Quick Navigation

Report Overview

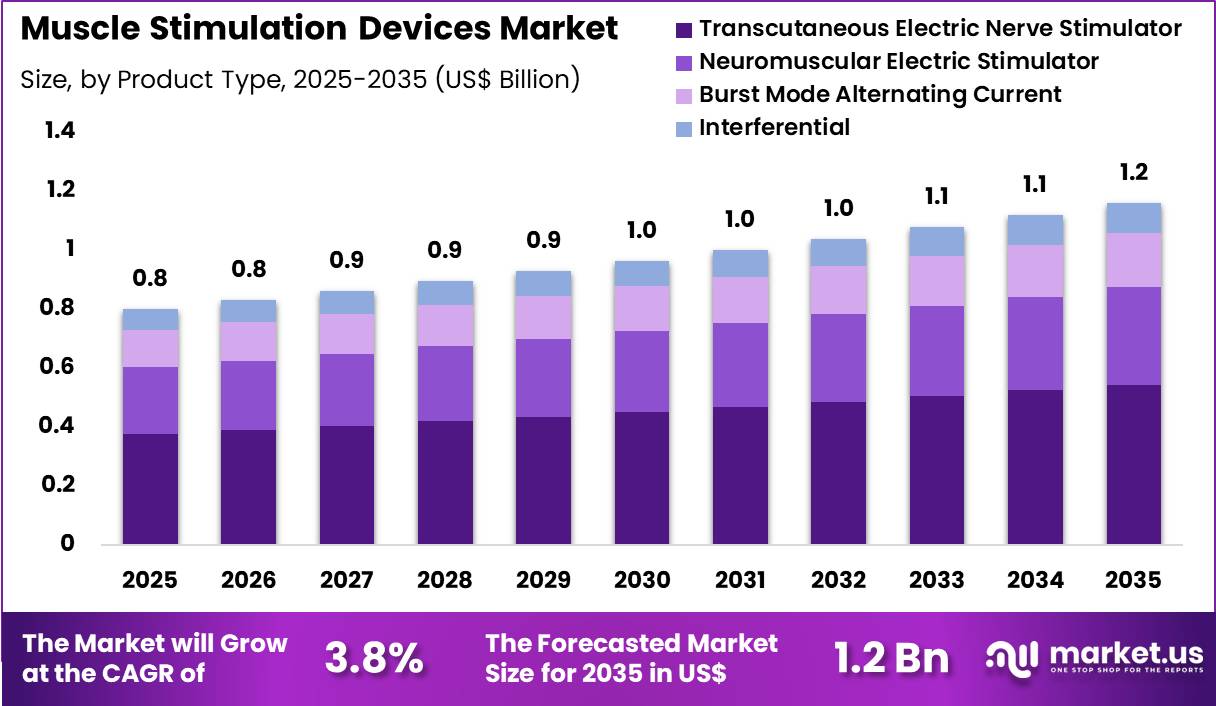

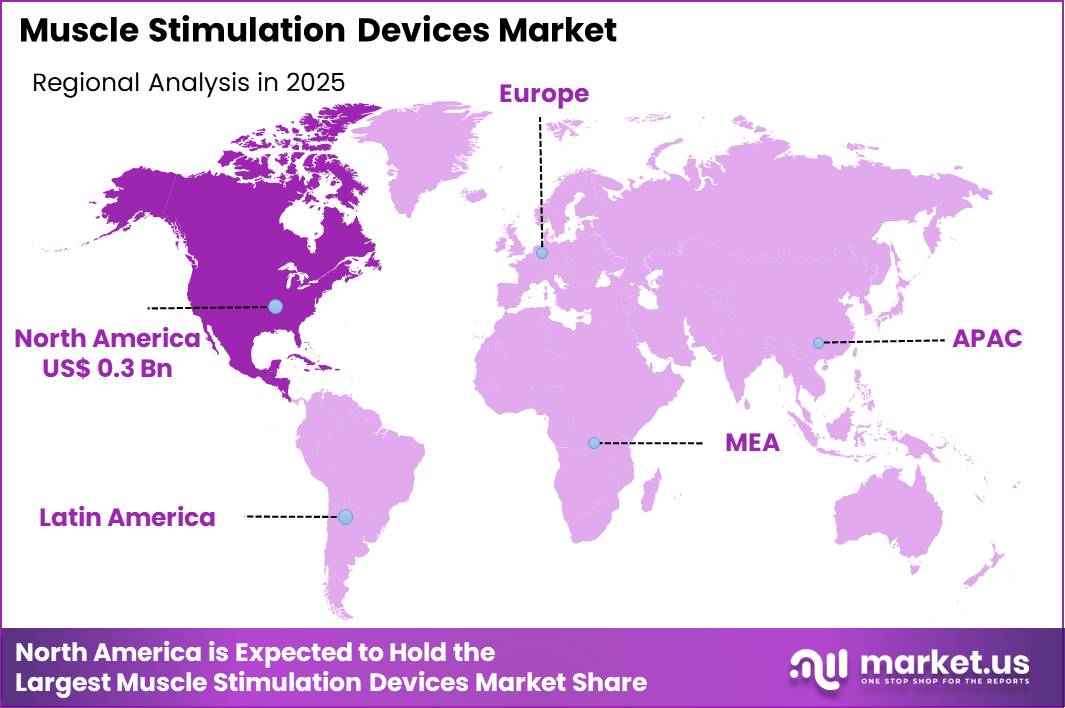

The Global Muscle Stimulation Devices Market size is expected to be worth around US$ 1.2 Billion by 2035 from US$ 0.8 Billion in 2025, growing at a CAGR of 3.8% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 38.8% share with a revenue of US$ 0.3 Billion.

Increasing prevalence of musculoskeletal disorders and sports-related injuries drives the muscle stimulation devices market as healthcare providers and consumers seek non-invasive solutions that promote recovery and enhance muscle function. Physiotherapists increasingly apply transcutaneous electrical nerve stimulation units to alleviate chronic pain in conditions like arthritis and fibromyalgia, delivering targeted pulses that block pain signals and improve joint mobility.

These devices support post-surgical rehabilitation by using neuromuscular electrical stimulation to prevent atrophy in immobilized limbs, facilitating earlier strength regain after knee or shoulder repairs. Athletes utilize functional electrical stimulation during training regimens to optimize muscle activation and endurance, reducing injury risk in high-impact sports.

Neurologists employ these tools in stroke recovery programs, stimulating affected muscles to restore motor control and coordination through repetitive patterned activation. Cosmetic applications involve electrical muscle stimulation for body contouring, where devices tone abdominal and gluteal muscles by inducing contractions equivalent to intense workouts.

Manufacturers pursue opportunities to integrate wearable technology and mobile apps that allow personalized stimulation protocols, expanding applications in home-based therapy for elderly patients managing age-related sarcopenia.

Developers advance biofeedback-enabled devices that adjust intensity based on real-time muscle response, broadening utility in occupational therapy for repetitive strain injuries. These innovations facilitate hybrid systems combining stimulation with virtual reality for engaging rehabilitation exercises. Opportunities emerge in sustainable, battery-efficient designs that support prolonged use without frequent recharging.

Companies invest in clinical validation for novel indications like peripheral neuropathy management. Recent trends emphasize AI-driven adaptive algorithms and connectivity for remote clinician oversight, positioning the market for growth in patient-centered, technology-enhanced muscle health solutions.

Key Takeaways

- In 2025, the market generated a revenue of US$ 0.8 Billion, with a CAGR of 3.8%, and is expected to reach US$ 1.2 Billion by the year 2035.

- The product type segment is divided into transcutaneous electric nerve stimulator, neuromuscular electric stimulator, burst mode alternating current and interferential, with transcutaneous electric nerve stimulator taking the lead with a market share of 46.8%.

- Considering application, the market is divided into pain management, musculoskeletal disorder management and neurological & movement disorder management. Among these, pain management held a significant share of 49.3%.

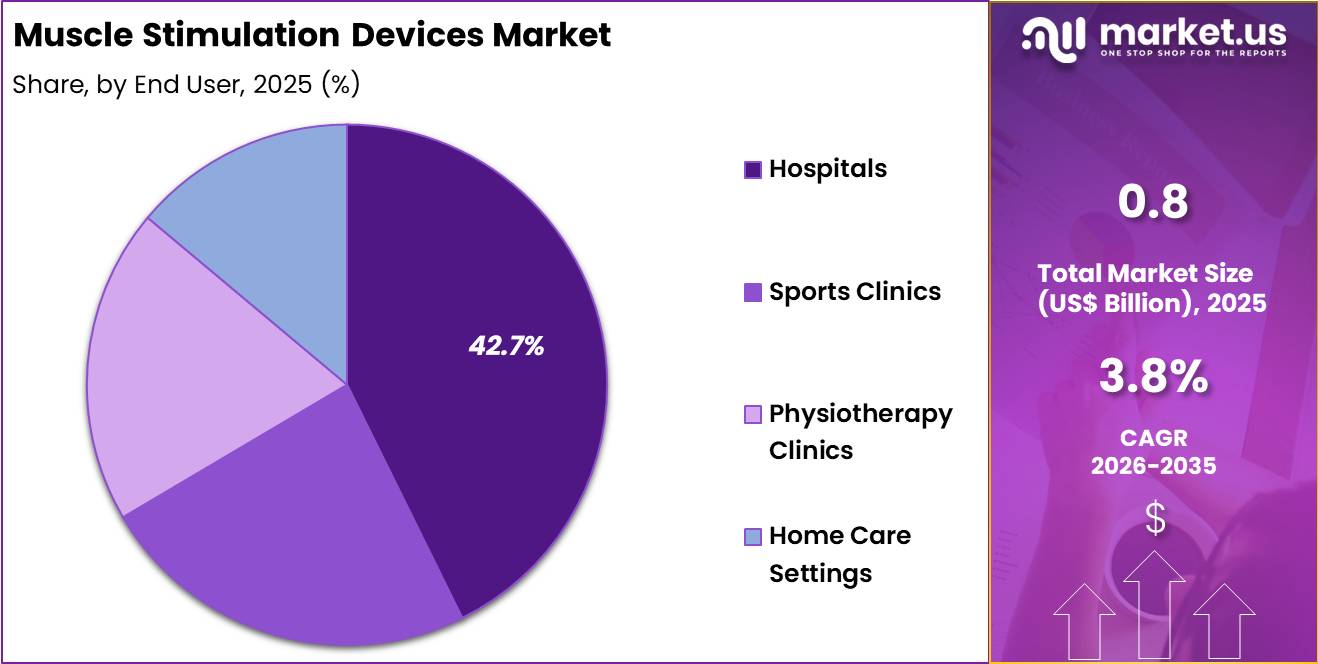

- Furthermore, concerning the end user segment, the market is segregated into hospitals, sports clinics, physiotherapy clinics and home care settings. The hospitals sector stands out as the dominant player, holding the largest revenue share of 42.7% in the market.

- North America led the market by securing a market share of 38.8%.

Product Type Analysis

Transcutaneous electric nerve stimulators accounted for 46.8% of growth within product type and dominate due to their effectiveness, ease of use, and portability. Hospitals and physiotherapy clinics favor these devices for non-invasive pain relief and muscle rehabilitation.

Segment growth is projected to strengthen as increasing incidence of chronic pain and musculoskeletal disorders drives demand for safe, drug-free therapies. Advancements in electrode technology, waveform customization, and wearable designs enhance treatment outcomes. Rising adoption in home care settings for patient-managed therapy supports market expansion.

Manufacturers focus on cost-effective and compact systems, improving accessibility in smaller clinics. The segment is anticipated to benefit from growing awareness among clinicians, insurance reimbursement policies, and integration into multimodal pain management programs.

Application Analysis

Pain management accounted for 49.3% of growth within applications and remains the leading driver of the market. Increasing prevalence of chronic pain conditions, including back pain, arthritis, and post-surgical pain, fuels device adoption. Hospitals implement pain management programs that incorporate muscle stimulation therapies for immediate symptom relief and improved patient mobility.

Segment growth is expected to continue as technological innovations, such as smart control systems and wireless connectivity, enhance precision and patient compliance. Rising patient preference for non-pharmacological interventions strengthens adoption.

Healthcare providers increasingly combine muscle stimulation devices with physiotherapy and rehabilitation programs to optimize outcomes. Insurance coverage and clinical guideline recommendations further encourage widespread use.

End-User Analysis

Hospitals accounted for 42.7% of growth within end users and dominate due to high patient volumes, multidisciplinary care teams, and access to specialized rehabilitation services. Hospitals integrate muscle stimulation devices into post-operative care, pain management, and neuromuscular rehabilitation protocols.

Segment growth is projected to continue as hospitals expand rehabilitation departments, adopt advanced therapy devices, and emphasize patient-centric care. Collaborations with manufacturers for training, device maintenance, and clinical support strengthen adoption.

Rising awareness of non-invasive therapies and government initiatives to improve chronic pain management further drive hospital-based usage. The segment benefits from both inpatient and outpatient care programs, supporting consistent market growth.

Key Market Segments

By Product Type

- Transcutaneous Electric Nerve Stimulator (TENS)

- Neuromuscular Electric Stimulator (NMES)

- Burst Mode Alternating Current (BMAC)

- Interferential (IF)

By Application

- Pain Management

- Musculoskeletal Disorder Management

- Neurological & Movement Disorder Management

By End‑user

- Hospitals

- Sports Clinics

- Physiotherapy Clinics

- Home Care Settings

Drivers

Increasing prevalence of musculoskeletal disorders is driving the market.

The escalating incidence of musculoskeletal disorders, such as arthritis and back pain, has substantially increased the demand for muscle stimulation devices to provide non-invasive pain relief and rehabilitation support. Greater clinical recognition and patient self-reporting have contributed to higher utilization rates of these devices in physical therapy settings.

Healthcare providers are increasingly prescribing muscle stimulation for chronic pain management in outpatient clinics. The correlation between sedentary lifestyles and muscular imbalances further amplifies the need for therapeutic stimulation solutions. Government health surveys document this rise as a major contributor to disability, prompting broader adoption.

Muscle stimulation devices offer targeted electrical impulses to strengthen muscles and reduce inflammation. National musculoskeletal health programs emphasize conservative treatments to avoid opioid dependence.

Key manufacturers are expanding product lines to address this clinical imperative. This driver fosters innovation in portable and wearable stimulation technologies. The increasing prevalence of musculoskeletal disorders is a major driver for the muscle stimulation devices market.

Restraints

High cost of advanced muscle stimulation devices is restraining the market.

The premium pricing of sophisticated muscle stimulation systems with multi-channel and programmable features limits their accessibility in home care and smaller therapy centers. Complex electronics and battery systems contribute to elevated manufacturing expenses passed on to consumers.

Patients often opt for basic over-the-counter devices due to budget constraints. Regulatory compliance for electrical safety adds to the overall cost structure for suppliers. In public health systems, allocation priorities favor low-cost alternatives over high-end stimulation equipment.

Providers must balance therapeutic benefits against economic viability when recommending these devices. This restraint impacts scalability, particularly in developing economies with limited reimbursement. Industry efforts to introduce affordable variants aim to alleviate these pressures partially. Despite clinical efficacy, the cost factor hinders universal implementation. The high cost of muscle stimulation devices is a major restraint in the market.

Opportunities

Growth in home-based rehabilitation programs is creating growth opportunities.

The expansion of home rehabilitation services for post-injury recovery presents avenues for muscle stimulation devices to penetrate consumer markets. Governmental policies supporting telemedicine encourage the distribution of portable stimulation units for remote therapy monitoring. Increasing patient preference for at-home treatment amplifies potential for user-friendly device solutions.

Partnerships with physical therapy networks facilitate customized device recommendations for home use. The large number of individuals recovering from surgeries or injuries at home magnifies prospects for stimulation applications. Educational resources for patients promote correct device usage in self-managed programs. This opportunity enables manufacturers to diversify beyond clinical settings.

Key corporations are developing app-controlled systems optimized for home rehabilitation. Overall, home-based growth aligns with efforts to reduce healthcare facility burden. Growth in home-based rehabilitation programs is a key market opportunity.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the muscle stimulation devices market as hospitals and clinics manage tighter budgets and prioritize essential equipment. Inflation and rising interest rates increase financing costs for portable and clinical-grade devices, which slows procurement and expansion.

Geopolitical tensions disrupt supply chains for electronic components and electrodes, adding delays and operational challenges. Current US tariffs on imported devices and key materials raise overall costs, which pressures smaller clinics and homecare providers. These factors create short-term adoption challenges and slow market penetration in cost-sensitive regions.

On the positive side, tariffs encourage domestic manufacturing, localized service networks, and partnerships with suppliers. Growing awareness of non-invasive therapies for pain and musculoskeletal recovery supports sustained demand. With strategic sourcing and patient-centered product offerings, the market remains on track for steady growth.

Latest Trends

Integration of smart features like app connectivity is a recent trend in the market.

In 2024, the incorporation of Bluetooth-enabled controls in muscle stimulation devices has advanced personalized therapy through smartphone app integration. These systems allow users to customize intensity and duration settings via mobile interfaces.

Manufacturers have emphasized data tracking for treatment progress monitoring. Clinical feedback in 2024 highlighted improved adherence with app-based reminders. Integration of smart features like app connectivity and customizable programs is a recent trend in the market. This development addresses limitations in traditional wired devices for home use.

The trend focuses on seamless synchronization with health tracking apps for comprehensive wellness data. Regulatory adaptations have supported approvals for connected features. Industry synergies concentrate on user-friendly software for diverse age groups. These evolutions aim to elevate patient engagement while maintaining therapeutic efficacy in stimulation protocols.

Regional Analysis

North America is leading the Muscle Stimulation Devices Market

North America accounted for 38.8% of the muscle stimulation devices market in 2024, as clinicians and patients increasingly adopted electrical stimulation technologies for rehabilitation, chronic pain management, and post‑injury recovery.

Usage of neuromuscular electrical stimulation grew as physiotherapy and sports medicine clinics reported a marked increase in therapy sessions incorporating these systems, with clinical utilization rising alongside the 41.86% share of transcutaneous electrical nerve stimulation devices in electrotherapy applications in 2024, reflecting broad therapeutic integration across pain relief and recovery settings.

Expansion of outpatient physical therapy services and home‑use programs encouraged healthcare providers to invest in both portable and clinical‑grade stimulators, improving continuity of care and patient outcomes. A rise in musculoskeletal conditions and age‑associated mobility issues among the region’s aging population further underlined demand.

Technology enhancements such as app‑enabled control and wearable form factors improved user experience and expanded adoption beyond traditional clinic environments. Reimbursement policies that increasingly recognize non‑pharmacological pain therapies lowered cost barriers for patients and insurers.

Integration of stimulation protocols into standard post‑surgical regimens helped reduce recovery times and readmission rates. Strong collaboration between device manufacturers and large healthcare systems streamlined distribution and training. These factors collectively propelled robust regional growth in 2024.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Across Asia Pacific, growth over the forecast period is expected as healthcare providers and consumers embrace electrical stimulation solutions to support rehabilitation, pain management, fitness recovery, and wellness therapies.

Rising prevalence of musculoskeletal disorders in the region was underscored by health statistics showing that musculoskeletal conditions affect more than 1.2 billion people across Asia Pacific in 2023, highlighting substantial unmet needs in both clinical and community settings. Rapid expansion of outpatient physiotherapy clinics, sports medicine facilities, and home‑care services is expanding access to therapeutic technologies that complement traditional care.

Governments are increasing healthcare funding and integrating non‑invasive therapies into public health initiatives to address chronic pain and mobility impairment. Larger middle‑class populations and higher healthcare spending are driving consumer interest in at‑home stimulation units that support recovery and fitness goals.

Local manufacturers and distributors are tailoring products to price‑sensitive markets, improving affordability and availability outside major cities. Cross‑border collaborations are building clinical expertise and knowledge sharing, boosting confidence among practitioners.

Rising sports participation and rehabilitation demand among younger cohorts also contribute to adoption. Collectively, these dynamics point to accelerating expansion of stimulation technology usage throughout Asia Pacific during the forecast period.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Leading firms in the therapeutic electrical stimulation sector pursue growth by launching technologically advanced products, expanding distribution channels, and forming alliances with rehabilitation centers and sports clinics. They invest heavily in clinical studies to validate efficacy and enhance credibility among healthcare professionals.

Enovis Corporation, a key market participant, develops portable bone and muscle stimulation solutions and maintains a strong presence in North America and Europe. The company emphasizes innovation, integrating user-friendly interfaces and wearable designs to improve patient compliance.

Competitors also pursue targeted marketing campaigns and strategic acquisitions to broaden their portfolios. These strategies collectively strengthen market positioning and accelerate adoption across hospital, home care, and sports therapy settings.

Top Key Players

- Zynex Medical

- DJO Global

- Omron Healthcare

- Beurer

- NeuroMetrix

- RS Medical

- EMS Physio

- Chattanooga (Enovis)

- Compex (DJO)

- TensCare

Recent Developments

- In November 2025, Motive Health, Inc. released Motive Lower Back, an FDA-cleared home-use device that stimulates stabilizing muscles to correct weakness and imbalances, addressing core causes of lower back pain. The launch builds on the company’s prior FDA-cleared muscle stimulation solution for knee pain.

- In 2025, Enovis Corporation introduced the Manafuse Bone Growth Stimulator, a portable Low-Intensity Pulsed Ultrasound (LIPUS) device. Clinical studies show it accelerates acute fracture healing by 38%, providing a non-invasive option to support faster recovery for patients with difficult or slow-healing fractures.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 0.8 Billion |

| Forecast Revenue (2035) | US$ 1.2 Billion |

| CAGR (2026-2035) | 3.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Transcutaneous Electric Nerve Stimulator (TENS), Neuromuscular Electric Stimulator (NMES), Burst Mode Alternating Current (BMAC) and Interferential (IF)), By Application (Pain Management, Musculoskeletal Disorder Management and Neurological & Movement Disorder Management), By End user (Hospitals, Sports Clinics, Physiotherapy Clinics and Home Care Settings) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Zynex Medical, DJO Global, Omron Healthcare, Beurer, NeuroMetrix, RS Medical, EMS Physio, Chattanooga (Enovis), Compex (DJO), TensCare |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |