Global Oral Anticoagulants Market By Drug Class(Vitamin K Antagonists, Direct Oral Anticoagulants) By Indication (Non-valvular Atrial Fibrillation (NVAF), Deep Vein Thrombosis (DVT), Pulmonary Embolism (PE), Post-orthopedic Surgery Thromboprophylaxis, Others) By Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies) Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Nov 2025

- Report ID: 166737

- Number of Pages: 313

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

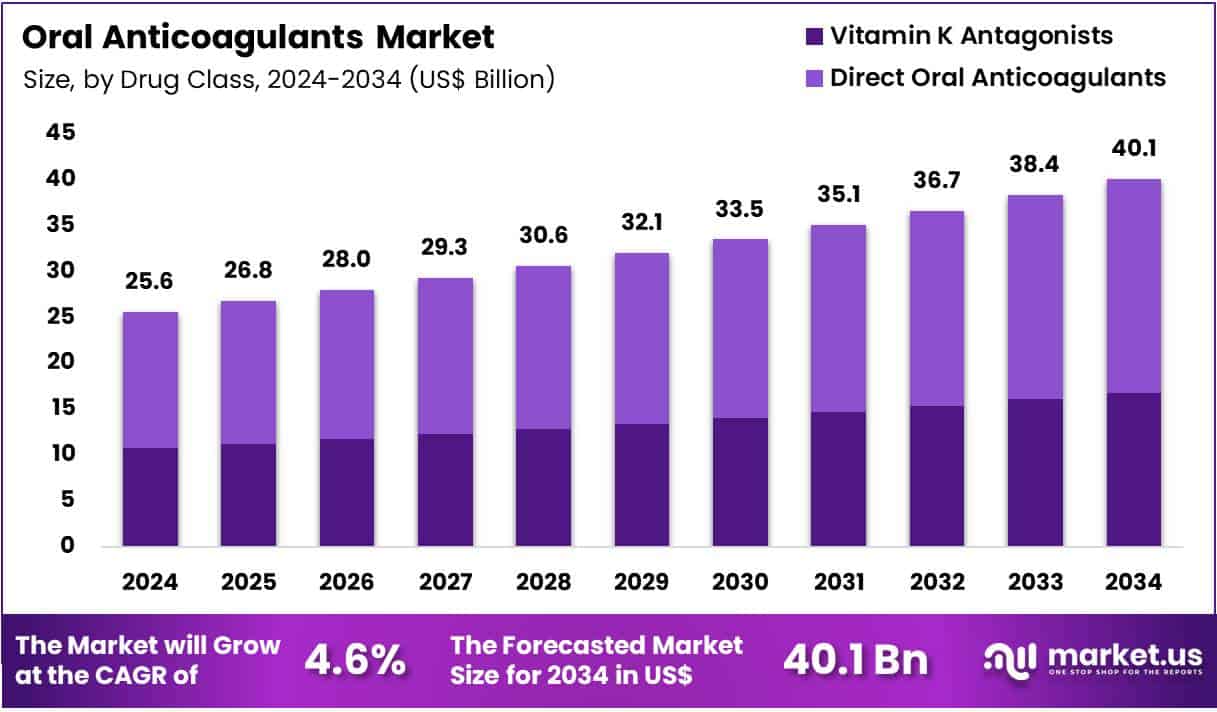

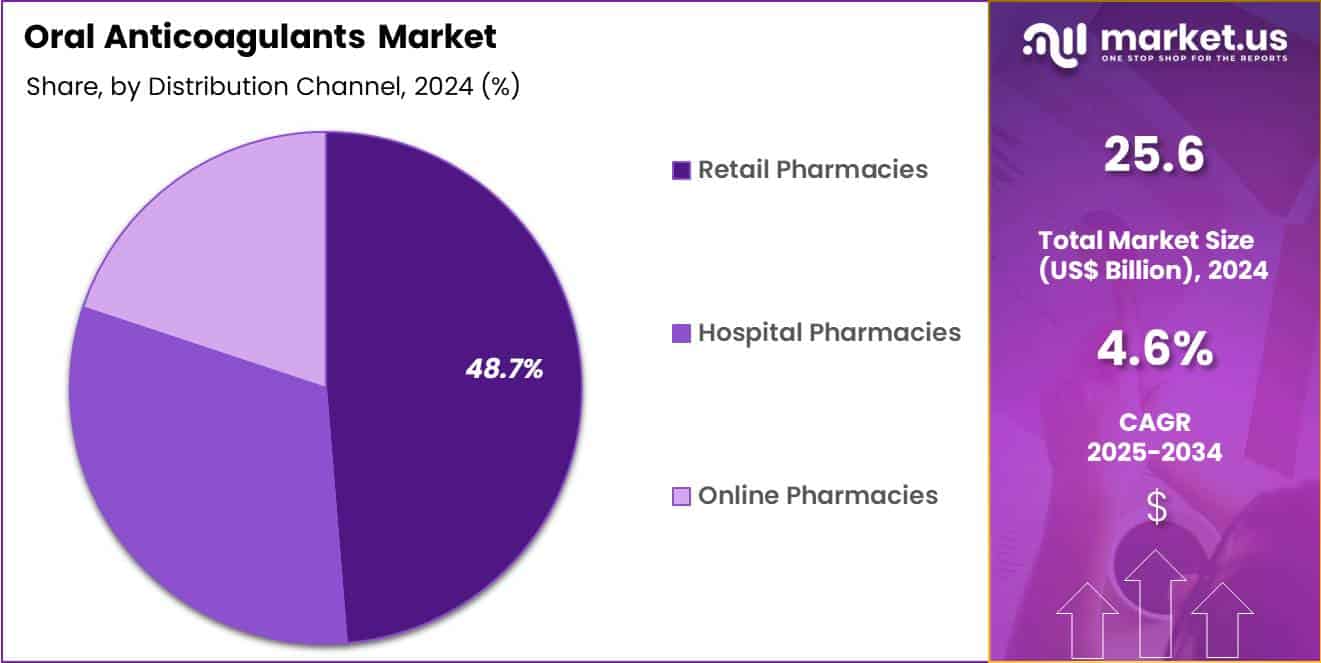

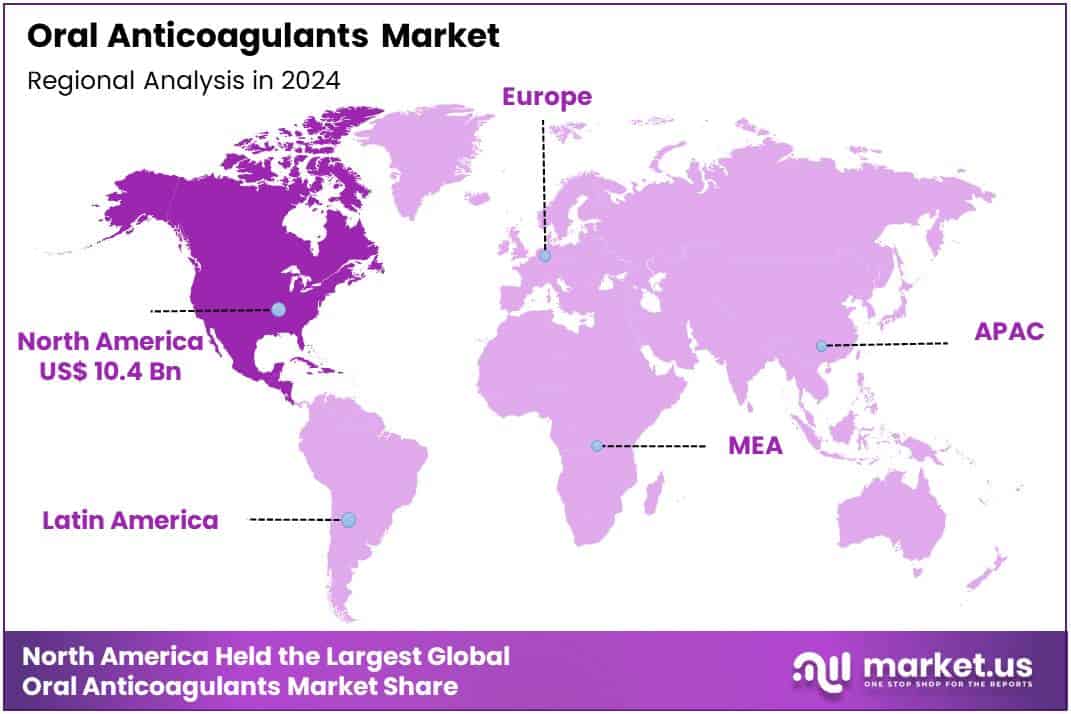

Global Oral Anticoagulants Market size is expected to be worth around US$ 40.1 Billion by 2034 from US$ 25.6 Billion in 2024, growing at a CAGR of 4.6% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 40.5% share with a revenue of US$ 10.4 Billion.

The oral anticoagulants sector shows that market expansion is being supported by strong clinical needs, demographic changes, and policy updates across global health systems. Oral anticoagulants are widely used to prevent harmful blood clots, particularly in conditions such as atrial fibrillation and venous thromboembolism, which includes deep vein thrombosis and pulmonary embolism. Their use has increased as the global burden of cardiovascular disease has risen.

According to the World Health Organization, cardiovascular diseases accounted for approximately one third of global deaths in 2022, with an estimated 19.8 million deaths. A significant share of these deaths resulted from heart attacks and strokes, conditions strongly linked to clot formation. This trend has encouraged health systems to strengthen prevention strategies, which has increased the use of oral anticoagulants across both developed and emerging markets.

Further growth is being driven by the high incidence of venous thromboembolism. Data from the U.S. Centers for Disease Control and Prevention indicate that up to 900,000 people in the United States develop venous thromboembolism annually, with 60,000 to 100,000 deaths each year. Similar patterns have been reported worldwide. The risk of venous thromboembolism increases sharply with age, reaching nearly 1 in 100 per year in older populations, compared with about 1 in 10,000 among younger adults. This demographic shift is also associated with higher rates of atrial fibrillation, further increasing long-term demand for anticoagulant therapy.

Growth is supported by evolving clinical guidelines, including the 2024 European Society of Cardiology recommendations, which prioritize oral anticoagulants for stroke prevention in high-risk atrial fibrillation patients. The adoption of direct oral anticoagulants, supported by their listing in the World Health Organization Model List of Essential Medicines, is improving access globally. Their predictable dosing, reduced monitoring needs, and favourable safety profile have strengthened clinician and payer confidence. Combined with better diagnosis, quality-of-care programs, and expanding public health initiatives, these factors are expected to support steady market growth in the years ahead.

Key Takeaways

- Market Size: Global Oral Anticoagulants Market size is expected to be worth around US$ 40.1 Billion by 2034 from US$ 25.6 Billion in 2024.

- Market Growth: The market growing at a CAGR of 4.6% during the forecast period from 2025 to 2034.

- Drug Class Analysis: In 2024, DOACs accounted for an estimated 58.1% of the global market, reflecting their strong clinical acceptance.

- Indication Anaysis: In 2024, Non-valvular Atrial Fibrillation (NVAF) accounted for an estimated 41.2% market share, representing the leading indication segment.

- Distribution Channel Analysis: Retail Pharmacies accounted for an estimated 48.7% market share, establishing this segment as the dominant distribution route.

- Regional Analysis: In 2024, North America led the market, achieving over 40.5% share with a revenue of US$ 10.4 Billion.

Drug Class Analysis

The oral anticoagulants market has been segmented by drug class into Direct Oral Anticoagulants (DOACs) and Vitamin K Antagonists (VKAs). Clear differentiation between these classes has shaped clinical adoption patterns and overall market dynamics.

In 2024, DOACs accounted for an estimated 58.1% of the global market, reflecting their strong clinical acceptance. This dominance can be attributed to predictable pharmacokinetics, reduced need for routine coagulation monitoring, and a lower risk profile for major bleeding events when compared with traditional therapies. Their expanding use in indications such as atrial fibrillation, venous thromboembolism, and prophylaxis in high-risk surgical procedures has further accelerated market penetration. The growth of the DOAC class has also been supported by favorable reimbursement frameworks and increasing physician preference for therapies with simplified dosing regimens.

In contrast, Vitamin K Antagonists continue to hold a smaller yet stable share of the market. Their use has been maintained in regions with cost-sensitive healthcare systems, as well as among patient populations requiring long-term therapy with proven historical outcomes. However, the need for frequent INR monitoring and the influence of dietary and drug interactions have limited broader uptake. Overall, the market has been shaped by a steady transition toward DOAC-based therapies.

Indication Anaysis

The oral anticoagulants market has been shaped by rising demand for effective prevention and management of thromboembolic disorders. In 2024, Non-valvular Atrial Fibrillation (NVAF) accounted for an estimated 41.2% market share, representing the leading indication segment. Its dominance can be attributed to the high global prevalence of atrial fibrillation and the increasing preference for novel oral anticoagulants that provide predictable anticoagulation and reduced monitoring requirements. The growing geriatric population has further supported expanded utilization in long-term stroke prevention.

The Deep Vein Thrombosis (DVT) segment has been supported by increasing diagnosis rates and the wider adoption of anticoagulant therapies in both acute and extended treatment settings. Pulmonary Embolism (PE) has represented another significant segment, driven by rising awareness of venous thromboembolism and improved clinical detection. Consistent guideline updates recommending direct oral anticoagulants have facilitated steady market uptake.

Post-orthopedic Surgery Thromboprophylaxis has continued to contribute to overall market growth due to established prophylactic use after hip and knee replacement procedures. The “Others” segment, which includes rare coagulation disorders and off-label uses, has demonstrated moderate expansion as clinical evidence broadens. Overall, demand across indications has remained positive, supported by clinical efficacy, safety advancements, and increasing global accessibility to novel agents.

Distribution Channel Analysis

The distribution landscape of the oral anticoagulants market has been defined by strong penetration across traditional and emerging channels. In 2024, Retail Pharmacies accounted for an estimated 48.7% market share, establishing this segment as the dominant distribution route. The prominence of retail outlets has been supported by widespread accessibility, consistent patient footfall, and the growing preference for convenient refills for chronic therapies such as oral anticoagulants. The trusted pharmacist–patient interaction has also encouraged adherence, contributing to sustained demand.

Hospital Pharmacies have represented the second major segment, driven by the high utilization of anticoagulants in inpatient settings, particularly for acute management of thromboembolic events. The increasing number of hospital admissions related to cardiovascular and orthopedic procedures has continued to support procurement volumes. The segment has benefited from structured treatment protocols and the availability of specialized clinical guidance.

Online Pharmacies have exhibited notable growth, propelled by the expansion of digital health platforms, rising consumer acceptance of e-prescriptions, and home-delivery convenience. Increased chronic disease management through telemedicine has further strengthened this channel. Overall, the distribution structure has remained balanced, with retail pharmacies maintaining leadership while hospital and online channels contribute to a broader, more accessible supply ecosystem.

Key Market Segments

By Drug Class

- Vitamin K Antagonists

- Direct Oral Anticoagulants

- Direct Thrombin Inhibitors

- Factor Xa Inhibitors

By Indication

- Non-valvular Atrial Fibrillation (NVAF)

- Deep Vein Thrombosis (DVT)

- Pulmonary Embolism (PE)

- Post-orthopedic Surgery Thromboprophylaxis

- Others

By Distribution Channel

- Retail Pharmacies

- Hospital Pharmacies

- Online Pharmacies

Driving Factors

The growth of the oral anticoagulant market is supported by a rising prevalence of thrombo-embolic and cardiovascular disorders. For example, Atrial Fibrillation (AF) is identified by the Centers for Disease Control and Prevention (CDC) as the most common arrhythmia, with cases rising as populations age.

Guideline bodies such as the American Society of Hematology (ASH) recommend the use of direct oral anticoagulants (DOACs) as first-line therapy for conditions such as acute deep vein thrombosis or pulmonary embolism, reflecting demand for newer oral agents. Increased access to healthcare and growing awareness of stroke and venous thromboembolism (VTE) prevention also drive market demand.

Trending Factors

Several key trends characterise the market for oral anticoagulants. First, there is a shift from traditional vitamin K antagonists (VKAs, e.g., warfarin) toward DOACs—owing to their more predictable pharmacokinetics, fewer monitoring requirements, and favourable guideline positioning. Second, guideline updates emphasise patient-centric therapy, including bleeding risk assessment tools and personalised anticoagulation duration.

Third, regulatory interest is rising in reversal agents, companion diagnostics and expansion of indications—for example in special populations such as cancer-associated VTE.

Restraining Factors

Market growth is tempered by several constraints. Bleeding risk remains a major concern with oral anticoagulants; DOACs, while advantageous, still carry a non-trivial risk of major bleeding, including gastrointestinal and intracranial haemorrhage.

Moreover, some agents face limitations in special patient groups (e.g., renal/hepatic impairment, mechanical prosthetic valves) and guideline exclusion criteria. Regulatory and reimbursement hurdles also present barriers, with strict oversight required for safety, dosing and monitoring protocols.

Opportunities

Several opportunities can be identified. The global geriatric population is expanding, raising the incidence of AF, VTE and other indications for oral anticoagulation this creates a sustained demand base.

Additionally, unmet needs persist in underserved regions and emerging markets where adoption of newer oral anticoagulants remains low; increased healthcare infrastructure and awareness in these regions represent growth potential.Finally, innovation in anticoagulant therapies such as novel mechanisms, improved safety profiles, tailored dosing, and digital monitoring presents opportunity for differentiation and market expansion.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 40.5% share and holds US$ 10.4 Billion market value for the year. The region gained this lead due to strong healthcare access, advanced treatment protocols, and rapid adoption of novel oral anticoagulants. The presence of large patient pools with cardiovascular disorders also supported demand. High awareness of stroke prevention therapies further strengthened market performance.

The market in North America expanded due to early access to innovative anticoagulant therapies. Growth was also supported by the rising incidence of atrial fibrillation and deep vein thrombosis. These conditions contributed to a steady need for long-term anticoagulation therapy. Improved diagnostic rates ensured that more patients received timely treatment. Strong reimbursement frameworks made advanced drugs more accessible. The availability of well-established distribution channels also improved adoption rates. Overall, sustained healthcare spending created favorable conditions for continuous market growth.

Europe observed steady demand for oral anticoagulants. The region’s aging population influenced long-term therapy use. Strong clinical guidelines encouraged physicians to switch from traditional therapies to newer, more predictable oral agents. National health systems supported consistent adoption. Regulatory approvals for improved formulations also heightened treatment penetration. Western Europe remained the leading sub-region, driven by robust healthcare infrastructure.

Asia-Pacific recorded rapid growth. Rising cardiovascular disease prevalence supported demand. Expanding healthcare coverage encouraged greater treatment uptake. Increased investments in hospital infrastructure improved market access. Urban populations showed higher awareness of chronic disease management. Demand in emerging economies grew due to larger untreated patient populations. Greater availability of generic versions also supported volume growth.

Latin America experienced moderate expansion. The burden of thrombotic disorders increased, creating gradual demand for oral anticoagulants. Improvements in healthcare access supported incremental growth. However, reimbursement gaps limited adoption in some countries. Economic fluctuations also influenced purchasing power. Despite these barriers, long-term opportunities remained positive.

Growth in the Middle East and Africa remained steady but slower. Higher adoption was observed in Gulf countries due to stronger healthcare systems. Stroke and clot-related complications increased across many nations. Limited specialist availability in low-income areas restricted widespread usage. However, expanding hospital networks supported gradual improvement in treatment access.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key participant activity in the oral anticoagulants market has been defined by sustained investment in therapeutic innovation and strategic portfolio expansion. Product pipelines have been strengthened through the development of advanced direct-acting agents, while lifecycle management strategies have enhanced competitiveness across major regions.

Market positioning has been supported by extensive clinical trial data demonstrating improved safety and efficacy profiles, which has facilitated strong adoption in atrial fibrillation and venous thromboembolism segments. Collaborations with research institutions and regional distributors have improved market penetration and clinical visibility. Continuous emphasis on patient-centric formulations, including once-daily dosing and reduced monitoring requirements, has reinforced differentiation.

Expansion into emerging economies has been enabled through pricing optimization and broader regulatory approvals. Overall, the market has been shaped by sustained R&D investments, diversified product strategies, and proactive regulatory engagement, which improved the competitive landscape and accelerated long-term market growth.

Market Key Players

- Pfizer Inc.

- Bristol Myers Squibb Company

- Bayer

- Johnson & Johnson

- Boehringer Ingelheim International GmbH

- Daiichi Sankyo Company, Limited

- Sanofi S.A.

- GSK plc

- AstraZeneca plc

- Teva Pharmaceutical Industries Ltd.

- Dr. Reddy’s Laboratories Ltd.

- Aspen Holdings

- Eisai Co., Ltd.

- Portola Pharmaceuticals, Inc.

Recent Developments

- Pfizer Inc. (Jul 2025): The Pfizer–Bristol Myers Squibb alliance announced a direct-to-patient option for their oral anticoagulant Eliquis (apixaban), enabling eligible U.S. patients to purchase it via discounted list-price shipping.

- Bristol Myers Squibb Company (Nov 2025): The Phase 3 “Librexia ACS” trial of the oral Factor XIa inhibitor milvexian (in collaboration with J&J) was terminated early due to low likelihood of meeting the primary endpoint.

- Bayer AG (Nov 2025): Bayer reported that sales of its oral anticoagulant Xarelto fell 31.4 % (fx & portfolio adjusted) in Q3 due to patent expirations.

- Johnson & Johnson (Nov 2025): In collaboration with BMS, J&J announced discontinuation of the milvexian ACS trial (Librexia), reflecting a strategic shift in its anticoagulants development.

Report Scope

Report Features Description Market Value (2024) US$ 25.6 Billion Forecast Revenue (2034) US$ 40.1 Billion CAGR (2025-2034) 4.6% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Drug Class(Vitamin K Antagonists, Direct Oral Anticoagulants) By Indication (Non-valvular Atrial Fibrillation (NVAF), Deep Vein Thrombosis (DVT), Pulmonary Embolism (PE), Post-orthopedic Surgery Thromboprophylaxis, Others) By Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies) Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Pfizer Inc., Bristol Myers Squibb Company, Bayer, Johnson & Johnson, Boehringer Ingelheim International GmbH, Daiichi Sankyo Company, Limited, Sanofi S.A., GSK plc, AstraZeneca plc, Teva Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Aspen Holdings, Eisai Co., Ltd., Portola Pharmaceuticals, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Pfizer Inc.

- Bristol Myers Squibb Company

- Bayer

- Johnson & Johnson

- Boehringer Ingelheim International GmbH

- Daiichi Sankyo Company, Limited

- Sanofi S.A.

- GSK plc

- AstraZeneca plc

- Teva Pharmaceutical Industries Ltd.

- Dr. Reddy’s Laboratories Ltd.

- Aspen Holdings

- Eisai Co., Ltd.

- Portola Pharmaceuticals, Inc.

Our Clients

- 166737

- Nov 2025