Quick Navigation

Report Overview

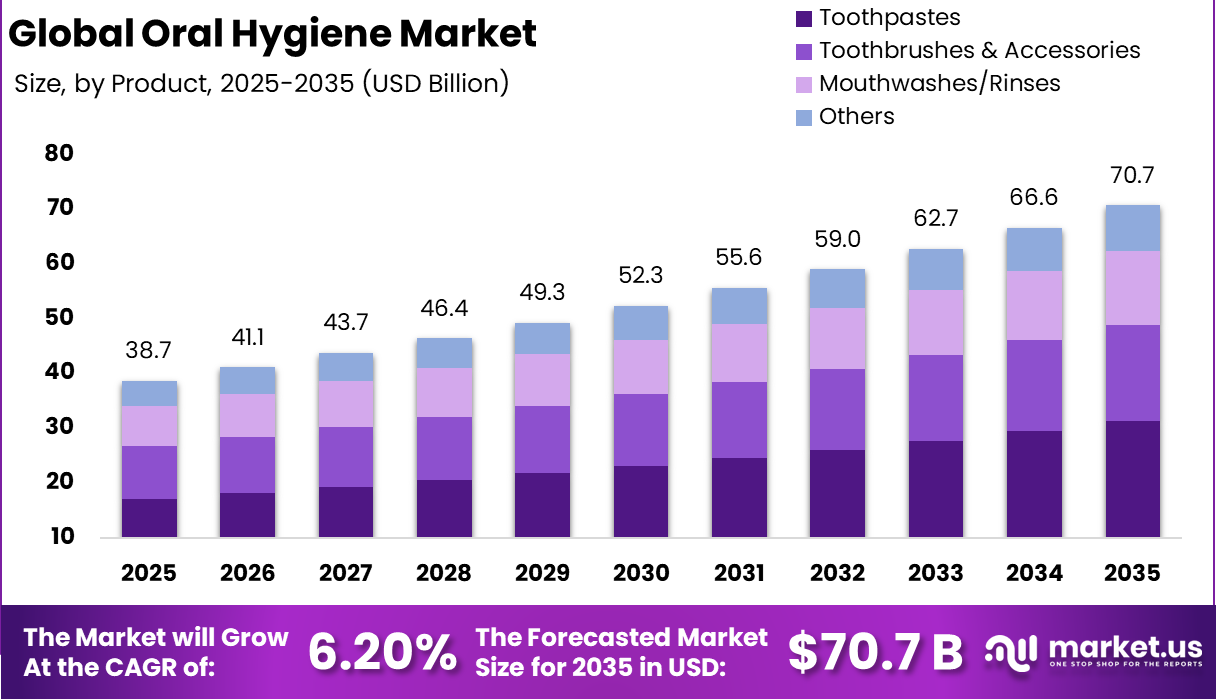

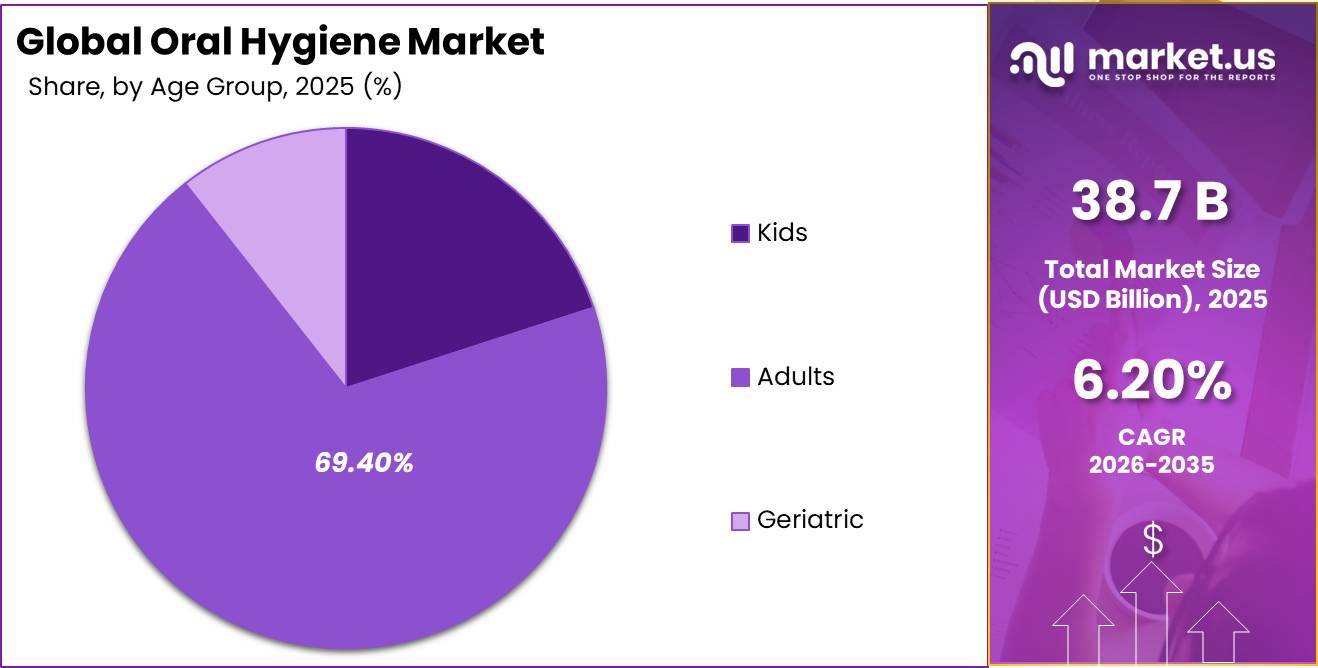

Global Oral Hygiene Market size is expected to be worth around USD 70.7 Billion by 2035 from USD 38.7 Billion in 2025, growing at a CAGR of 6.20% during the forecast period 2026 to 2035.

The oral hygiene market covers consumer and therapeutic products designed to maintain or improve oral health. This includes toothpastes, toothbrushes and accessories, mouthwashes and rinses, and adjacent hygiene formats. Products reach consumers through both offline retail networks and online channels. This reflects a market with broad household penetration and rising clinical engagement across age groups and geographies.

Key Takeaways

- Oral Hygiene Market size in 2025 is valued at USD 38.7 Billion, reaching USD 70.7 Billion by 2035.

- The market grows at a CAGR of 6.20% from 2026 to 2035.

- By Product, Toothpastes dominates with a 44.20% share.

- By Age Group, Adults holds a dominant share of 69.40%.

- By Formulation, Paste leads with a 56.80% share.

- By Distribution Channel, Offline channels account for 76.30% of sales.

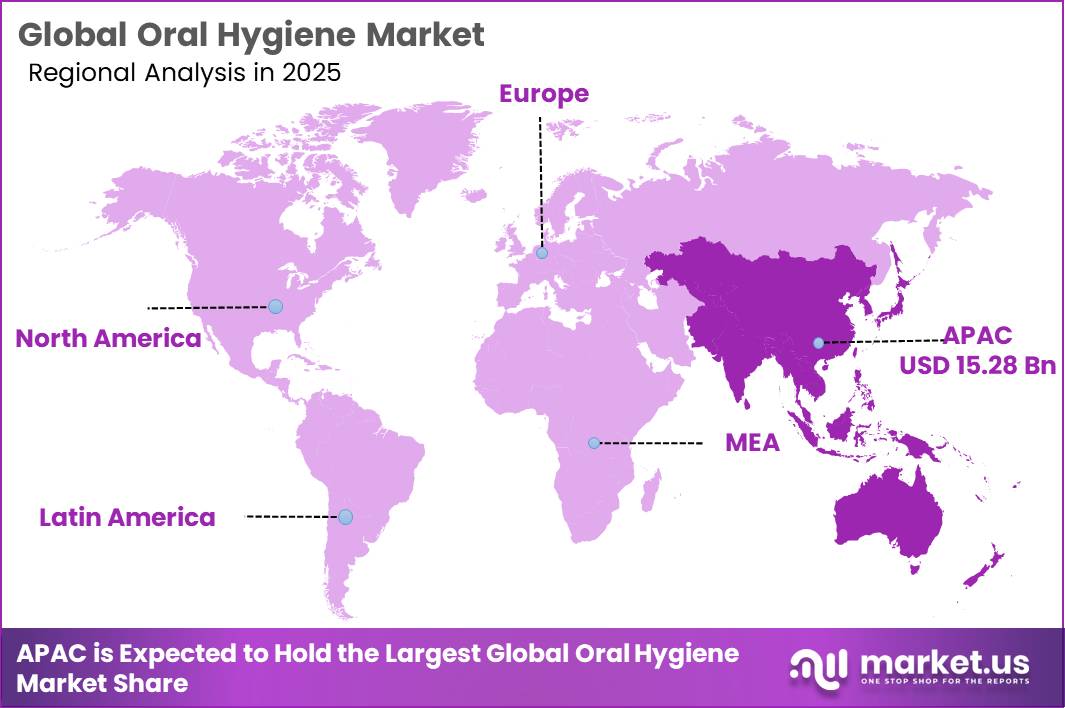

- Asia Pacific leads all regions with a 39.50% market share, valued at USD 15.29 Billion in 2025.

Government health agencies and international bodies are increasing oral health mandates across school-based programs and public dental care schemes. These initiatives create structured demand for baseline oral hygiene products in markets where household penetration remains low. This signals that institutional procurement, not just retail consumer demand, will shape volume growth in emerging regions through the forecast period.

According to a meta-analysis of 29 studies covering 17,734 participants, the global pooled prevalence of twice-daily toothbrushing among adults was 44.6%, with only 25.8% of females and 12.2% of males brushing twice daily. This gap between recommended and actual brushing behavior identifies a large addressable population for behavior-change marketing and preventive product formats. Brands that invest in compliance-focused messaging and convenient format innovation will access this underserved group first.

Data from the Journal of Global Health shows 80.9% of people brush their teeth one to three times per day, while 8.6% never brush at all. In January 2026, UK oral health brand Gutology secured £1.8 million in funding to develop microbiome-focused oral care products and expand into German and US markets. This signals investor confidence in science-backed oral care formats targeting hygiene gaps at the population level.

Product Analysis

Toothpastes dominates with 44.20% due to daily household use and wide format range.

In 2025, Toothpastes held a dominant market position in the By Product segment of the Oral Hygiene Market, with a 44.20% share. Daily mandatory usage, broad price-point coverage from economy to premium, and continuous formulation innovation across whitening, sensitivity, and herbal variants sustain this leadership. This means vendors competing on product differentiation rather than price alone will hold stronger margin positions within this segment.

Toothbrushes and Accessories capture 25.00% of the market, driven by electric toothbrush adoption and accessory upsell behavior. Global household adoption of electric toothbrushes has crossed 28% in urban middle-income populations, creating a recurring consumables stream through replacement heads and compatible accessories. This consumables model delivers more predictable revenue than one-time manual brush sales.

Mouthwashes and Rinses account for 19.00% share, with growth concentrated in therapeutic and alcohol-free formulations. Consumer sensitivity to alcohol-based rinses is pushing brands toward sulfate-free and antimicrobial alternatives. This creates a product differentiation window for manufacturers that lead reformulation ahead of mainstream competitors.

Age Group Analysis

Adults dominates with 69.40% due to high purchase frequency and premium product uptake.

In 2025, Adults held a dominant market position in the By Age Group segment of the Oral Hygiene Market, with a 69.40% share. Adult consumers drive volume through routine daily purchases across multiple product categories and demonstrate willingness to trade up into premium formulations. This means adult-targeted positioning delivers the highest return on marketing investment in the current market structure.

Kids represent 20.00% of the market, supported by pediatric-specific flavors, fluoride-level variants, and licensed brand formats that drive parental purchase decisions. Development of children-specific oral care products targeting early childhood caries prevalence in emerging economies reinforces this segment’s structural importance. Brands that establish loyalty at the pediatric stage lock in long-term household adoption.

Geriatric consumers account for 10.60% of market share, with demand concentrated in denture care, dry-mouth treatment, and periodontal sensitivity products. Japan, Western Europe, and China represent the primary geographic corridors for this segment, driven by aging population demographics. This segment is structurally underpenetrated relative to its clinical need, creating a clear entry point for specialized product developers.

Key Market Segments

By Product

- Toothpastes

- Toothbrushes & Accessories

- Mouthwashes/Rinses

- Others

By Age Group

- Kids

- Adults

- Geriatric

By Formulation

- Gel

- Paste

- Liquid

- Powder

- Spray

- Others

By Distribution Channels

- Online

- Offline

Drivers

The rapid shift toward digital and direct-to-consumer oral care channels is transforming how brands engage consumers and drive sales. E-commerce is the fastest-growing distribution channel, supported by online purchasing growth and subscription-based oral care programs. Quick-commerce platforms are accelerating replenishment purchases through on-demand delivery, increasing purchase frequency for everyday products such as toothpaste and mouthwash.

D2C subscription models generate 15 to 25% higher operating margins by reducing intermediary costs and enabling personalized marketing. Digital channels also provide first-party consumer data that supports product innovation and targeted premium product recommendations. Social media is a major discovery platform, with 53% of US Gen Z consumers reporting they use social media for dental advice, which gives brands with strong digital presence a direct path to high-value younger consumers.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Burden of Oral Disease & Preventive Care Shift — Escalating prevalence of caries, periodontitis, and edentulism driving clinical & consumer-grade preventive product demand | +1.4% | Global core; highest uplift in APAC, Sub-Saharan Africa, South Asia | Short–Medium Term (1–4 yrs) |

| Premiumization & Oral Aesthetics Boom — Consumer trading-up into whitening, sensitivity, hydroxyapatite, and cosmetic-grade formulations, especially among Millennials & Gen Z | +1.2% | North America core; EU secondary; APAC corridors (China, South Korea, Japan) | Short–Medium Term (1–3 yrs) |

| Smart & Connected Oral Care Technology Adoption — AI-enabled toothbrushes, IoT integration, app-linked diagnostics, and real-time brushing feedback shifting the product model | +0.9% | North America & Western EU primary; APAC fast-follower (China, ANZ, South Korea) | Medium Term (2–4 yrs) |

| Natural, Organic & Clean-Label Product Demand — Fluoride-free, herbal, microbiome-safe, and ayurvedic formulations disrupting traditional fluoride-dominant BoM | +0.8% | EU (Germany, UK, France) and South Asia (India) primary; North America spill-over | Short–Medium Term (1–3 yrs) |

| E-Commerce, D2C & Subscription Channel Expansion — Digital distribution and DTC subscription models accelerating consumer acquisition, repeat purchase and margin uplift | +0.7% | North America and East Asia digital-first; EU omnichannel; India/SEA emerging | Short Term (≤ 2 yrs) |

| Aging Population & Geriatric Oral Care Demand — Growing 60+ population driving demand for denture care, dry-mouth, periodontal, and specialist sensitivity products | +0.6% | Japan, Western EU, China, and North America long-term care corridors | Medium–Long Term (3–6 yrs) |

Restraints

Titanium dioxide has become a significant regulatory challenge for oral care manufacturers in Europe after its ban as a food additive over genotoxicity concerns. Toothpaste formulations rely heavily on this ingredient for whitening and opacifying functions, making substitution difficult without altering product appearance and consumer acceptance. European regulatory reviews in 2024 and 2026 confirmed that no direct substitute currently delivers equivalent performance.

Manufacturers must undertake extensive reformulation programs involving stability testing, consumer validation studies, and regulatory re-registration of updated products. European regulators continue evaluating additional oral care ingredients, including sodium fluoride and other functional actives. This expanding ingredient-safety scrutiny is increasing R&D workloads, extending product development timelines, and diverting resources away from innovation initiatives across oral care portfolios.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Absent/Inadequate Dental Insurance Coverage | -1.1% | South & Southeast Asia, MENA, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Entrenched Traditional Oral Hygiene Practices | -0.8% | Rural South Asia, Sub-Saharan Africa, rural Southeast Asia | Long term (≥ 4 years) |

| US Trade Tariffs & Import Cost Inflation | -0.7% | North America (manufacturing & retail); cascading to EU, APAC exporters | Short term (≤ 2 years) |

| Titanium Dioxide & Ingredient Safety Bans | -0.5% | European Union regulatory core; extension risk to UK, Australia | Medium term (2–4 years) |

| Oligopolistic Market Concentration | -0.6% | Global; particularly suppressive in price-sensitive APAC, Latin America | Long term (≥ 4 years) |

| Product Safety Recalls & Consumer Trust Erosion | -0.4% | North America, Europe; emerging risk in APAC e-commerce channels | Short term (≤ 2 years) |

Challenges

Fluoride is facing regulatory scrutiny across major oral care markets, creating formulation and compliance challenges for manufacturers. Several US states have introduced restrictions on fluoride use, while regulatory actions targeting fluoride-containing pediatric products have intensified safety debates. In Europe, ongoing evaluations of sodium fluoride could reshape compliance requirements for toothpaste and mouthwash formulations across the region.

More than 80% of oral care SKUs in Europe currently rely on fluoride-based ingredients, highlighting the scale of potential disruption. Companies are accelerating development of fluoride-free alternatives such as hydroxyapatite and nano-calcium phosphate. However, reformulation programs typically require 18 to 36 months of stability testing, clinical validation, and regulatory review, creating a compounding operational burden for manufacturers already managing ingredient substitution across multiple markets.

A cross-sectional study of 44,779 respondents in Saudi Arabia found 57.3% of the population brushed their teeth less than once a day. This low brushing frequency reflects structural access and education gaps that compound the regulatory challenges manufacturers already face when entering these markets. Brands that build education-led market entry programs alongside affordable product formats will convert this behavioral gap into measurable volume.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Fluoride Regulatory Fragmentation | -0.8% | North America, EU regulatory hubs, Australia | Medium term (2–4 years) |

| Raw Material Volatility & Supply Chain Friction | -0.7% | Global; severity concentrated in APAC sourcing corridors & EU manufacturing | Medium term (2–4 years) |

| Oral Healthcare Workforce Deficit | -0.6% | North America, rural APAC, Sub-Saharan Africa | Long term (≥ 4 years) |

| Sustainable Packaging Transition Costs | -0.5% | EU compliance core, North America, urban APAC | Medium term (2–4 years) |

| Premiumisation–Price Sensitivity Divide | -0.9% | South & Southeast Asia, Latin America, MENA | Long term (≥ 4 years) |

| Smart Oral Care Technology Adoption Friction | -0.6% | North America, Western Europe, urban East Asia | Medium term (2–4 years) |

Opportunities

Growing clinical evidence has established a strong bidirectional relationship between oral health conditions, particularly periodontitis, and chronic diseases such as Type 2 diabetes and cardiovascular disease. Effective periodontal treatment can improve glycemic control and reduce systemic inflammation. Healthcare providers and insurers are incorporating oral health into broader chronic disease management programs, opening a distribution path for specialized oral care products beyond traditional retail channels.

Oral care companies can develop therapeutic toothpastes, periodontal gels, and oral irrigation systems tailored to patients with chronic conditions. Distribution through pharmacies, healthcare facilities, and chronic disease management platforms extends market reach beyond conventional retail. Co-marketing partnerships with healthcare professionals can lower customer acquisition costs while increasing adoption rates among clinically motivated consumer segments.

Figures from an international brushing intervention study show twice-daily brushing increased from 60% to 73% after a 12-month behavior change program. This 13 percentage-point gain demonstrates that structured consumer education programs produce measurable compliance improvements. Brands investing in digital-led behavior change tools and subscription accountability models position themselves to capture this behavior-driven volume uplift ahead of passive competitors.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Oral Microbiome Therapeutics & Probiotic Formats | +1.8% | North America, EU, urban APAC | Medium term (2–4 years) |

| Tele-Dentistry & AI-Powered At-Home Diagnostics | +1.5% | North America core; EU, SEA emerging | Short term (≤ 2 years) |

| Oral–Systemic Health Integration (Chronic Disease Adjacency) | +2.0% | North America, EU, Tier-1 APAC (Japan, South Korea) | Medium–Long term (3–5 years) |

| Emerging-Market Rural Penetration & Affordable Format Innovation | +1.6% | Sub-Saharan Africa, South & Southeast Asia | Medium term (2–4 years) |

| Sustainable & Solid-Format Oral Care (Tablets, Refillables, Zero-Waste) | +1.2% | EU, North America, Urban APAC | Short–Medium term (1–3 years) |

| PE-Led M&A Roll-Up: Dental DSO & Consumer Brand Convergence | +1.4% | North America, Western & Eastern Europe | Short term (≤ 2 years) |

Regional Analysis

Asia Pacific Dominates the Oral Hygiene Market with a Market Share of 39.50%, Valued at USD 15.29 Billion

Asia Pacific holds the largest regional share at 39.50%, valued at USD 15.29 Billion in 2025. Large population bases in China, India, and Southeast Asia, combined with rising urban middle-class incomes, sustain high-volume product consumption. Herbal and ayurvedic product formats are gaining traction in India, where non-fluoride consumer segments are actively seeking alternative oral care solutions aligned with traditional health preferences.

North America represents a mature but high-value market where premiumization and digital direct-to-consumer channels are the primary growth mechanisms. Electric toothbrush adoption, whitening formulations, and AI-integrated oral care devices command higher average selling prices. Consumers in this region demonstrate strong willingness to pay for clinically validated and aesthetics-oriented oral care products, keeping revenue per unit above the global average.

Middle East and Africa remains an early-stage market where oral hygiene penetration varies sharply across urban and rural populations. As reported by a cross-sectional study of 44,779 respondents in Saudi Arabia, 57.3% of the population brushed their teeth less than once a day. This low baseline brushing frequency represents a structural opportunity for brands that invest in public health education and affordable entry-level product distribution.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Colgate-Palmolive Company maintains global distribution dominance across both offline and online channels, with strong presence in every major regional market. Their multi-tier product architecture, spanning economy, mid-market, and premium formulations, allows them to defend volume share in price-sensitive markets while capturing margin growth in premiumizing ones. This breadth creates structural barriers for single-tier challengers.

Procter and Gamble competes primarily through its Oral-B brand, which anchors the electric toothbrush and accessories segment. Their investment in AI-enabled smart toothbrush technology, including real-time brushing analytics and app integration, positions them directly against clinical-grade compliance tools. In April 2026, Novateor Labs launched its SmiloShine Herbafresh Toothpaste, signaling that new herbal entrants are targeting the formulation innovation space where legacy brands like P&G move more slowly.

Key Players

- Colgate-Palmolive Company

- Procter & Gamble

- Koninklijke Philips N.V.

- Unilever

- Johnson & Johnson

- Haleon

- Church & Dwight Co., Inc.

- Kenvue Inc.

- Sunstar Group

- Lion Corporation

Recent Developments

- July 2025 – Swiss dental company vVARDIS secured $50 million in new funding, bringing total financing to $85 million from OrbiMed, to expand the global rollout of its drill-free early tooth decay treatment Curodont.

- April 2026 – vVARDIS announced a strategic minority investment from Apollo-managed funds, establishing the company as a privately held billion-plus healthcare company and supporting expansion of its Curodont technology suite.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 38.7 Billion |

| Forecast Revenue (2035) | USD 70.7 Billion |

| CAGR (2026-2035) | 6.20% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Toothpastes, Toothbrushes and Accessories, Mouthwashes/Rinses, Others), By Age Group (Kids, Adults, Geriatric), By Formulation (Gel, Paste, Liquid, Powder, Spray, Others), By Distribution Channels (Online, Offline) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Colgate-Palmolive Company, Procter and Gamble, Koninklijke Philips N.V., Unilever, Johnson and Johnson, Haleon, Church and Dwight Co. Inc., Kenvue Inc., Sunstar Group, Lion Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |