Quick Navigation

Report Overview

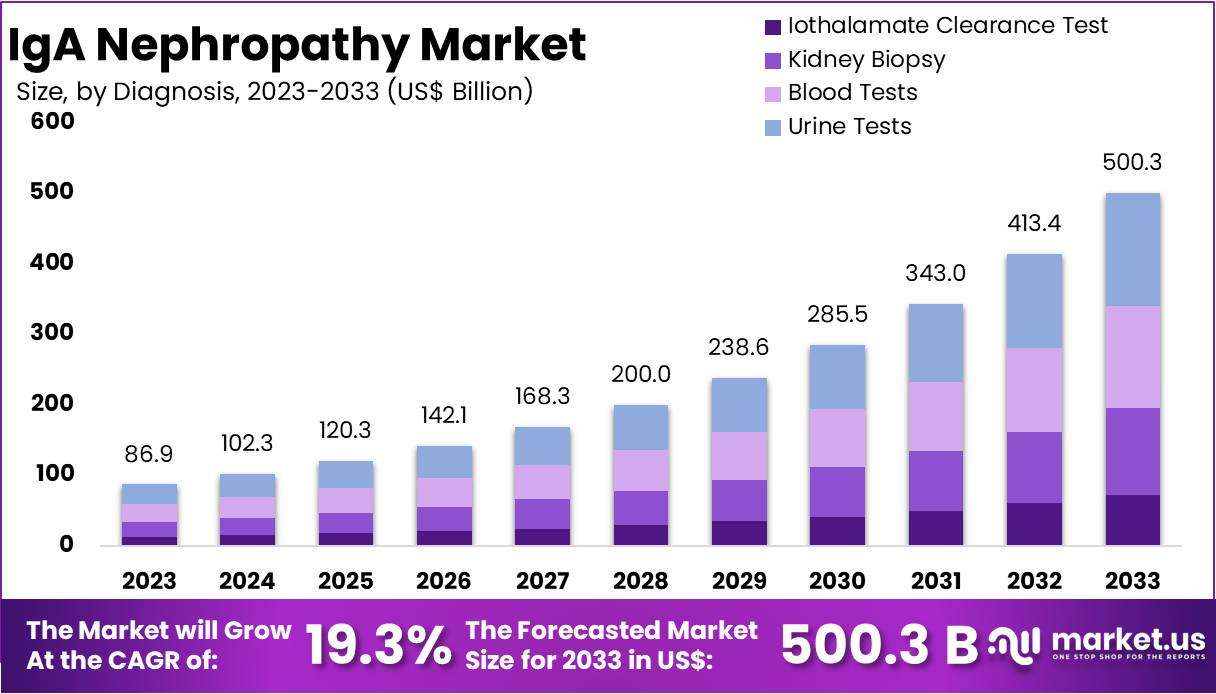

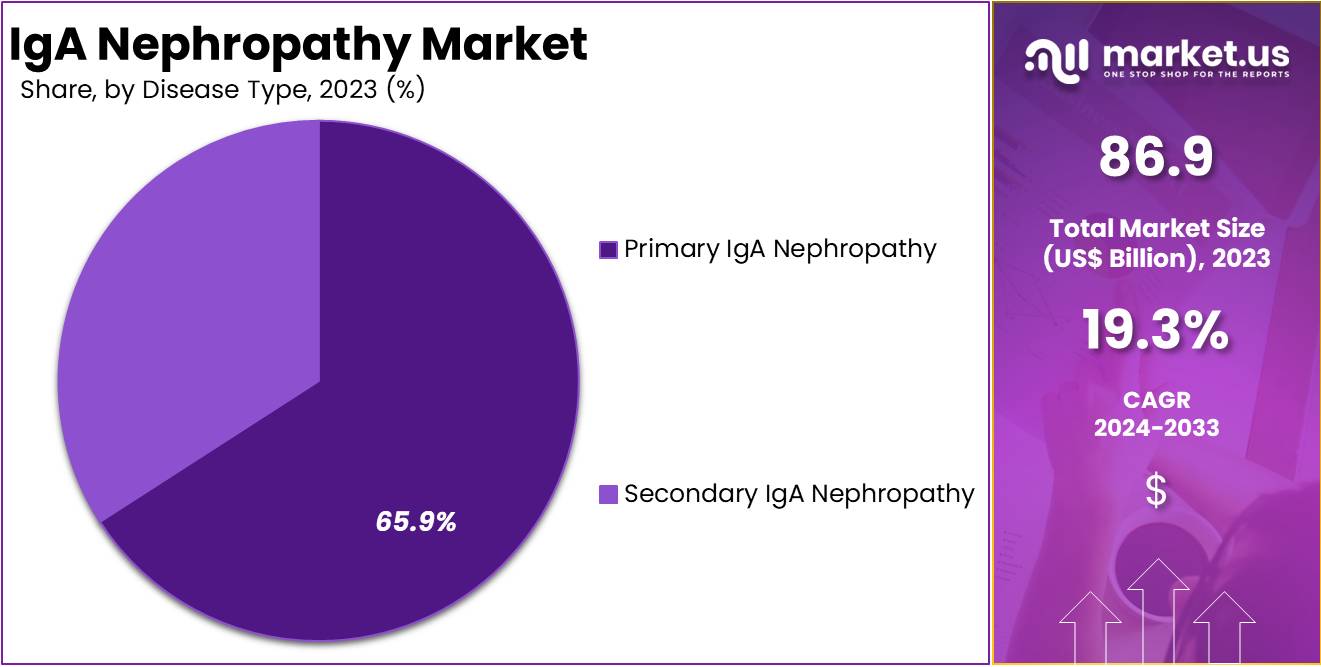

The Global IgA Nephropathy Market size is expected to be worth around US$ 500.3 Billion by 2033, from US$ 86.9 Billion in 2023, growing at a CAGR of 19.3% during the forecast period from 2024 to 2033.

IgA Nephropathy, also known as Berger’s disease, is a kidney disorder that occurs when immunoglobulin A (IgA)-a protein that helps the body fight infections—settles in the kidneys. This leads to inflammation that, over time, can hamper the kidneys’ ability to filter waste from blood. The disease can progress slowly, and while some may live a normal life without much intervention, others might develop end-stage kidney failure.

The IgA Nephropathy Market encompasses the research, development, and distribution of treatments for this chronic kidney condition. The market focuses on managing symptoms, preventing complications, and improving patient outcomes. Treatments range from corticosteroids and immunosuppressants to innovative biological therapies targeting specific immune pathways. As there is no cure for IgA Nephropathy (IgAN), ongoing research into advanced therapies is a critical growth driver in this market.

According to the National Library of Medicine, IgAN is the most common glomerulonephritis globally, with an annual incidence of 2.5 per 100,000 population. Approximately 30% of patients progress to end-stage renal disease (ESRD) within 20 years of diagnosis, requiring dialysis or kidney transplantation. A study by Frontiers in Medicine highlights that IgAN accounts for 40% of native kidney biopsies in Japan, 25% in Europe, and 12% in the USA, showing significant geographical variability.

Recent advancements in understanding the disease’s pathophysiology have fueled the development of targeted therapies. For instance, in February 2023, the FDA granted accelerated approval for sparsentan (brand name Filspari). This dual endothelin and angiotensin II receptor antagonist has demonstrated significant proteinuria reduction and slower kidney function decline compared to standard treatments like irbesartan. Such innovations reflect the market’s potential for growth and improved patient care.

The disease’s progression is linked to abnormal immune reactions, including the deposition of IgA in the glomeruli and interstitial fibrosis. Research identifies genetic factors, such as mutations in the C1GALT1 and C1GALT1C1 genes, contributing to IgAN. However, more than 90% of cases are sporadic, with familial occurrences accounting for fewer than 10%. No specific infectious agents or food hypersensitivity, except in celiac disease cases, have been confirmed as triggers.

Increased awareness and improved diagnostic techniques are enabling earlier detection and treatment, expanding the market’s reach. With rising investments in novel therapies and enhanced understanding of genetic and immune mechanisms, the IgAN market is poised for significant advancements. For example, ongoing research aims to refine treatments further, offering hope for better outcomes in managing this complex disease.

Key Takeaways

- The global IgA nephropathy market is projected to reach US$ 500.3 billion by 2033, up from US$ 86.9 billion in 2023, growing at a 19.3% CAGR.

- Urine tests led the diagnosis segment in 2023, holding a significant 32.1% share of the IgA nephropathy market.

- Primary IgA nephropathy dominated the disease type segment in 2023, capturing over 65.9% of the IgA nephropathy market share.

- Hematuria was the leading condition in the systems segment in 2023, accounting for more than 41.6% of the market.

- Pediatrics held the largest share in the population type segment in 2023, with more than 76.8% of the IgA nephropathy market share.

- Oral administration was the preferred route in 2023, dominating the market with a 63.8% share in IgA nephropathy treatments.

- Hospitals were the primary end users in 2023, capturing a dominant 36.9% share of the IgA nephropathy market.

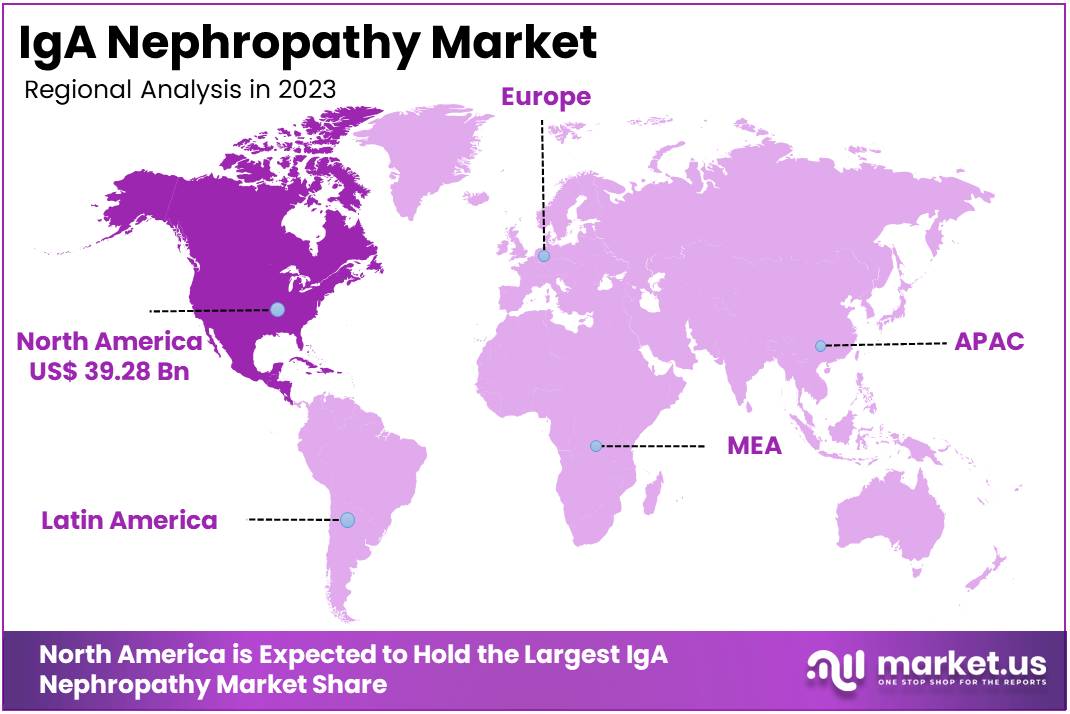

- North America led the regional market in 2023, commanding a 45.2% share with a market value of US$ 39.28 billion.

Diagnosis Analysis

In 2023, Urine Tests held a dominant market position in the Diagnosis Segment of the IgA Nephropathy Market, capturing more than a 32.1% share. This trend highlights their non-invasive nature and ease of use. Healthcare providers prefer urine tests due to their affordability and ability to detect early signs of kidney damage. Their accessibility in primary care settings makes them an essential tool for initial screenings and monitoring disease progression.

Blood tests also contributed significantly to the market share. These tests are vital for identifying abnormalities like high creatinine levels, which indicate impaired kidney function. They are commonly used alongside urine tests to provide a more complete diagnostic picture. The complementary role of blood tests helps physicians confirm and monitor disease stages effectively. Their simplicity and reliability make them a key part of IgA nephropathy diagnosis strategies.

Kidney biopsies, although less common, are crucial for definitive diagnoses in complicated cases. This invasive procedure helps identify IgA deposits in kidney tissues. Meanwhile, Iothalamate clearance tests serve as a precise method for assessing renal function, albeit in specialized settings. The rising incidence of IgA nephropathy is boosting demand for advanced diagnostic tools. Focus on early detection and customized care solutions is expected to drive further growth in this market segment over the coming years.

Diseases Type Analysis

In 2023, Primary IgA Nephropathy held a dominant market position in the Diseases Type segment of the IgA Nephropathy Market. It captured more than a 65.9% share. This leadership is largely due to its higher prevalence compared to other types. The condition, marked by IgA antibody deposits in the kidneys, causes inflammation and long-term damage. Growing awareness and advancements in diagnostic techniques have played a crucial role in its increased identification globally.

Secondary IgA Nephropathy, though less common, is also contributing to the market’s growth. This form often occurs alongside other conditions like liver disease, infections, or autoimmune disorders. Its rising prominence in research and treatment development is expanding its market share. Improved medical understanding and therapeutic interventions are expected to further enhance the segment’s growth. These advancements are creating better opportunities for accurate diagnosis and effective treatment options.

The overall market is witnessing dynamic changes driven by innovative therapies. Targeted treatments focusing on specific disease pathways are improving patient outcomes. This trend is particularly impactful for managing both primary and secondary types of IgA Nephropathy. The increasing emphasis on early detection and personalized care is transforming disease management. As these efforts progress, the market is set to expand further in the coming years.

Systems Analysis

In 2023, Hematuria held a dominant market position in the Systems Segment of the IgA Nephropathy Market, capturing more than a 41.6% share. This dominance is attributed to hematuria’s frequent occurrence as an early symptom of the disease. Medical professionals increasingly rely on its presence for preliminary diagnosis. Greater awareness among patients and healthcare providers about its significance has also boosted its role in the market, solidifying its leading position in the segment.

Proteinuria emerged as the second-largest contributor to the systems segment. Its strong presence is linked to its importance as a marker of disease progression. Healthcare advancements have increased the focus on proteinuria for monitoring the severity of IgA nephropathy. This has led to its growing adoption in clinical practices. As its significance continues to rise, proteinuria remains a key area of focus within the IgA nephropathy market.

Edema and other symptoms, such as hypertension and fatigue, made up the rest of the market share. Edema plays a critical role in later stages of the disease and is closely monitored to assess kidney function decline. While less prominent, these additional systems are gaining attention for their importance in holistic disease evaluation. Improvements in diagnostic tools are expected to enhance their market share. Together, these systems highlight the comprehensive approach taken in managing IgA nephropathy.

Population Type Analysis

In 2023, Pediatrics held a dominant market position in the Population Type Segment of the IgA Nephropathy Market, capturing more than a 76.8% share. This is largely due to the growing recognition of IgA nephropathy in children. Pediatric patients often experience more severe forms of the disease, which increases the demand for treatments specially designed for younger populations. The awareness among healthcare professionals about early diagnosis and treatment options also plays a key role in this dominance.

The adult segment, while smaller, continues to grow steadily. IgA nephropathy is often diagnosed in adults at an older age, which leads to different approaches for treatment. Over time, the prevalence of the disease in adults has been rising. Aging populations and greater awareness of the disease contribute to this upward trend. Although the adult population holds a smaller share, its growth potential in the market remains significant.

The pediatric segment’s lead is expected to persist in the coming years. Ongoing research and development efforts are focused on improving therapies for children. As new, more effective treatments emerge, pediatric patients will likely benefit the most. Meanwhile, the adult segment is also seeing growth, especially as early diagnosis becomes more common. Overall, both segments are likely to expand, driven by advances in treatment and increasing patient awareness.

Route of Administration Analysis

In 2023, Oral held a dominant market position in the Route of Administration Segment of the IgA Nephropathy Market, capturing more than a 63.8% share. The oral route is favored due to its convenience and ease of use. Patients prefer taking oral medications over injectable ones. This preference is driven by the ability to manage treatment at home without requiring medical assistance. As a result, oral therapies see a higher adoption rate for long-term care and management of IgA Nephropathy.

The parenteral route, which includes intravenous and subcutaneous injections, is also growing in the market. However, it holds a smaller share compared to oral treatments. Parenteral administration is typically used for severe cases when oral treatments fail. Although effective, this method requires healthcare professionals for administration. The higher cost and complexity of injections limit the widespread adoption of parenteral therapies for IgA Nephropathy.

Other routes of administration are in the early stages of development. These methods have not gained significant market share yet. However, with ongoing research, new delivery methods could emerge in the future. Still, the oral route remains the dominant choice in the treatment of IgA Nephropathy. Oral therapies are expected to continue leading the market as they offer convenience, cost-effectiveness, and ease of use for patients.

End Users Analysis

In 2023, Hospitals held a dominant market position in the End Users Segment of the IgA Nephropathy Market, capturing more than a 36.9% share. Hospitals are key players in the treatment of IgA Nephropathy. These facilities provide a wide range of services, including advanced diagnostics, specialized care, and continuous monitoring. The infrastructure and expertise in hospitals make them the go-to choice for treating complex kidney conditions, including IgA Nephropathy.

The Oral segment also plays a significant role in treating IgA Nephropathy. Oral medications are frequently prescribed as the first line of treatment. These drugs are convenient for patients, offering ease of administration. The demand for oral treatments continues to grow, as they help patients manage their conditions with less disruption to their daily lives. Oral therapies are an attractive option for many patients in the early stages of the disease.

The Parenteral segment is gaining traction in the IgA Nephropathy treatment market. Parenteral drugs, which are administered through injections, are often used for more severe cases. These therapies are vital for patients who need more immediate or stronger intervention. The growth of this segment is driven by the increasing demand for injectable treatments that offer targeted and effective solutions for managing IgA Nephropathy.

Key Market Segments

By Diagnosis

- Iothalamate Clearance Test

- Kidney Biopsy

- Blood Tests

- Urine Tests

By Diseases Type

- Primary IgA Nephropathy

- Secondary IgA Nephropathy

By Systems

- Hematuria

- Proteinuria

- Edema

- Others

By Population Type

- Pediatrics

- Adults

By Route of Administration

- Oral

- Parenteral

- Others

By End Users

- Hospitals

- Specialty Clinics

- Homecare

- Others

Drivers

Increased Prevalence of Chronic Kidney Diseases

The global rise in chronic kidney diseases is significantly impacting the IgA Nephropathy market. As the prevalence of kidney-related ailments increases, so does the demand for advanced treatments. Improved diagnostic techniques and heightened awareness about kidney health are key factors. These advancements aid in the early detection and management of IgA Nephropathy, thereby enhancing patient outcomes and driving market growth.

Additionally, educational campaigns and better healthcare infrastructure are leading to higher diagnosis rates of IgA Nephropathy. This surge in awareness not only facilitates early detection but also emphasizes the critical need for timely medical interventions. As a result, the market for IgA Nephropathy treatments is expected to experience sustained growth, fueled by an informed population seeking effective solutions.

IgA Nephropathy can progress to severe kidney damage, which may worsen gradually or rapidly. This condition often leads to kidney failure, a life-threatening stage where the kidneys are unable to filter blood effectively. Treatment options at this stage include dialysis or a kidney transplant, highlighting the gravity of advanced IgA Nephropathy.

A 2023 study in the United Kingdom analyzed 2,299 adults and 140 children with IgA Nephropathy, tracking them for an average of 5.9 years. The findings revealed that about 50% of participants experienced kidney failure or death during the study period. The average age of kidney failure onset was 49 years for adults and 27 years for those diagnosed in childhood, underscoring the urgent need for effective treatment strategies.

Restraints

High Cost of Treatment

IgA Nephropathy (IgAN) is the most common primary glomerulonephritis globally, predominantly affecting younger individuals. It involves the deposition of immune complexes with galactose-deficient IgA1 in the kidney’s mesangial area, causing progressive kidney damage. This disease necessitates costly medications and supportive care, which escalate expenses as the condition worsens, potentially requiring dialysis or transplantation.

The financial burden of treating IgAN is significant, particularly in lower-income regions where healthcare access is restricted. According to The Professional Society for Health Economics and Outcomes Research (ISPOR), the annual cost of medications like Nefecon is substantial, with a wholesale acquisition cost of approximately $118 USD per 4 mg unit, amounting to a daily dose cost of about $472 USD. This economic barrier limits patient compliance and effective disease management, perpetuating health disparities.

Advanced treatments such as dialysis and kidney transplantation are resource-intensive. According to a study, the annual cost for hemodialysis in the United States is estimated at $105,600, while peritoneal dialysis costs around $89,226. Kidney transplantation incurs an average expense of $453,703. These high costs contribute to unequal treatment outcomes across different socioeconomic groups, reinforcing a cycle of health inequality.

Opportunities

Advancements in Treatment Options

There is a significant opportunity within the healthcare sector for the development of new therapeutic approaches, particularly in the fields of targeted immunosuppressants and biologics. These innovative treatments promise to enhance the management of various diseases by focusing precisely on affected immune responses. This precision not only aims to improve patient outcomes but also reduces the side effects associated with broader immunosuppressive methods.

The emergence of these advanced therapies could catalyze the creation of new markets. As patients and healthcare providers seek more effective treatment options, the demand for specialized, targeted treatments is likely to increase. This shift towards precision medicine is expected to drive investment and innovation in biopharmaceutical research, further fueling the growth of this sector.

Additionally, by introducing more effective management strategies for chronic conditions, these new therapies have the potential to significantly reduce long-term healthcare costs. Improved disease management leads to fewer hospital visits and a lesser need for complex medical procedures, benefiting both patients and insurance systems. This economic advantage, coupled with enhanced treatment efficacy, positions targeted therapies as a key area of growth in the healthcare market.

Trends

Growing Research in Biomarkers

The growing interest in biomarkers for IgA Nephropathy marks a significant trend in the field of medical research. Biomarkers are biological indicators that can help in early and accurate diagnosis of diseases. In the case of IgA Nephropathy, a chronic kidney disease, identifying specific biomarkers could lead to significant advancements. Researchers are focusing on how these biomarkers can detect the disease earlier than traditional methods, which often rely on symptoms and kidney function tests. This early detection is crucial as it allows for the initiation of treatment before significant kidney damage occurs.

The emphasis on biomarker research is not just about early diagnosis but also enhancing the precision of treatment plans. With specific biomarkers, healthcare providers can tailor treatments to individual patients, increasing the effectiveness of the interventions. This personalized approach can potentially lead to better patient outcomes, less treatment-related side effects, and more efficient use of healthcare resources. As research progresses, the goal is to integrate these biomarkers into routine clinical practice, thereby transforming how IgA Nephropathy is managed and treated.

The acceleration of biomarker research in IgA Nephropathy also stimulates broader developments within the healthcare sector. It encourages investments in research and development by pharmaceutical companies and academic institutions, fostering innovation in diagnostic technologies and therapeutic strategies. This trend not only benefits patients with IgA Nephropathy but also enhances the overall capabilities of medical science in dealing with complex diseases. Continued advancements in this area are expected to contribute significantly to the evolution of nephrology and personalized medicine.

Regional Analysis

In 2023, North America held a dominant market position, capturing more than a 45.20% share and holding a market value of US$ 39.28 billion for the year. This dominance is linked to the high prevalence of IgA nephropathy in the region. With more patients requiring treatment, demand for innovative therapies has risen. North America’s advanced healthcare systems further support this growth by providing access to cutting-edge medical solutions and facilities.

The presence of world-class research institutions also contributes to the market’s strength. These organizations focus on developing effective drugs and therapies for IgA nephropathy. Regulatory frameworks in the region allow quicker approvals for new treatments, speeding up their availability. These factors collectively make North America a hub for innovation and development in IgA nephropathy care.

The United States plays a significant role in this market leadership. It hosts many pharmaceutical companies and clinical trial facilities. These companies invest heavily in creating new treatments. Additionally, awareness campaigns and advocacy groups help in spreading information about early diagnosis and care. This proactive approach adds to the region’s dominance.

High healthcare spending and comprehensive insurance coverage in North America also enhance accessibility to treatment. Patients benefit from advanced medical technologies and supportive care systems. These factors ensure that individuals receive timely and effective treatment. As a result, North America remains a leader in the IgA nephropathy market and is expected to continue driving innovation and growth in the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The IgA nephropathy market is driven by key players like Astellas Pharma Inc., Kyowa Kirin Co. Ltd., and Merck & Co. Inc. Astellas focuses on precision medicine and partnerships to enhance its pipeline of innovative treatments. Kyowa Kirin leverages its expertise in immunology and biologics to develop targeted therapies, particularly in regions like Asia. Merck utilizes its global network and R&D capabilities to address chronic kidney diseases. These companies emphasize accessibility and scalability to meet the growing demand for IgA nephropathy treatments.

Pfizer Inc. and Johnson & Johnson Services Inc. are also prominent players in the IgA nephropathy market. Pfizer focuses on RNA-based and small-molecule therapies, supported by strategic acquisitions. Johnson & Johnson integrates drug innovation with patient support programs and combination therapies. Both companies aim to expand their global reach and address unmet needs in IgA nephropathy care. Their commitment to affordability and patient-centric strategies strengthens their market positions in diverse geographic regions.

Emerging players like Omeros Corporation and Calliditas Therapeutics contribute to the market’s growth. Omeros focuses on complement-mediated pathways in IgAN, while Calliditas specializes in precision medicine for kidney diseases. Travere Therapeutics develops orphan drugs to tackle rare nephrology conditions. These companies bring innovation through niche solutions, targeting specific disease mechanisms. Their strategies often involve collaborations and licensing agreements to expand their reach and enhance their product pipelines, fostering competition and innovation in the market.

The IgA nephropathy market benefits from increasing awareness, improved diagnostic methods, and growing R&D investments. Companies are focusing on novel mechanisms of action to address the disease’s complex pathology. Strategic collaborations, patient-centric approaches, and regional expansions are key to gaining a competitive edge. With a rise in healthcare needs, the market offers growth opportunities for both established and emerging players. These developments reflect a dynamic environment where innovation and accessibility drive the future of IgA nephropathy care.

Market Key Players

- Astellas Pharma Inc.

- Kyowa Kirin Co. Ltd.

- Merck Co. Inc.

- Pfizer Inc.

- Johnson Johnson Services Inc.

- Novartis AG

- Baxter International Inc.

- Fresenius Medical Care AG Co. KGaA

- Otsuka Pharmaceutical Co. Ltd.

- AbbVie Inc.

- Bristol-Myers Squibb Company

- Chugai Pharmaceutical Co. Ltd.

- HoffmannLa Roche Ltd.

Recent Developments

- In December 2022: Astellas Pharma Inc. completed the acquisition of Propella Therapeutics, Inc. This strategic move cost Astellas approximately US $175 million and involved acquiring all outstanding common stock and equity interests of Propella. Propella Therapeutics is known for its innovative drug PRL-02, an androgen biosynthesis inhibitor under development for prostate cancer treatment, which is in Phase 1 clinical trials and expected to enter Phase 2a in 2024.

- In March 2022: Merck Co. Inc. acquired Harpoon Therapeutics for approximately $680 million, intending to expand its oncology pipeline. Harpoon Therapeutics is known for its novel immunotherapy platforms, including a Tri-specific T cell Activating Construct (TriTAC) technology, which is used in several clinical trials including those for treating cancers with specific antigen expressions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 500.3 Billion |

| Forecast Revenue (2033) | US$ 86.9 Billion |

| CAGR (2024-2033) | 19.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Diagnosis (Iothalamate Clearance Test, Kidney Biopsy, Blood Tests, Urine Tests), By Diseases Type (Primary IgA Nephropathy, Secondary IgA Nephropathy), By Systems (Hematuria, Proteinuria, Edema, Others), By Population Type (Pediatrics, Adults), By Route of Administration (Oral, Parenteral, Others), By End Users (Hospitals, Specialty Clinics, Homecare, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Astellas Pharma Inc., Kyowa Kirin Co. Ltd., Merck Co. Inc., Pfizer Inc., Johnson Johnson Services Inc., Novartis AG, Baxter International Inc., Fresenius Medical Care AG Co. KGaA, Otsuka Pharmaceutical Co. Ltd., AbbVie Inc., Bristol-Myers Squibb Company, Chugai Pharmaceutical Co. Ltd., HoffmannLa Roche Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |