Global Irrigation Automation Market Size, Share Analysis Report By Automation (Time-Based, Volume-Based, Real-time Based, Computer-Based Control System), By Component (Controllers, Sensors, Valves, Sprinklers, Others), By Irrigation (Sprinkler Irrigation, Drip Irrigation, Surface Irrigation, Others), By Application (Agricultural, Non-agricultural) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180900

- Number of Pages: 223

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

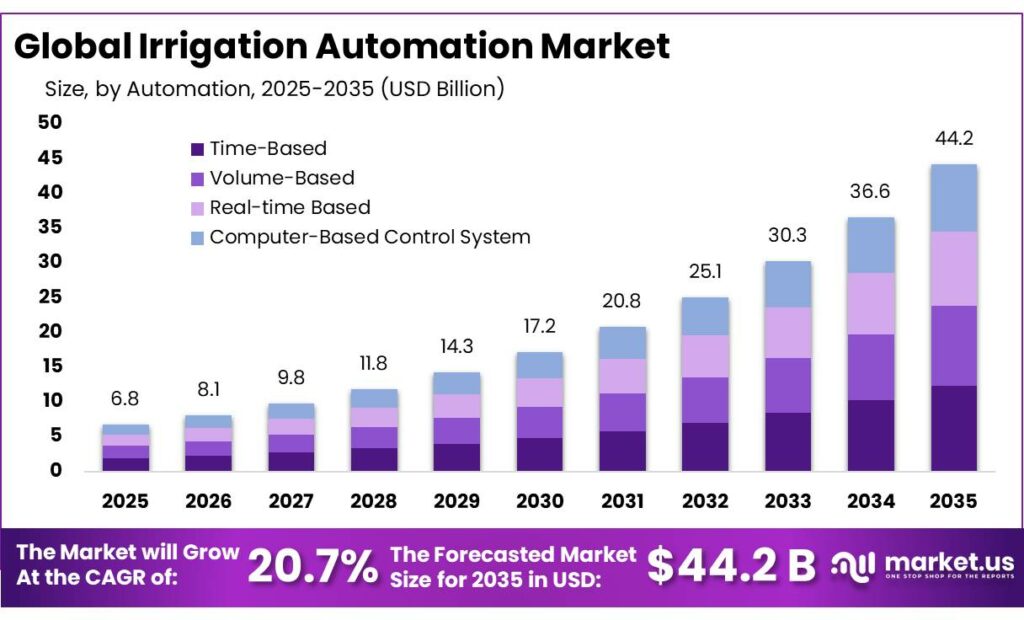

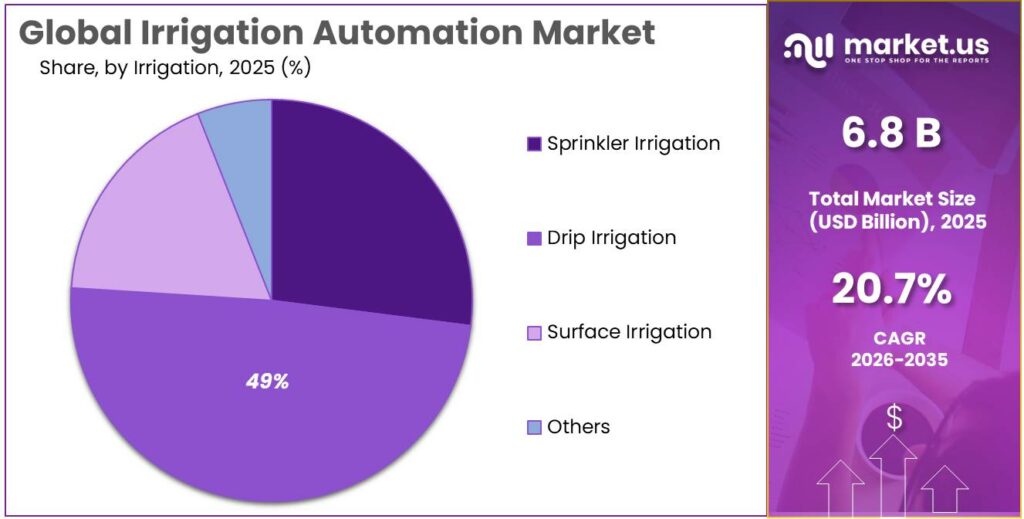

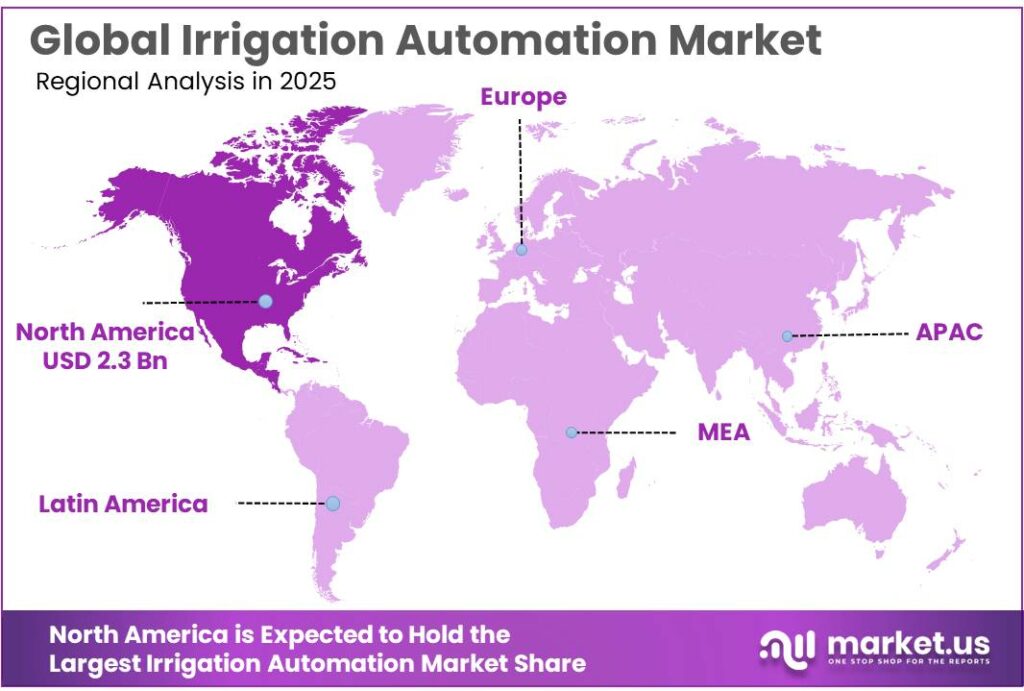

The Global Irrigation Automation Market size is expected to be worth around USD 44.2 Billion by 2035, from USD 6.8 Billion in 2025, growing at a CAGR of 20.7% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 34.8% share, holding USD 2.3 Billion revenue.

The irrigation automation industry represents an evolving segment within the broader agricultural technology landscape, focused on deploying automated systems that optimize the delivery of water to crops with minimal human intervention. These systems integrate sensors, controllers, software, and smart valves to adjust water application based on real-time soil moisture, weather data and crop needs, thereby supporting sustainable water management.

- Agriculture globally consumes roughly 70% of freshwater withdrawals, with irrigated agriculture alone accounting for the majority of this demand, underscoring the need for smarter irrigation solutions.

The industrial scenario for irrigation automation is increasingly shaped by water scarcity, demographic pressures and the imperative to boost agricultural productivity. Agriculture’s heavy burden on freshwater resources — consuming up to 70% of all accessible freshwater — drives investment in technologies that reduce waste and improve water use efficiency. Field studies have found that intelligent irrigation methods can improve water use efficiency dramatically — in some cases by up to 40–60% compared to traditional irrigation practices — while also enhancing yield performance.

These systems are designed to improve water-use efficiency, reduce labor dependency, and enhance crop productivity through intelligent water management practices. Smart irrigation technologies combine hardware components such as valves, pumps, and controllers with software analytics and data platforms to create a connected agricultural ecosystem capable of supporting sustainable farming. Research indicates that smart irrigation technologies can reduce water consumption by approximately 30–50% while increasing crop yields by 10–25%, demonstrating their strong potential in addressing global agricultural efficiency challenges.

Government initiatives and policy frameworks are also playing a crucial role in accelerating the adoption of irrigation automation solutions. For example, India’s Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) promotes micro-irrigation and smart water management to improve agricultural productivity and water conservation.

- Recent programs integrating sensor-based irrigation systems have demonstrated potential water savings of 20–30%, while offering subsidies of up to ₹2.4 lakh per hectare for farmers adopting advanced irrigation technologies. Similarly, regional programs promoting drip and sprinkler irrigation technologies have demonstrated significant water conservation potential, with some modern irrigation practices capable of saving 40–80% of water compared with traditional irrigation methods.

Key Takeaways

- Irrigation Automation Market size is expected to be worth around USD 44.2 Billion by 2035, from USD 6.8 Billion in 2025, growing at a CAGR of 20.7%

- Time-Based held a dominant market position, capturing more than a 27.7% share.

- Controllers held a dominant market position, capturing more than a 32.4% share.

- Drip Irrigation held a dominant market position, capturing more than a 49.6% share.

- Agricultural held a dominant market position, capturing more than a 78.9% share.

- North America stands out as a dominant force, accounting for approximately 34.8% of global market share with an estimated market value of USD 2.3 billion.

By Automation Analysis

Time-Based Irrigation Leads the Market with 27.7% Share in 2024

In 2024, Time-Based held a dominant market position, capturing more than a 27.7% share. This segment continues to be widely adopted across agricultural fields, landscaping projects, and commercial farming operations due to its simplicity and reliability. Time-based irrigation systems operate on pre-set schedules, allowing water to be delivered at fixed intervals without the need for complex sensors or real-time monitoring tools. Farmers and land managers prefer this system because it offers predictable watering cycles and is easy to manage, especially in regions where crop patterns and climate conditions remain relatively stable throughout the season.

By Component Analysis

Controllers dominate with 32.4% share as the core decision-making unit in irrigation systems

In 2024, Controllers held a dominant market position, capturing more than a 32.4% share. This strong position reflects their central role in irrigation automation systems. Controllers act as the brain of the entire setup, managing watering schedules, regulating water flow, and coordinating with valves, pumps, and sensors. Without controllers, automated irrigation systems cannot function efficiently. Their widespread adoption across farms, greenhouses, sports fields, and landscaping projects significantly contributed to their leading share during the year.

By Irrigation Analysis

Drip Irrigation leads the way with 49.6% share driven by water efficiency and precise delivery

In 2024, Drip Irrigation held a dominant market position, capturing more than a 49.6% share. This strong leadership reflects the growing shift toward water-efficient farming practices across the world. Drip irrigation systems deliver water directly to the plant root zone through a network of pipes and emitters, minimizing evaporation and runoff. Because of this targeted approach, farmers are able to use water more efficiently while maintaining healthy crop growth. The high adoption rate of drip systems across horticulture, fruits, vegetables, and plantation crops significantly supported its leading share during the year.

By Application Analysis

Agricultural application leads strongly with 78.9% share driven by farm-level automation demand

In 2024, Agricultural held a dominant market position, capturing more than a 78.9% share. This overwhelming share clearly reflects that irrigation automation is primarily driven by farming activities. The agricultural sector remains the largest user of automated irrigation systems, as water management directly affects crop yield, quality, and overall farm profitability. Farmers across both developed and developing regions are increasingly turning to automated irrigation solutions to manage water more efficiently and reduce dependency on manual labor.

Key Market Segments

By Automation

- Time-Based

- Volume-Based

- Real-time Based

- Computer-Based Control System

By Component

- Controllers

- Sensors

- Valves

- Sprinklers

- Others

By Irrigation

- Sprinkler Irrigation

- Drip Irrigation

- Surface Irrigation

- Others

By Application

- Agricultural

- Open Fields

- Greenhouses

- Others

- Non-agricultural

- Golf Courses

- Residential

- Sports Grounds

- Others

Emerging Trends

Rise of Smart and Connected Irrigation with Real-Time Data at the Core

One of the most exciting and transformative trends in irrigation automation today is the rise of smart and connected irrigation systems that use real-time data from sensors, weather services and remote monitoring to make irrigation decisions automatically. This isn’t just about turning water on and off at set times anymore — farmers are beginning to use data the same way they use sun and soil information, treating moisture levels and weather forecasts as essential partners in growing crops.

At its heart, this trend reflects a deeper understanding of how water use and crop needs are connected. The Food and Agriculture Organization (FAO) notes that irrigation supports about 40% of the world’s crop production while using only 20% of cultivated land — a striking statistic that highlights both the importance and the challenges of efficient water use in agriculture. With farming taking such a major role in feeding the world, innovations that save water and boost yields are becoming central to modern agriculture.

Smart irrigation systems build on this foundation by integrating digital technologies that could have sounded like science fiction a decade ago. Soil moisture sensors, for example, can track the exact amount of water in the root zone of plants throughout the day. Research into smart irrigation demonstrates that such systems can improve water use efficiency by between 20 % and 50 %, meaning farmers can stretch each drop of water much further than with traditional methods.

Government support and research institutions have also played a role in promoting this trend. In some regions, technology-driven irrigation initiatives now include sensor-based solutions under government schemes aimed at sustainability and farm income growth. For example, recent programmes in India under the Pradhan Mantri Krishi Sinchayee Yojana have introduced automation and sensor-based micro-irrigation systems that can save 20–30 % of water compared to traditional practices, while helping farmers manage their resources more effectively.

Drivers

Efficient Water Use in Agriculture: The Key Driver Behind Irrigation Automation

One of the strongest forces pushing farmers and agri-businesses toward irrigation automation today is the urgent need to use water more wisely. Agriculture already uses a huge share of the world’s freshwater supplies, and this puts immense pressure on farmers to rethink how water is managed in their fields.

Globally, about 70 % of freshwater withdrawals are used by the agricultural sector to grow crops and support food production. This staggering figure highlights just how dependent farming is on water and how much of the planet’s freshwater resources are at stake whenever irrigation takes place.

In many regions, traditional irrigation methods—such as flooding fields or using simple sprinkler systems—do not distribute water efficiently. Large volumes are lost through evaporation, runoff and seepage long before plant roots can actually benefit from it. According to estimates, up to 60% of water withdrawn for agriculture can be lost due to these inefficiencies. These losses are not just numbers on a page: they represent real water that could have supported crops, soil health, livestock and entire rural communities.

For farmers, this inefficiency translates into higher costs and greater vulnerability. When water is scarce, crops suffer, yields drop, and farmers must either invest in more water sources or rethink their cultivation patterns. It also means that agricultural production contributes disproportionately to water stress in many parts of the world. Across low-income countries, water used for farming can account for up to 90% of all freshwater withdrawals, heightening the urgency to improve water productivity at the farm level.

Government initiatives and international organizations are also encouraging this shift. For example, programs that support precision irrigation and micro-irrigation often come with technical assistance and financial incentives to help farmers adopt automation technologies. These efforts are part of broader strategies to improve agricultural water productivity and achieve sustainable food systems. In some developing regions, support from agencies like the Food and Agriculture Organization helps farmers access automated irrigation solutions that would otherwise be out of reach.

Restraints

High Initial Cost and Infrastructure Challenges Hinder Wider Adoption

One major factor restraining the growth of irrigation automation is the high initial cost and associated infrastructure challenges that many farmers, especially smallholders, face when trying to adopt these systems. While the benefits of automated irrigation—such as better water use and reduced labour—are clear, the financial barrier to entry remains a serious hurdle for many working in agriculture.

Another part of the problem is that, in some areas, the supporting infrastructure needed for effective irrigation automation isn’t yet well-developed. Reliable electricity, access to broadband or mobile networks, and technical service providers are all vital for advanced irrigation systems to work as intended. In many rural regions, these basic services are limited or sporadic, which makes it harder to adopt technology that depends on them.

This issue is compounded by the fact that agriculture already consumes a massive amount of the world’s freshwater supply—about 70% of all freshwater withdrawals. This statistic, highlighted by the Food and Agriculture Organization (FAO), underscores how much water agriculture uses compared to other sectors and why efficient systems matter. Yet even with this pressing need for water efficiency, the expensive upfront costs of automation create a barrier that slows widespread adoption.

In parts of the world where agriculture accounts for an even higher percentage of water withdrawals—sometimes up to 90% in low-income countries, according to the World Bank—this challenge becomes even more stark. These regions could arguably benefit most from automation yet often lack the resources to fully adopt it.

Opportunity

Growing Demand from Water-Stressed Regions Opens Big Opportunities for Irrigation Automation

One of the most significant growth opportunities for irrigation automation lies in meeting the increasing need for efficient water use in regions suffering from water scarcity. As climate change alters rainfall patterns and droughts become more frequent, farmers in many parts of the world are feeling squeezed between the need to grow more food and the reality of limited water supplies. This tension is turning attention toward smarter irrigation methods that can deliver water where it’s needed most, and avoid waste wherever possible.

Globally, agriculture already accounts for a huge slice of freshwater use — roughly 70% of all freshwater withdrawals goes toward growing crops and supporting livestock. That number comes from work by the Food and Agriculture Organization (FAO), and it shows just how central water is to farming everywhere. The flip side of this reality is that when water becomes scarce — whether because of drought, population growth, or competing demand from cities and industry — traditional irrigation starts to look unsustainable and inefficient.

In addition to policy support, wider awareness about water stress is helping drive adoption. Farmers are increasingly exposed to the hard facts: in some low-income countries, water withdrawals for agriculture can reach up to 90% of all freshwater use, according to research cited by the World Bank. When you hear numbers like that, it’s easy to understand why growers are motivated to rethink how they irrigate their fields.

Regional Insights

North America Leads with Strong Adoption, Holding 34.8% Share and USD 2.3 Bn in Value

In the regional landscape of the irrigation automation market, North America stands out as a dominant force, accounting for approximately 34.8% of global market share with an estimated market value of USD 2.3 billion. This leadership reflects the region’s advanced agricultural infrastructure, strong emphasis on technology adoption, and supportive policy environment that encourages efficient water management practices across commercial and small-scale farms alike.

Government initiatives in North America have also bolstered the uptake of irrigation automation technologies. Federal and state programs provide funding and technical support for water-saving practices, including precision irrigation and automation upgrades. These incentives have reduced financial barriers for growers considering modernising their irrigation systems, further contributing to the region’s sizeable market share.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

CALSENSE is a US-based irrigation technology provider with over 30 years of experience in designing automated irrigation control systems that help users manage water usage efficiently. The company’s solutions include advanced irrigation controllers and water management software designed to reduce water waste and labour costs while boosting operational performance. Its technology supports data-driven irrigation decisions and is widely used across commercial landscapes, turf management, and smart irrigation installations to conserve water and labour resources.

Hunter Industries is a prominent American manufacturer of irrigation equipment including controllers, sensors, rotors, valves and water-management software. Founded in 1981, the company operates in 125+ countries and holds over 250 product patents and 40 trademarks. Its automation offerings, enhanced by the Hydrawise Wi-Fi irrigation platform, allow users to monitor and adjust irrigation schedules based on real-time weather and site conditions, driving water conservation and operational ease.

Top Key Players Outlook

- CALSENSE

- Galcon (PLASSON)

- HUNTER INDUSTRIES

- Hydropoint Data Systems

- Rivulis

- Lindsay Corporation

- Mottech Water Solutions Ltd.

- Nelson Irrigation Corporation

- NETAFIM

- Orbit Irrigation Products

- Rain Bird Corporation

- The Toro Company

- Valmont Industries

- Weathermatic

Recent Industry Developments

By 2025, Rivulis’ current corporate profile shows further expansion to 19 manufacturing facilities, more than 2,500 employees, 3 R&D centers, over 6,000 partners, and 7,000 growers served worldwide, which signals stronger reach for deploying automated irrigation systems at farm level.

In 2025, Lindsay Corporation, irrigation segment delivered $129.0 million in revenue, with $50.0 million from North America and $79.0 million from international markets, while irrigation operating income improved to $17.7 million and margin edged up to 13.7%.

Report Scope

Report Features Description Market Value (2025) USD 6.8 Bn Forecast Revenue (2035) USD 44.2 Bn CAGR (2026-2035) 20.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Automation (Time-Based, Volume-Based, Real-time Based, Computer-Based Control System), By Component (Controllers, Sensors, Valves, Sprinklers, Others), By Irrigation (Sprinkler Irrigation, Drip Irrigation, Surface Irrigation, Others), By Application (Agricultural, Non-agricultural) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape CALSENSE, Galcon (PLASSON), HUNTER INDUSTRIES, Hydropoint Data Systems, Rivulis, Lindsay Corporation, Mottech Water Solutions Ltd., Nelson Irrigation Corporation, NETAFIM, Orbit Irrigation Products, Rain Bird Corporation, The Toro Company, Valmont Industries, Weathermatic Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Irrigation Automation MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Irrigation Automation MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- CALSENSE

- Galcon (PLASSON)

- HUNTER INDUSTRIES

- Hydropoint Data Systems

- Rivulis

- Lindsay Corporation

- Mottech Water Solutions Ltd.

- Nelson Irrigation Corporation

- NETAFIM

- Orbit Irrigation Products

- Rain Bird Corporation

- The Toro Company

- Valmont Industries

- Weathermatic

Our Clients

- 180900

- Mar 2026