Quick Navigation

Market Size

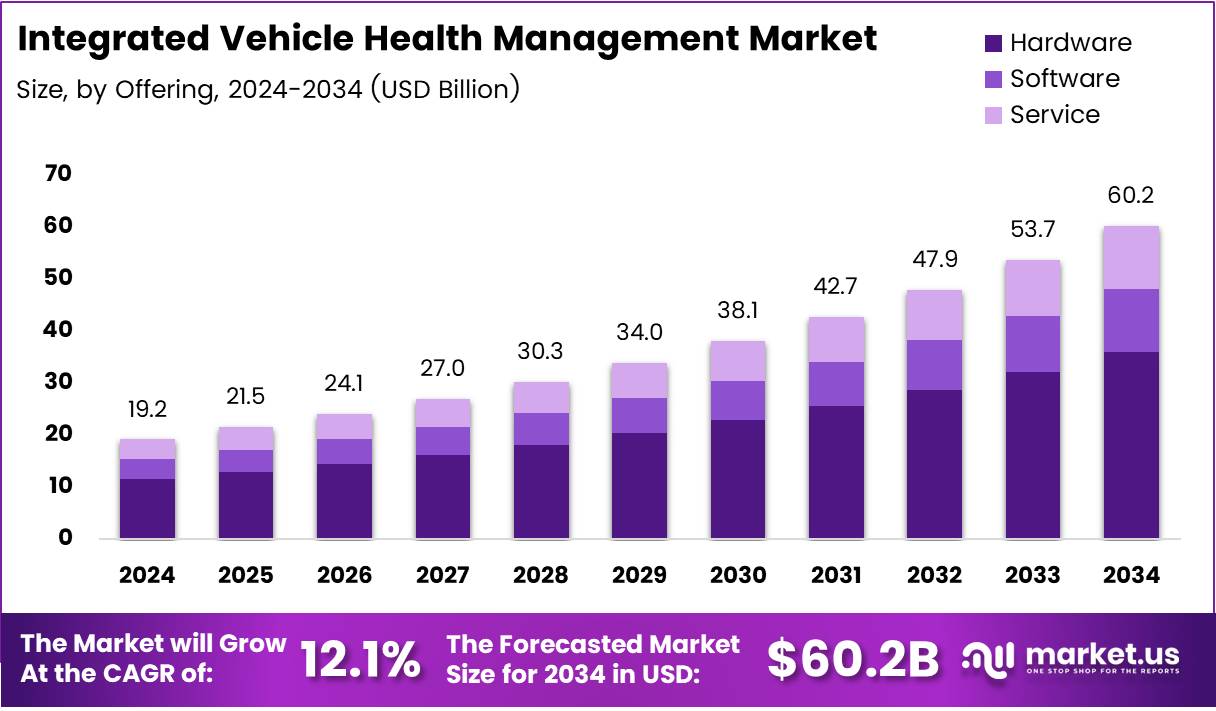

The Global Integrated Vehicle Health Management Market size is expected to be worth around USD 60.2 Billion by 2034, from USD 19.2 Billion in 2024, growing at a CAGR of 12.1% during the forecast period from 2025 to 2034. This growth is driven by the increasing demand for connected vehicle technologies, improved vehicle safety features, and advancements in predictive maintenance solutions.

Key Takeaways

- The Global Integrated Vehicle Health Management Market is expected to reach USD 60.2 Billion by 2034, growing at a CAGR of 12.1% from 2025 to 2034.

- Hardware accounted for the largest share in the By Offering Analysis segment, with 58.2% in 2024.

- Diagnostics dominated the By Application Analysis segment in 2024, ensuring timely interventions and minimizing unexpected vehicle failures.

- Service Centers led the By Channel Analysis segment in 2024, offering specialized maintenance and troubleshooting.

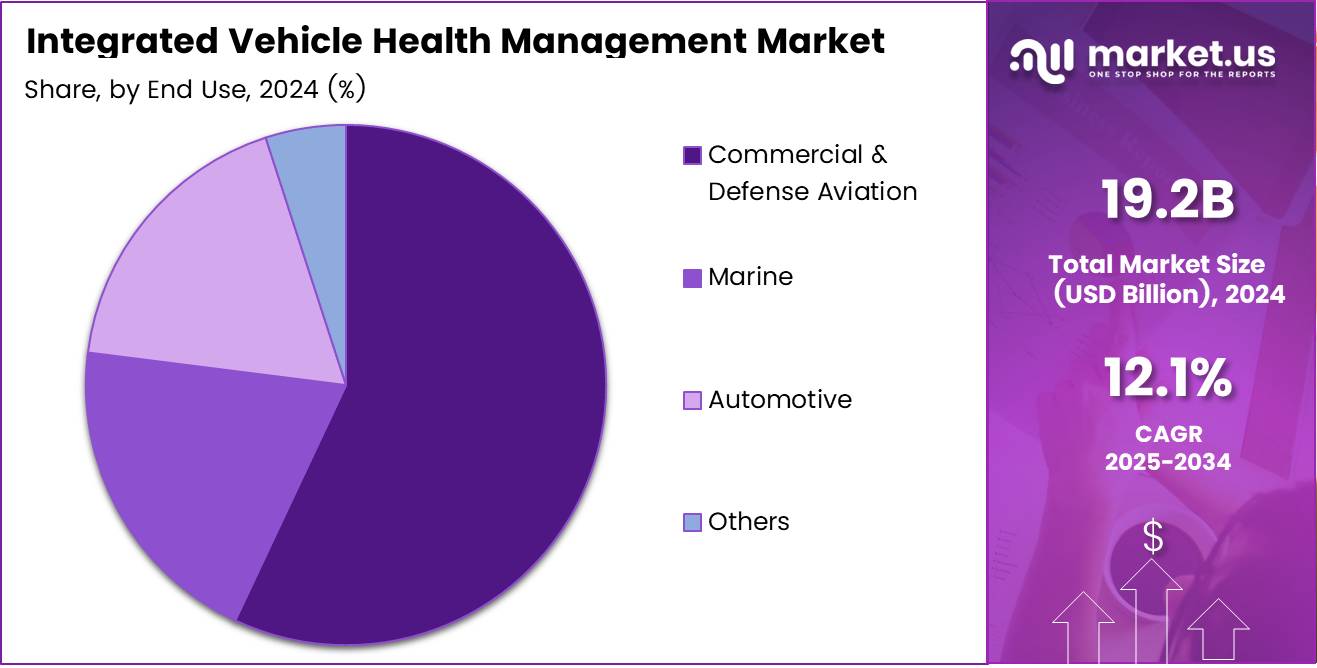

- Commercial & Defense Aviation held the dominant position in the By End Use Analysis segment in 2024.

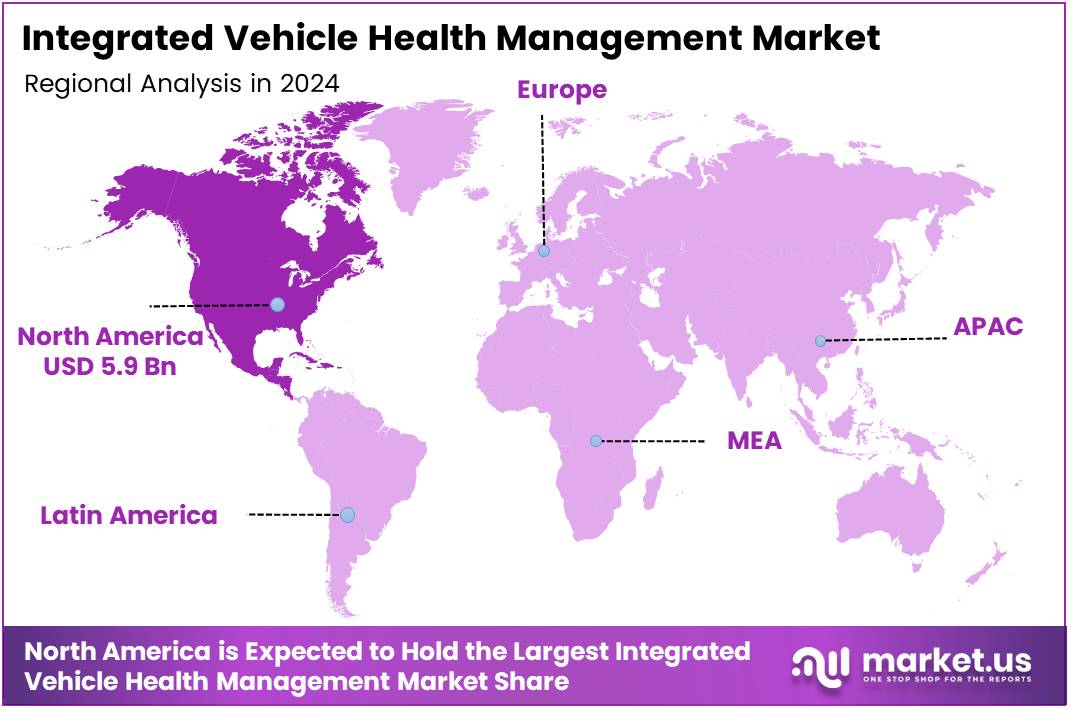

- North America led the IVHM market in 2025 with a 31.2% market share, valued at USD 5.9 Billion.

Report Overview

Integrated Vehicle Health Management (IVHM) refers to a system that continuously monitors, diagnoses, and predicts the health of vehicle components to ensure optimal performance, reduce downtime, and enhance safety. It integrates sensor data, diagnostics software, and analytics to deliver predictive insights. As vehicles become more connected and autonomous, IVHM becomes increasingly vital for automotive, aviation, and defense sectors, ensuring real-time decision-making and efficient maintenance.

The Integrated Vehicle Health Management market is witnessing steady growth, driven by the rising adoption of smart mobility solutions and connected vehicles. According to Salesforce, by 2030, 95% of new vehicles sold will be connected, which is expected to significantly drive demand for IVHM solutions. These connected platforms allow seamless health tracking of components and enable predictive maintenance, minimizing vehicle failures.

In the U.S., the surge in connected car sales is already evident. As per Smartcar, 91% of new vehicles sold in the country are connected, underlining the country’s readiness to embrace IVHM systems. This widespread connectivity lays the foundation for widespread adoption of vehicle health diagnostics and monitoring solutions, as OEMs integrate advanced telematics.

Growth opportunities are also emerging from the operational inefficiencies in vehicle diagnostics. According to IJRASET, nearly 30% of vehicle breakdowns occur due to delayed diagnostics. This highlights the critical role of IVHM in preventing unplanned downtimes and reducing costly repairs, especially in commercial fleets and defense aviation.

Furthermore, governments are investing heavily in vehicle safety and predictive technologies. For instance, regulatory bodies in North America and Europe are promoting vehicle safety mandates that encourage OEMs to deploy predictive maintenance systems, creating favorable conditions for IVHM market expansion.

Rapid digitization in the automotive industry, coupled with the growing integration of AI and IoT technologies, is fueling adoption across various end-use industries. With embedded sensors and cloud-based analytics, vehicle health can be monitored in real-time, allowing for timely interventions and cost savings.

Emerging economies are also catching up, especially in Asia-Pacific, where increased industrial transportation and a push toward electric mobility are driving the need for health monitoring systems in vehicles. As governments tighten emission standards, IVHM tools become essential to maintain compliance and operational efficiency.

On the commercial aviation front, IVHM systems are being increasingly deployed to ensure mission readiness and safety. Aircraft manufacturers are embedding these systems to track mechanical health and schedule repairs without disrupting flight schedules.

Offering Analysis

Hardware holds a dominant market position with 58.2% share in 2024

In 2024, Hardware accounted for the largest share in the By Offering Analysis segment of the Integrated Vehicle Health Management market, with a significant share of 58.2%. This dominance is attributed to the essential role hardware plays in providing the core infrastructure necessary for the functioning of vehicle health systems. Components like sensors, processors, and communication units are critical for real-time monitoring and diagnostics.

Software and services also contribute to the market, but hardware remains central due to the growing need for robust physical components that support advanced vehicle health management systems. Hardware enables seamless integration with other vehicle systems, ensuring continuous performance monitoring and predictive maintenance.

As the demand for efficient and reliable vehicle health management solutions continues to rise, the hardware segment is expected to retain its leadership position, driven by technological advancements and increasing adoption of IoT-enabled systems in vehicles.

Application Analysis

Diagnostics leads the market with the highest share, driven by its critical role in vehicle health management.

In 2024, Diagnostics held a dominant market position in the By Application Analysis segment of the Integrated Vehicle Health Management market. Diagnostics tools are essential in identifying issues within vehicles, ensuring timely interventions and minimizing unexpected failures. The growing demand for advanced diagnostic tools in the automotive and aerospace industries has led to the sector’s substantial growth.

Prognostics, though important for predicting future vehicle health trends, does not yet match diagnostics in terms of market share. While prognostics will continue to evolve and gain importance, diagnostics remains the backbone of vehicle health management systems in 2024, securing its market leadership position.

As vehicle technology advances and demands for real-time diagnostics increase, the diagnostics segment will likely maintain its leading share, supported by improvements in sensor technology and data analytics.

Channel Analysis

Service Centers hold a dominant market position in 2024, leading the By Channel Analysis segment of Integrated Vehicle Health Management market

In 2024, Service Centers dominated the By Channel Analysis segment of the Integrated Vehicle Health Management market. This is due to the high demand for expert repairs and diagnostics that require specialized service center facilities. Service centers offer direct, hands-on maintenance and troubleshooting, ensuring that vehicles maintain optimal health.

OEMs (Original Equipment Manufacturers) also contribute to the market, but service centers are the preferred channel for end-users seeking specialized, timely, and cost-effective solutions. The flexibility and convenience offered by service centers in dealing with complex vehicle health issues make them the most popular choice for consumers.

As the market for integrated vehicle health management solutions continues to expand, service centers are expected to remain the dominant channel, driven by their established expertise and customer trust.

End Use Analysis

Commercial & Defense Aviation leads the By End Use Analysis segment in 2024 with a dominant market share

In 2024, Commercial & Defense Aviation held a dominant position in the By End Use Analysis segment of the Integrated Vehicle Health Management market.

Aviation systems require the highest standards of reliability and maintenance, with real-time health monitoring being crucial for ensuring the safety and operational efficiency of aircraft. This sector’s stringent regulations and high safety standards further emphasize the importance of integrated vehicle health management solutions.

Other sectors such as Marine, Automotive, and Others also contribute to the market but do not surpass the aviation industry in terms of market share. While automotive applications are growing with increasing integration of vehicle health systems in commercial and consumer vehicles, aviation’s advanced and high-cost equipment needs ensure its continued market dominance.

As demand for cutting-edge health management systems increases across industries, aviation is likely to maintain its leadership, particularly in sectors demanding high reliability and predictive maintenance capabilities.

Key Market Segments

By Offering

- Hardware

- Software

- Service

By Application

- Diagnostics

- Prognostics

By Channel

- Service Center

- OEM

By End Use

- Commercial & Defense Aviation

- Marine

- Automotive

- Others

Drivers

Increasing Adoption of Connected Vehicles and IoT Technologies Drives Integrated Vehicle Health Management Market

The rapid adoption of connected vehicles and IoT technologies has been a key driver for the growth of the integrated vehicle health management (IVHM) market.

As more vehicles are equipped with advanced sensors and connectivity features, there is an increasing demand for systems that can monitor and manage vehicle health in real-time. These technologies enable better diagnostics, predictive maintenance, and improved overall vehicle performance, which leads to enhanced customer satisfaction and reduced operational costs.

Furthermore, the integration of IoT technologies with vehicles provides valuable data that helps manufacturers, fleet managers, and consumers to make informed decisions. This connectivity helps in identifying potential issues before they become critical, improving safety and performance.

Restraints

Challenges Hindering the Growth of Integrated Vehicle Health Management Market

Despite the potential benefits, there are several challenges restraining the widespread adoption of integrated vehicle health management systems. One major obstacle is the high initial investment required for implementing these systems. The cost of integrating advanced sensors, software, and telematics into vehicles can be prohibitive, especially for smaller manufacturers or fleet operators.

Additionally, there is a limited availability of skilled professionals to manage and maintain these advanced systems. As vehicle technology evolves, the demand for experts in vehicle health management technologies increases, but the supply of qualified individuals remains insufficient.

Data privacy and security concerns also play a significant role in slowing down market growth. As vehicles become more connected, the risk of cyber threats and data breaches grows, leading to hesitance among consumers and manufacturers alike. Finally, integrating new technologies with existing legacy vehicle systems presents additional complexities, which can delay the implementation of integrated vehicle health management solutions.

Growth Factors

Growth Opportunities for the Integrated Vehicle Health Management Market

The integrated vehicle health management market presents significant growth opportunities, particularly in emerging markets. As vehicle manufacturers and fleet operators seek to improve efficiency and reduce downtime, there is increasing interest in implementing IVHM solutions in countries with growing automotive industries.

With the rise of electric and autonomous vehicles, the demand for advanced health monitoring systems is set to grow. These vehicles, which rely heavily on electronics and software, benefit from real-time monitoring to ensure optimal performance and safety. Moreover, advancements in artificial intelligence (AI) and machine learning are enhancing predictive analytics, enabling better forecasts of vehicle health and performance.

Another promising growth opportunity lies in the development of partnerships between original equipment manufacturers (OEMs) and telematics service providers. These collaborations can lead to the creation of integrated solutions that provide more comprehensive monitoring, reducing operational costs and improving vehicle longevity.

Emerging Trends

Trending Factors Shaping the Integrated Vehicle Health Management Market

Several emerging trends are shaping the future of the integrated vehicle health management market. One of the key trends is the increasing use of big data analytics for real-time vehicle performance monitoring. By leveraging large datasets, vehicle health systems can provide actionable insights, enabling fleet operators and manufacturers to improve vehicle reliability and reduce maintenance costs.

Another significant trend is the shift towards cloud-based platforms for vehicle health management. Cloud solutions offer flexibility, scalability, and easier access to vehicle data, improving the overall management of vehicle health across large fleets.

In addition, there is a growing emphasis on eco-friendly and sustainable vehicle technologies. Consumers and manufacturers alike are seeking solutions that minimize environmental impact, and the integration of health management systems can help optimize fuel efficiency and reduce emissions.

Lastly, the integration of 5G connectivity is playing a crucial role in enhancing vehicle communication systems. The high-speed, low-latency features of 5G enable faster data transfer and real-time diagnostics, significantly improving the efficiency and performance of integrated vehicle health management systems.

Regional Analysis

North America Dominates the Integrated Vehicle Health Management Market with a Market Share of 31.2%, Valued at USD 5.9 Billion

In 2025, North America is leading the Integrated Vehicle Health Management (IVHM) market, holding a dominant share of 31.2%, valued at USD 5.9 Billion. This is largely attributed to the strong adoption of advanced connected vehicle technologies, coupled with regulatory frameworks that promote vehicle safety and performance. Government incentives and high demand for predictive maintenance in the region are driving market growth.

Europe IVHM Market Trends

Europe follows closely as a significant market for IVHM, characterized by growing regulatory pressure to improve vehicle emissions and safety standards. The European market is seeing a rise in the integration of IoT and AI technologies in the automotive industry. The presence of established automotive players, particularly in Germany and France, further supports the demand for integrated vehicle health management systems.

Asia Pacific IVHM Market Trends

Asia Pacific is expected to experience substantial growth in the IVHM market due to the rapidly expanding automotive sector in countries like China, Japan, and India. The increasing adoption of connected vehicles and a rising middle class with higher disposable income is driving the demand for advanced vehicle health management solutions in the region. Moreover, the government’s focus on reducing vehicle emissions is contributing to the market’s expansion.

Middle East and Africa IVHM Market Trends

The Middle East and Africa region is experiencing steady growth in the IVHM market, driven by the increasing adoption of new vehicle technologies and rising urbanization. In addition, significant investments in smart city projects and infrastructure development are expected to bolster the adoption of connected vehicle solutions. While market penetration remains low compared to other regions, the growing interest in vehicle safety and performance diagnostics offers a positive outlook.

Latin America IVHM Market Trends

In Latin America, the IVHM market is showing signs of growth, though at a slower pace than other regions. The demand for connected vehicle systems is gaining momentum in countries like Brazil and Mexico, where improving road safety and reducing vehicle downtime is becoming a priority. However, limited infrastructure and economic factors pose challenges to rapid adoption in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Integrated Vehicle Health Management Company Insights

ZF Friedrichshafen AG is positioning itself as a leader in the integrated vehicle health management space through its focus on advanced sensor technologies and predictive analytics. The company is driving innovation with its cutting-edge solutions, enabling real-time monitoring and diagnostics of vehicle systems, which enhances operational efficiency and vehicle safety.

OnStar, a subsidiary of General Motors, has made significant strides in providing vehicle connectivity solutions. With its integrated telematics services, it offers real-time diagnostics and remote health checks, strengthening the vehicle’s ability to anticipate maintenance needs, thus minimizing downtime and improving vehicle longevity.

Garrett Motion Inc. is leveraging its expertise in turbocharging technologies to support the growth of integrated vehicle health management systems. The company is focused on enhancing engine performance and health monitoring through real-time data analysis, helping vehicle manufacturers optimize fuel efficiency and performance while reducing maintenance costs.

KPIT is enhancing the digitalization of vehicle health management with a focus on cloud-based solutions and AI-powered diagnostics. Their advanced software platforms are aimed at enabling predictive maintenance, which aids OEMs in managing vehicle health and enhancing the overall driving experience by reducing system failures and unplanned downtime.

These key players are contributing significantly to the development of the integrated vehicle health management market by focusing on advancements in telematics, sensor technology, and AI, which are critical for delivering robust, efficient, and predictive vehicle management solutions.

Top Key Players in the Market

- ZF Friedrichshafen AG

- OnStar

- Garrett Motion Inc.

- KPIT

- Continental AG

- Denso Corporation

- Vector Informatik GmbH

- Robert Bosch GmbH

- Visteon Corporation

- Cummins Inc.

Recent Developments

- In March 2025, Transit Technologies announced a strategic acquisition aimed at integrating advanced trip and charter management capabilities into its market-leading K-12 solutions. This acquisition is set to enhance the company’s offering for school transportation systems, addressing the growing need for more efficient routing and management in the education sector.

- In January 2025, UVeye secured $191M in funding to support the skyrocketing demand for its AI-powered vehicle inspection systems. This new funding will enable UVeye to expand its operations and further develop its cutting-edge technology, enhancing vehicle safety and operational efficiency.

- In April 2025, TTTech Auto’s CEO provided insights into the rationale behind NXP’s acquisition of the company, which aims to accelerate the development of advanced automotive technologies. The acquisition is expected to boost TTTech Auto’s role in the autonomous vehicle and safety systems sectors.

- In June 2024, COMPREDICT secured $15M in a Series B funding round, led by Woven Capital. This investment will help COMPREDICT expand its predictive analytics technology for the automotive sector, improving vehicle health monitoring and maintenance efficiency.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 19.2 Billion |

| Forecast Revenue (2034) | USD 60.2 Billion |

| CAGR (2025-2034) | 12.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Offering (Hardware, Software, Service), By Application (Diagnostics, Prognostics), By Channel (Service Center, OEM), By End Use (Commercial & Defense Aviation, Marine, Automotive, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | ZF Friedrichshafen AG, OnStar, Garrett Motion Inc., KPIT, Continental AG, Denso Corporation, Vector Informatik GmbH, Robert Bosch GmbH, Visteon Corporation, Cummins Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |