Global Lentein Plant Protein Market Size, Share, And Industry Analysis Report By Product Type (Powder, Liquid, Capsules), By Application (Food and Beverages, Nutritional Supplements, Animal Feed, Pharmaceuticals, Others), By Distribution Channel (Supermarkets and Hypermarkets, Online Stores, Specialty Stores, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: February 2026

- Report ID: 176711

- Number of Pages: 352

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

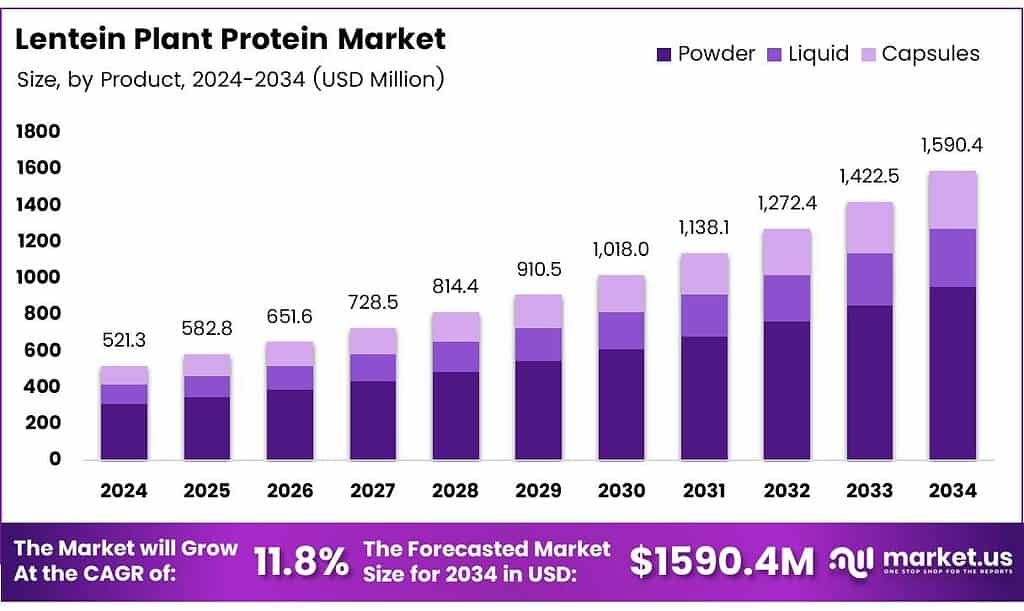

The Global Lentein Plant Protein Market size is expected to be worth around USD 1590.4 million by 2034, from USD 521.3 million in 2024, growing at a CAGR of 11.8% during the forecast period from 2025 to 2034.

The Lentein Plant Protein Market continues to gain recognition as consumers shift toward clean, sustainable, and nutrient-rich ingredients. Lentein, derived from water-grown lentils, supports efficiency and low environmental impact. This strengthens its position in beverages, snacks, and supplements as plant-based diets accelerate globally and brands seek high-quality protein alternatives with better functionality.

Moreover, growing demand for eco-efficient ingredients encourages food producers to adopt Lentein due to its rapid growth cycle and strong amino acid profile. As manufacturers reformulate products, they prioritize texture stability, digestibility, and mild taste. These requirements boost interest in Lentein across sports nutrition, fortified foods, and functional beverages, where protein enhancement is a major purchase driver.

- Lentils have been cultivated since 7000 BC, making them among the oldest agricultural staples. Nearly 75% of lentil production occurs in developing countries, demonstrating their agronomic resilience. Lentils are categorized into large Chilean seeds, averaging 50 g/1,000 seeds, and small Persian seeds, averaging 40 g/1,000 seeds, which influences raw-material selection strategies.

Lentil flour shows a bimodal particle distribution between 10–1000 μm, with a mean diameter of 356.85 μm and a span of 1.97. Extraction studies used Viscozyme L containing 100 FBG units/100 g, SDS-PAGE markers ranging 6–180 kDa, and sample preparation at a 1:10 ratio, pH 8–9, stirred 120 min at 25°C, then centrifuged at 10,000 × g for 20 min at 4°C before protein assessment.

Additionally, supportive government investments in sustainable agriculture and climate-resilient crops widen opportunities for emerging proteins. Regulatory frameworks that encourage low-carbon food systems help companies expand production capacity. This enables broader commercial use of Lentein-based ingredients, especially in markets seeking non-soy, non-pea, allergen-friendly protein sources with minimal processing and strong nutritional value.

Key Takeaways

- The Global Lentein Plant Protein Market is valued at USD 521.3 million in 2024 and is projected to reach USD 1590.4 million by 2034, at a CAGR of 11.8% from 2025 to 2034.

- Powder is the dominant product type, accounting for 67.3% of the total market share in 2025.

- Food and Beverages lead the application segment with a 58.1% share in 2025.

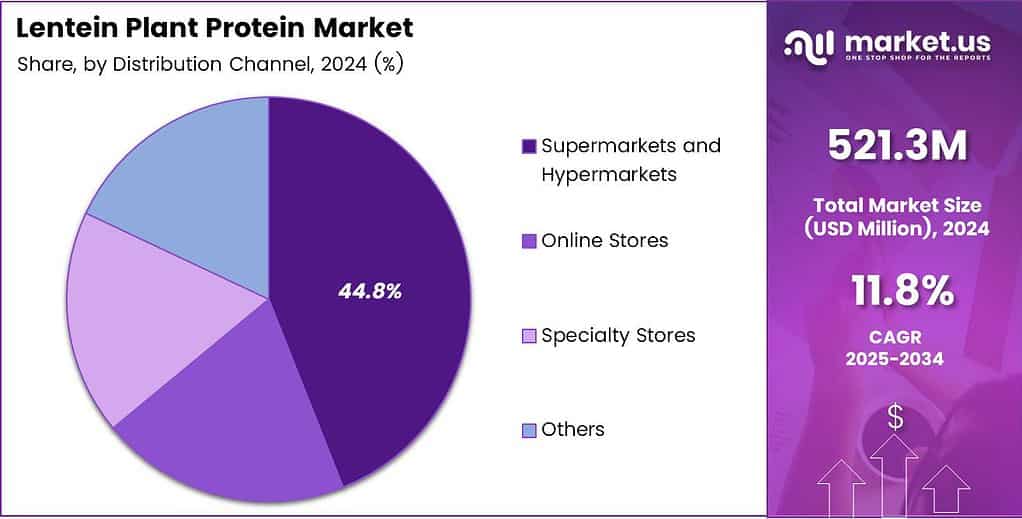

- Supermarkets and Hypermarkets dominate distribution with a 44.8% share in 2025.

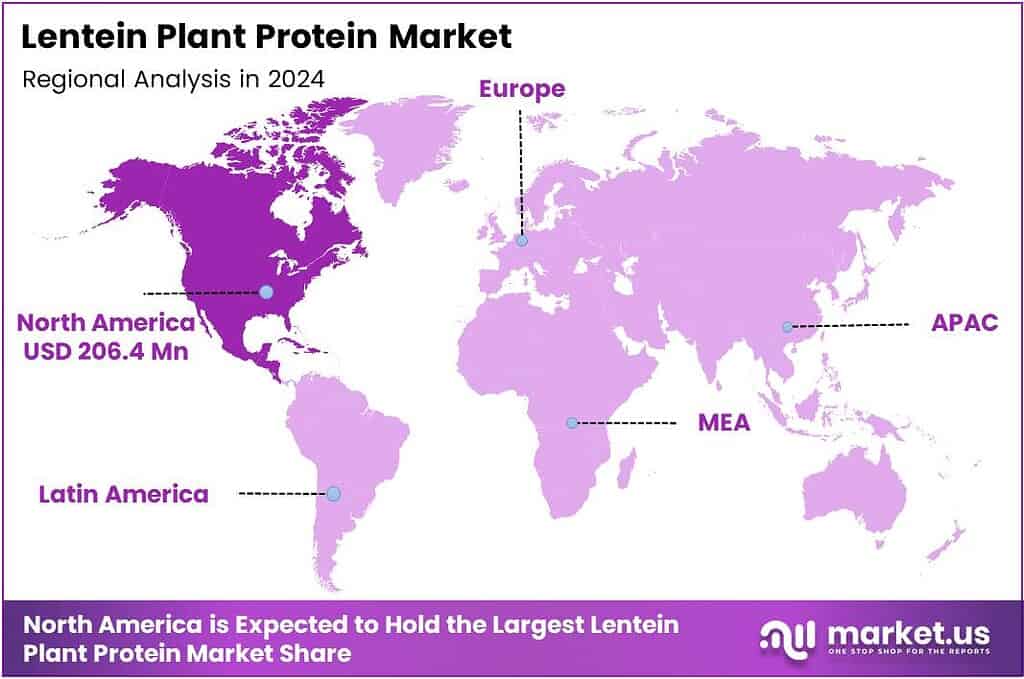

- North America is the leading regional market with a 39.6% share, valued at USD 206.4 million.

By Product Type Analysis

Powder dominates with 67.3% due to its strong commercial acceptance and versatile application range.

In 2025, Powder held a dominant market position in the By Product Type segment of the Lentein Plant Protein Market, with a 67.3% share. Powder forms gained traction because they blend easily into beverages, snacks, and supplements. Additionally, manufacturers prefer powder formats for long shelf life and efficient transport, strengthening market penetration.

Liquid formats continued expanding as brands introduced ready-to-drink protein beverages. These products attracted consumers seeking quick nutritional intake without preparation. Although liquid formats did not surpass the powder category, growing demand for convenience positioned this sub-segment for steady long-term development, supported by rising lifestyle-related nutritional needs across global markets.

Capsules experienced moderate adoption as consumers increasingly pursued precise dosage formats. Their ease of consumption encouraged use among individuals who prefer supplement-style protein intake. While capsules remain a niche compared to powders and liquids, their relevance grows in clinical nutrition and targeted health products, strengthening their role within specialized consumption patterns.

By Application Analysis

Food and Beverages dominate with 58.1% as clean-label protein innovation accelerates.

In 2025, Food and Beverages held a dominant market position in the By Application segment of the Lentein Plant Protein Market, with a 58.1% share. This segment grew as consumers increasingly chose plant-based alternatives for sustainability and health. Lentein’s nutrient density supported its use in snacks, bakery, beverages, and fortified meals.

Nutritional Supplements continued expanding as active consumers and athletes sought natural, high-quality protein sources. Lentein’s amino acid profile and digestibility positioned it as an appealing alternative to dairy-based supplements. Brands increasingly incorporated it into powders, capsules, and bars, strengthening market visibility and boosting functional nutrition adoption.

Animal Feed applications saw rising interest as producers sought sustainable protein alternatives to traditional feed components. Lentein’s rich nutrient composition supported improved feed efficiency, especially for aquaculture and poultry farming. Though smaller than other segments, its role continues growing as sustainability demands reshape animal nutrition strategies worldwide.

Pharmaceuticals and Others contributed incremental growth through specialized formulations, medical nutrition products, and research-driven innovations. Lentein’s bioavailability and nutrient density made it suitable for targeted therapeutic applications. These segments benefited from scientific exploration, supporting broader diversification across the global plant protein ecosystem.

By Distribution Channel Analysis

Supermarkets and Hypermarkets dominate with 44.8% due to high visibility and consumer accessibility.

In 2025, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the lentil plant protein market, with a 44.8% share. These outlets maintained strong consumer trust and convenience, offering extensive product variety. Their structured retail environment enhanced brand visibility and boosted impulse purchases across plant protein categories.

Online Stores expanded rapidly as digital shopping became mainstream. Consumers increasingly preferred online platforms for product comparison, discounts, and doorstep delivery. E-commerce growth enabled niche Lentein protein brands to reach wider audiences, promoting innovation and supporting direct-to-consumer business models across multiple regions.

Specialty Stores played a meaningful role by catering to health-conscious buyers seeking premium plant proteins. Their curated product offerings and knowledgeable staff enhanced customer experience. These outlets strengthened Lentein’s adoption among early adopters, athletes, and wellness-focused consumers, helping establish credibility within the broader nutritional marketplace.

Key Market Segments

By Product Type

- Powder

- Liquid

- Capsules

By Application

- Food and Beverages

- Nutritional Supplements

- Animal Feed

- Pharmaceuticals

- Others

By Distribution Channel

- Supermarkets and Hypermarkets

- Online Stores

- Specialty Stores

- Others

Emerging Trends

Rising Preference for Sustainable Protein Sources Drives Market Growth

One of the strongest trends shaping the Lentein plant protein market is the growing focus on regenerative and climate-positive foods. Water lentils grow rapidly with minimal environmental impact, making Lentein an attractive ingredient for eco-driven brands.

- Another trend is the rise of high-protein vegan products. Consumers want plant proteins that match animal protein in quality, and Lentein’s amino acid profile supports this shift. The LENTEIN technical white paper describes it as a free-flowing powder with at least 65% crude protein, which helps food formulators benchmark it against familiar plant proteins during R&D and scale-up.

Innovation in extraction and processing technologies is also trending, helping improve taste, texture, and cost efficiency. Companies are investing in advanced cultivation systems to scale production. These factors collectively push Lentein closer to mainstream adoption.

Drivers

Rising Preference for Sustainable Protein Sources Drives Market Growth

Growing consumer awareness about sustainable nutrition is a major driver for the Lentein plant protein market. Lentein, derived from water lentils, uses very little land and water, making it highly eco-friendly. This sustainability appeal encourages food manufacturers to use it in shakes, snacks, and functional foods.

- The rising shift toward clean-label and natural ingredients also supports its adoption. Consumers increasingly look for proteins that are GMO-free and allergen-friendly, and Lentein fits this demand. The U.S. Food and Drug Administration lists intended uses for Lemna (water-lentil) leaf protein across common categories such as baked goods, beverages, cereals, dressings, pasta, yogurts, smoothies, snacks, and “plant protein products,” with use levels up to 5.0% in several applications.

Additionally, Lentein offers a high protein concentration and essential amino acids, making it an attractive alternative to soy and pea protein. Its nutritional density positions it well in sports nutrition and wellness categories. These combined drivers create steady long-term demand.

Restraints

Rising Preference for Sustainable Protein Sources Drives Market Growth

Even with strong advantages, the Lentein plant protein market faces notable restraints. One major limitation is the low consumer awareness compared to more established plant proteins like soy or pea. This makes it harder for brands to include Lentein in mainstream products.

- Production scalability is another challenge. Growing and harvesting water lentils require controlled environments, which increases operational costs. The Good Food Institute reports the 2024 retail plant-based food market was worth $8.1 billion. Even with some categories cooling, that is still a large shelf footprint that keeps ingredient innovation moving.

Flavor and formulation challenges remain concerns for manufacturers. Although Lentein is nutrient-dense, it may have a stronger taste profile, requiring additional processing. These restraints collectively limit the market’s faster expansion despite its strong potential.

Growth Factors

Rising Preference for Sustainable Protein Sources Drives Market Growth

The Lentein plant protein market presents several growth opportunities as demand for sustainable foods accelerates worldwide. One of the biggest opportunities lies in expanding its use in sports nutrition, where consumers seek complete and highly digestible plant proteins.

- Another opportunity is the rising popularity of functional beverages. Lentein’s smooth texture and high micronutrient content make it suitable for fortified drinks, health shots, and ready-to-mix powders. The Plant-Based Foods Association marketplace report highlights plant-based protein powders and liquids reaching $450M, with +11% dollar growth and +13% unit growth in 2024.

Food manufacturers are also exploring Lentein in bakery, snacks, and dairy alternatives. Its sustainability credentials offer strong branding potential. Partnerships between ingredient producers and food companies can further boost product availability, opening new commercial pathways.

Regional Analysis

North America Dominates the Lentein Plant Protein Market with a Market Share of 39.6%, Valued at USD 206.4 Million

North America leads the global Lentein Plant Protein Market with a commanding 39.6% share, reaching a valuation of USD 206.4 million. The region benefits from strong consumer demand for sustainable, plant-based proteins and an accelerated shift toward environmentally friendly food sources. Growing awareness of the nutritional advantages of water-lentil protein also drives adoption across functional foods, beverages, and dietary supplements, positioning North America as the core growth hub.

Europe represents a mature and steadily expanding market driven by strict sustainability standards and high acceptance of alternative protein ingredients. The region shows increasing consumer preference for nutrient-rich, allergen-free plant proteins such as Lentein, supported by robust innovation across food and beverage applications. Strong governmental focus on reducing environmental impact and encouraging plant-based diets continues to fuel long-term demand across major European countries.

The Asia Pacific region is emerging as one of the fastest-growing markets due to rapid urbanisation, rising disposable incomes, and heightened interest in high-protein, plant-based food formats. Expanding vegan and flexitarian populations in countries such as India, China, and Australia contribute significantly to growing demand. Additionally, the region’s large-scale food manufacturing sector increasingly integrates Lentein into mainstream and fortified products, strengthening market penetration.

Latin America shows rising interest in Lentein plant protein due to increasing health awareness and a shift toward plant-based food consumption. Countries across the region are adopting more sustainable nutrition habits, contributing to steady market growth. Expanding food processing industries and demand for affordable, nutrient-dense ingredients further accelerate Lentein usage in regional product formulations.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Parabel USA Inc. stands out in 2025 for pushing water lentil (duckweed) protein as a clean, functional ingredient for beverages, bars, and ready-to-mix nutrition. Its edge is speed: shorter crop cycles and a sustainability story that brands can communicate easily. The near-term focus is likely on scaling supply reliability and tightening specs for taste, color, and solubility to win larger food-and-sports-nutrition accounts.

TerraVia Holdings, Inc. (known for algae-based ingredients) remains strategically relevant to lentil/plant-protein buyers because it competes for the same “high-protein + better-for-you” formulation space. In 2025, the practical value is in blending: algae-derived proteins and lipids can help texture, mouthfeel, and nutrition claims when paired with lentil protein. The key watch-out is cost positioning versus mainstream plant proteins, which pushes the company toward premium applications rather than commodity volumes.

Roquette Frères S.A. continues to benefit from its scale in plant proteins and its ability to serve multinational customers with consistent quality and documentation. Analyst-wise, Roquette’s advantage is application support—helping brands solve gritty textures and off-notes that can show up in lentil-based formulas. In 2025, it is well placed to win “reformulation” projects where customers want higher protein without sacrificing taste or process efficiency.

Cargill, Incorporated brings muscle in sourcing, global distribution, and customer access across food, beverage, and nutrition channels. The 2025 opportunity is to make lentil protein easier to buy and easier to use—bundling it with stabilizers, sweeteners, and texturizers for turnkey solutions. From a competitive lens, Cargill can accelerate adoption by de-risking supply and offering strong technical service for large-scale launches.

Top Key Players in the Market

- Parabel USA Inc.

- TerraVia Holdings, Inc.

- Roquette Frères S.A.

- Cargill, Incorporated

- Ingredion Incorporated

- Kerry Group plc

- Archer Daniels Midland Company

- Burcon NutraScience Corporation

- Glanbia plc

- Emsland Group

- Axiom Foods, Inc.

- Beneo GmbH

Recent Developments

- In 2025, Parabel USA Inc., known for its Lentein plant protein derived from water lentils (Lemna), has focused on regulatory advancements and safety validations for its products. In March 2025, the company submitted a GRAS Notice (GRN) 1256 to the FDA for Lemna leaf protein, produced from Lemnaceae aquatic plants.

- In 2025, TerraVia Holdings, Inc. (formerly Solazyme, Inc.), has seen its algae-based technologies integrated into Corbion’s operations for plant-based proteins and ingredients. Recent Corbion developments include advancements in algae-derived plant-based proteins for meat alternatives.

Report Scope

Report Features Description Market Value (2024) USD 521.3 Million Forecast Revenue (2034) USD 1590.4 Million CAGR (2025-2034) 11.8% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Powder, Liquid, Capsules), By Application (Food and Beverages, Nutritional Supplements, Animal Feed, Pharmaceuticals, Others), By Distribution Channel (Supermarkets and Hypermarkets, Online Stores, Specialty Stores, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Parabel USA Inc., TerraVia Holdings, Inc., Roquette Frères S.A., Cargill, Incorporated, Ingredion Incorporated, Kerry Group plc, Archer Daniels Midland Company, Burcon NutraScience Corporation, Glanbia plc, Emsland Group, Axiom Foods, Inc., Beneo GmbH Customization Scope Customisation for segments, region/country-level will be provided. Moreover, additional customisation can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Lentein Plant Protein MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Lentein Plant Protein MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Parabel USA Inc.

- TerraVia Holdings, Inc.

- Roquette Frères S.A.

- Cargill, Incorporated

- Ingredion Incorporated

- Kerry Group plc

- Archer Daniels Midland Company

- Burcon NutraScience Corporation

- Glanbia plc

- Emsland Group

- Axiom Foods, Inc.

- Beneo GmbH

Our Clients

- 176711

- February 2026