Quick Navigation

Report Overview

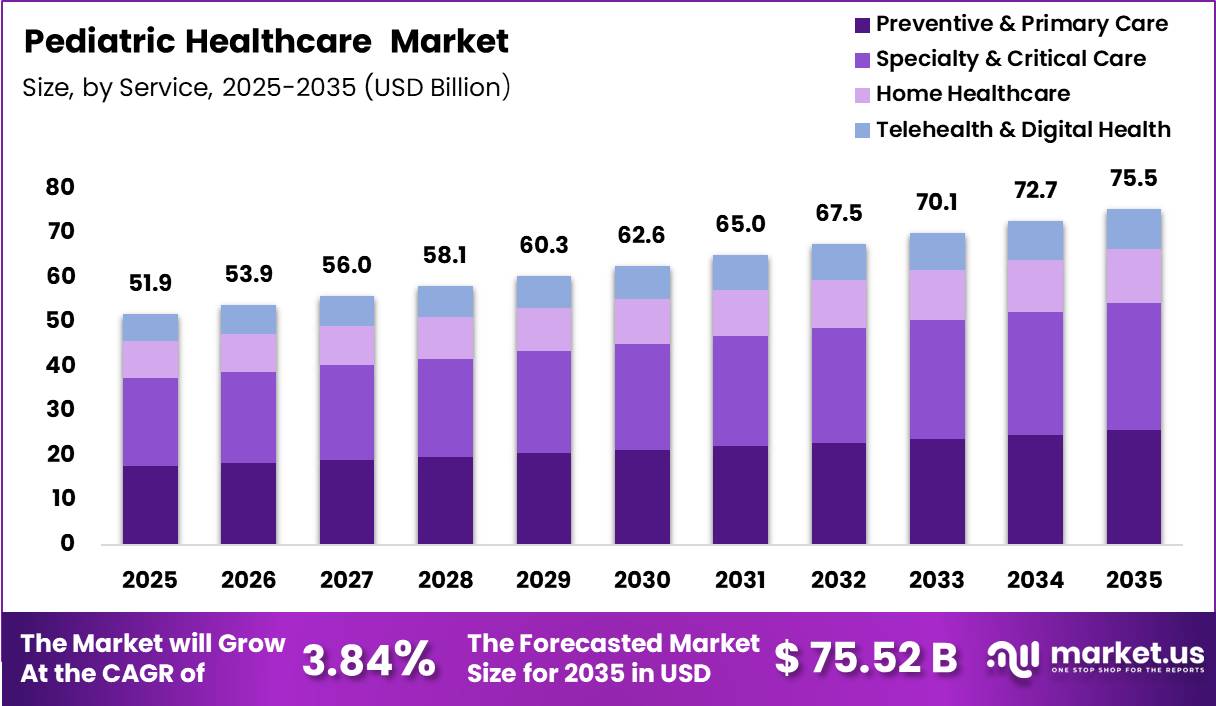

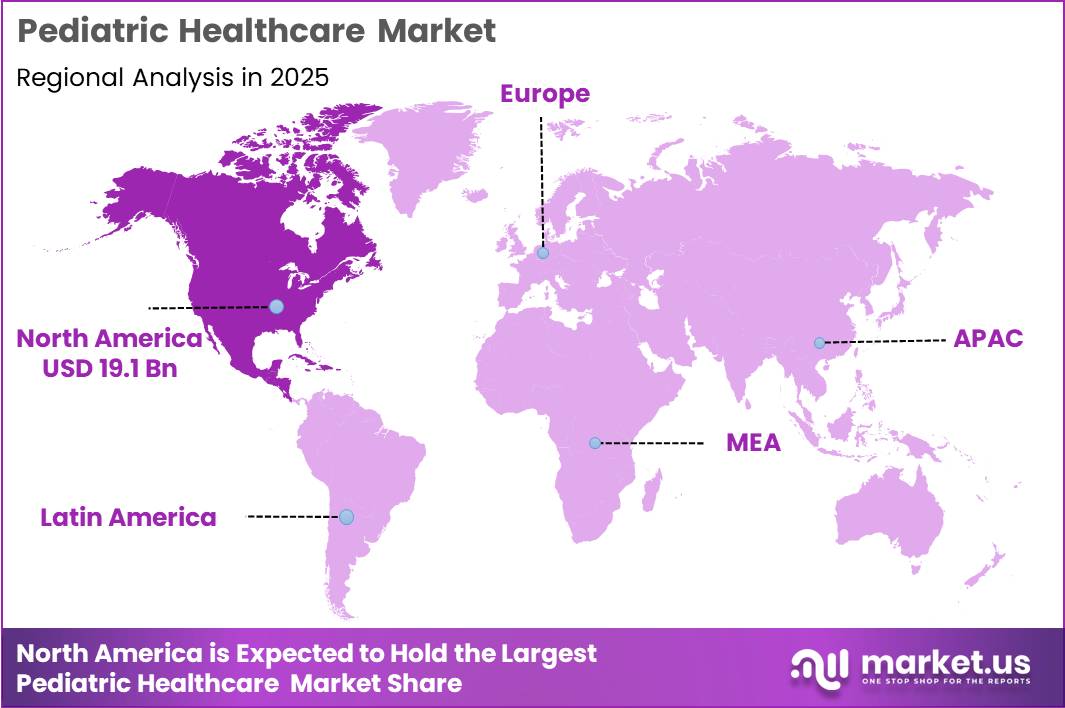

In 2025, the Global Pediatric Healthcare Market was valued at US$ 51.92 Billion, and between 2026 and 2035, this market is estimated to register a CAGR of 3.84%, reaching about US$ 75.52 Billion by 2035. North America held a dominant market position, capturing more than a 36.9% share, holding USD 19.1 Billion in revenue.

The Global Pediatric Healthcare Market plays an important role in the healthcare industry, dealing with the prevention, detection, treatment, and care of illnesses and health issues in babies, kids, and teenagers. Factors like higher birth rates in developing countries, greater awareness about children’s health, more widespread immunization efforts, and more funding for pediatric hospitals and specialized medical services are helping the market grow.

At the same time, there is a growing demand for preventive and basic healthcare services as governments and health providers place more emphasis on early disease detection and promoting the overall well-being of children.

- In July 2024, According to the World Health Organization (WHO), routine immunization programs were estimated to prevent approximately 3.5 to 5 million deaths annually from vaccine-preventable diseases such as measles, diphtheria, tetanus, influenza, and pertussis, highlighting the critical importance of pediatric vaccination programs worldwide.

North America and Europe remain major markets because to their strong healthcare systems, high healthcare spending, and extensive usage of specialist pediatric services. At the same time, the Asia-Pacific region is expanding rapidly. This is due to the large number of children in the area, increased access to healthcare, increased income, and efforts by governments to reduce infant and young child mortality.

Increased investments in pediatric hospitals, neonatal intensive care units (NICUs), and advanced digital healthcare technologies are further supporting market expansion, particularly across developing economies where healthcare infrastructure is undergoing significant modernization.

- In November 2024, According to UNICEF’s State of the World’s Children Report, released in November 2024, approximately 2.3 billion children live worldwide, representing nearly 30% of the global population and creating sustained demand for pediatric healthcare services, vaccines, medicines, and nutritional products.

New technology is transforming the way children’s healthcare is delivered by utilizing remote medical services, digital health tracking tools, smart systems that assist doctors in diagnosing ailments, and treatments tailored to each child’s specific needs.

As more children suffer from long-term health concerns such as asthma, obesity, diabetes, and birth abnormalities, the demand for continuing care and management grows. At the same time, there is a growing interest in special nutrition items and targeted treatments, which opens up new opportunities for doctors and medical product manufacturers worldwide.

- In April 2025, According to the International Diabetes Federation (IDF) Diabetes Atlas, more than 1.8 million children and adolescents under the age of 20 were living with Type 1 diabetes globally, underscoring the increasing need for specialized pediatric treatment, monitoring, and chronic disease management services.

Key Takeaways

- The global pediatric healthcare market was valued at US$ 51.92 Billion in 2025.

- The global pediatric healthcare market is projected to grow at a CAGR of 3.8% and is estimated to reach US$ 75.52 Billion by 2035.

- By service, Specialty & Critical Care dominated the market, accounting for 38.0% of the total market share in 2025.

- Based on product type, Vaccines led the market, comprising 38.5% of the total market share.

- By type, Chronic Illnesses represented the largest segment, holding 57.0% of the global pediatric healthcare market.

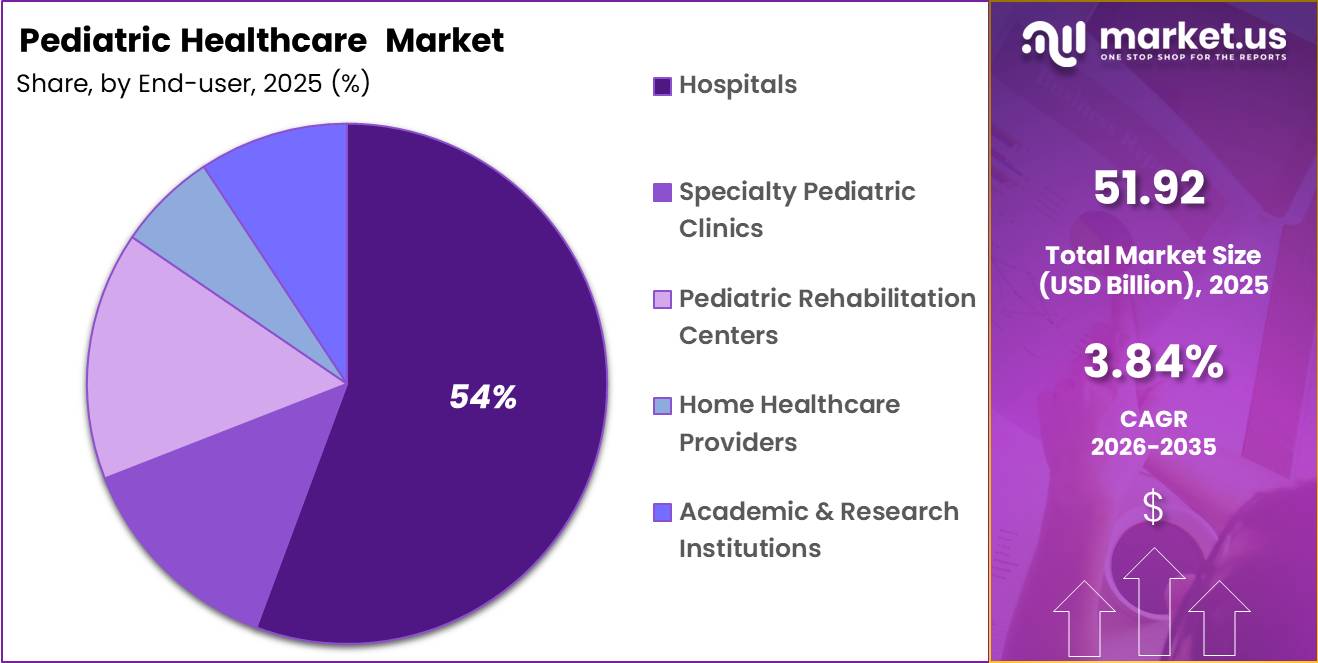

- Among end users, Hospitals dominated the market, accounting for 54.0% of the total market share.

- Among regions, North America emerged as the leading regional market, contributing 36.9% of the global pediatric healthcare market revenue in 2025.

Service Analysis

Specialty and Critical Care represents dominant Segment in the Market.

Specialty and Critical Care made up the biggest part of the global pediatric healthcare market in 2025, taking up 38.0% of all revenue. This field is expanding as more children are born with complex health conditions such as birth abnormalities, respiratory difficulties, mental illnesses, cancer, and problems that arise shortly after birth.

These illnesses necessitate the use of highly trained doctors and cutting-edge medical technology. Increased investment in locations like pediatric critical care units, neonatal intensive care units, and children’s hospitals, allowing this segment of the market to expand. New methods for diagnosing diseases, performing surgeries, and using critical care instruments are improving treatments while increasing the demand for these specialized services.

Preventive and primary care is a major part of the pediatric healthcare market, as more attention is being given to keeping children healthy through routine check-ups, vaccinations, developmental evaluations, and early diagnosis of illnesses. Across the world, governments, healthcare groups, and public health institutions are putting more money into programs that promote child wellness and vaccination efforts to lower the number of preventable diseases and better long-term health results.

At the same time, home healthcare is becoming more popular because families are opting for personalized and convenient care for kids who need ongoing treatment, rehabilitation, or recovery support outside of standard medical facilities. Alongside this, telehealth and digital health are growing quickly, thanks to improvements in virtual doctor visits, remote patient tracking, mobile health apps, and digital care systems that help make pediatric care more accessible and improve how healthcare is provided.

Product Type (Health Product) Analysis

Vaccines a significant product type.

Vaccines account for the largest share of the global pediatric healthcare market, accounting for 38.5% in 2025. This is mostly due to the importance of vaccines in preventing infectious diseases and improving the health of children all around the world. Government-led immunization campaigns, backing from international health organizations, and increased parental understanding of vaccine advantages all contribute to increased demand.

Standard children vaccination schedules, which protect against diseases such as measles, polio, hepatitis, diphtheria, and flu, have contributed significantly to market growth. Vaccines have become increasingly significant in pediatric healthcare systems around the world as the focus has shifted to disease prevention rather than treatment.

Therapeutics and drugs, such as antibiotics, antivirals, analgesics, and other pediatric medicines, are a significant market segment due to the continued need to treat infectious infections, respiratory problems, allergies, and chronic health concerns in children. Nutritional supplements, such as infant formula and pediatric nutrition products, are steadily increasing as public knowledge of child nutrition, immunity, and healthy development rises.

Increased concerns about hunger and vitamin deficits are driving rising demand. Meanwhile, Other Pediatric Health items, such as diagnostic instruments, medical devices, hygiene items, and child-care accessories, help to drive market growth by continuous product innovation and an increasing emphasis on comprehensive pediatric healthcare solutions.

Type Analysis

Chronic illnesses are the dominant type of the market.

Chronic illnesses were responsible for 57.0% of the worldwide pediatric healthcare market in 2025, making it the largest segment by type. This segment’s domination is due to the increased occurrence of long-term health issues in children, such as asthma, diabetes, obesity, congenital illnesses, neurological conditions, and genetic diseases.

These disorders frequently necessitate continuous medical supervision, regular monitoring, long-term medication, specialized therapies, and ongoing rehabilitation services, resulting in a steady demand for pediatric healthcare services.

Growing awareness of early diagnosis and disease management, combined with advances in pediatric treatment options and healthcare technologies, is driving segment growth. Furthermore, rising survival rates for children with complicated medical disorders, as well as greater access to specialist pediatric care, are helping to drive global growth in this market.

Acute Illnesses continue to represent an important part of the pediatric healthcare market, driven by the frequent occurrence of infectious diseases, respiratory infections, gastrointestinal disorders, seasonal illnesses, and injuries among children.

Demand for acute care services remains strong due to the need for prompt diagnosis, treatment, and emergency medical intervention. Improvements in healthcare accessibility, expanding pediatric emergency care facilities, and growing adoption of telehealth services are enhancing the management of acute conditions. Furthermore, increasing awareness among parents regarding timely medical consultation and treatment is supporting the continued demand for acute pediatric healthcare services worldwide.

End-User Analysis

Pediatric healthcare Held a Major Share of the Pediatric Healthcare Market.

Hospitals accounted for 54.0% of the worldwide pediatric healthcare market in 2025, making them the dominant end-user segment. Their supremacy stems from the provision of comprehensive pediatric services such as emergency care, neonatal and pediatric critical care units, specialized treatments, advanced diagnostic facilities, and surgical procedures.

Hospitals are the primary source of care for children with complex medical diseases, chronic illnesses, congenital disorders, and acute health emergencies. Continuous investments in pediatric infrastructure, expansion of children’s hospitals, and the use of new medical technologies are all helping to increase hospitals’ position in pediatric care delivery. Furthermore, the presence of multidisciplinary healthcare teams and pediatric specialists promotes effective illness management and better patient outcomes.

Specialty Pediatric Clinics provide concentrated care for specific medical disorders, including specialized consultations, diagnostics, and treatment services. Pediatric rehabilitation centers provide physical, occupational, and speech therapy to children suffering from injuries, surgeries, neurological problems, and developmental abnormalities.

Home healthcare providers are gaining popularity as families seek more tailored and convenient care for children who require long-term treatment and monitoring. Academic and research institutions help to drive market growth through pediatric research, clinical trials, medical education, and the development of novel medicines.

Meanwhile, governments and public health agencies continue to play an important role in developing pediatric healthcare systems through immunization programs, illness preventive measures, public health campaigns, and policies targeted at improving child health outcomes and healthcare access.

Key Market Segments

By Service

- Preventive & Primary Care

- Specialty & Critical Care

- Home Healthcare

- Telehealth & Digital Health

By Product Type (Health Products)

- Vaccines

- Therapeutics / Drugs (antibiotics, antivirals, analgesics, etc.)

- Nutritional Supplements (infant formula, pediatric nutrition)

- Other Pediatric Health Products

By Type

- Chronic Illnesses

- Acute Illnesses

By End User

- Hospitals

- Specialty Pediatric Clinics

- Pediatric Rehabilitation Centers

- Home Healthcare Providers

- Academic & Research Institutions

- Government & Public Health Agencies

Driver

Immunization scale-up and catch-up pediatrics

Immunization remains one of the strongest volume drivers for pediatric healthcare because it creates repeat touchpoints across infancy and school-age cohorts while lowering downstream acute-care costs, making payers and ministries more willing to fund delivery infrastructure.

Commercially, this does more than raise vaccine sales: it pulls demand for cold-chain logistics, pediatric visits, diagnostic triage, pharmacy dispensing, and digital reminder software, especially in under-immunized districts where catch-up campaigns convert missed cohorts into concentrated treatment demand.The strategic effect on the pediatric healthcare market is that vaccination is increasingly being valued as a system-efficiency lever rather than a narrow public-health line item.

WHO reported in 2024 that better use of vaccines against 23 pathogens could reduce antibiotic use by 22%, or 2.5 billion defined daily doses globally each year, including 33 million doses potentially saved through stronger pneumococcal coverage and 45 million through faster typhoid rollout in high-burden settings.

That changes provider economics in two ways: first, it improves the ROI case for public procurement and pediatric primary-care integration; second, it shifts demand from late-stage infectious treatment toward scheduled preventive care, which favors subscription-like care plans, pharmacy-based administration, and digitally managed outreach in South Asia, Africa, and underserved OECD geographies.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Immunization scale-up and catch-up pediatrics | +1.6% | South Asia, Sub-Saharan Africa, North America core, EU | Short term (≤ 2 years) |

| Primary-care financing and UHC expansion for children | +1.9% | LMICs broad base, APAC, Africa, Latin America, selective Middle East | Medium term (2-4 years) |

| Pediatric mental-health service formalization | +1.3% | North America core, EU, OECD APAC, urban middle-income markets | Medium term (2-4 years) |

| Childhood cancer access platforms and specialty care build-out | +0.9% | Latin America pilots, Central Asia, South Asia, MENA, Africa spill-over | Medium term (2-4 years) |

| Climate-linked child morbidity and resilience spending | +1.1% | South Asia, Africa, Southeast Asia, Southern Europe, climate-exposed US states | Long term (≥ 4 years) |

| Nutrition, obesity, and chronic-childhood condition management | +1.4% | EU, North America, Gulf, China, Latin America urban clusters | Medium term (2-4 years) |

Challenge

Structural pediatric workforce shortages and capacity strain

Persistent pediatric workforce shortfalls are creating a structural drag on pediatric healthcare expansion, with multiple surveys indicating that over one-third of children’s hospitals report severe shortages in at least six non-physician roles and critical gaps in neurology, behavioral health, and other subspecialties, which directly limits throughput capacity even where infrastructure exists.

In practice, these gaps manifest as 10–25% vacancy rates for pediatric nurses and allied professionals in many tertiary centers, average wait times of 30–90 days for pediatric neurology or developmental appointments, and unfilled rural pediatrician posts that leave catchment areas of 50,000–200,000 children without consistent specialist coverage, which collectively trims potential encounter volumes by an estimated 8–12%.

Workforce pipeline data show that although recent residency matches are filling over 95% of pediatric positions in some regions, subspecialty training remains undersupplied relative to need, especially in complex care and mental health, resulting in a widening mismatch between rising chronic and behavioral caseloads and available expertise.

To navigate this friction, systems are being forced into long-term strategic adjustments such as reallocating 10–15% of capital budgets toward workforce retention and training programs, scaling tele-pediatrics to cover 15–30% of follow-up visits, creating cross-trained multidisciplinary teams that can manage broader scopes of practice, and reconfiguring service lines to concentrate highly specialized care into regional hubs while deploying nurse practitioners and physician associates to extend pediatric coverage in underserved zones, a rebalancing that will likely take at least one to two training cycles (6–10 years) to fully normalize.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Chronic pediatric workforce gaps | -1.4% | North America, Europe, urban EM hubs | Long term (≥ 4 years) |

| Fragmented pediatric care infrastructure | -1.2% | Sub-Saharan Africa, South Asia, LatAm | Long term (≥ 4 years) |

| Rising complexity of pediatric disease mix | -1.0% | Global, high-burden LMICs | Medium term (2-4 years) |

| Reimbursement and payer misalignment | -0.9% | North America, EU regulatory hubs | Medium term (2-4 years) |

| Pediatric digital and data lag | -0.8% | Global, APAC and EM digital corridors | Medium term (2-4 years) |

| Supply and access volatility for essential pediatric therapies | -0.7% | Sub-Saharan Africa, South Asia, small markets | Short term (≤ 2 years) |

Restraints

Systemic drug shortages eroding pediatric care growth

Systemic pediatric drug shortages have emerged as a first-order drag on pediatric healthcare growth by directly constraining procedure volumes, elongating length of stay, and forcing sub-optimal therapeutic substitutions: in the US alone, children’s hospitals reported 84 pediatric drug shortages in 2023, with nearly 50% of essential pediatric medications affected and an estimated financial hit of around 900 million dollars, indicating a structural mismatch between pediatric formulation demand and manufacturing economics for low-margin generics.

Root causes span concentrated active pharmaceutical ingredient (API) sourcing in China and India, lean just-in-time inventories, and under-investment in pediatric-specific dosage forms, so when seasonal respiratory infections or post-pandemic catch-up waves push demand 20–40% above baseline, supply chains exhibit 8–12 week lead-time slippages, forcing hospitals to reschedule 20–30% of elective pediatric procedures and absorb overtime labor and compounding costs that can add 3–5 percentage points to pharmacy operating expense ratios.

Strategically, this translates into both revenue and margin compression: if 3–5% of pediatric encounters are deferred or downgraded in acuity because the optimal medicine is unavailable, top-line volumes grow more slowly than epidemiological need would suggest, while substitution to higher-priced or adult formulations adds 5–10% to per-case drug spend without a commensurate reimbursement uplift, prompting hospital systems to cap or phase pediatric CapEx (wards, neonatal ICU refurbishments, and infusion suites) by 10–15% versus pre-shortage plans over the next 2–3 years.

The modeled -2.0 percentage point hit to pediatric healthcare CAGR over the short to medium term reflects a base case in which intermittent shortages persist through 2027–2028, with only partial mitigation from dual-sourcing APIs, strategic stockpiles, and targeted incentives for essential pediatric generics.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Systemic pediatric drug shortages | -2.0% | North America, Europe core | Short–Medium term |

| Pediatric workforce & capacity gaps | -2.2% | North America, EU, selected APAC | Medium–Long term |

| Public payer budget compression | -1.6% | EU, UK, Latin America, parts of APAC | Medium term |

| Regulatory & compliance drag | -0.9% | US, EU, China | Medium–Long term |

| Fragmented pediatric reimbursement models | -1.1% | US, emerging APAC, Latin America | Short–Medium term |

| Supply chain & input cost inflation | -0.8% | Global, higher in import-dependent markets | Short term |

Opportunity

Embedding school-linked adolescent mental health care platforms

This is an opportunity rather than a current driver because mental health need is already present, but monetization remains structurally underdeveloped: most pediatric systems still treat adolescent behavioral health as a low-capacity referral service instead of embedding screening, counseling, digital CBT, crisis triage, and family support into school-linked and community-linked pediatric pathways.

WHO estimates that one in seven adolescents aged 10–19 lives with a mental disorder, and that these conditions account for 15% of disease burden in that age group, yet much of this demand remains unrecognized or untreated, which defines a clear uncaptured service market rather than a demand force already fully reflected in baseline growth.

The strategic white space is to create hybrid B2B2C platforms sold to schools, municipalities, insurers, and pediatric provider networks with per-student or per-member contracts, where CAC can fall 25–40% versus clinic-led acquisition, clinician utilization can rise 15–20% through stepped care, and digital-first triage can shift 30–50% of mild-to-moderate cases away from high-cost specialist settings; with adolescent cohorts representing a large and recurring population block, these platform models can open a scalable, higher-frequency revenue stream capable of adding roughly +1.6% points to market CAGR in countries where school systems and payers can be aligned quickly.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Pediatric virtual specialty hubs | +1.8% | North America core, EU, GCC, urban APAC | Short term (≤ 2 years) |

| Home-based chronic pediatric care | +2.1% | North America, EU, Japan, South Korea, tier-1 China | Medium term (2-4 years) |

| School-linked mental health platforms | +1.6% | North America, EU, India, Brazil, Southeast Asia | Short term (≤ 2 years) |

| Climate-resilient child health systems | +1.4% | South Asia, Sub-Saharan Africa, ASEAN, LATAM | Medium term (2-4 years) |

| Vaccine catch-up and zero-dose outreach | +1.9% | Africa core, South Asia, fragile MENA markets | Short term (≤ 2 years) |

| Pediatric retail-financing ecosystems | +1.3% | India, Indonesia, Philippines, Nigeria, Egypt, LATAM | Long term (≥ 4 years) |

Regional Analysis

North America Held the Largest Share of the Global Pediatric Healthcare Market.

In 2025, North America dominated the global pediatric healthcare market by accounting 36.9% and us$ 19.1 billion revenue, owing to its sophisticated healthcare infrastructure, high healthcare expenditure, robust insurance coverage, and broad availability of specialist pediatric services. The region has a well-established network of children’s hospitals, pediatric specialist clinics, and research facilities that help with the diagnosis and treatment of a variety of juvenile disorders.

Rising prevalence of chronic pediatric illnesses, increased acceptance of new medical technologies, and strong government support for child health initiatives all help to drive market expansion. Furthermore, the presence of major pharmaceutical and healthcare corporations, combined with continued expenditures in pediatric research and innovation, helps to improve the region’s market position.

Europe is a substantial market for pediatric healthcare, thanks to universal healthcare systems, widespread vaccine coverage, and increasing spending in child health and preventative care initiatives. Demand for early disease diagnosis, pediatric specialized care, and digital health solutions is increasing across the region. Government activities focused at enhancing healthcare accessible and lowering pediatric disease burdens bolster market growth.

Asia Pacific is predicted to develop the fastest throughout the forecast period, owing to its huge pediatric population, rising healthcare expenditure, improved healthcare infrastructure, and growing awareness of child health. Countries such as China, India, and Japan are investing heavily in pediatric hospitals, immunization programs, and healthcare modernization initiatives.

Meanwhile, Latin America, the Middle East, and Africa are witnessing consistent development, thanks to expanded healthcare access, increased government healthcare investments, and continued initiatives to strengthen maternal and child healthcare services. Growing adoption of telehealth solutions and international healthcare support programs is also contributing to market development across these regions.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global pediatric healthcare market is moderately consolidated, with the top market players accounting for a sizable chunk of overall market revenue. Large pharmaceutical businesses, pediatric hospital networks, medical device makers, and healthcare service providers maintain strong market positions thanks to diverse product portfolios, improved treatment capabilities, and widespread geographic reach.

Continuous investment in pediatric medication discovery, vaccine innovation, specialized healthcare services, and digital health technology fuels market rivalry. Strategic relationships with healthcare institutions, government agencies, and research organizations are also important for increasing market competitiveness.

Key players in the pediatric healthcare industry, including Pfizer Inc., Johnson & Johnson, Sanofi, GlaxoSmithKline plc (GSK), Merck & Co., Inc., are concentrating on innovation, product development, and strategic collaborations to increase their market position. To improve treatment outcomes, companies are investing in pediatric vaccinations, pharmaceuticals tailored to children, sophisticated diagnostics, and digital health platforms.

They are also increasing telemedicine services, improving specialist pediatric care capabilities, and seeking partnerships, acquisitions, and research efforts to diversify their portfolio. Continuous attempts to improve the accessibility, cost, and quality of pediatric care continue to be significant drivers of worldwide market rivalry.

Major Key Players

- Pfizer Inc.

- Sanofi S.A.

- GlaxoSmithKline plc (GSK)

- Novartis AG

- Merck & Co., Inc.

- AstraZeneca plc

- Boehringer Ingelheim GmbH

- Gilead Sciences, Inc.

- Johnson & Johnson (incl. Janssen)

- Eli Lilly and Company

- Abbott Laboratories

- Mylan N.V. (now part of Viatris)

- Eisai Co., Ltd.

- Pediapharm Inc.

- Perrigo Company plc

Key Development

- In June 2025, Merck received U.S. FDA approval for ENFLONSIA™ (clesrovimab), a preventive treatment designed to protect infants from respiratory syncytial virus (RSV), strengthening efforts to reduce severe respiratory infections among young children.

- In May 2025, the U.S. FDA approved Sanofi’s MenQuadfi meningococcal vaccine for infants as young as six weeks of age, based on data from more than 6,000 infants and toddlers, expanding protection against invasive meningococcal disease in pediatric populations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 51.92 Bn |

| Forecast Revenue (2035) | US$ 75.52 Bn |

| CAGR (2026-2035) | 3.84% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Service (Preventive & Primary Care, Specialty & Critical Care, Home Healthcare, and Telehealth & Digital Health), By Product Type (Health Products) (Vaccines, Therapeutics/Drugs (Antibiotics, Antivirals, Analgesics, etc.), Nutritional Supplements (Infant Formula, Pediatric Nutrition), and Other Pediatric Health Products), By Type (Chronic Illnesses and Acute Illnesses), By End User (Hospitals, Specialty Pediatric Clinics, Pediatric Rehabilitation Centers, Home Healthcare Providers, Academic & Research Institutions, and Government & Public Health Agencies) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Pfizer Inc., Sanofi S.A., GlaxoSmithKline plc (GSK), Novartis AG, Merck & Co., Inc., AstraZeneca plc, Boehringer Ingelheim GmbH, Gilead Sciences, Inc., Johnson & Johnson (including Janssen), Eli Lilly and Company, Abbott Laboratories, Mylan N.V. (now part of Viatris), Eisai Co., Ltd., Pediapharm Inc., Perrigo Company plc, and other key players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |