Quick Navigation

Report Overview

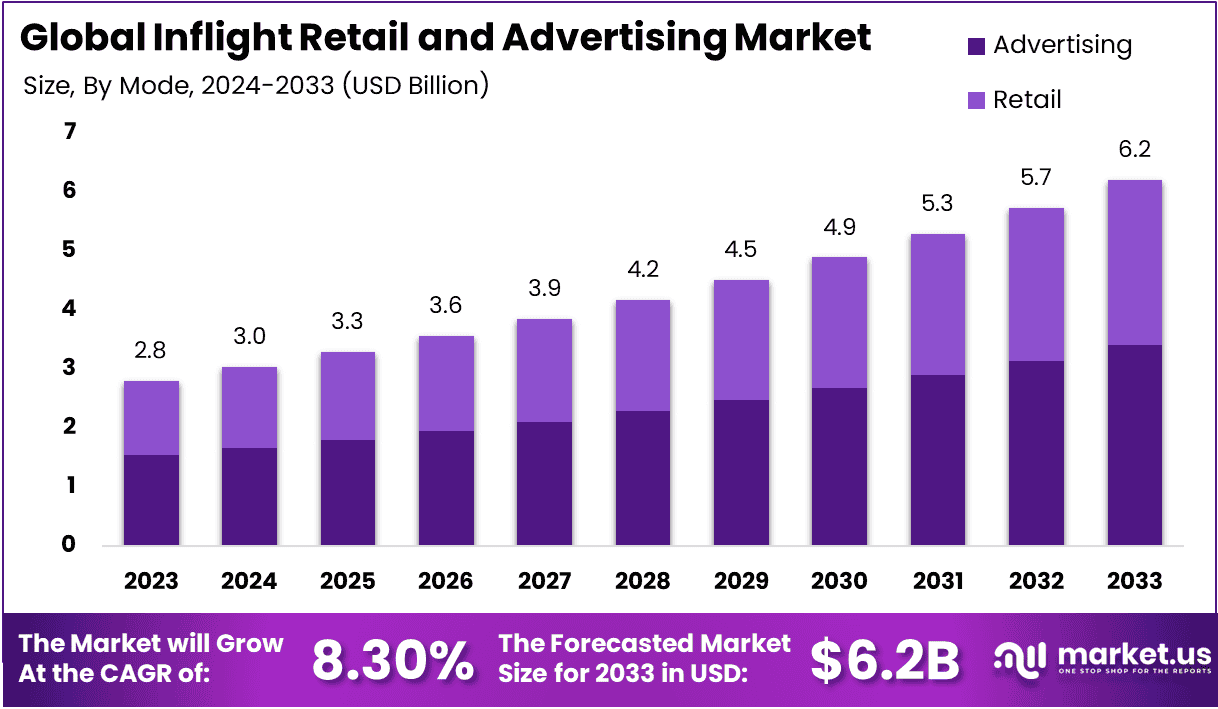

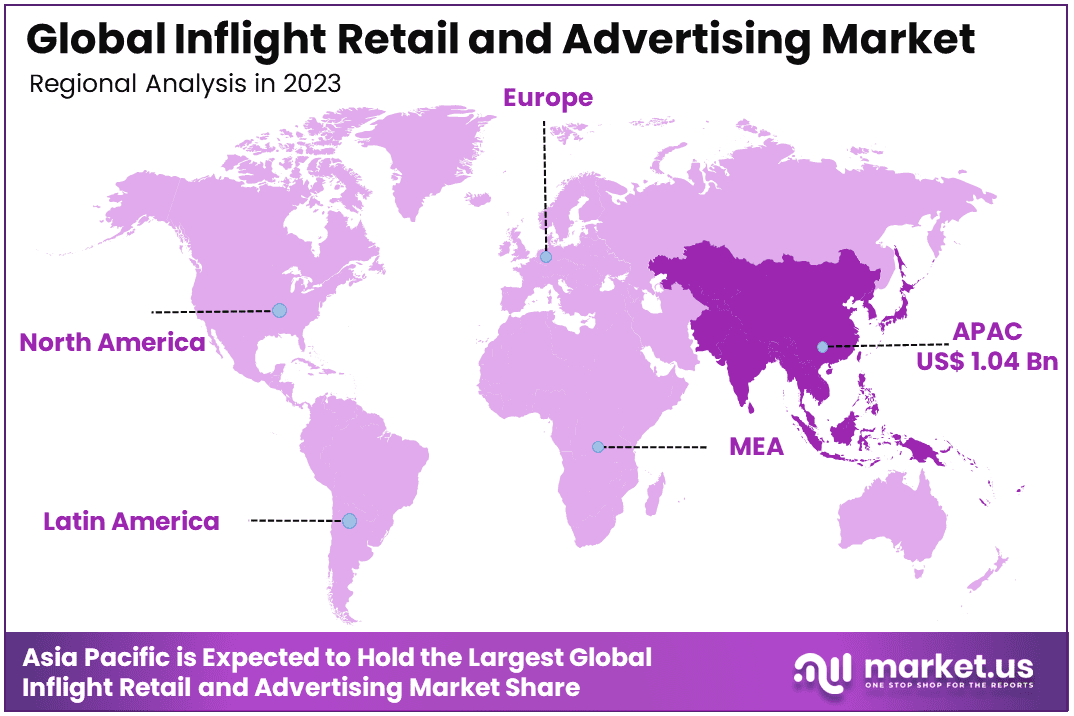

The Global Inflight Retail and Advertising Market is expected to be worth around USD 6.2 Billion By 2033, up from USD 2.8 billion in 2023. It will grow at a CAGR of 8.30% during the forecast period from 2024 to 2033. In 2023, Asia Pacific held a dominant market position, capturing more than a 37.4% share and holding USD 1.04 billion in revenue.

Inflight retail and advertising encompass the sale of products and services, as well as promotional activities within the cabin of an aircraft. This includes the sale of traditional duty-free items, food and beverages, travel accessories, and luxury goods to passengers during a flight.

Additionally, airlines partner with various brands to display advertisements on in-flight entertainment systems, magazines, or even through on-demand videos and Wi-Fi-enabled platforms. The primary goal is to create an additional revenue stream for airlines while enhancing the overall passenger experience. In recent years, inflight retail has evolved, integrating digital platforms where passengers can purchase products through seatback screens or their smartphones, thus enabling a more interactive shopping experience.

Inflight advertising, on the other hand, utilizes technologies such as targeted ads based on passenger demographics, preferences, and even travel destinations. With the growing demand for personalized experiences, airlines are increasingly using data analytics to offer more tailored promotions to passengers.

This is particularly evident in the rise of dynamic advertising, where the content displayed on entertainment screens adapts to a passenger’s location, time of day, or flight duration. The inflight retail and advertising market is a critical segment within the broader travel and tourism industry, helping airlines diversify revenue sources while fostering stronger customer engagement.

The inflight retail and advertising market has witnessed significant growth due to the increasing number of air passengers and the continuous expansion of airlines’ services. As airlines strive to recover from the impact of the COVID-19 pandemic, the demand for ancillary services such as inflight retail and advertising has surged.

The market benefits from increasing passenger disposable income, as well as advancements in inflight technology that enable a more seamless and personalized shopping and advertising experience. Airlines are now leveraging data-driven solutions to target passengers with relevant product offerings and advertisements, enhancing the potential for increased conversion rates.

Market demand is further driven by the shift towards digitalization, where inflight sales and advertising are increasingly moving online. Many airlines are now offering wireless internet connectivity on flights, creating opportunities for digital advertising and e-commerce.

Additionally, partnerships with major retail brands and the integration of loyalty programs are fueling the growth of the inflight retail sector. With global air travel set to increase in the coming years, the inflight retail and advertising market is expected to experience substantial growth, particularly in emerging markets such as Asia-Pacific, where the rising middle class is driving demand for both air travel and premium inflight services.

Moreover, passengers are increasingly seeking convenience and personalization when flying, leading airlines to invest in advanced technology solutions for inflight shopping and advertising. Personalized product recommendations based on travel data, flight duration, and personal preferences are becoming more common, helping to drive sales and customer satisfaction.

Furthermore, growing collaboration between airlines and major brands for co-branded advertising opportunities is expected to significantly contribute to the market’s expansion. With an increasing number of airlines embracing these new models, the market is poised for continued growth.

There are several key opportunities within the inflight retail and advertising market. One of the most significant is the potential for airlines to enhance their digital presence by integrating e-commerce platforms into inflight entertainment systems.

This allows passengers to browse and purchase products in real-time, without interrupting their in-flight experience. The development of loyalty programs that reward passengers for inflight purchases, along with personalized promotions, offers a significant growth opportunity for airlines to foster customer loyalty and increase revenues.

In terms of passenger demographics, the economy class segment is anticipated to grow at the highest rate, driven by its large audience base, which constitutes over 70% of total airline seating capacity, translating to around 60 million economy class passengers per month globally.

The North American region leads this market, accounting for more than 35% of the global share in 2023, largely due to high passenger volumes that reached approximately 800 million travelers in the region that year. The inflight advertising segment is expected to dominate the market, with revenues projected to reach around USD 1.2 billion by 2024.

Additionally, airlines are increasingly leveraging data analytics for personalized marketing strategies, enhancing customer engagement and driving sales growth. Inflight retail and advertising initiatives are supported by technological advancements that facilitate seamless shopping experiences and effective advertising placements, with estimates suggesting that digital advertising spend in this sector could exceed USD 500 million by 2025. Overall, the inflight retail and advertising market reflects a dynamic intersection of technology and consumer engagement within the aviation industry.

Key Takeaways

- Market Growth: The global Inflight Retail and Advertising market is projected to grow from USD 2.8 billion in 2023 to USD 6.2 billion by 2033, reflecting a robust CAGR of 8.30%.

- Dominant Mode: Advertising leads the market with a share of 54.7% in 2023, driven by the increasing use of targeted, digital advertising in flight to engage passengers.

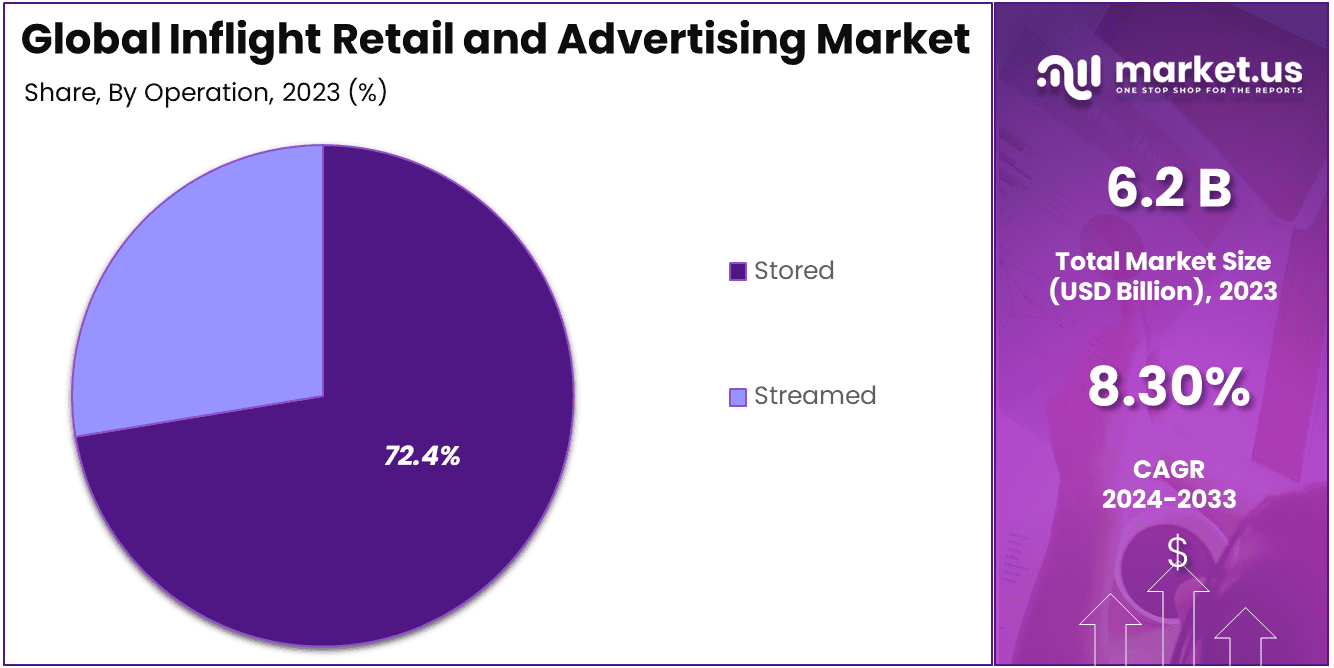

- Pre-loaded Content: The Stored operation segment holds a significant share of 72.4% in 2023, driven by the use of pre-loaded digital content, including ads and product offerings, available to passengers during flights without needing internet connectivity.

- Seat Class Preferences: Economy Class is the largest seat class segment, making up 48.3% of the market, as it accommodates the highest number of passengers, which provides a larger target audience for inflight retail and advertising.

- End-User Dominance: Commercial Aviation is the largest end-user segment, accounting for 57.4% of the market share, as airlines actively utilize inflight retail and advertising to enhance passenger experiences and generate revenue.

- Regional Leadership: The Asia Pacific region dominates the market with a share of 37.4% in 2023, driven by growing air travel, the adoption of advanced digital technologies, and rising consumer demand for personalized inflight services.

- Revenue Growth Drivers: Technological advancements in digital content delivery, personalized advertising, and the expansion of low-cost carriers in emerging markets are key factors propelling the market’s growth.

By Mode

In 2023, the Advertising segment held a dominant market position, capturing more than 54.7% of the total share in the inflight retail and advertising market. This leadership can be attributed to the increasing demand for targeted, personalized advertising that airlines can deliver to passengers during flights.

As digital technologies continue to advance, airlines are increasingly leveraging data-driven advertising platforms to engage passengers in a more relevant and impactful manner. These personalized ad experiences can be delivered via inflight entertainment systems, mobile apps, and seatback screens, providing brands with direct access to a captive audience.

The growth of the advertising segment is also fueled by the rising popularity of digital ads over traditional methods. Digital screens and interactive platforms enable advertisers to run dynamic, location-based, and interest-based advertisements.

The ability to tailor ads based on passenger demographics, flight routes, and personal preferences has proven effective in enhancing engagement, driving higher conversion rates, and increasing ad revenue for airlines. Moreover, with a large portion of passengers spending extended hours on flights, the inflight advertising opportunity is significant, as brands are keen to reach these individuals during their travel time.

Additionally, airlines have recognized the potential for advertising revenue as an important ancillary income stream. With a growing number of airlines adopting modern, digitally-enabled inflight entertainment systems, advertising has become an integral part of their business models. The growing interest from advertisers seeking access to high-value engaged audiences contributes further to the increasing share of the advertising segment within the market.

By Operation

In 2023, the Stored segment held a dominant market position, capturing more than 72.4% of the total share in the inflight retail and advertising market. This strong dominance can be attributed to the ability of airlines to offer content that is readily accessible without the need for a constant internet connection. Stored content, which includes pre-loaded videos, advertisements, and other digital media, is delivered via seatback screens or personal devices, providing a seamless and uninterrupted experience for passengers throughout the flight.

The Stored segment is particularly advantageous for airlines operating on long-haul or remote routes, where internet connectivity may be limited or unreliable. By offering stored content, airlines can ensure that passengers have access to entertainment, information, and targeted advertisements regardless of their location or the quality of in-flight connectivity. Additionally, the ability to pre-load content helps airlines manage bandwidth and ensure smooth operations, without the risk of service disruptions that can sometimes occur with streamed content.

Another key driver for the dominance of the Stored segment is its cost-effectiveness. With the infrastructure for storing content already in place, airlines can avoid the costs associated with high-bandwidth data transmission required for streaming services.

Stored content allows airlines to cater to a wide range of passengers with minimal overhead. Furthermore, advertisers can tailor their messages in stored content, making it highly effective for inflight campaigns. This pre-loaded advertising can be curated to target specific passenger demographics, enhancing the relevance and effectiveness of the ads.

By Seat Class

In 2023, the Economy Class segment held a dominant market position, capturing more than 48.3% of the total share in the inflight retail and advertising market. This segment’s leading position is primarily driven by the sheer volume of passengers traveling in economy class on both domestic and international flights. Economy class accounts for the largest proportion of seats on most aircraft, which directly translates into a higher number of potential touchpoints for inflight retail and advertising content.

The Economy Class segment’s dominance is also driven by its broad demographic reach. Passengers in economy class tend to represent a diverse cross-section of travelers, including families, business travelers on a budget, and leisure passengers.

As a result, advertisers and retailers find this segment particularly attractive for targeted marketing campaigns. Airlines benefit from this large and varied audience by offering a range of advertising opportunities, including promotions, product placements, and video ads, which can appeal to different consumer groups within the same flight.

Furthermore, the affordability of economy-class tickets means that it remains the most popular choice for many travelers. As air travel continues to grow, particularly in emerging markets, the demand for economy-class seats is expected to rise, further boosting the potential for inflight retail and advertising in this segment. This consistent demand provides advertisers with a reliable channel for reaching large numbers of passengers regularly.

By End-User

In 2023, the Commercial Aviation segment held a dominant market position, capturing more than 57.4% of the total share in the inflight retail and advertising market. This dominance is primarily driven by the massive scale of commercial aviation operations worldwide. Commercial airlines cater to a broad and diverse passenger base, offering significant reach for both retail and advertising activities.

With millions of passengers flying daily across short-haul, medium-haul, and long-haul routes, commercial aviation represents a large, untapped market for brands looking to engage with a wide range of consumers.

The sector’s extensive network of routes and its high passenger volume give commercial aviation a unique advantage. Airlines in this segment operate on a larger scale, with numerous flights per day, compared to business aviation, thus providing more opportunities for advertisers to target passengers across multiple touchpoints, such as in-flight magazines, digital screens, and Wi-Fi-enabled services.

The large passenger base further increases the attractiveness of commercial airlines as a platform for targeted marketing and inflight retail sales. Moreover, commercial airlines frequently offer a wide variety of services, including duty-free shopping, food and beverages, and entertainment options, providing advertisers with multiple avenues to promote products and services to passengers.

In addition, the rising popularity of low-cost carriers has further boosted the commercial aviation segment. These carriers are responsible for a significant share of the global air travel market, particularly in emerging regions, where increasing middle-class populations are driving air travel demand.

The ability to reach an increasingly broad demographic, including value-conscious travelers, has made commercial aviation a key player in the inflight retail and advertising space. Furthermore, with advancements in digital advertising technologies, such as personalized content delivery and in-flight entertainment systems, the effectiveness of advertising campaigns in commercial aviation continues to grow.

Key Market Segments

By Mode

- Advertising

- Retail

By Operation

- Stored

- Streamed

By Seat Class

- First Class

- Business Class

- Economy Class

- Premium Economy Class

By End-User

- Commercial Aviation

- Business Aviation

Driving Factors

Increasing Adoption of In-Flight Entertainment Systems

The growth of the inflight retail and advertising market is significantly driven by the increasing adoption of in-flight entertainment systems (IFE) across airlines. With the rise in passenger demand for enhanced in-flight experiences, airlines have been investing in advanced IFE systems that offer passengers a variety of entertainment options, including movies, TV shows, games, and internet access.

These systems have become a key platform for inflight advertising, allowing airlines to deliver personalized content and advertisements to passengers in real-time. The integration of digital advertising in IFE systems has opened new revenue streams for airlines, enabling them to partner with brands and advertisers to showcase their products and services.

In addition to traditional advertising, IFE systems are being enhanced with interactive features such as touch screens, personalized recommendations, and digital coupons. This allows airlines to engage passengers more effectively, promoting retail products such as duty-free items, food, beverages, and other services.

As passengers increasingly expect connectivity during flights, the demand for these advanced entertainment and advertising systems is expected to continue growing. The ability to offer a seamless and engaging digital experience has proven to be a critical driver of the inflight retail and advertising market, contributing to both increased passenger satisfaction and higher in-flight sales.

Moreover, the rising trend of business travelers seeking enhanced in-flight experiences further supports the growth of IFE systems. Airlines that offer superior IFE services can differentiate themselves in a competitive market, attracting both leisure and business travelers.

As these systems become more sophisticated, airlines can enhance passenger engagement through targeted advertisements based on passenger preferences, travel behavior, and purchase history. This trend not only improves the overall travel experience but also offers lucrative opportunities for advertisers to reach a captive audience during flights, making IFE systems a pivotal driver of the inflight retail and advertising market’s growth.

Restraining Factors

Regulatory and Compliance Challenges

Despite the promising growth prospects, the inflight retail and advertising market faces significant regulatory and compliance challenges. Airlines and advertisers must navigate a complex web of regulations concerning advertising content, privacy protection, and consumer rights, particularly when operating across different countries with varying legal frameworks.

Regulatory bodies in many regions have strict rules regarding the types of content that can be displayed during flights, especially in the case of targeted digital advertisements. In some regions, regulations surrounding the collection of consumer data for personalized advertising also place limitations on how airlines and advertisers can operate.

For example, in the European Union, the General Data Protection Regulation (GDPR) imposes stringent rules on how customer data is collected, stored, and used for advertising purposes. Airlines that serve European routes must ensure compliance with these regulations, which may limit their ability to collect passenger data for targeted advertising.

Additionally, there are concerns about data privacy and the potential misuse of personal information, which can lead to passenger resistance towards personalized ads. The complex regulatory environment, combined with the potential for hefty fines for non-compliance, poses a challenge for both airlines and advertisers as they look to capitalize on the inflight retail and advertising market.

Furthermore, some countries have limitations on the type of products and services that can be marketed through inflight channels, especially when it comes to age-restricted items such as alcohol, tobacco, or gambling. Airlines need to carefully tailor their advertising campaigns to meet these restrictions while still generating revenue from in-flight retail and advertising. Navigating these regulatory hurdles requires significant investment in compliance and legal expertise, which can slow down the growth of the inflight retail and advertising market.

Growth Opportunities

Expansion of Low-Cost Carriers

The rise of low-cost carriers (LCCs) presents a significant opportunity for growth in the inflight retail and advertising market. These airlines have become an integral part of the global aviation landscape, particularly in emerging economies where air travel is becoming increasingly affordable. LCCs typically operate on a point-to-point model and offer competitive ticket prices by reducing costs associated with in-flight services, including meals and entertainment. However, they are also leveraging inflight retail and advertising as a key strategy to offset low ticket prices and generate additional revenue.

The potential for in-flight retail and advertising on LCCs is considerable. Unlike full-service carriers, which already have well-established business models for inflight retail and advertising, LCCs often rely on ancillary services like food, beverages, and duty-free sales to generate revenue.

By incorporating more sophisticated advertising and digital retail platforms, LCCs can further monetize their inflight services. This is especially true as passengers increasingly demand in-flight connectivity and entertainment options, providing new avenues for airlines to engage with passengers and advertisers.

In addition, the rising number of budget-conscious travelers in emerging regions, particularly in Asia Pacific, presents an opportunity for LCCs to expand their inflight advertising offerings. Airlines in these regions are focusing on improving passenger experience while maintaining cost efficiency, creating a perfect environment for integrating targeted advertising campaigns. With LCCs rapidly increasing their market share in both domestic and international travel, the growth of their inflight retail and advertising services presents a major opportunity for advertisers and brands looking to reach a large, diverse audience of budget travelers.

Challenging Factors

Passenger Experience and Customer Satisfaction

One of the main challenges in the inflight retail and advertising market is maintaining a balance between enhancing passenger experience and avoiding excessive commercialization that may negatively impact customer satisfaction.

While in-flight advertising can be a significant source of revenue for airlines, over-saturation of advertisements or intrusive marketing tactics can detract from the overall passenger experience. Passengers expect a certain level of comfort and relaxation during their flights, and excessive or poorly targeted ads can cause frustration, especially on longer flights.

Furthermore, there is the challenge of creating non-intrusive advertisements that align with passengers’ preferences and interests. While personalized advertising has proven to be effective, airlines need to strike the right balance to avoid irritating passengers. If advertisements are irrelevant or excessive, passengers may develop negative perceptions of the airline and choose competitors in the future. The key challenge for airlines, therefore, lies in effectively integrating advertising without overwhelming passengers.

Additionally, the digital divide poses a challenge in certain markets. Not all passengers have access to in-flight Wi-Fi or entertainment systems, especially on older aircraft or regional routes. Airlines must ensure that their inflight advertising and retail platforms are accessible to all passengers, including those who may not have the necessary technology or internet access to interact with these services. Ensuring a positive experience for all passengers while monetizing inflight advertising requires careful planning and continuous adaptation to passenger needs and preferences.

Growth Factors

The inflight retail and advertising market is experiencing significant growth, largely driven by the increasing demand for additional revenue streams in the aviation sector. Airlines are constantly seeking ways to diversify their income, and inflight retail and advertising provide a lucrative opportunity beyond ticket sales. As airlines adopt advanced in-flight entertainment (IFE) systems, the market for digital advertisements and onboard retail is expanding rapidly.

These systems are evolving into sophisticated platforms that deliver dynamic and personalized content, including advertisements, shopping options, and destination-based promotions. This trend is driven by the growing number of passengers using their devices to access onboard services, creating an ideal environment for airlines to engage with their audience.

The increasing adoption of Wi-Fi connectivity on flights is another key growth factor. With connectivity, passengers can browse products, access targeted advertisements, and make purchases while in the air, enhancing the inflight retail experience. Additionally, the rise of low-cost carriers (LCCs) has also spurred market growth, as these airlines leverage inflight retail and advertising to boost ancillary revenues.

Another growth factor is the desire for brands to reach a captive audience during flights, leading to partnerships between airlines and advertisers. As more airlines upgrade their services and systems, the market for inflight retail and advertising is expected to continue growing at a robust pace.

Emerging Trends

One of the most significant emerging trends in the inflight retail and advertising market is the integration of advanced technologies, particularly Artificial Intelligence (AI) and machine learning. These technologies allow airlines to deliver highly personalized and targeted advertisements to passengers based on their preferences and behavior.

By analyzing passenger data, airlines can tailor the advertising content to specific demographics, significantly increasing the effectiveness of in-flight campaigns. This trend is expected to drive increased revenue for airlines while improving the overall passenger experience by delivering relevant and engaging content.

Another key trend is the rise of interactive, content-rich experiences through in-flight entertainment (IFE) systems. Passengers can now engage with advertisements in more immersive ways, such as through video ads, product demos, and interactive games that offer rewards or discounts for participation.

The growth of mobile and Wi-Fi-enabled devices is also facilitating this trend, as passengers can interact with advertisements directly through their smartphones, tablets, or other personal devices. This creates an opportunity for airlines and advertisers to create more interactive and engaging experiences that resonate with passengers.

Business Benefits

The inflight retail and advertising market offers numerous business benefits for airlines, advertisers, and other stakeholders in the aviation sector. For airlines, inflight retail and advertising represent a significant source of ancillary revenue, which is becoming increasingly important in a highly competitive industry with tight profit margins. By monetizing inflight entertainment systems and onboard services, airlines can tap into a steady stream of income that complements their core ticket sales. This is particularly valuable for low-cost carriers (LCCs), which often rely on ancillary services to maintain profitability.

Additionally, the shift towards personalized advertising and targeted retail offerings allows airlines to enhance passenger satisfaction. By delivering tailored content and promotions that are relevant to individual passengers, airlines can improve the customer experience and foster brand loyalty. Personalized experiences are proven to increase engagement, and satisfied passengers are more likely to return for future flights, creating long-term value for airlines.

Regional Analysis

In 2023, Asia Pacific held a dominant market position in the inflight retail and advertising sector, capturing more than a 37.4% share and generating approximately USD 1.04 billion in revenue. The region’s growth can be attributed to the rapid expansion of air travel, particularly in countries like China, India, and Japan, where a rising middle class is increasing passenger volumes.

The strong demand for air travel in this region has created a favorable environment for airlines to capitalize on inflight retail and advertising opportunities. Furthermore, the increasing adoption of digital advertising platforms and inflight entertainment systems among Asia Pacific carriers is boosting the market. As airlines strive to enhance the passenger experience, the integration of personalized retail and advertising offerings is expected to grow, propelling the market forward.

North America is another key region, though it holds a slightly smaller share compared to Asia Pacific. In 2023, North America accounted for a significant share of the market, contributing a robust portion to the overall revenue. The region benefits from a mature aviation infrastructure and a well-established inflight retail and advertising ecosystem.

Many leading airlines in North America have integrated advanced technologies like Wi-Fi and digital displays, providing advertisers with the ability to engage with passengers in real-time. The high level of disposable income among passengers and their willingness to engage with premium retail offerings further strengthens the market dynamics in this region.

Europe is also a prominent player in the inflight retail and advertising market, with airlines continually improving the quality of in-flight services. The growing emphasis on passenger comfort and convenience has led to a rise in inflight retail offerings, while advanced digital platforms allow for targeted advertising. The region’s high number of international flights also contributes to a wide-reaching and diverse audience for advertisers.

In Latin America, while smaller in comparison to the leading regions, the inflight retail and advertising market is experiencing steady growth. The increase in air traffic, particularly in Brazil and Mexico, is driving demand for better onboard services and retail offerings. Similarly, the Middle East and Africa are witnessing gradual market growth, with airlines investing in premium in-flight services as they look to cater to high-net-worth passengers traveling long distances.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

Panasonic Avionics Corporation has been a key player in the inflight retail and advertising market, consistently strengthening its position through strategic partnerships and technology innovations. In 2023, Panasonic Avionics expanded its offerings by integrating cutting-edge inflight entertainment and advertising solutions, aimed at enhancing the passenger experience and providing targeted advertising opportunities.

The company’s recent acquisition of Boeing’s Inflight Connectivity business in 2022, valued at approximately USD 3.5 billion, further bolstered its ability to deliver high-speed internet and integrated advertising platforms to airlines globally. With more than 100 airline customers and a broad reach across 160+ countries, the company’s commitment to creating seamless connectivity for both passengers and advertisers solidifies its leadership position in the market.

Viasat, Inc., a leading player in satellite communications and inflight connectivity, has made notable strides in the inflight retail and advertising space with its cutting-edge satellite systems and data solutions. In 2023, Viasat partnered with major airlines to offer enhanced inflight internet services, allowing for more interactive and engaging advertising formats.

The company’s focus on innovation in internet connectivity has positioned Viasat as a crucial enabler for the future of inflight retail and advertising, creating new opportunities for targeted, personalized advertising that maximizes passenger engagement. Viasat’s revenue from inflight connectivity services is expected to exceed USD 1 billion by 2025, showcasing its growing presence in the market.

IMM International, known for its inflight advertising solutions, has been making significant advancements in delivering premium advertising and retail offerings to airlines. In 2023, IMM launched a new in-seat advertising platform, allowing brands to target passengers with tailored messages throughout their flight experience.

IMM’s partnerships with major global airlines, such as Lufthansa and Emirates, to provide tailored, interactive content across the inflight entertainment system have helped solidify its role in shaping the inflight retail and advertising landscape. With a growing portfolio of 50+ airline clients and a continued focus on innovation, IMM International is poised to expand its market share as airlines increasingly look to leverage inflight advertising to boost revenue. IMM’s projected annual revenue growth in the inflight advertising segment is around 15%, reflecting strong market demand for its services.

Top Key Players in the Market

- Panasonic Avionics Corporation

- Viasat, Inc

- IMM International

- Thales

- Collins Aerospace

- Anuvu

- EAM

- Inmarsat

Recent Developments

- In February 2024, Panasonic Avionics Corporation launched its next-generation inflight advertising platform, integrating AI-powered personalized advertising across its inflight entertainment systems.

- In January 2024, Viasat, Inc. partnered with JetBlue Airways to roll out high-speed satellite connectivity on all long-haul flights, enabling more interactive and immersive advertising opportunities.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 2.8 Bn |

| Forecast Revenue (2033) | USD 6.2 Bn |

| CAGR (2024-2033) | 8.30% |

| Largest Market | Asia Pacific |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Mode (Advertising, Retail), By Operation (Stored, Streamed), By Seat Class (First Class, Business Class, Economy Class, Premium Economy Class), By End-User (Commercial Aviation, Business Aviation) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Panasonic Avionics Corporation, Viasat, Inc., IMM International, Thales, Collins Aerospace, Anuvu, EAM, Inmarsat |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |