Quick Navigation

Report Overview

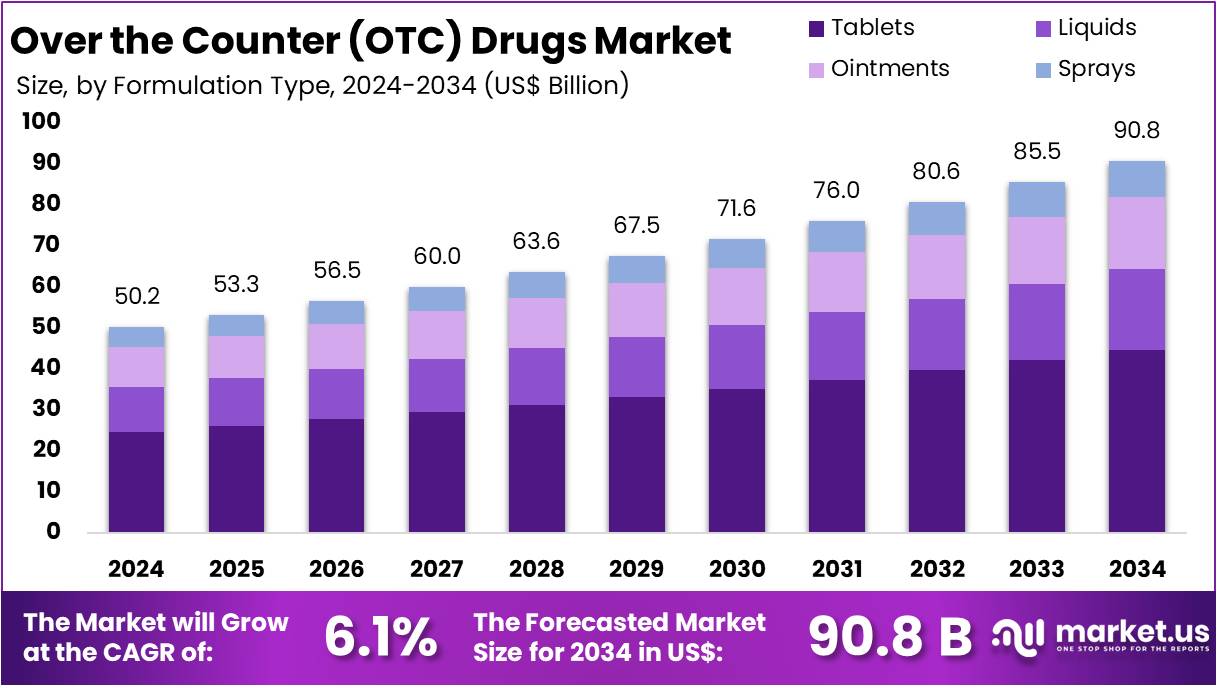

The Global Over the Counter (OTC) Drugs Market size is expected to be worth around US$ 90.8 Billion by 2034, from US$ 50.2 Billion in 2024, growing at a CAGR of 6.1% during the forecast period from 2025 to 2034.

The Over-the-Counter (OTC) drugs sector is expanding rapidly due to shifting healthcare preferences, rising consumer awareness, and improved accessibility. According to industry observations, growing interest in self-care has encouraged individuals to manage minor health issues like colds, headaches, and allergies without physician intervention. The COVID-19 pandemic reinforced this behavior, as consumers sought safer, quicker treatment alternatives outside clinical settings. A study found that self-medication practices increased significantly during the pandemic, with prevalence ranging from 33.9% to 51.3%.

Government efforts have supported this shift by easing regulations and promoting responsible drug use. For example, in the United States, the Food and Drug Administration (FDA) collected $27 million in fiscal year 2023 under its OTC Monograph Drug User Fee program and spent $26 million to accelerate product reviews. Similarly, in India, amendments to the Drugs and Cosmetics Rules, 1945, aim to formalize the OTC category. These regulatory developments aim to improve product transparency, ensure consumer safety, and reduce strain on healthcare infrastructure.

Economic and technological factors also contribute to the sector’s growth. As per U.S. healthcare data, OTC drugs generate approximately $167.1 billion in annual savings. For every $1 spent on OTC products, the healthcare system saves $7.33. This includes $110.3 billion from avoided clinical visits, $56.8 billion in drug cost savings, and $45 billion through workplace productivity gains. These savings underscore the economic value of OTC medications in enhancing healthcare efficiency.

Online retail platforms have also widened the reach of OTC drugs. E-commerce has improved access for consumers in rural or underserved regions by offering product information, reviews, and doorstep delivery. In parallel, the rising demand for herbal and natural remedies has strengthened the segment. For instance, traditional Indian medicines like Ayurveda are becoming increasingly mainstream, driving demand for natural formulations perceived as safer and more holistic.

However, this growing reliance on OTC drugs is not without risks. According to the World Health Organization (WHO), over 50% of medicines are improperly prescribed, dispensed, or consumed. A study by Lippincott Journals revealed that 50.65% of respondents lacked proper knowledge of OTC medications. Misuse may result in severe consequences, including adverse drug reactions, antibiotic resistance, or delayed diagnosis of serious health conditions. Therefore, public education on correct dosage and responsible usage remains essential.

Demographic trends further influence OTC drug consumption. Aging populations and increasing chronic diseases have led to higher demand for accessible medication. Older adults often prefer OTC options for managing recurring conditions. Moreover, pharmaceutical companies are investing in product innovation. For example, advancements in packaging, digital tools, and new formulations are enhancing user experience. These innovations, combined with increased disposable income and health consciousness among the middle class, are expected to sustain the market’s upward trajectory.

Key Takeaways

- By 2034, the global OTC drugs market is projected to reach approximately US$ 90.8 billion, up from US$ 50.2 billion in 2024.

- The market is expected to grow at a compound annual growth rate (CAGR) of 6.1% between 2025 and 2034, reflecting steady demand.

- In 2024, cold and cough remedies led the drug category segment, accounting for over 28.5% of the global OTC drugs market share.

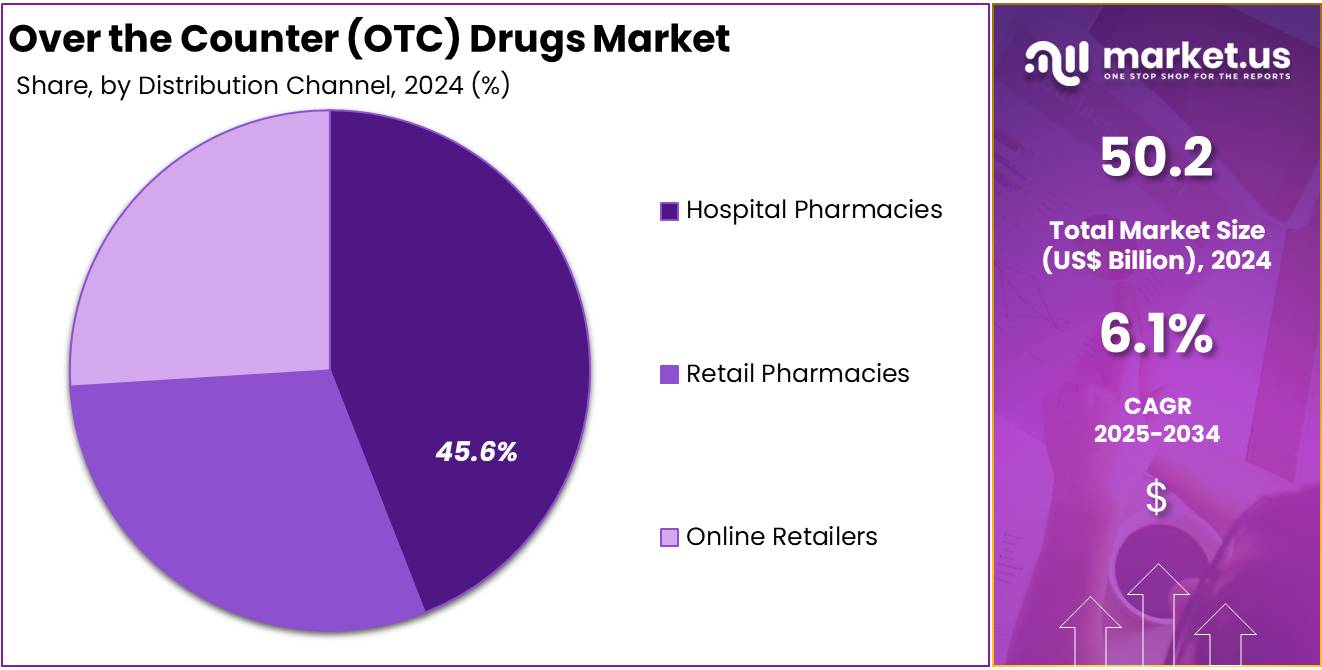

- Hospital pharmacies captured the largest distribution share in 2024, holding more than 45.6% of the overall OTC drug market segment.

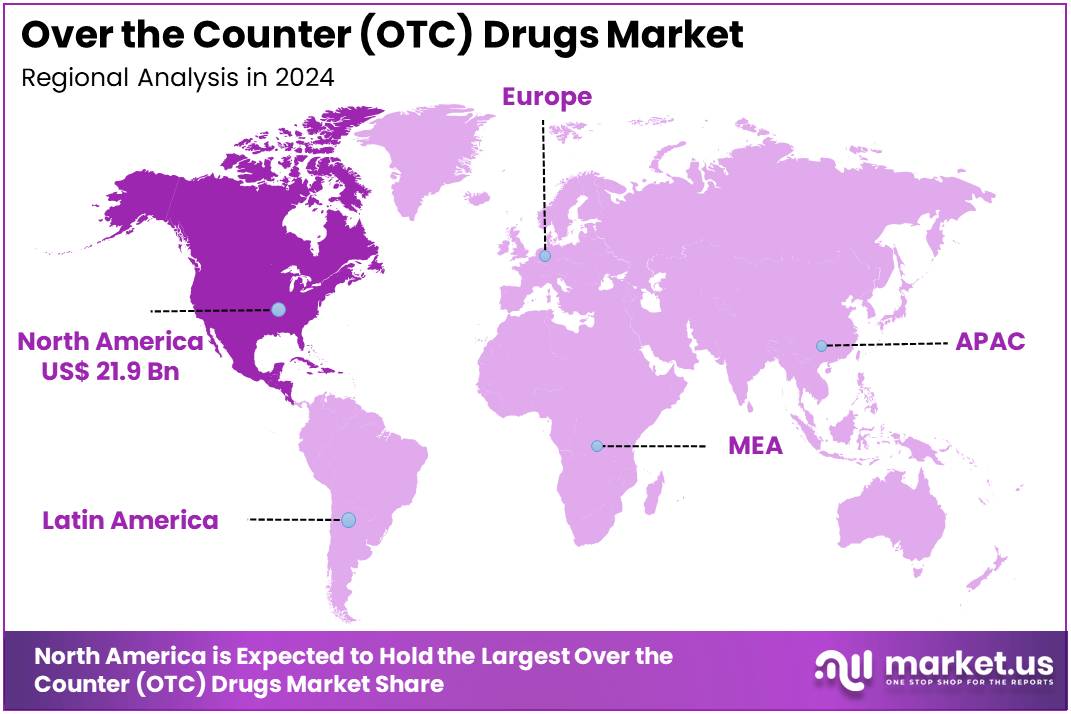

- North America dominated the regional landscape in 2024, representing over 43.7% market share and achieving a valuation of US$ 21.9 billion.

Drug Category Analysis

In 2024, the Cold and Cough Remedies section held a dominant market position in the Drug Category Segment of the Over the Counter (OTC) Drugs Market. It captured more than a 28.5% share. According to industry observations, this growth was driven by increased cases of seasonal flu and respiratory infections. Experts noted that consumers preferred quick-relief options. Easy availability and widespread use made these products a leading choice. Air pollution and changing weather patterns also played a key role in rising demand.

Vitamins and Supplements were observed as the next major category. Analysts highlighted growing interest in preventive healthcare. Consumers across age groups were seen buying vitamin D, vitamin C, and multivitamin products. This trend was particularly strong among older adults. The segment grew as people became more health-conscious. Digestive and Intestinal Remedies also saw steady demand. Market participants reported rising purchases of antacids, laxatives, and probiotics due to unhealthy diets and sedentary lifestyles.

Skin Treatment products maintained consistent market performance. Analysts linked this to the widespread occurrence of minor skin conditions like acne and rashes. OTC creams, ointments, and antiseptics were commonly used for self-treatment. Analgesics also held a strong presence in the market. These were frequently used for headaches, body aches, and menstrual pain. Sleeping Aids gained moderate traction, as more users turned to melatonin and herbal tablets. The Others segment, including eye care and smoking cessation products, showed targeted but growing demand.

Formulation Type Analysis

In 2024, the tablets section held a dominant market position in the formulation type segment of the Over the Counter (OTC) drugs market, and captured more than a 42.4% share. Tablets remain the most preferred option for self-medication. They offer accurate dosing and a longer shelf life. These products are widely used to treat headaches, fever, colds, and allergies. Their availability in multiple dosage strengths makes them convenient for all age groups. Retail accessibility further supports their strong market presence.

Following tablets, liquid formulations held the second-largest share. Liquids are often chosen for children and older adults who have trouble swallowing pills. These products are popular for treating coughs, indigestion, and sore throats. Easy dosing and improved taste profiles have helped boost demand. The use of child-friendly syrups in pediatric care is expanding. Liquid OTC drugs are now available in a variety of forms, including suspensions and solutions, offering flexibility in administration.

Ointments and sprays accounted for the remaining market share. Ointments are commonly used for skin-related issues such as burns, rashes, and minor wounds. They deliver medicine directly to the affected area, which speeds up recovery. Sprays are gaining attention due to their quick action and ease of use. These are widely used for nasal relief, pain management, and wound care. Their touch-free application also reduces contamination risks. Growth in self-care habits is supporting demand for these formats.

Distribution Channel Analysis

In 2024, the hospital pharmacies section held a dominant market position in the distribution channel segment of the Over the Counter (OTC) drugs market and captured more than a 45.6% share. This leadership was due to the high patient visits to hospitals. Experts note that hospital pharmacies ensure supervised access to OTC medicines. This helps reduce misuse and builds consumer trust. The presence of trained pharmacists adds value to the purchase experience. As a result, hospitals remain a preferred channel for many buyers.

Retail pharmacies ranked next in terms of OTC drug distribution. Analysts explain that their strong presence in cities and towns boosts customer access. Retail stores also offer a wide variety of OTC drugs. Customers often seek help from local pharmacists for quick advice. Long working hours and nearby locations make retail pharmacies highly convenient. Their trusted role in communities continues to support market demand across therapeutic categories such as pain relief, cold remedies, and digestive aids.

Online retailers are gaining momentum in the OTC drugs market. Market observers link this trend to rising digital health awareness and internet access. Online stores offer home delivery and easy reordering options. These features attract busy consumers. Many platforms also provide discounts and customer reviews, enhancing the buying experience. Though still emerging, this channel is expanding quickly. As digital adoption grows, e-pharmacies are expected to capture a larger share in the coming years, especially among tech-savvy and urban users.

Key Market Segments

By Drug Category

- Cold and Cough Remedies

- Vitamins and Supplements

- Digestive and Intestinal Remedies

- Skin Treatment

- Analgesics

- Sleeping Aids

- Others

By Formulation Type

- Tablets

- Liquids

- Ointments

- Sprays

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Retailers

Drivers

Increasing Self-Medication Practices

The over-the-counter (OTC) drugs market is witnessing rapid expansion due to rising self-medication practices among consumers. People are increasingly using OTC medicines to treat minor health issues such as colds, headaches, or digestive problems. This growing trend reflects a shift towards self-care, supported by better health awareness. Consumers now have easy access to drug-related information through digital platforms. These factors reduce reliance on healthcare professionals for non-serious conditions. This shift is helping people make informed choices about their health using readily available OTC solutions.

Self-medication is emerging as a key driver in the growth of the OTC drugs market. According to a study, around 81% of adults choose OTC medicines as the first line of treatment for minor illnesses. This behavior is increasingly common in both developed and emerging economies. Improved health literacy and internet access are encouraging people to handle simple health problems on their own. This trend is shaping consumer behavior and boosting the demand for a wider variety of OTC products across pharmacies and online platforms.

OTC drugs offer significant cost benefits to healthcare systems globally. For instance, these medicines help generate $146 billion in savings annually. This includes $94.8 billion in clinical cost savings and $51.6 billion in drug cost reductions. By using OTC medications, individuals can avoid costly doctor visits for manageable conditions. These savings extend to governments and insurance providers. Moreover, OTC access reduces the pressure on healthcare infrastructure and allows better resource allocation to critical and chronic care services.

Greater reliance on OTC drugs also brings productivity gains. For example, the U.S. healthcare system could save $5.2 billion annually if half of the unnecessary primary care visits were replaced by responsible self-care using OTC medicines. This shows the potential of OTC products in supporting economic efficiency. As distribution channels continue to grow—especially through retail pharmacies and online platforms—the availability and accessibility of OTC drugs are expected to rise. This positions the OTC market for sustained long-term growth globally.

Restraints

Risk of Misuse and Incorrect Dosage

One of the key restraints in the Over the Counter (OTC) drugs market is the potential for misuse and incorrect dosage. Consumers often use these medications without professional supervision. This can lead to overuse, taking higher doses than recommended, or using multiple drugs that interact negatively. Such practices are especially common in treating recurring symptoms like headaches, colds, or allergies. These issues raise public health concerns and challenge the perception that OTC drugs are completely safe when used without medical advice.

Prolonged and unsupervised use of OTC medications may result in adverse health effects. For example, excessive use of pain relievers can cause liver damage or gastrointestinal issues. Additionally, self-medicating may delay the diagnosis of more serious conditions. As a result, health authorities and regulatory agencies have introduced stricter labeling requirements and consumer education initiatives. These regulatory actions are designed to mitigate health risks and improve patient safety, but they may also slow market growth by restricting access or limiting product claims.

Opportunities

Expansion of E-Pharmacy Platforms

The growing popularity of e-pharmacy platforms is creating new growth avenues for the over-the-counter (OTC) drugs market. Consumers now prefer to purchase medicines online due to the convenience and ease of access. These platforms enable users to compare prices, check product details, and receive doorstep delivery. This digital shift is especially important in urban and semi-urban regions where time constraints limit in-store visits. Additionally, the presence of user-friendly mobile apps and multilingual interfaces is helping to improve consumer engagement across different demographics.

In regions with poor physical pharmacy infrastructure, e-pharmacies serve as a critical healthcare access point. This is particularly true in rural and underserved areas, where brick-and-mortar pharmacies are often scarce. Online platforms bridge this gap by delivering OTC medications directly to consumers, improving treatment continuity. Governments and private players are increasingly supporting digital healthcare initiatives. This trend aligns with broader goals of improving universal healthcare access and enhancing medication adherence through timely deliveries.

The COVID-19 pandemic significantly accelerated the adoption of digital health services, including online medicine purchases. Lockdowns and infection fears pushed consumers toward contactless options, and many have continued these habits post-pandemic. E-pharmacies capitalized on this shift by expanding their product portfolios, integrating AI-based recommendation tools, and offering subscription-based services for regular purchases. These advancements have created a more reliable and efficient supply chain for OTC products.

Moreover, the use of digital platforms allows for personalized marketing and health recommendations based on user data. Many e-pharmacies now offer tailored product suggestions, dosage reminders, and wellness tips through integrated apps. This targeted approach enhances the consumer experience while driving higher engagement and sales conversion rates. As technology continues to evolve, e-pharmacy platforms are expected to become central to the OTC drug distribution model in both developed and emerging markets.

Trends

Increased Demand for Natural and Herbal OTC Products

There is a noticeable rise in consumer demand for natural and herbal over-the-counter (OTC) drugs. This shift is especially seen in products related to digestive health, stress relief, and common colds. Consumers are increasingly choosing plant-based ingredients like peppermint, ginger, chamomile, and echinacea over synthetic alternatives. The preference for natural solutions is influenced by cultural traditions, wellness trends, and growing skepticism about prolonged chemical drug use. As a result, herbal OTC products are gaining higher visibility in pharmacies and retail shelves.

The preference for holistic health is growing among health-conscious consumers. People are paying closer attention to ingredient lists and avoiding artificial additives. Products that emphasize “clean labels” and natural origin are more likely to attract attention. This is particularly evident among millennials and Gen Z, who often associate natural ingredients with better safety profiles and long-term wellness. The rising popularity of digital wellness platforms is also contributing to increased awareness about the health benefits of herbal ingredients.

In the OTC segment, herbal immunity boosters and sleep aids have become popular categories. Products with ingredients like ashwagandha, melatonin from natural sources, and turmeric have gained traction. These ingredients are often promoted for reducing stress, improving sleep quality, and supporting immune function. Consumers trust traditional medicine systems such as Ayurveda and Traditional Chinese Medicine (TCM), which further supports demand for botanical alternatives in modern retail.

Pharmaceutical and consumer health companies are responding by expanding their natural product lines. Innovation in formulations, such as sugar-free, vegan, and preservative-free herbal tablets or syrups, is on the rise. Regulatory support for traditional medicines in countries like India and China is further aiding product launches. As consumers continue to prioritize preventive health and sustainable lifestyles, the natural OTC segment is expected to grow steadily in both developed and emerging markets.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 43.7% share and holds US$ 21.9 Billion market value for the year. This strong position is driven by high consumer awareness and easy access to OTC medications across the United States and Canada. Widespread retail availability and the presence of well-established pharmacy chains have contributed to steady sales growth. The increasing shift towards self-medication for minor ailments has also fueled the demand for OTC products in the region.

The U.S. Food and Drug Administration (FDA) has supported the expansion of OTC drug categories by approving more medications for non-prescription use. This regulatory flexibility has enabled faster product launches and greater consumer choice. Moreover, digital platforms and e-pharmacy channels have improved product accessibility, especially in rural areas. As a result, consumers are more empowered to manage their own health, boosting market revenues.

Chronic conditions such as allergies, digestive issues, and cold and flu symptoms are common in the region, encouraging regular OTC usage. North America also benefits from a high number of aging individuals who frequently rely on OTC remedies for pain relief and sleep support. Combined with rising healthcare costs and efforts to reduce clinical burdens, OTC drugs continue to serve as a cost-effective first-line solution in North America’s evolving healthcare landscape.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Over the Counter (OTC) drugs market is led by established players with strong brand portfolios and global operations. Abbott remains a key contributor, focusing on nutritional supplements and gastrointestinal health. Its growth is supported by innovation and digital health integration. Alkem Laboratories, with its diverse product range in antacids and dermatology, leverages its deep distribution in India and expanding global presence. Aytu Biopharma is gaining traction through its focus on wellness products, pediatric care, and sleep aids, supported by strategic acquisitions and retail partnerships.

Bayer AG holds a leading position in the OTC market through its broad range of products including pain relief and cardiovascular support. The company’s global strategies, brand equity, and investment in R&D drive consistent performance. Cipla has made significant progress in the OTC segment, with a focus on respiratory and digestive health. It uses digital engagement and competitive pricing to reach urban and rural consumers. Cipla also benefits from strong manufacturing capabilities and consumer education initiatives.

GlaxoSmithKline (GSK) continues to lead with trusted brands in oral health, pain management, and nutrition. Its market strategy is built around innovation and targeted outreach. GSK maintains dominance in North America and Europe, while increasing its footprint in Asia and Latin America. Other key participants include Johnson & Johnson, Sanofi, Reckitt Benckiser, and Procter & Gamble. These companies focus on expanding OTC lines, retail accessibility, and digital tools to enhance their market share.

Market Key Players

- Abbott

- Alkem Laboratories

- Aytu Biopharma

- Bayer AG

- Cipla

- GlaxoSmithKline

- Johnson & Johnson Services

- Pfizer

- Piramal Enterprises

- Reckitt Benckiser Group

- Sanofi

- Sun Pharmaceuticals

- Teva Pharmaceutical Industries

Recent Developments

- In June 2024: Abbott received U.S. Food and Drug Administration (FDA) clearance for two over-the-counter (OTC) continuous glucose monitoring (CGM) systems, Libre Rio and Lingo. Libre Rio is designed for adults with Type 2 diabetes who do not use insulin, offering them a convenient way to monitor glucose levels without prescription barriers. Lingo targets health-conscious individuals without diabetes, providing personalized glucose insights to support overall well-being. Both devices are based on Abbott’s FreeStyle Libre technology and aim to expand access to glucose monitoring.

- In January 2024: Sun Pharma completed the merger with Taro Pharmaceutical Industries, acquiring the remaining stake for $347.73 million. This transaction consolidated Sun Pharma’s ownership of Taro to 100%, leading to Taro’s delisting from the New York Stock Exchange. The merger is anticipated to strengthen Sun Pharma’s position in the OTC market by integrating Taro’s established formulations and specialty products with Sun Pharma’s extensive global reach.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 50.2 Billion |

| Forecast Revenue (2034) | US$ 90.8 Billion |

| CAGR (2025-2034) | 6.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Category (Cold and Cough Remedies, Vitamins and Supplements, Digestive and Intestinal Remedies, Skin Treatment, Analgesics, Sleeping Aids, Others), By Formulation Type (Tablets, Liquids, Ointments, Sprays), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Retailers) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Abbott, Alkem Laboratories, Aytu Biopharma, Bayer AG, Cipla, GlaxoSmithKline, Johnson & Johnson Services, Pfizer, Piramal Enterprises, Reckitt Benckiser Group, Sanofi, Sun Pharmaceuticals, Teva Pharmaceutical Industries |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Drugs Market")