined as products susceptible to spoilage, perishable foods need careful protection during preparation, storage, and distribution to maintain their shelf life. Most people incorporate both perishable and nonperishable items into their meal plans and grocery lists, balancing health, taste, and convenience in home kitchens.

Simply put, some foods can remain stable in a pantry for months, while others may last only a few days even under ideal refrigeration. The United States Department of Agriculture (USDA) states that perishable foods will spoil, decay, or become unsafe unless refrigerated at 40°F (4°C) or frozen at 0°F (-17°C) or below. Robert Powitz, PhD, MPH, RS, a sanitarian and advisor to the Indoor Health Council, recommends storing them at 40°F (4°C) or colder.

Most bacteria that cause foodborne illness grow well at temperatures between 41°F to 135°F (5° to 57°C), Powitz told Healthline, noting this range as the temperature danger zone. Perishable foods include meat, poultry, fish, eggs, dairy products, cooked leftovers, and any cut or chopped fruit or vegetable. Fresh fruits and vegetables are also perishable, with very few suitable for long-term room-temperature storage.

Even with the dangers of poor temperature management, only roughly one-tenth of the world’s perishable food is refrigerated. Developing nations are much less likely to adopt this practice compared to developed ones. Experts estimate that 25–30% of perishable food goes to waste, and most of this loss could be avoided with proper refrigeration after harvest. Frozen storage has transformed modern large-scale food production.

Key Takeaways

- The Global Perishable Prepared Food Market is expected to grow from USD 102.8 billion in 2024 to USD 224.0 billion by 2034 at 8.1% CAGR.

- Salads dominated By Product Type in 2024 with a 32.8% share due to freshness, low calories, convenience, and variety.

- Supermarkets led by Distribution Channel in 2024 with 39.1% share, driven by one-stop shopping, fresh displays, high footfall, promotions, and loyalty programs.

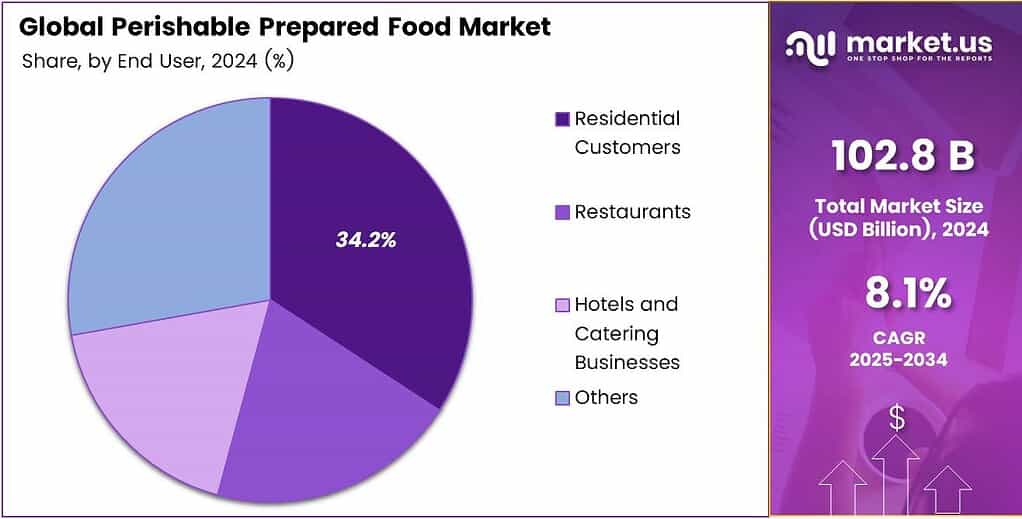

- Residential Customers held the top By End User position in 2024 with 34.2% share, favoring time-saving, affordable prepared foods and meal kits.

- Asia-Pacific commanded 48.9% market share in 2024 of USD 50.2 billion, fueled by urbanization, long work hours, and dual-income households in China, India, Japan, South Korea, and Southeast Asia.

By Product Type Analysis

Salads dominate with 32.8% due to rising health awareness and demand for quick, nutritious meals.

In 2024, Salads held a dominant market position in the By Product Type Analysis segment of the Perishable Prepared Food Market, with a 32.8% share. Consumers increasingly prefer salads for their freshness and low-calorie benefits. This segment thrives on convenience and variety, boosting sales in busy lifestyles.

Sandwiches follow as a popular choice, offering portable and customizable options. They cater to on-the-go consumers seeking quick bites. However, competition from salads limits expansion. Yet, premium ingredients like artisanal breads sustain steady demand across demographics.

Fresh-Cut Fruits and Vegetables gain traction through emphasis on natural snacking. Pre-packaged cuts save preparation time, appealing to health-focused buyers. Additionally, seasonal availability influences variety, supporting consistent market presence despite lower dominance.

By Distribution Channel Analysis

Supermarkets dominate with 39.1% due to a wide product range and easy accessibility for daily shoppers.

In 2024, Supermarkets held a dominant market position in the By Distribution Channel Analysis segment of the Perishable Prepared Food Market, with a 39.1% share. They provide one-stop shopping with fresh displays. This channel benefits from high footfall and promotions, encouraging impulse buys. Furthermore, loyalty programs strengthen customer retention.

Convenience Stores serve urgent needs with extended hours. They stock ready-to-eat items for immediate consumption. Although space constraints exist, strategic placements boost visibility. Thus, they maintain relevance in urban settings.

Online Retail expands rapidly via home delivery options. Platforms offer subscriptions and discounts, attracting tech-savvy users. However, logistics challenges persist. Still, contactless trends accelerate adoption, promising future growth.

By End User Analysis

Residential Customers dominate with 34.2% due to increasing home cooking avoidance and preference for ready meals.

In 2024, Residential Customers held a dominant market position in the By End User Analysis segment of the Perishable Prepared Food Market, with a 34.2% share. Families opt for time-saving prepared foods amid hectic schedules. This group values affordability and portion control. Additionally, meal kits integrate seamlessly into routines.

Restaurants utilize these products to streamline operations. They incorporate prepped items for efficiency without compromising quality. Though costs vary, bulk purchases ensure supply stability. Consequently, menu innovation flourishes. Hotels and Catering Businesses rely on perishable prepared foods for events. High-volume needs demand reliability and freshness. Partnerships with suppliers minimize waste. Therefore, scalability supports large-scale service delivery effectively.

Key Market Segments

By Product Type

- Salads

- Sandwiches

- Fresh-Cut Fruits and Vegetables

- Meals and Snacks

By Distribution Channel

- Supermarkets

- Convenience Stores

- Online Retail

- Foodservice

- Others

By End User

- Residential Customers

- Restaurants

- Hotels and Catering Businesses

- Others

Emerging Trends

Shift from Ultra-Processed to Fresher Chilled Convenience Meals

Consumers are quietly rethinking what convenience food should look like. Ultra-processed products dominated, but health worries are nudging people toward fresher, perishable prepared meals with shorter ingredient lists. A recent CDC data brief shows that ultra-processed foods still supply about 54–56% of daily calories for U.S. adults and youth, yet intake has started to edge down.

Health agencies are taking a harder line on processing levels. In 2025, the World Health Organization launched work on formal guidelines for ultra-processed food consumption, reflecting mounting evidence linking these products to chronic disease risk. When the WHO starts talking about how much is too much, food manufacturers and retailers listen very closely.

This policy pressure is encouraging retailers to expand chilled cabinets filled with fresh salads, grain bowls, sushi, and chef-style ready plates that must be consumed. These options still save time, but feel closer to home-cooked food than shelf-stable, heavily processed items. FAO/WHO’s GIFT platform is helping governments see how processed foods contribute to national diets and where fresher, prepared options can plug nutritional gaps.

Drivers

Time-Pressed Households Lean on Ready-to-Eat Fresh Meals

Behind the growth of perishable prepared foods, daily life is getting busier and more fragmented. Many households simply do not have the time or energy to cook from scratch every evening. USDA research on working-age Americans shows that people who work from home prepare food on 75% of weekdays, compared with 63% for those working away from home, and they spend more minutes doing it.

For those commuting, juggling multiple jobs, or managing childcare, cooking can fall to the bottom of the list. At the same time, more meals are eaten at home overall, as food-service prices rise and families watch their budgets. USDA’s FoodAPS survey underlines how much household food now comes from supermarkets and take-home channels rather than dine-in restaurants.

Perishable prepared foods answer a very simple question: What can I eat in the next 10 minutes that isn’t junk? Chilled soups, pasta dishes, marinated meats, and salad kits cut preparation to almost zero while feeling more real than something from the freezer or drive-through. When daily time spent cooking often sits well under an hour for many adults, these shortcuts make the difference between eating something balanced and skipping a meal altogether.

Restraints

High Food Waste and Spoilage Risks Limit Aggressive Expansion

The biggest brake on perishable prepared foods is the simple fact that they expire quickly. Short shelf lives mean retailers and manufacturers must constantly balance availability with the very real risk of throwing away unsold items. In the European Union, households alone generate 69 kg of food waste per person each year and account for 53% of total food waste across the chain. Fresh and prepared chilled products are a visible part of that loss.

- Studies of European households suggest total food waste can reach around 290 kg per person annually, with roughly 168 kg occurring at the consumer level. When a prepared salad or ready-to-eat plate is tossed because the use-by date passed yesterday, that loss hits both the retailer’s margin and the shopper’s wallet, not to mention the environmental impact.

For perishable prepared foods, the challenge is harder than for raw ingredients. Recipes are more complex, ingredients are pre-mixed, and safety margins must be conservative. Retailers often feel compelled to discount aggressively or remove stock well before the printed date. That makes planners cautious about expanding ranges too far, especially in smaller stores or regions with less predictable demand.

Opportunity

Using Fresh Prepared Meals to Cut Waste and Improve Food Security

The flip side of the waste problem is a major opportunity. Globally, an estimated 2.5 billion tons of food are lost or wasted every year, contributing about 8–10% of greenhouse-gas emissions. At the same time, around 783 million people are still affected by hunger. Those two facts sit uncomfortably together and are pushing governments and businesses to rethink how food is prepared and sold.

Perishable prepared foods can become part of the solution rather than the problem. Central kitchens and in-store preparation give operators better control over portion sizes and raw-material use. Trimmings from vegetables, meats, and bakery items can be turned into soups, sauces, and ready dishes instead of being discarded. With clear date-coding and smart packaging, these items can move quickly from about to be wasted to tonight’s dinner.

- In the United States alone, roughly 60 million tons of food—almost 40% of the national supply is thrown away each year, averaging 325 pounds per person. Redirecting even a small share of that into well-managed prepared meals would have visible climate and social benefits. Retail chains that design prepared-food programs around waste-reduction goals can tell a strong story to regulators, investors, and customers.

Regional Analysis

Asia Pacific Dominates the Perishable Prepared Food Market with a 48.9% Share, Valued at USD 50.2 Billion

Asia-Pacific stands as the clear powerhouse in the global perishable prepared food market, accounting for a dominant 48.9% share, valued at around USD 50.2 billion. Rapid urbanization, long working hours, and the growth of dual-income households across China, India, Japan, South Korea, and Southeast Asian countries are pushing consumers towards chilled ready meals.

Modern retail formats, from hypermarkets to convenience store chains, are expanding chilled sections and partnering with central kitchens to ensure consistent quality and food safety. At the same time, strong penetration of food-delivery platforms and quick-commerce players is blurring the line between restaurant food and retail prepared offerings, further lifting demand.

North America maintains a sizeable but more mature market, driven by a well-established convenience culture and increasing interest in fresher, cleaner-label refrigerated meals. Europe remains important, with strong emphasis on transparency, origin labeling, and waste reduction, which favors shorter-shelf-life but higher-quality prepared options.

Emerging markets in Latin America and the Middle East & Africa are at earlier stages, yet rising incomes, modern grocery formats, and tourism-led foodservice are opening space for chilled ready meals and grab-and-go solutions. Asia-Pacific’s scale, demographic momentum, and rapid evolution of cold-chain logistics and retail infrastructure position the region as the central growth engine for perishable prepared foods.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

AdvancePierre Foods specializes in convenient, ready-to-eat sandwiches, stuffed entrées, and snacks primarily for the foodservice and retail channels. Known for brands like Pierre and Barber Foods, its strength lies in large-scale production and extensive distribution networks, including a strong presence in the on-the-go sector. Its acquisition by Tyson Foods provided significant resources.

Aryzta AG is a global baking giant with a core focus on artisanal and specialty baked goods for foodservice and retail. The company’s key brands include La Brea Bakery and Otis Spunkmeyer. While historically a major force, Aryzta has undergone significant restructuring and divestments to streamline its operations and reduce debt. Its current strategy emphasizes a refocused portfolio on core markets in North America and Europe.

Bakkavör Group is a leading international producer of fresh prepared foods, with a particular emphasis on fresh produce, meals, and desserts. A key supplier to major UK retailers, the company champions a field-to-fork model, offering high levels of customization and innovation. Owned by the Icelandic investment fund Lýsir, Bakkavör excels in private-label manufacturing.

Top Key Players in the Market

- AdvancePierre Foods

- Aryzta AG

- Bakkavör Group

- Campbell Soup Company

- Cargill Inc.

- Conagra Brands Inc.

- Flowers Foods

- General Mills

- Greencore Group

- Grupo Bimbo

- Hormel Foods Corporation

- JBS USA Holdings Inc.

Recent Developments

- In 2025, AdvancePierre Foods specializes in ready-to-eat sandwiches, protein-packed entrees, and bakery items for foodservice, retail, and convenience channels. However, as part of Tyson Foods, it benefits from broader company initiatives in the perishable prepared foods sector, including expansions in plant-based and protein alternatives.

- In 2025, Bakkavor, the UK’s largest fresh prepared foods provider (meals, salads, desserts, dips, pizzas), will have growing U.S. and China operations. The strategy centers on scale, innovation, and trusted partnerships, with U.S. operations emphasizing premium, fresh-prepared items for retailers.

Report Scope

Report Features Description Market Value (2024) USD 102.8 Billion Forecast Revenue (2034) USD 224.0 Billion CAGR (2025-2034) 8.1% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Salads, Sandwiches, Fresh-Cut Fruits and Vegetables, Meals and Snacks), By Distribution Channel (Supermarkets, Convenience Stores, Online Retail, Foodservice, Others), By End User (Residential Customers, Restaurants, Hotels and Catering Businesses, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape AdvancePierre Foods, Aryzta AG, Bakkavör Group, Campbell Soup Company, Cargill Inc., Conagra Brands Inc., Flowers Foods, General Mills, Greencore Group, Grupo Bimbo, Hormel Foods Corporation, JBS USA Holdings Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Perishable Prepared Food MarketPublished date: November 2025add_shopping_cartBuy Now get_appDownload Sample

Perishable Prepared Food MarketPublished date: November 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- AdvancePierre Foods

- Aryzta AG

- Bakkavör Group

- Campbell Soup Company

- Cargill Inc.

- Conagra Brands Inc.

- Flowers Foods

- General Mills

- Greencore Group

- Grupo Bimbo

- Hormel Foods Corporation

- JBS USA Holdings Inc.

Our Clients

- 165739

- November 2025