Quick Navigation

Report Overview

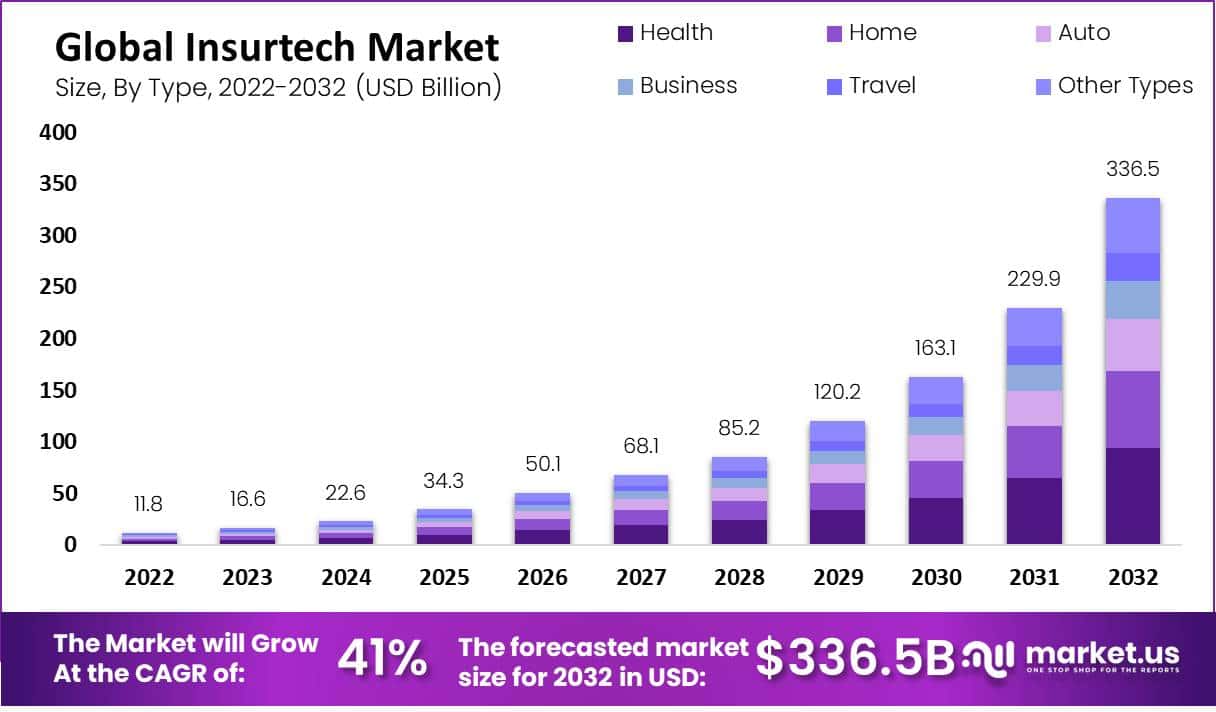

In 2023, the Global Insurtech Market was valued at USD 16.6 Billion and is expected to reach USD 336.5 billion in 2032. This market is estimated to register the highest CAGR of 41.0% between 2023 and 2032.

Insurtech refers to the use of technology to innovate and transform the insurance industry. It encompasses various digital tools, platforms, and applications that streamline and enhance the insurance process, from underwriting and policy management to claims processing and customer service. Insurtech aims to improve efficiency, accuracy, and customer experience within the insurance sector by leveraging advancements in areas such as data analytics, artificial intelligence, machine learning, Internet of Things (IoT), and blockchain.

The insurtech market has witnessed significant growth and disruption in recent years. One of the driving forces behind this market expansion is the increasing consumer demand for personalized and convenient insurance solutions. Insurtech companies have developed user-friendly platforms and mobile applications that allow customers to compare policies, obtain quotes, and purchase insurance coverage online, eliminating the need for traditional paperwork and lengthy processing times. This digital transformation has not only improved customer satisfaction but also increased the efficiency and speed of policy issuance.

Analyst Viewpoint

One of the primary driving factors is the increasing consumer demand for personalized and convenient insurance solutions. Traditional insurance processes have often been perceived as time-consuming. Insurtech companies have leveraged technology to streamline these processes, offering digital platforms and mobile applications that provide customers with easy access to insurance products and services. This customer-centric approach, coupled with the ability to provide tailored coverage based on individual needs and risk profiles, has propelled the growth of the insurtech sector.

According to the latest statistics from Gallagher Re, The insurtech sector experienced a significant funding downturn in the second quarter of 2023. The data reveals that New funding dropped to $916.71 million, marking a notable 34% decrease from the previous quarter’s total of $1.39 billion.

Insurtech companies have the chance to disrupt traditional insurance models by offering innovative products and services that cater to evolving customer needs. They can leverage technology to provide personalized insurance experiences, improve risk assessment accuracy, and enhance claims processing efficiency. Additionally, insurtech companies can tap into underserved markets or niche segments that traditional insurers may have overlooked.

The rise of insurtech also presents opportunities for collaboration between insurtech startups and established insurance companies. Incumbents can leverage the technological capabilities of insurtech companies to enhance their digital transformation efforts. This collaboration allows incumbents to benefit from the agility and innovation of insurtech startups while providing insurtech companies with access to established distribution networks, capital, and industry expertise.

Key Takeaways

- Insurtech Market is projected to reach a staggering USD 336.5 billion by 2032, with a promising Compound Annual Growth Rate (CAGR) of 41.0% during the forecast period from 2023 to 2032.

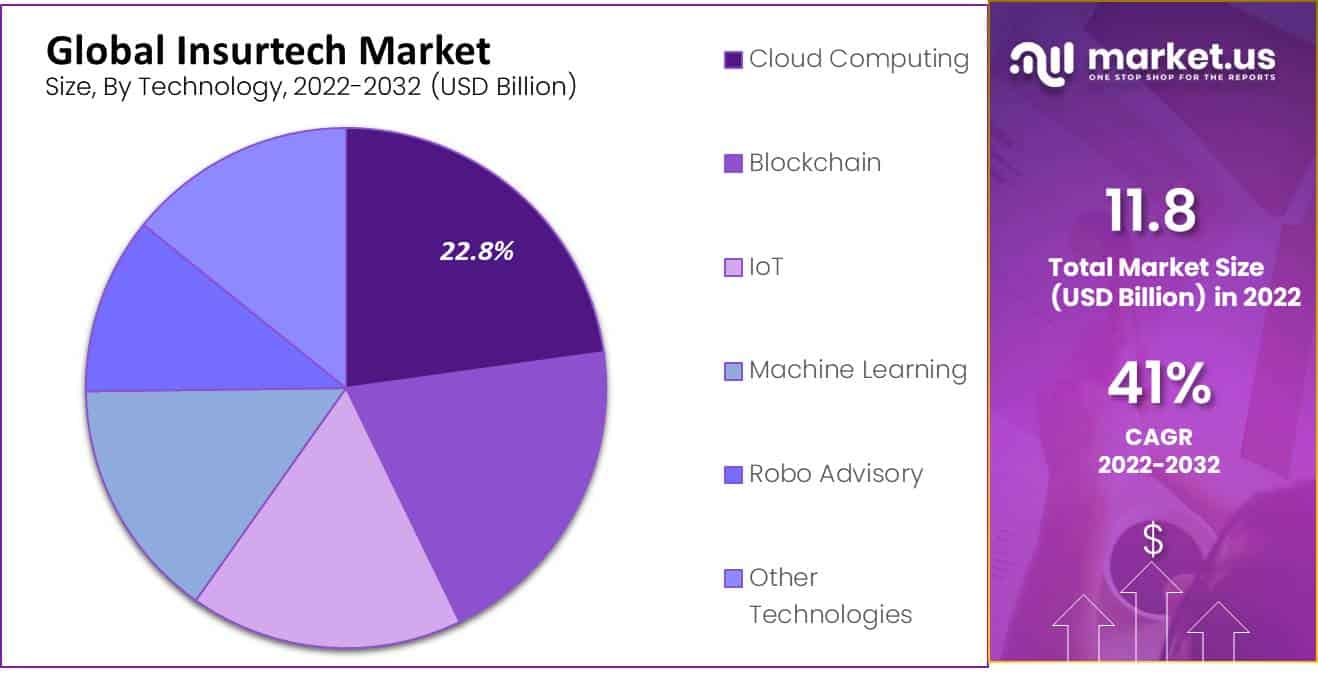

- Cloud computing holds a substantial market share, offering flexibility, deployment simplicity, and resourcefulness, revolutionizing the insurance industry and propelling the growth of the Insurtech market. (Cloud computing revenue share exceeding 22.8% by 2022)

- Managed services account for a significant share, offering insurers expertise and technology to facilitate transformation, improve business models, and adopt best practices, driving growth within the Insurtech market. (Managed services segment accounted for more than 36% of all revenue)

- In 2023, insurtech funding decreased to $4.6 billion, representing the lowest level since 2017.

- There was a 45% year-over-year (YoY) decline in total insurtech funding, down from $8.3 billion in 2022.

- The year witnessed 455 insurtech deals globally, the lowest in 6 years.

- Property & Casualty (P&C) insurtech deals experienced a 25% YoY reduction, whereas Life & Health (L&H) insurtech deals saw an even steeper decline.

- Early-stage insurtech deal sizes remained consistent at $3 million in 2023.

- Early-stage deals constituted 62% of all insurtech transactions, marking the lowest deal share in 5 years.

- The United States regained its position, accounting for over 50% of global insurtech deals in 2023, the first time since 2020.

- By 2024, it is estimated that more than 60% of insurance companies will have implemented at least one insurtech solution.

- The adoption of insurtech solutions for automated claims processing is projected to see a 45% increase among insurance providers from 2022 to 2024.

- Approximately 55% of insurance companies aim to integrate insurtech solutions for personalized product recommendations and dynamic pricing by the end of 2024.

- Over 65% of insurtech platforms are expected to offer embedded insurance capabilities for seamless integration with other products and services by 2024.

- The utilization of insurtech solutions for fraud detection and prevention is anticipated to grow by 40% among insurance companies from 2022 to 2024.

- By 2024, over 60% of insurtech deployments are projected to involve the use of artificial intelligence (AI) and machine learning (ML) for risk assessment and underwriting.

- Approximately 50% of insurance companies plan to adopt insurtech solutions for customer engagement and digital self-service capabilities by the end of 2024.

- It’s estimated that by 2024, over 70% of insurtech platforms will offer advanced data analytics and predictive modeling capabilities.

- The adoption of insurtech solutions for usage-based insurance (UBI) and telematics is projected to increase by 35% between 2022 and 2024.

- Over 55% of insurtech deployments are expected to involve the use of blockchain technology for secure data sharing and smart contracts by 2024

Type Analysis

The health segment dominates Insurtech. The growing demand for digital platforms that connect brokers, exchanges, providers, and health insurance carriers is expected to drive the market for this segment. Advanced analytics is a key focus for life and health insurance companies to serve their customers better. Many insurance companies use Insurtech to speed up claims processing. Insurers also want to combine their health insurance services and mobility features for added convenience.

Over the forecast period, the fastest growth is expected in the home segment. Many home insurance companies are looking to develop innovative products for residential and commercial real estate professionals, as well as their tenants and residents. These companies are adopting Insurtech solutions to speed up the list-to-lease time. These solutions use AI technology to create personalized insurance policies for customers and handle their claims efficiently without needing an insurance broker.

With auto insurance, customers can get financial protection against damage caused by traffic collisions and vehicle theft. It also covers injuries, death, and property damage to other drivers, vehicles, or property, such as fences, buildings, utility poles, or other property. While auto insurance requirements can vary from state to state, many jurisdictions require bodily injury and property damage liability coverage before a vehicle can be driven on public roads. As the number of road crashes is rising in many countries around the world, the potential for growth of the auto segment in the Insurtech market is high.

Deployment Analysis

Cloud-based solutions can be less costly than those on-premise. They also help Insurtech cut down on licensing, hardware, and the maintenance of its core infrastructure. Cloud platforms reduce the barriers to entry for Insurtech and increase market competition. They also drive customer value innovation. The cloud-based Insurtech is anticipated to grow during the forecast period due to increased data generation and mobile and social media usage. Declining data storage costs coupled with increasing adoption of cloud computing are accelerating the growth of this Insurtech market segment.

By Technology Analysis

Cloud computing dominated the market, with a revenue share exceeding 22.8% by 2022. With its flexibility, simplicity of deployment, and resourcefulness, cloud computing has revolutionized the insurance industry. The growing number of data that insurance companies have is expected to fuel the acceptance of Bring Your Own Device policies, and the increasing amount of data they hold will drive this growth.

Insurance companies are adopting cloud computing solutions due to their benefits, such as speed of deployment, cost-effectiveness, and scalability. Moreover, cloud computing solution providers are partnering with insurance companies to help companies improve their Insurtech products. This is expected to increase market growth.

Blockchain is expected to experience the greatest growth during the forecast period. Insurance companies can use blockchain technology to reduce operational costs and improve operational efficiency. Insurance companies can use this technology to increase growth, integrate different Insurtech platforms, and enable new services to go to market, especially for those who couldn’t access insurance before.

Insurance agencies can use blockchain innovation to lower operational expenses and increase functional efficiency. This innovation can increase development, integrate fluctuating Insurtech stages, or empower new administrations that advertise, especially those who cannot get protection. Because of its strengths like smart agreements, high-level mechanization, and solid online protection, Insurtech companies are expected to choose blockchain innovation.

Insurers can monitor even the smallest anomalies by offering IoT devices to monitor connected homes’ security and safety. The IoT system will alert insurance companies if there is an abnormality. This allows them to intervene to prevent further damage. IoT is a better option for customers and can reduce risk for insurance companies. Insurers can also partner with IoT vendors from third parties to increase their IoT offerings. They can also work with policyholders to ensure that the property and people covered are safe. IoT reduces the chance of a small issue becoming a costly problem and gives policyholders more security and care. These factors are expected to propel the growth of IoT technology in Insurtech.

By Services Analysis

The managed services segment accounted for more than 36% of all revenue. By combining expertise and talent with the latest technologies, managed services providers can offer insurers a gradual gateway to transformation. Suppliers of overseen administrations can offer guarantors a way to make a difference by offering a pathway to change that combines mastery and ability with innovative ideas.

Suppliers of overseen administrations can also offer the best cycles, rehearsals, and administrative contemplations for guarantors. Insurers also get the best practices, processes, and regulatory considerations from managed services providers. Managed services allow insurers to tackle challenges and opportunities in IT and operations. Managed services have become a growth opportunity for insurers as they recognize and embrace the benefits of better business models.

Over the forecast period, the support and maintenance segment will experience the greatest growth. Insurance companies are increasingly adopting advanced technologies and distributing through more channels, which is why the support and maintenance sector has seen a significant increase in growth. Insurance agencies are increasingly embracing cutting-edge innovations and distributing them through more channels.

This has led to an increase in the support and upkeep segment. Many insurance agencies around the world are focusing on delivering innovative and customized heritage programming to specific needs. Many insurance companies worldwide are investing in advanced technology and adapting legacy software products to meet specific requirements. This will likely drive demand for maintenance and support services around the world.

End-User Analysis

The BFSI segment was the dominant market with a large global revenue share. BFSI companies are increasingly adopting Insurtech solutions to improve their business efficiency. The increasing number of connected devices within the BFSI industry generates a lot of data. Insurance agencies have realized that such information can improve administration, increase costs, gain knowledge, and raise incomes. The increasing penetration of smartphones worldwide is expected to increase the demand for Insurtech solutions within the BFSI sector.

Over the forecast period, the fastest-growing segment will be healthcare. The rising digitization of the insurance industry will influence Insurtech solutions for healthcare. A growing number of devices means that healthcare organizations must be able to monitor, manage, and maintain their data effectively. In addition, customers are increasingly digitizing their lives, which has increased the need for better and easier access to insurance technology services. The segment is expected to grow due to life and health insurance companies increased use of blockchain technology.

Telematics will play an increasingly important role in pricing and underwriting in the automotive segment as these systems become more advanced. As more people rent or lease cars, insurance’s nature is changing. As manufacturers act as a distribution platform, this will likely include auto coverage. In many cities, mobility as a service (MAAS) is becoming more popular. This is where a car is used as a service. The way to a profitable automobile business is not in the race for the bottom.

It’s likely to be in creating the auto insurance ecosystem that begins at the car’s dashboard. Insurers should also consider this as a potential point of inflection. Automakers can take control of the value chain if they don’t have an easy-to-use engagement point with consumers (the dashboard). In the meantime, insurers might have to accept that they will be a part of the new ecosystem where automakers and their distribution channels are the sales platform that will help grow the Insurtech market’s automotive segment.

Key Market Segments

By Type

- Auto

- Business

- Health

- Home

- Specialty

- Travel

- Other Types

By Deployment

- On-Premise

- Cloud-Based

By Technology

- Blockchain

- Cloud Computing

- IoT

- Machine Learning

- Robo Advisory

- Other Technologies

By Services

- Consulting

- Support & Maintenance

- Managed Services

By End-User

- Automotive

- BFSI

- Government

- Healthcare

- Manufacturing

- Retail

- Transportation

- Other End-Users

Driving Factors

Innovative Solutions and Rising Awareness About Insurance are Driving the Growth of the Insurtech Market

Moving plans of action are driving the Insurtech deals. Insurtech companies use innovative solutions to scale their businesses and create product offerings that rely on specialty client interests. This is expected to increase Insurtech market growth and stimulate interest in Insurtech arrangements. However, various protection area regulations and security concerns limit Insurtech market expansion. Nevertheless, there are many opportunities for Insurtech solutions to expand and foster the Insurtech market due to rising interest in Insurtech arrangements in developing economies, particularly in emerging economies such as South Korea, China, India, and Singapore.

The increasing number of protection claims is complementing market development. Individuals around the globe have a wide range of protection claims, including auto, life, and home. According to a report, Americans want more security in 2021. Insurance agencies invest in advanced innovations to reduce functional expenses and improve the client experience. Computerized innovations can be used to understand client needs and adjust their contributions to meet changing client requirements.

According to EIS Group, an insurance company, the majority of the agencies that were studied increased their interest in computerized foundations in 2021, according to a report. Blockchain innovation is attracting the attention of insurance agencies around the globe due to its benefits, such as expense investment funds, faster installments, and misrepresentation relief. Insurance agencies use blockchain innovation to make distributed models, as well as for Know Your Customer (KYC) and Anti-illegal Tax Avoidance (AML).

The increased availability of transactional data has increased the adoption of data analytics in insurance underwriting to reduce risk, reduce costs, optimize profits, and provide improved customer service and customized solutions. Data analytics trends, such as customer analytics, marketing analytics, etc., enable businesses to improve operational efficiency and profits while providing personalized customer solutions. In addition, increased adoption of artificial intelligence will simplify and improve onboarding and customer service, claims processing, fraud prevention, and anti-money laundering.

Restraining Factors

High Cost and Different Laws are Hindering the Insurtech Market

High investment costs hinder global market growth in insurance technology. As a result, insurance companies face new challenges when selling products that use the most advanced technology. This requires extensive training for employees of insurance companies on advanced technology. In addition, insurance company employees must undergo retraining to provide products that meet the client’s needs.

Insurance companies must invest in training insurance agents and brokers. Many insurance companies have begun integrating different products and services with advanced technology through banks and agents. Before vendors or startups invest, they need to know the path and outcome of their research project. The result and the path might not be obvious at the start of projects. Commercialization of technology is another issue. Despite having superior technology and product plans, many companies fail to meet customer demands. These factors will limit market growth over the forecast period.

Different laws have different norms and regulations. Financial centers take a more coordinated approach to regulation. As a result, Insurtech companies face difficulty in developing Insurtech solutions that comply with multiple regulations, such as GDPR and MiFID II.

This can lead to inter-regulation conflict. This hinders the growth of the Insurtech industry. For example, the National Association of Insurance Commissioners oversees and regulates insurance businesses in the United States. In Europe, MiFID 2 requirements apply to all insurance companies under its control. This is a major factor in the expansion of the Insurtech market and the sale of Insurtech solutions.

Growth Opportunity

Innovative Developments are Creating Many Opportunities in the Insurtech Market.

Insurtech arrangements are gaining popularity as it raises buyer expectations, increase buying amounts, upgrade direction, and protect arranging using AI and man-made consciousness and distributed computing. Moreover, deals in Insurtech arrangements are growing because of various hearty innovations such as AI, AI blockchain, and distributed computing, which offer continuous surveillance and checking of protected action for certain organizations.

This development is being driven primarily by full-service providers Metromile, Root, Lemonade, and several smaller businesses. This unique incident shows how Insurtech is gaining momentum with clients and growing. The digital environment has facilitated this expansion, which has led to increased mobility, travel, and home coverage options. As a result, many industry groups are keen to collaborate with Insurtech in order to reap the benefits of this mutually beneficial environment.

Latest Trends

While Insurtech needs to gain market share and show product market fit, they are keen to demonstrate better unit economics as well as combined ratios. In 2023, the focus will not be on every customer but on acquiring the right ones. Insurtech and VC have learned a lot about adverse selection over the past few years. Next year, expect to see better customer acquisition strategies. Whereas Insurtech 1.0 used IoT primarily as a marketing tool, 2.0 leverages IoT across a range of insurance lines, especially specialized commercial lines, with a real impact on underwriting, claims, and claims management.

Although AI models can be a powerful tool for internal insight, regulators remain hesitant about black box models being used as a way to price or segment risk. Unexplainable pricing decisions can cause confusion and friction between customers and agents. You are at risk of being adversely selected if you cannot explain your value proposition beyond the price. Insurtechs must realize that models are only as good as the quality and uniqueness of their data.

All those who predicted their eventual disintermediation a few years ago are now aware of the resiliency and resilience of the agent channel. Insurtechs are now more open to working with agents than those around them. Tech-forward agencies have responded by being more open to this. Insurtechs will benefit from strong agency relationships that provide predictable unit economics. Both parties will also collaborate to find novel ways to distribute their products by 2023.

Regional Analysis

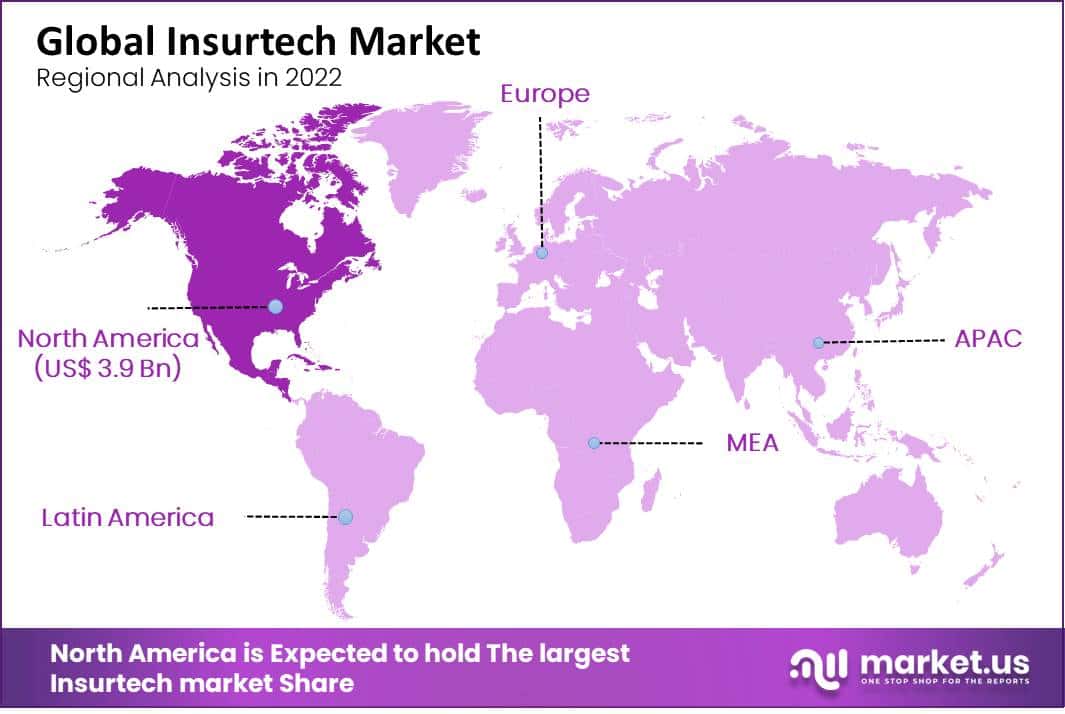

North America was the dominant market for Insurtech, accounting for 33.6% of global revenue. Due to increasing insurance-related product purchases, the region is seeing an increase in the adoption of Insurtech products. These solutions also offer flexible and customizable property and health insurance plans. Market growth is also being driven by the increasing number of startups in Insurtech in the region.

Asia Pacific will be the fastest-growing regional market during the forecast period. Due to the presence in Asia Pacific of many emerging economies and financial centers such as India, and Singapore, significant growth is expected. The region’s insurance service providers are striving to offer affordable premium plans. The growth of the region’s market will also be driven by the increasing penetration of smartphones in Asia Pacific countries.

Key Regions and Countries Covered in this Report:

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

This market is fragmented and characterized by large numbers of small players catering to both life- and non-life insurance markets. To strengthen their market position, market players focus on partnerships. For example, in November 2021, Heritage Insurance Holdings Inc., a property- and casualty insurer, announced its partnership with Slide, an Insurtech P&C company. The partnership would allow Slide to leverage the capabilities of the former company to improve rating and underwriting decisions.

Various regulations restrict vendors’ ability to be creative on the market. But, they have no reason to experiment in the market due to high competition. Market players have created global supply chains through technological data communication and digitization advances. Insurance companies can benefit from the ability of Insurtech companies to innovate in the insurance sector by developing new products and solutions.

Top Market Leaders

- Damco Group

- DXC Technology Company

- KFin Technologies

- Majesco

- Oscar Insurance

- OutSystems

- Quantemplate

- Shift Technology

- Trov Insurance Solutions LLC

- Wipro Limited

- Zhongan Insurance

- Other Key Players

Recent Developments

1. Damco Group:

- February 2023: Partnered with insurtech platform “Covera Health” to offer integrated insurance administration solutions for health insurers.

- June 2023: Launched “Damco CONNECT,” a digital platform for streamlining policy administration and customer interactions in the insurance sector.

- October 2023: Announced a cloud-based solution for automating claims processing and improving efficiency for insurance companies.

2. DXC Technology Company:

- March 2023: Acquired “Logicalis,” expanding its capabilities in offering cloud-based solutions for insurance companies.

- July 2023: Partnered with “Guidewire” to offer cloud-based core insurance platform solutions to its clients.

- November 2023: Launched “DXC Digital Insurance Platform,” a suite of integrated solutions for policy management, claims processing, and customer self-service in insurance.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 16.6 Bn |

| Forecast Revenue (2032) | US$ 336.5 Bn |

| CAGR (2023-2032) | 41% |

| Base Year for Estimation | 2023 |

| Historic Period | 2016-2022 |

| Forecast Period | 2023-2032 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type – Auto, Business, Health, Home, Speciality, Travel, and Other Types; By Deployment – On-Premise, and Cloud Based; By Technology – Blockchain, Cloud Computing, IoT, Machine Learning, Robo Advisory, and Other Technologies; By Services – Consulting, Support and Maintenance, and Managed Services; By End-User – Automotive, BFSI, Government, Healthcare, Manufacturing, Retail, Transportation, and Other End-Users. |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; the Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Damco Group, DXC Technology Company, Kfin Technologies, Majesco, Oscar Insurance, OutSystems, Quantemplate, Shift Technology, Trov, Insurance Solutions LLC, Wipro Limited, Zhongan Insurance, and Other Key Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

In 2032, the Insurtech Market will reach USD 336.5 billion.

The Insurtech Market is expected to grow at 41.0% CAGR (2023-2032).

Market.US has segmented the Insurtech Market Market by geographic (North America, Europe, APAC, South America, and MEA). By Type, market has been segmented into Auto, Business, Health, Home, Specialty, Travel and Other Types. By Deployment, the market has been further divided into On-Premise and Cloud-Based.

With respect to the Insurtech industry, vendors can expect to leverage greater prospective business opportunities through the Health segment, as this dominate this industry.

Damco Group, DXC Technology Company, KFin Technologies, Majesco, Oscar Insurance, OutSystems, Quantemplate and Other Key Players are the main vendors in this market.