Global Industrial And Institutional Cleaning Chemicals Market Size, Share, And Industry Analysis Report By Raw Material (Surfactant, Chlor-alkali, Solvents, Phosphates, Biocides, Others), By Product (General Purpose Cleaners, Disinfectants And Sanitizers, Others), By End-use (Commercial, Manufacturing), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180272

- Number of Pages: 203

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

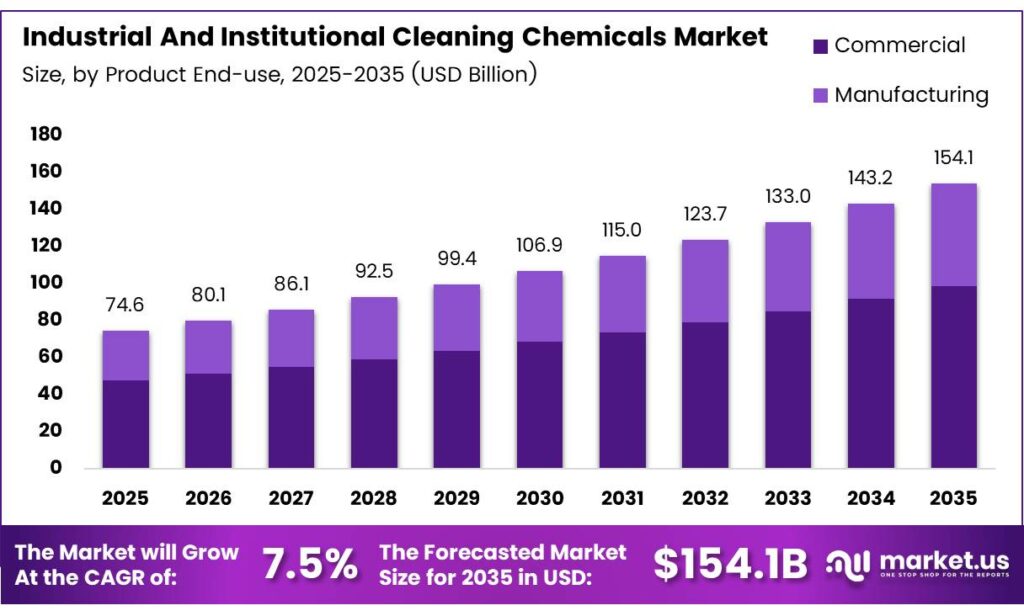

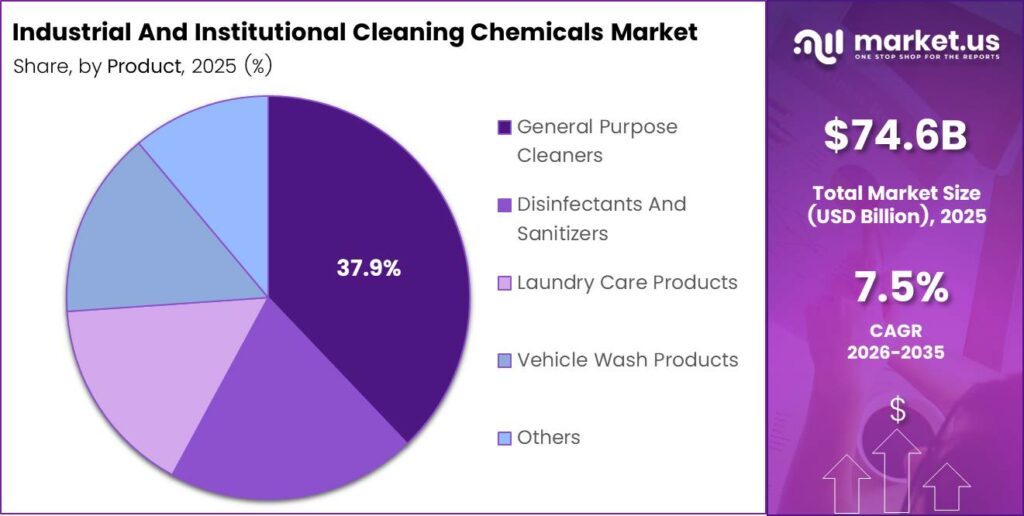

The Global Industrial and Institutional Cleaning Chemicals Market size is expected to be worth around USD 154.1 billion by 2035 from USD 74.6 billion in 2025, growing at a CAGR of 7.5% during the forecast period 2026 to 2035.

The industrial and institutional cleaning chemicals market covers a wide range of chemical formulations used in commercial, healthcare, food service, and manufacturing environments. These products include disinfectants, surfactants, general-purpose cleaners, and laundry care solutions. Consequently, they serve critical roles in maintaining hygiene and regulatory compliance across diverse sectors.

Market growth reflects rising global awareness of sanitation standards. Businesses across healthcare, hospitality, and food processing sectors demand higher-performance cleaning solutions. Moreover, stricter regulatory frameworks governing food safety and pharmaceutical cleanliness drive procurement of specialized formulations across institutional and industrial channels.

- The United States imports of soap and surface-active products reached $618,054.73K and 231,356,000 kg in 2024. This positions the U.S. as the largest importer by both value and volume, underscoring robust domestic demand for cleaning chemical raw materials and formulations.

- The European Union exported $133,855.87K and 52,200,100 kg of soap and surface-active products in 2024. This export volume reflects the EU’s strong regional production base for cleaning-related surfactant preparations used across institutional markets.

Urbanization continues to fuel demand for institutional cleaning services globally. New commercial buildings, shopping centers, and hospitality complexes require professional cleaning solutions at scale. Additionally, the outsourcing of janitorial services in manufacturing and hospitality sectors creates sustained demand for bulk cleaning chemical supplies.

Key Takeaways

- The Global Industrial and Institutional Cleaning Chemicals Market is valued at USD 74.6 billion in 2025, projected to reach USD 154.1 billion by 2035, growing at a CAGR of 7.5%.

- Surfactants dominate with a 36.7% market share in 2025.

- General Purpose Cleaners hold the leading position with a 37.9% share.

- The Commercial segment leads with a 67.1% market share.

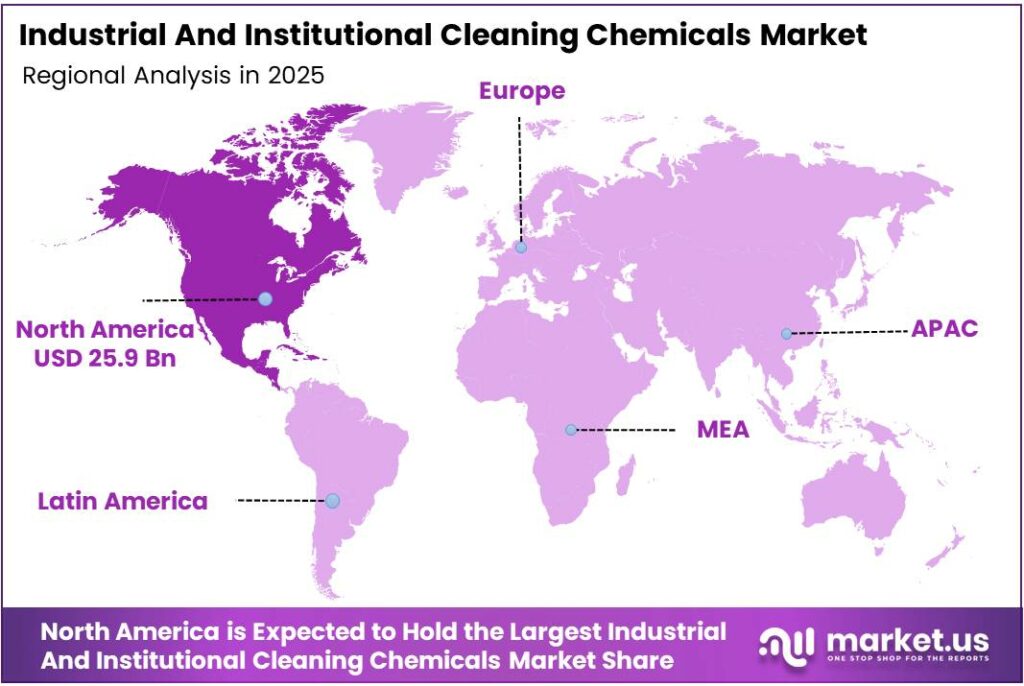

- North America is the dominant region, holding a 34.8% share valued at USD 25.9 billion.

By Raw Material Analysis

Surfactants dominate with 36.7% due to their broad-spectrum cleaning efficacy and wide application across industrial and institutional formulations.

In 2025, Surfactants held a dominant market position in the By Raw Material segment of the Industrial and Institutional Cleaning Chemicals Market, with a 36.7% share. Surfactants serve as the primary active ingredient in most cleaning formulations. Moreover, their ability to reduce surface tension and emulsify oils makes them indispensable in food service, healthcare, and general-purpose cleaning products.

Chlor-alkali products, including caustic soda, soda ash, and chlorine, play a critical supporting role in industrial cleaning chemistry. These compounds enable pH adjustment and disinfection in heavy-duty applications. Additionally, caustic soda remains essential in drain cleaners and degreasers used across food processing and metal fabrication facilities.

Solvents encompass alcohols, hydrocarbons, chlorinated compounds, and ethers used in specialty cleaning applications. They effectively dissolve grease, oils, and adhesives in electronics and industrial maintenance. Consequently, solvent-based cleaners maintain steady demand in manufacturing sectors where aqueous cleaning alone proves insufficient.

Phosphates and Biocides round out the raw material portfolio with targeted functionality. Phosphates enhance detergency and water softening in laundry formulations, while biocides provide antimicrobial protection in healthcare and food-contact surface cleaners. These specialty inputs support premium product segments with high regulatory requirements.

By Product Analysis

General Purpose Cleaners dominate with 37.9% due to their versatile application across commercial, institutional, and light industrial cleaning tasks.

In 2025, General Purpose Cleaners held a dominant market position in the By Product segment of the Industrial and Institutional Cleaning Chemicals Market, with a 37.9% share. These versatile formulations address everyday surface cleaning needs in offices, retail spaces, and institutional buildings. Therefore, their broad applicability and cost-effectiveness ensure consistently high procurement volumes across end-use sectors.

Disinfectants And Sanitizers represent the fastest-growing product category, accelerated by heightened hygiene awareness. Healthcare facilities, food processing plants, and hospitality venues prioritize pathogen-eliminating formulations. Moreover, evolving regulatory mandates require certified disinfection protocols, sustaining demand for hospital-grade and food-safe sanitizer products.

Laundry Care Products serve commercial laundry operations in hotels, hospitals, and institutional settings. These products include detergents, fabric softeners, and stain removers formulated for high-volume industrial washers. Additionally, Vehicle Wash Products address the transportation and logistics sector with specialized degreasers and surface-safe cleaning agents.

By End-Use Analysis

The commercial segment dominates with 67.1% due to the expansive network of food service, healthcare, retail, and institutional building operators requiring consistent cleaning solutions.

In 2025, the Commercial segment held a dominant market position in the By End-Use segment of the Industrial and Institutional Cleaning Chemicals Market, with a 67.1% share. This segment spans food service, retail, healthcare, laundry care, and institutional buildings. Consequently, the sheer volume and diversity of commercial cleaning requirements sustain its leadership position across global markets.

Within the Commercial segment, Food Service and Healthcare sub-segments drive premium product demand. Food service operators require NSF-certified cleaners and sanitizers for compliance. Moreover, healthcare institutions depend on EPA-registered disinfectants to prevent healthcare-associated infections, creating a high-value, recurring demand cycle.

The Manufacturing end-use segment includes food and beverage processing, metal manufacturing, and electronic components cleaning. These applications demand specialized formulations with precise performance characteristics. Additionally, the electronics sub-segment increasingly drives demand for ultra-pure cleaning chemicals as semiconductor fabrication expands globally.

Key Market Segments

By Raw Material

- Surfactant

- Nonionic

- Anionic

- Cationic

- Amphoteric

- Chlor-alkali

- Caustic Soda

- Soda Ash

- Chlorine

- Solvents

- Alcohols

- Hydrocarbons

- Chlorinated Ethers

- Others

- Phosphates

- Biocides

- Others

By Product

- General Purpose Cleaners

- Disinfectants And Sanitizers

- Laundry Care Products

- Vehicle Wash Products

- Others

By End-use

- Commercial

- Food Service

- Retail

- Healthcare

- Laundry Care

- Institutional Buildings

- Others

- Manufacturing

- Food and Beverage Processing

- Metal Manufacturing and Fabrication

- Electronic Components

- Others

Emerging Trends

Sustainability, Smart Technologies, and Premiumization Reshape the Cleaning Chemicals Landscape

The cleaning chemicals industry is transitioning rapidly toward concentrated low-water formulations. Manufacturers develop ultra-concentrated products that reduce packaging waste and transportation emissions. Moreover, these formulations lower the total cost of ownership for institutional buyers, making sustainability a commercial advantage rather than just an environmental commitment.

- Digital technologies reshape how facilities monitor and manage hygiene compliance. Smart dispensing systems, IoT-connected cleaning equipment, and real-time hygiene monitoring platforms gain traction in hospitals and food processing plants. The Hygiene segment delivered +4.2% like-for-like growth, reflecting rising demand for technologically supported cleaning and disinfection solutions globally.

Commercial facility managers increasingly prefer fragrance-enhanced cleaning products that signal cleanliness to occupants and visitors. Additionally, advances in antimicrobial technologies now enable multi-surface pathogen elimination with single-application products. Bosnia and Herzegovina’s domestic production of washing and cleaning preparations reached 20,367,203 kg, reflecting growing output capacity that mirrors rising global demand trends.

Drivers

Regulatory Mandates, Urbanization, and Healthcare Hygiene Standards Drive Sustained Market Growth

Escalating regulatory requirements for food safety and pharmaceutical cleanliness compliance create consistent demand for certified cleaning formulations. Regulatory agencies worldwide mandate documented sanitation protocols in food processing and drug manufacturing facilities. Consequently, institutional buyers invest heavily in approved cleaning systems to maintain certifications and avoid costly compliance failures.

- China exported $974,564.93K and 681,726,000 kg of surface-active cleaning products in 2024, positioning China as the top global exporter. This volume reflects how rapid urbanization and commercial infrastructure growth across emerging economies translate directly into expanding cleaning chemical demand at scale.

Healthcare institutions worldwide heighten their focus on preventing healthcare-associated infections through specialized disinfectants. Hospitals and clinics expand procurement of hospital-grade sanitizers and surface disinfectants. Additionally, the outsourcing of janitorial services in manufacturing and hospitality sectors sustains commercial demand for bulk cleaning chemical supplies across institutional channels.

Restraints

Regulatory Restrictions on Hazardous Chemicals and Labor Cost Pressures Constrain Market Expansion

Stringent government restrictions on hazardous chemical formulations and volatile organic compound emissions present a significant challenge for manufacturers. Formulators must reformulate existing products to meet evolving environmental regulations across multiple jurisdictions. Therefore, compliance costs and development timelines slow innovation cycles and increase operational expenses for cleaning chemical producers.

- Detergents and washing preparations production reached 88,641,987 kg with a sold production value of 211,091 thousand BGN in 2024. However, rising operational costs associated with skilled labor shortages in cleaning applications affect profitability margins. Manufacturers struggle to maintain cost efficiency while meeting both regulatory requirements and customer quality expectations simultaneously.

The transition away from phosphate-based and chlorinated formulations further complicates product development for established manufacturers. Alternative chemistries often carry higher input costs and require new manufacturing infrastructure. Consequently, smaller producers face disproportionate financial burdens when adapting their portfolios to meet tightening environmental and safety standards across global markets.

Growth Factors

Bio-Based Chemistries, Enzyme Technology, and Semiconductor Cleaning Demand Accelerate Market Expansion

Bio-based surfactants and sustainable green cleaning alternatives represent a major growth frontier for the market. Plant-derived ingredients appeal to environmentally conscious institutional buyers in healthcare and food service. Moreover, regulatory incentives in Europe and North America encourage formulators to shift toward renewable raw materials, expanding the addressable market for premium sustainable cleaning products.

- Global Institutional and Specialty segment sales reached $1,367.3 million, reflecting a +6% year-over-year increase. Additionally, Kao Corporation’s Hygiene and Living Care Business posted net sales of 544.3 billion yen in FY 2024, covering laundry detergents and institutional cleaning chemistry. These results confirm that institutional cleaning demand grows robustly across both Western and Asian markets.

Semiconductor and electronics manufacturing creates a high-growth niche requiring ultra-pure cleaning chemistries. The global expansion of chip fabrication facilities drives demand for contamination-free surface preparation solutions. Furthermore, the development of smart automated dispensing systems enables precise chemical dosing, reducing waste and lowering total cost per clean cycle in large-scale industrial operations.

Regional Analysis

North America Dominates the Industrial and Institutional Cleaning Chemicals Market with a Market Share of 34.8%, Valued at USD 25.9 Billion

North America leads the global industrial and institutional cleaning chemicals market, holding a dominant 34.8% share valued at USD 25.9 billion in 2025. The United States drives regional demand through stringent food safety regulations, well-developed healthcare infrastructure, and a mature commercial cleaning services industry. Moreover, high adoption of premium disinfectants and specialty cleaners in healthcare and food processing sustains strong regional revenue growth.

Europe maintains a strong second position in the global market, supported by rigorous environmental and chemical safety regulations. The EU’s REACH framework and VOC emission directives push manufacturers toward greener formulations. Additionally, Germany, France, and the UK represent the largest national markets, with institutional cleaning demand concentrated in healthcare, food processing, and hospitality sectors.

Asia Pacific is the fastest-growing regional market, propelled by rapid urbanization, industrial expansion, and rising hygiene awareness. China dominates regional production and consumption, while India and Southeast Asian nations accelerate demand through expanding healthcare and food processing infrastructure. Consequently, multinational cleaning chemical companies increasingly prioritize capacity investments and distribution partnerships across this high-growth region.

The Middle East and Africa region shows promising growth driven by hospitality sector expansion and rising healthcare investments. Gulf Cooperation Council nations lead regional demand, supported by large hotel complexes and modern healthcare facilities requiring professional-grade cleaning solutions. Therefore, international cleaning chemical suppliers actively expand their distribution networks across key GCC markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Procter and Gamble operates as one of the world’s largest consumer and institutional cleaning product companies. Its professional cleaning division supplies disinfectants, surface cleaners, and laundry care products to healthcare, food service, and hospitality customers. The company leverages deep retail distribution and brand equity to maintain leadership across both consumer and institutional cleaning segments globally.

BASF SE serves as a critical raw material and specialty chemical supplier to the cleaning chemicals industry. The company produces high-performance surfactants, biocides, and functional ingredients used by formulators worldwide. Moreover, BASF’s broad chemical portfolio and innovation pipeline support cleaning product manufacturers in developing more effective and environmentally compliant formulations for institutional and industrial applications.

Clariant focuses on specialty surfactants and functional additives that enhance cleaning efficacy and sustainability. The company’s care chemicals division develops bio-based and biodegradable surfactant solutions for institutional and industrial cleaning markets. Additionally, Clariant’s investment in green chemistry positions it favorably as regulatory pressure and customer sustainability commitments drive demand for cleaner formulation inputs globally.

The Clorox Company, Inc. operates a diversified portfolio of cleaning and disinfection brands targeting both consumer and professional markets. Its CloroxPro and Clorox Healthcare lines supply certified disinfectants and sanitizers to hospitals, food service, and commercial cleaning operations. Reflecting how premium disinfection brand portfolios generate high-value recurring institutional revenue streams across global markets.

Top Key Players in the Market

- Procter and Gamble

- BASF SE

- Clariant

- The Clorox Company, Inc.

- Henkel AG and Co. KGaA

- 3M

- Kimberly-Clark Corporation

- Reckitt Benckiser Group plc

- Croda International PLC

- Albemarle Corporation

Recent Developments

- In 2025, BASF featured a dedicated session for the Home Care and I&I Cleaning industries, focused on integrating sustainability “from molecules to formulations.” BASF launched Trilon G, a new sustainable chelating agent based on GLDA chemistry, specifically for Home Care and I&I Cleaning applications. It improves surfactant efficiency through water softening and advances both performance and sustainability goals.

- In 2025, CloroxPro reported the following recent activity on its professional and investor sites: The company launched Clorox Screen+ Sanitizing Wipes, a new professional-grade product designed to clean and sanitize sensitive electronics. It kills 99.9% of bacteria, removes fingerprints/smudges, and is formulated to avoid damage to delicate surfaces.

Report Scope

Report Features Description Market Value (2025) USD 74.6 Billion Forecast Revenue (2035) USD 154.1 Billion CAGR (2026-2035) 7.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Raw Material (Surfactant (Nonionic, Anionic, Cationic, Amphoteric), Chlor-alkali (Caustic Soda, Soda Ash, Chlorine), Solvents (Alcohols, Hydrocarbons, Chlorinated, Ethers, Others), Phosphates, Biocides, Others), By Product (General Purpose Cleaners, Disinfectants And Sanitizers, Laundry Care Products, Vehicle Wash Products, Others), By End-use (Commercial (Food Service, Retail, Healthcare, Laundry Care, Institutional Buildings, Others), Manufacturing (Food and Beverage Processing, Metal Manufacturing and Fabrication, Electronic Components, Others)) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Procter and Gamble, BASF SE, Clariant, The Clorox Company Inc., Henkel AG and Co. KGaA, 3M, Kimberly-Clark Corporation, Reckitt Benckiser Group plc, Croda International PLC, Albemarle Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Industrial And Institutional Cleaning Chemicals MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Industrial And Institutional Cleaning Chemicals MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Procter and Gamble

- BASF SE

- Clariant

- The Clorox Company, Inc.

- Henkel AG and Co. KGaA

- 3M

- Kimberly-Clark Corporation

- Reckitt Benckiser Group plc

- Croda International PLC

- Albemarle Corporation

Our Clients

- 180272

- March 2026