Global Optical Power Monitor Chip Market Size, Share, Growth Analysis By Product Type (Integrated Optical Power Monitor Chips, Discrete Optical Power Monitor Chips), By Application (Telecommunications, Data Centers, Industrial, Consumer Electronics, Medical Devices, Others), By Wavelength Range (850 nm, 1310 nm, 1550 nm, Others), By End-User (Network Equipment Manufacturers, Test and Measurement, Research and Development, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 182271

- Number of Pages: 239

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Core Key Insights

- Market Outlook

- Future Predictions

- Key Market Segments

- Research-Based Segments

- By Product Type

- By Application

- By Wavelength Range

- By End-User

- Regional Analysis

- US Market Size

- Driving Factors

- Restraint Factors

- Growth Opportunities

- Trending Factors

- Competitive Analysis

- Recent Developments

- Report Scope

Report Overview

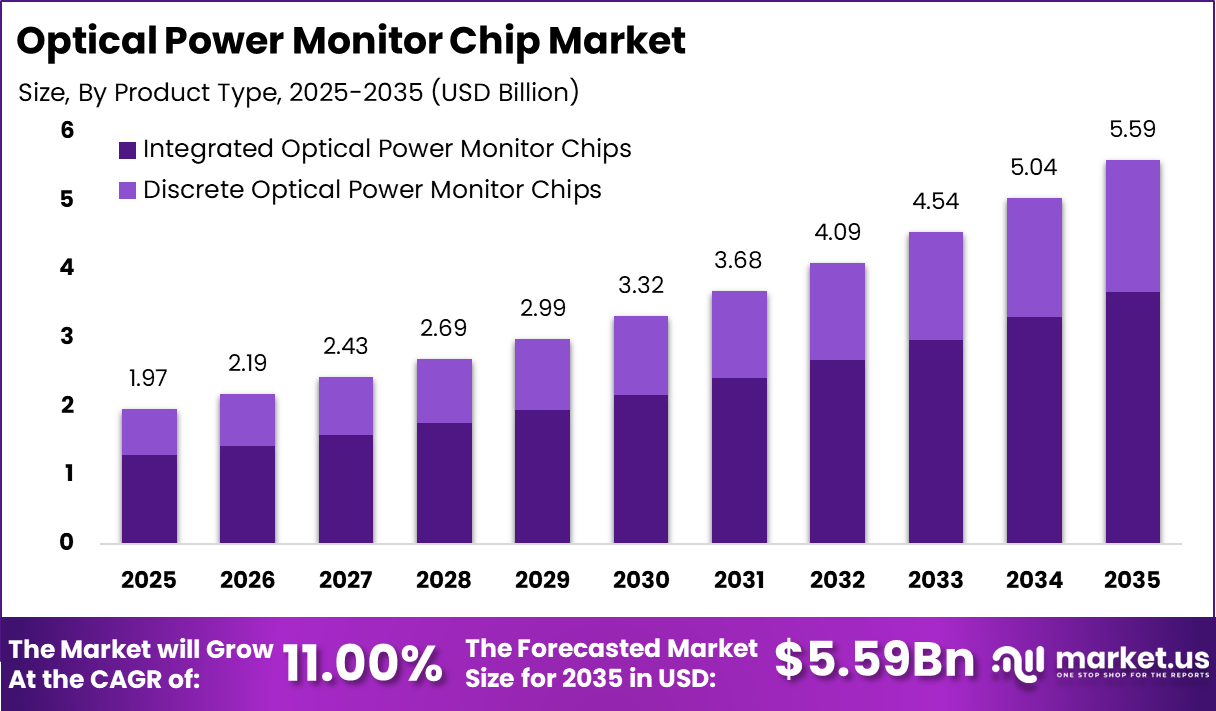

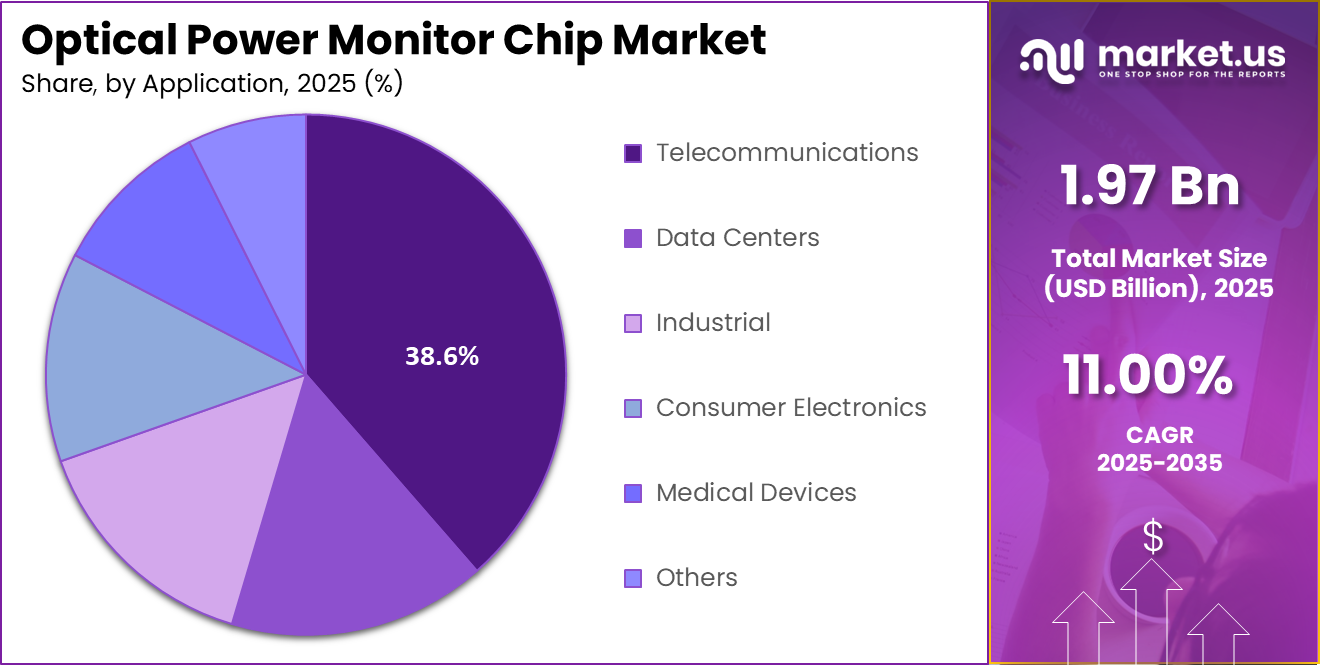

The Optical Power Monitor Chip Market is emerging as an important part of the broader optical components industry, supported by rising demand for reliable signal monitoring in fiber optic communication systems. The market was valued at USD 1.97 billion in 2025 and is anticipated to reach USD 5.59 billion by 2035, reflecting a CAGR of 11.0% over the forecast period.

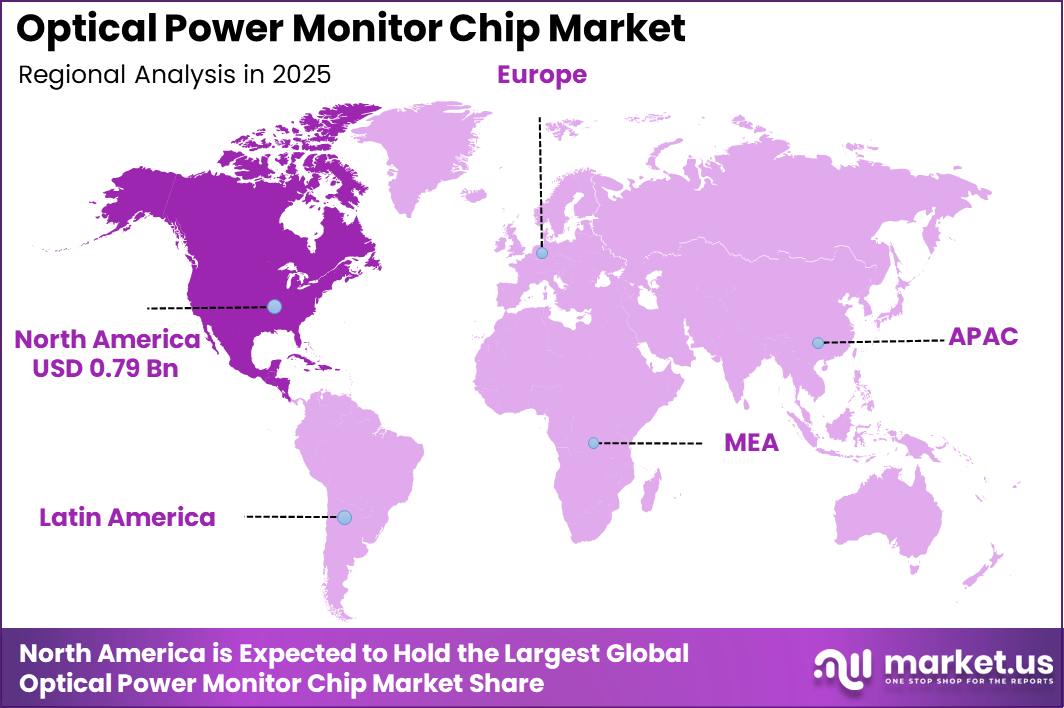

This growth indicates a healthy long term outlook, driven by increasing use of optical networks in telecom infrastructure, hyperscale data centers, and high-speed transmission systems. From a regional perspective, North America held a leading 40.5% share in 2025, equivalent to USD 0.79 billion. The region benefits from strong investment in data infrastructure, advanced semiconductor development, and early adoption of high-performance optical technologies.

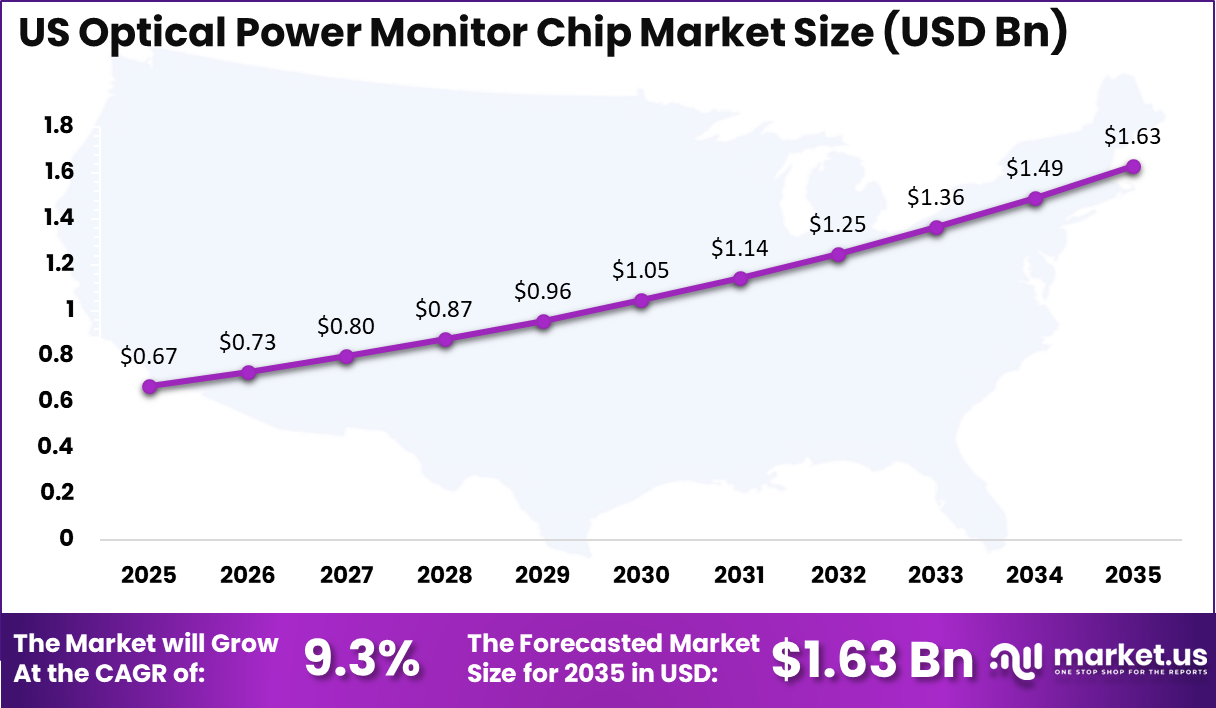

The US remains the key contributor within North America, with a market size estimated at USD 0.67 billion in 2025 and projected to reach USD 1.63 billion by 2035, at a CAGR of 9.3%. For clients, this market reflects strong potential in applications requiring precise optical signal control, system efficiency, and dependable performance across next-generation communication environments, especially as network operators and technology providers continue to expand optical capacity and improve transmission reliability.

For clients tracking the Optical Power Monitor Chip space, the strongest evidence comes from the underlying optical and broadband infrastructure numbers rather than headline market estimates. Globally, fixed broadband internet traffic is estimated at 6 zettabytes in 2024, up from 5.1 zettabytes in 2023, while mobile broadband traffic is expected to approach 1.3 zettabytes in 2024.

In parallel, active mobile broadband subscriptions worldwide reached 94.6 per 100 inhabitants in 2024, showing how quickly high-speed data networks are scaling. Across OECD countries, fixed broadband subscriptions reached 504 million by June 2024, and fibre accounted for 44.6% of all fixed broadband subscriptions.

In the US, the FCC reported 135 million fixed broadband connections as of December 31, 2024, including 38.6 million connections with downstream speeds of at least 940 Mbps. FCC data also show optical carrier connections at 25/3 Mbps reached 33.3 million in December 2024, up from 17.4 million in December 2020. These figures point to rising demand for accurate optical signal monitoring across faster and denser fibre networks.

Core Key Insights

- The Optical Power Monitor Chip Market reached USD 1.97 billion in 2025 and is projected to grow to USD 5.59 billion by 2035.

- The market is expected to expand at a CAGR of 11.0%, reflecting steady demand across optical communication and monitoring applications.

- North America held the leading regional position with a 40.5% share in 2025, reaching USD 0.79 billion.

- The US remained the largest country-level contributor, valued at USD 0.67 billion in 2025.

- The US market is anticipated to reach USD 1.63 billion by 2035, supported by a CAGR of 9.3%.

- By product type, integrated optical power monitor chips led the market with a 65.5% share due to their strong use in compact and efficient optical systems.

- By application, telecommunications accounted for 38.6% of the market, driven by rising fiber network deployment and signal monitoring needs.

- By wavelength range, 850 nm captured 40.5%, reflecting its wide use in short-distance optical communication.

- By end-user, network equipment manufacturers held 42.6%, showing strong demand from companies developing advanced networking hardware.

Market Outlook

The outlook for the optical power monitor chip market remains strongly linked to the rapid expansion of global optical communication infrastructure. Worldwide internet traffic continues to surge, with total IP traffic exceeding 5 zettabytes annually and expected to grow steadily as video streaming, cloud computing, and AI workloads expand.

Data centers alone are estimated to account for over 1% of global electricity consumption, reflecting the scale at which high-speed optical interconnects are being deployed. This directly increases the need for precise optical signal monitoring components within these systems.

Fibre deployment is also accelerating across regions. OECD data shows fibre connections now represent nearly 45% of fixed broadband subscriptions, while countries such as South Korea and Japan have already crossed 80% fibre penetration. In the US, more than 60 million homes are passed by fibre networks, with continuous expansion supported by federal broadband funding programs exceeding USD 40 billion.

Additionally, hyperscale data center capacity is growing, with over 900 facilities globally, each relying heavily on optical links. These trends highlight a strong and sustained demand for optical monitoring solutions, especially in high-density and high-performance network environments.

Future Predictions

The future of the optical power monitor chip market is expected to align closely with the expansion of high-speed optical networks and next-generation digital infrastructure. Global data consumption is projected to surpass 7 zettabytes annually before the end of the decade, driven by AI workloads, edge computing, and ultra-high definition streaming.

At the same time, more than 75% of global mobile traffic is expected to be carried over 5G networks, increasing reliance on dense fiber backhaul systems where precise optical monitoring becomes essential.

Fibre rollout is anticipated to deepen further, with global fibre to the home connections expected to exceed 1.5 billion by the early 2030s. In parallel, hyperscale data centers are projected to cross 1200 facilities worldwide, significantly increasing the need for efficient optical interconnects and monitoring solutions.

Governments are also expected to continue strong investments in digital infrastructure, with broadband funding programs across North America, Europe, and Asia collectively exceeding USD 100 billion. These developments indicate a sustained rise in demand for compact, high-accuracy optical monitoring chips, especially in environments requiring stable, high-capacity data transmission.

Key Market Segments

The Optical Power Monitor Chip Market is segmented across product type, application, wavelength range, and end-user, with each category reflecting specific demand patterns across optical communication systems.

By product type, integrated optical power monitor chips accounted for 65.5% of the market, driven by their compact design, improved accuracy, and ability to support high-density optical modules. These chips are widely adopted in modern photonic circuits where space efficiency and performance stability are critical.

By application, telecommunications held a 38.6% share, supported by the continuous expansion of fiber optic networks, rising data traffic, and increasing deployment of high-speed transmission systems. Optical monitoring plays a key role in maintaining signal strength and network reliability across long-distance communication infrastructure.

In terms of wavelength range, 850 nm accounted for 40.5%, reflecting its strong usage in short-range communication, such as data centers and enterprise networks, where cost efficiency and performance balance are important.

By end-user, network equipment manufacturers led with a 42.6% share, as they integrate optical monitoring components into switches, routers, and transmission systems. This dominance is linked to growing demand for advanced networking hardware capable of handling higher bandwidth and ensuring stable optical performance.

Research-Based Segments

By Product Type

- Integrated Optical Power Monitor Chips

- Discrete Optical Power Monitor Chips

By Application

- Telecommunications

- Data Centers

- Industrial

- Consumer Electronics

- Medical Devices

- Others

By Wavelength Range

- 850 nm

- 1310 nm

- 1550 nm

- Others

By End-User

- Network Equipment Manufacturers

- Test and Measurement

- Research and Development

- Others

By Product Type

65.5% of the market share was held by integrated optical power monitor chips, making them the dominant segment within the product type category. This dominance is due to their ability to combine monitoring functionality directly within optical modules, reducing system complexity and improving overall performance.

Integrated chips are widely used in compact photonic designs where space efficiency, low power consumption, and high accuracy are essential. Their compatibility with advanced optical transceivers and increasing use in high-speed data communication systems further support their strong market position.

Discrete optical power monitor chips continue to play an important role, especially in applications where flexibility and customization are required. These chips are typically used in systems that need external monitoring components or where integration is not feasible due to design constraints.

Discrete solutions offer ease of replacement and can be tailored for specific performance requirements, making them suitable for testing environments and legacy optical systems. However, as optical networks continue to shift toward miniaturization and integrated solutions, the preference for integrated optical power monitor chips is expected to remain strong across telecom, data center, and networking applications.

By Application

38.6% of the market share was held by telecommunications, making it the leading application segment in the Optical Power Monitor Chip Market. This dominance is driven by the continuous expansion of fiber optic networks and the rising need for stable, high-speed data transmission.

Optical power monitor chips are widely used in telecom infrastructure to maintain signal strength, detect losses, and ensure efficient network performance. Increasing deployment of 5G networks and long-haul communication systems is further supporting the demand for these monitoring solutions.

Data centers represent a significant and fast-growing segment, supported by the rapid rise in cloud computing, AI workloads, and high-capacity data storage. Optical monitoring is critical in maintaining reliable interconnects between servers and networking equipment. Industrial applications also contribute steadily, where optical systems are used in automation and sensing environments requiring precise signal control.

Consumer electronics and medical devices are emerging segments, where compact optical components are being integrated into advanced devices for improved performance and accuracy. The other segment includes research and specialized applications, where customized optical monitoring solutions are required for specific use cases.

By Wavelength Range

40.5% of the market share was held by the 850 nm wavelength range, making it the leading segment in the Optical Power Monitor Chip Market. This dominance is mainly due to its widespread use in short-range optical communication, particularly in data centers and enterprise networks. The 850 nm wavelength is commonly used with multimode fiber, offering cost-effective deployment and reliable performance for high-speed data transmission over shorter distances.

The 1310 nm and 1550 nm wavelength ranges are also important, especially in long-distance and high-capacity communication systems. The 1310 nm range is widely used in metro and access networks due to its lower dispersion, while 1550 nm is preferred for long-haul transmission because of its lower signal attenuation and compatibility with optical amplification technologies.

These wavelengths are critical in telecom backbone infrastructure, where maintaining signal quality over long distances is essential. The other segment includes specialized wavelength ranges used in niche applications such as sensing, research, and advanced photonic systems, where specific performance characteristics are required.

By End-User

42.6% of the market share was held by network equipment manufacturers, making them the leading end-user segment in the Optical Power Monitor Chip Market. This dominance is driven by the increasing production of routers, switches, and optical transmission systems that require precise monitoring of signal strength and stability.

These manufacturers integrate optical power monitor chips directly into networking hardware to ensure reliable performance, especially as data traffic continues to rise across telecom and data center environments. The test and measurement segment plays a crucial supporting role, as optical monitoring components are widely used in equipment designed to evaluate network performance, detect signal loss, and maintain system quality.

Research and development activities also contribute to market demand, particularly in photonics innovation, advanced communication systems, and next-generation optical technologies. The other segment includes specialized industries and niche applications where optical monitoring is required for customized systems, including defense, aerospace, and academic research setups.

Regional Analysis

40.5% of the global market share was held by North America in 2025, with a regional value of USD 0.79 billion, making it the leading region in the Optical Power Monitor Chip Market. This dominance is supported by strong deployment of fiber optic infrastructure, high adoption of advanced networking technologies, and the presence of a well-established semiconductor and photonics ecosystem.

The region continues to benefit from increasing data consumption, expansion of cloud services, and ongoing upgrades in telecom networks. The US plays a central role in driving regional growth, supported by large-scale investments in broadband expansion and data center infrastructure. Federal and private sector initiatives aimed at improving high-speed connectivity are accelerating fiber deployment across urban and rural areas.

In addition, the growing number of hyperscale data centers and rising demand for high-performance computing are increasing the need for efficient optical monitoring solutions. Canada also contributes steadily, with continued focus on digital infrastructure development and network modernization.

Overall, North America is expected to maintain its leadership position due to its early adoption of advanced technologies, strong investment environment, and continuous demand for reliable and high-speed optical communication systems.

US Market Size

The US Optical Power Monitor Chip Market was valued at USD 0.67 billion in 2025 and is projected to reach USD 1.63 billion by 2035, registering a CAGR of 9.3% over the forecast period. This growth reflects the country’s strong demand for advanced optical components and its leadership in high-speed communication infrastructure.

The US continues to see rising deployment of fiber optic networks across both urban and rural areas, supported by large-scale broadband expansion initiatives. Increasing demand for cloud computing, artificial intelligence workloads, and high-capacity data centers is driving the need for precise optical signal monitoring.

Optical power monitor chips are widely used in networking equipment to maintain signal quality and ensure system efficiency. In addition, the expansion of 5G networks and edge computing infrastructure is further increasing reliance on optical technologies.

The presence of a strong semiconductor ecosystem and continuous innovation in photonics are also contributing to market growth. As digital infrastructure continues to evolve, the demand for reliable and high-performance optical monitoring solutions is expected to remain strong across telecom, enterprise, and data center applications in the US.

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driving Factors

The growth of the optical power monitor chip market is strongly influenced by the rapid increase in global data consumption and the expansion of high-speed communication networks. With rising demand for video streaming, cloud computing, and AI-driven applications, telecom operators and data center providers are investing heavily in fiber optic infrastructure.

Optical power monitor chips play a critical role in maintaining signal quality, detecting power fluctuations, and ensuring stable transmission across these networks. The increasing deployment of 5G technology is further accelerating the need for efficient optical backhaul systems, where precise monitoring becomes essential.

In addition, hyperscale data centers are expanding globally, requiring high-density optical interconnects that depend on accurate signal control. The push for network reliability and performance optimization is encouraging equipment manufacturers to integrate advanced monitoring components within their systems.

Furthermore, the shift toward automated network management and real-time performance tracking is increasing the adoption of optical monitoring solutions. These factors collectively support consistent demand for optical power monitor chips across telecom, enterprise, and data infrastructure environments.

Restraint Factors

The optical power monitor chip market faces certain challenges that can limit its growth potential. One of the primary restraints is the complexity associated with integrating optical components into compact and high-performance systems. Designing chips that can deliver precise measurements while maintaining low power consumption requires advanced engineering capabilities and increases production costs.

This can create barriers for smaller manufacturers or new entrants. Additionally, the cost of high-quality materials and specialized fabrication processes can impact overall pricing, making it difficult for some end users to adopt these solutions at scale. Compatibility with existing infrastructure is another concern, especially in legacy systems that may not support advanced integrated components.

There are also challenges related to calibration and accuracy, as optical monitoring requires consistent performance across varying environmental conditions. Any deviation in measurement can affect network reliability. Moreover, supply chain disruptions in semiconductor manufacturing can lead to delays in production and availability, further impacting market growth and adoption rates.

Growth Opportunities

The market presents strong growth opportunities driven by the continuous expansion of digital infrastructure and emerging technologies. One of the key opportunities lies in the rapid development of hyperscale data centers, which require advanced optical interconnects to handle increasing workloads.

As cloud computing, artificial intelligence, and edge computing continue to grow, the demand for reliable optical monitoring solutions is expected to rise. Another significant opportunity is the expansion of fiber to the home and broadband connectivity initiatives across both developed and developing regions.

Governments are investing in improving digital access, which supports the deployment of optical networks and related components. The automotive and industrial sectors also offer potential opportunities, particularly with the adoption of optical communication in autonomous systems and smart manufacturing environments.

In addition, advancements in photonic integration are enabling more compact and efficient chip designs, opening new possibilities for product innovation. Companies focusing on energy-efficient and scalable solutions are likely to gain a competitive advantage in this evolving market landscape.

Trending Factors

The optical power monitor chip market is witnessing several important trends that are shaping its future direction. One of the most notable trends is the increasing adoption of integrated photonic solutions, where multiple optical functions are combined within a single chip. This approach helps reduce system size, improve performance, and lower overall costs.

Another key trend is the growing focus on energy efficiency, as data centers and telecom networks aim to reduce power consumption while maintaining high performance. There is also a shift toward high-density optical modules, which require precise monitoring to ensure stable operation in compact environments.

The use of automation and intelligent network management systems is becoming more common, driving the need for real-time optical monitoring capabilities. In addition, the rise of silicon photonics is influencing chip design and manufacturing processes, enabling higher levels of integration and scalability. These trends indicate a clear movement toward more advanced, efficient, and intelligent optical monitoring solutions across modern communication systems.

Competitive Analysis

The competitive landscape of the Optical Power Monitor Chip Market is moderately consolidated, with a mix of established semiconductor companies and emerging photonics innovators shaping the industry. Key players are primarily focused on developing integrated photonic solutions that offer higher accuracy, lower power consumption, and better compatibility with high-speed optical systems.

Companies such as Intel Corporation, Cisco Systems, MACOM, Lumentum, Coherent, and STMicroelectronics are actively involved in silicon photonics and optical component development, strengthening their position through vertical integration and advanced chip design capabilities.

Competition in the market is largely driven by innovation, performance efficiency, and the ability to support next-generation applications such as AI-driven data centers and high-capacity telecom networks. Many companies are investing in research to enhance chip sensitivity, reduce signal loss, and enable seamless integration into compact optical modules.

Strategic collaborations, acquisitions, and investments are also shaping the competitive environment, as firms aim to expand their technological capabilities and production capacity. Emerging startups and photonics-focused ecosystems are introducing new solutions, increasing competitive intensity, and pushing established players to accelerate innovation. Overall, the market is expected to witness continuous technological advancement, with competition centered on delivering reliable, scalable, and high-performance optical monitoring solutions.

Top Key Players in the Market

- Analog Devices Inc.

- Texas Instruments Inc.

- Maxim Integrated (now part of Analog Devices)

- Broadcom Inc.

- Hamamatsu Photonics K.K.

- Keysight Technologies

- Finisar Corporation (now part of II-VI Incorporated)

- Thorlabs, Inc.

- Yokogawa Electric Corporation

- EXFO Inc.

- Viavi Solutions Inc.

- Newport Corporation (part of MKS Instruments)

- Opto Diode Corporation

- Ophir Optronics Solutions Ltd. (part of MKS Instruments)

- Santec Corporation

- NeoPhotonics Corporation

- Lumentum Holdings Inc.

- Anritsu Corporation

- OZ Optics Limited

- Shenzhen Kexin Communication Technologies Co., Ltd.

- Others

Recent Developments

- In 2024, global fiber optic cable deployment continued to expand rapidly, with annual installations exceeding 500 million fiber kilometers, reflecting strong growth in broadband and telecom infrastructure worldwide.

- In 2025, hyperscale data center capacity surpassed 900 operational facilities globally, driven by increasing demand for cloud computing, artificial intelligence, and high-speed data processing.

- In 2024, global 5G subscriptions crossed 1.9 billion, highlighting the growing need for high-capacity optical backhaul networks and advanced signal monitoring technologies.

Report Scope

Report Features Description Market Value (2025) USD 4.67 Billion Forecast Revenue (2035) USD 14.90 Billion CAGR(2025-2035) 12.30% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics, and Emerging Trends Segments Covered By Product Type (Integrated Optical Power Monitor Chips, Discrete Optical Power Monitor Chips), By Application (Telecommunications, Data Centers, Industrial, Consumer Electronics, Medical Devices, Others), By Wavelength Range (850 nm, 1310 nm, 1550 nm, Others), By End-User (Network Equipment Manufacturers, Test and Measurement, Research and Development, Others), Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Analog Devices Inc., Texas Instruments Inc., Maxim Integrated (now part of Analog Devices), Broadcom Inc., Hamamatsu Photonics K.K., Keysight Technologies, Finisar Corporation (now part of II-VI Incorporated), Thorlabs, Inc., Yokogawa Electric Corporation, EXFO Inc., Viavi Solutions Inc., Newport Corporation (part of MKS Instruments), Opto Diode Corporation, Ophir Optronics Solutions Ltd. (part of MKS Instruments), Santec Corporation, NeoPhotonics Corporation, Lumentum Holdings Inc., Anritsu Corporation, OZ Optics Limited, Shenzhen Kexin Communication Technologies Co., Ltd., Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Optical Power Monitor Chip MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Optical Power Monitor Chip MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Analog Devices Inc.

- Texas Instruments Inc.

- Maxim Integrated (now part of Analog Devices)

- Broadcom Inc.

- Hamamatsu Photonics K.K.

- Keysight Technologies

- Finisar Corporation (now part of II-VI Incorporated)

- Thorlabs, Inc.

- Yokogawa Electric Corporation

- EXFO Inc.

- Viavi Solutions Inc.

- Newport Corporation (part of MKS Instruments)

- Opto Diode Corporation

- Ophir Optronics Solutions Ltd. (part of MKS Instruments)

- Santec Corporation

- NeoPhotonics Corporation

- Lumentum Holdings Inc.

- Anritsu Corporation

- OZ Optics Limited

- Shenzhen Kexin Communication Technologies Co., Ltd.

- Others

Our Clients

- 182271

- Mar 2026