Quick Navigation

Report Overview

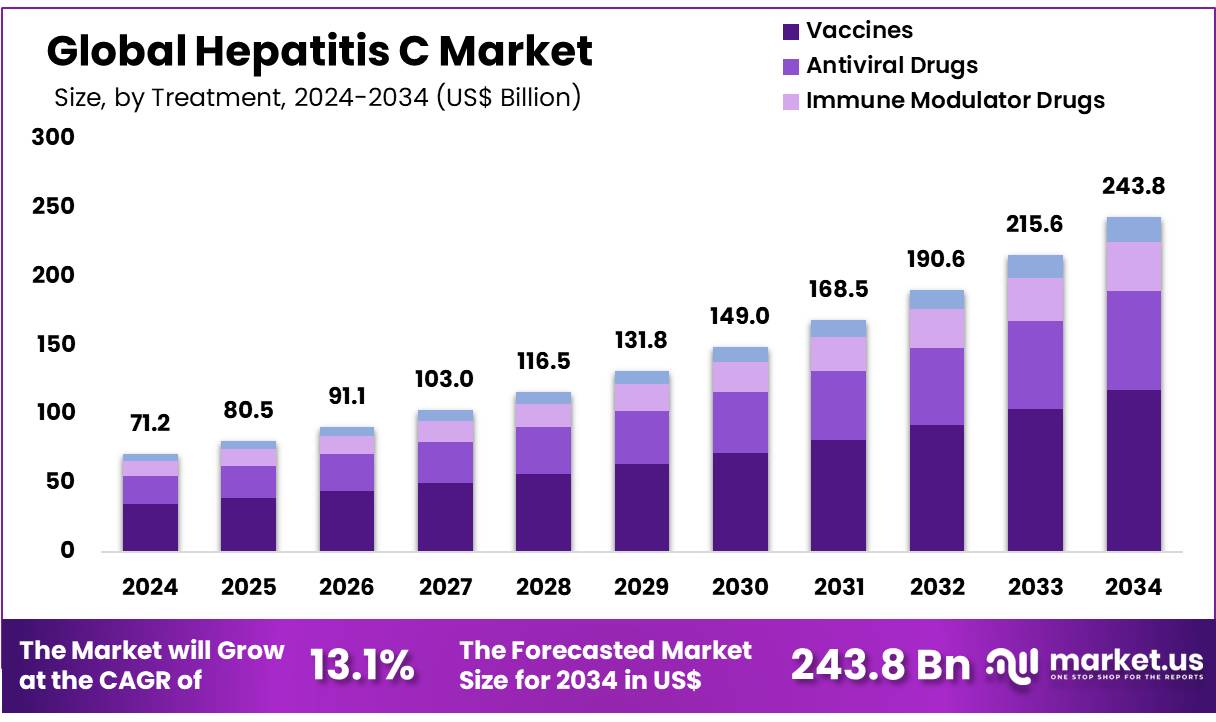

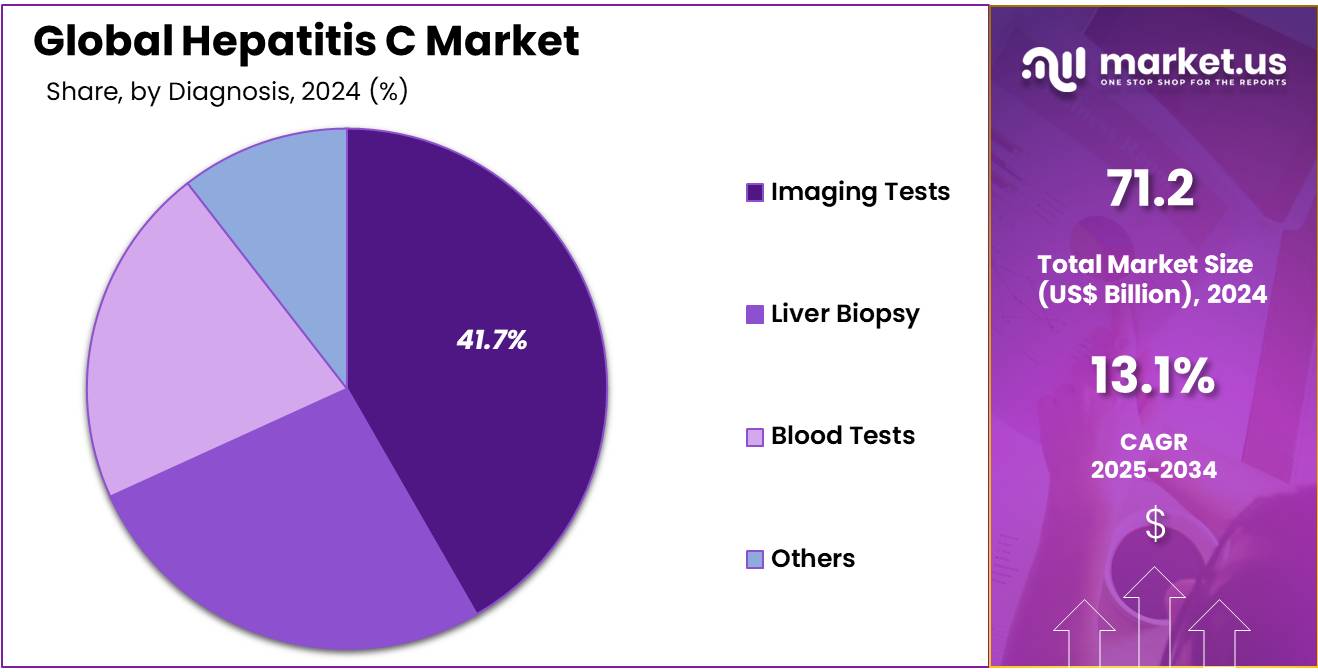

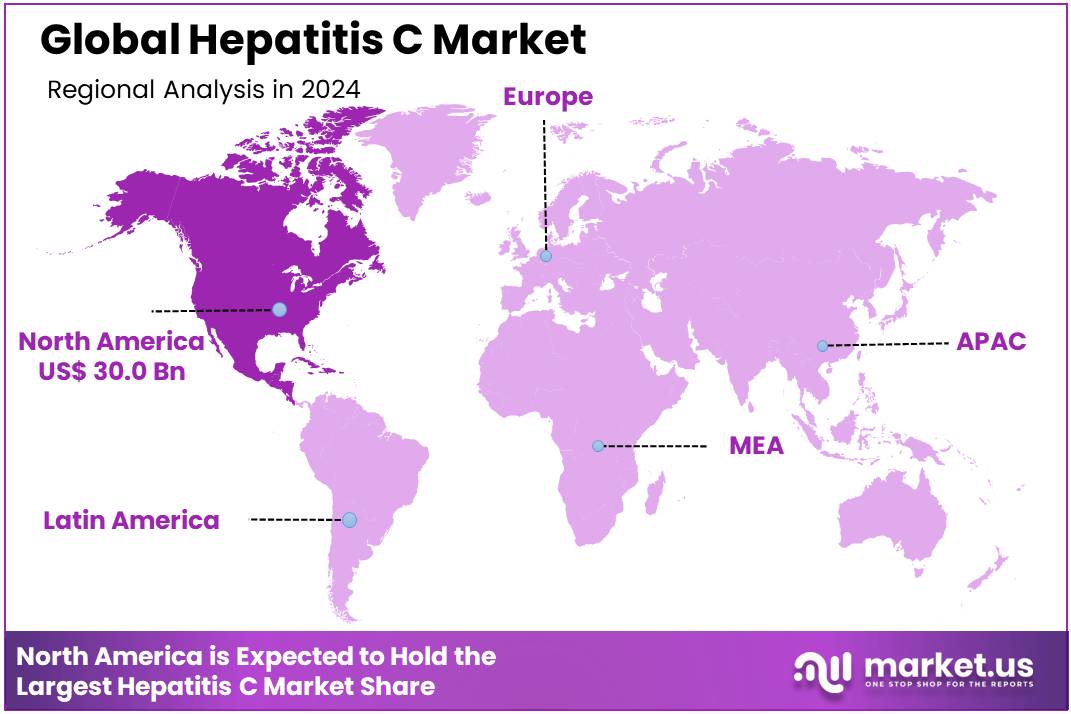

Global Hepatitis C Market size is expected to be worth around US$ 243.8 billion by 2034 from US$ 71.2 billion in 2024, growing at a CAGR of 13.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 42.2% share with a revenue of US$ 30.0 Billion.

Increasing awareness of hepatitis C (HCV) and the growing availability of effective treatments are driving significant growth in the hepatitis C market. Rising global incidence rates and the prevalence of chronic HCV infections continue to fuel demand for better diagnostic tools, therapies, and patient management solutions. In July 2021, the World Health Organization (WHO) reported that approximately 58 million people globally live with chronic hepatitis C virus (HCV) infection, with 1.5 million new infections annually.

This underscores the ongoing global health challenge posed by the disease and the urgent need for improved treatment options. Innovations in direct-acting antivirals (DAAs) have revolutionized HCV treatment, offering higher cure rates, shorter treatment durations, and fewer side effects. Opportunities in the market lie in expanding access to these life-saving therapies, especially in low- and middle-income countries, and improving diagnostic capabilities.

Rising adoption of screening and prevention programs and expanding healthcare infrastructure create a promising environment for further market development. Recent trends indicate a growing focus on personalized medicine and the exploration of combination therapies, which could lead to more targeted and effective treatment regimens for HCV patients.

Key Takeaways

- In 2024, the market for hepatitis C generated a revenue of US$ 71.2 billion, with a CAGR of 13.1%, and is expected to reach US$ 243.8 billion by the year 2033.

- The treatment segment is divided into vaccines, antiviral drugs, immune modulator drugs, and others, with vaccines taking the lead in 2024 with a market share of 48.3%.

- Considering diagnosis, the market is divided into liver biopsy, imaging tests, blood tests, and others. Among these, imaging tests held a significant share of 41.7%.

- Furthermore, concerning the route of administration segment, the market is segregated into oral, parenteral, and others. The oral sector stands out as the dominant player, holding the largest revenue share of 58.3% in the hepatitis C market.

- The end-users segment is segregated into hospitals, homecare, specialty clinics, and others, with the hospitals segment leading the market, holding a revenue share of 52.2%.

- North America led the market by securing a market share of 42.2% in 2024.

Treatment Analysis

The vaccines segment led in 2024, claiming a market share of 48.3% as healthcare providers focus on preventing the spread of the disease. Vaccines are anticipated to play a critical role in controlling hepatitis C infections, especially in high-risk populations, and are projected to gain wider adoption due to ongoing research and development efforts.

The development of effective vaccines to prevent hepatitis C, combined with the rising global burden of the disease, is likely to drive demand for vaccine-based interventions. Additionally, as governments and health organizations prioritize vaccination campaigns, the vaccines segment is projected to expand, contributing to the global fight against hepatitis C.

Diagnosis Analysis

The imaging tests held a significant share of 41.7% due to the increasing use of non-invasive diagnostic methods. Imaging tests, such as elastography and ultrasound, provide a reliable means to assess liver damage and fibrosis in hepatitis C patients, reducing the need for more invasive procedures like liver biopsy.

As the demand for early diagnosis and monitoring of liver conditions grows, imaging tests are expected to become more widely used in clinical settings. The rising awareness about the importance of early detection and the ability to track disease progression without invasive procedures is likely to fuel the growth of the imaging tests segment in the hepatitis C market.

Route of Administration Analysis

The oral segment had a tremendous growth rate, with a revenue share of 58.3% as oral antiviral drugs offer a more convenient and patient-friendly treatment option compared to parenteral alternatives. Oral therapies for hepatitis C, such as direct-acting antivirals (DAAs), have gained widespread popularity due to their high efficacy, ease of administration, and reduced side effects.

The increasing preference for non-injection treatments, particularly among patients who seek less invasive and more convenient options, is likely to drive the growth of the oral segment. Additionally, as new oral drugs continue to emerge, improving cure rates and treatment regimens, the demand for oral hepatitis C therapies is projected to continue expanding.

End-Users Analysis

The hospitals segment grew at a substantial rate, generating a revenue portion of 52.2% due to the central role hospitals play in the diagnosis and treatment of hepatitis C patients. Hospitals are anticipated to remain the primary setting for the management of hepatitis C, as they provide specialized care, advanced diagnostics, and access to cutting-edge therapies.

As the prevalence of hepatitis C increases and treatment options improve, hospitals are likely to see higher demand for both outpatient and inpatient services related to hepatitis C management. Furthermore, with the growing adoption of telemedicine and the expansion of hepatitis C care programs in hospitals, the demand for hospital-based care is projected to continue growing, contributing to the overall growth of this segment in the market.

Key Market Segments

By Treatment

- Vaccines

- Antiviral Drugs

- Immune Modulator Drugs

- Others

By Diagnosis

- Liver Biopsy

- Imaging Tests

- Blood Tests

- Others

By Route of Administration

- Oral

- Parenteral

- Others

By End-Users

- Hospitals

- Homecare

- Specialty Clinics

- Others

Drivers

Increasing Prevalence of Hepatitis C Infections is Driving the Market

The rising prevalence of hepatitis C infections globally is a key driver of the market. According to the World Health Organization (WHO), approximately 58 million people worldwide had chronic hepatitis C infection in 2022, with 1.5 million new infections occurring annually. This high burden of disease is pushing governments and healthcare organizations to prioritize screening, diagnosis, and treatment programs.

In the US, the Centers for Disease Control and Prevention (CDC) reported that hepatitis C-related deaths reached nearly 15,000 in 2022, underscoring the urgent need for effective interventions. Pharmaceutical companies like Gilead Sciences and AbbVie are expanding their portfolios of direct-acting antivirals (DAAs), which offer cure rates exceeding 95%. The growing demand for these therapies, coupled with increased awareness campaigns, is driving market growth and improving patient outcomes.

Restraints

High Cost of Treatment is Restraining the Market

Despite the availability of effective treatments, the high cost of hepatitis C therapies remains a significant restraint. A full course of direct-acting antivirals (DAAs) can range from US$26,000 to US$95,000, depending on the region and healthcare system. In 2022, a report by the US Department of Health and Human Services revealed that cost barriers prevented nearly 40% of eligible patients from accessing treatment.

This issue is especially pronounced in low- and middle-income countries, where healthcare budgets are constrained. Even in developed nations, insurers and governments often impose strict eligibility criteria to control spending. For instance, some US states restrict access to treatment for patients with advanced liver disease, which results in delayed care for many others. These financial challenges limit the widespread adoption of life-saving therapies, hindering overall market growth and access to essential hepatitis C treatments.

Opportunities

Expansion of Screening and Diagnosis Programs is Creating Growth Opportunities

The expansion of screening and diagnosis programs presents a significant growth opportunity in the hepatitis C market. Many infections remain undiagnosed due to the asymptomatic nature of the disease in its early stages. In 2023, the WHO launched a global initiative to increase testing rates, aiming to diagnose 90% of infected individuals by 2030.

In the US, the CDC reported that only 60% of people with hepatitis C were aware of their infection in 2022, leaving a substantial gap in diagnosis. Companies like Roche and Abbott are developing advanced diagnostic tools, including point-of-care tests, to improve detection rates. Increased screening efforts, combined with government funding for public health programs, are expected to drive demand for both diagnostic and therapeutic solutions, creating new opportunities for market players.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors are shaping the hepatitis C market in profound ways. Rising healthcare costs and budget constraints in many countries are limiting access to expensive treatments, particularly in low-income regions. For instance, the US healthcare inflation rate reached 4.6% in 2023, forcing some states to prioritize spending on other urgent health needs. Geopolitical tensions, such as trade restrictions and supply chain disruptions, have also impacted the availability of raw materials for drug manufacturing, leading to delays and price increases.

However, government initiatives and international collaborations are mitigating these challenges. Programs like the WHO’s global hepatitis strategy and funding from organizations like the Global Fund are expanding access to diagnostics and treatments. These efforts, combined with the growing availability of affordable generics, are driving progress toward eliminating hepatitis C as a public health threat. Despite the hurdles, the market is poised for growth, offering hope for millions of patients worldwide.

Latest Trends

Growing Adoption of Generic DAAs is a Recent Trend

The growing adoption of generic direct-acting antivirals is a notable trend in the hepatitis C market. Generic versions of drugs like sofosbuvir and daclatasvir have become widely available, particularly in low- and middle-income countries, where they are offered at a fraction of the cost of branded therapies. In 2022, the Medicines Patent Pool reported that generic DAAs had treated over 10 million patients globally since their introduction.

This trend is supported by initiatives like the WHO’s prequalification program, which ensures the quality and affordability of generic medicines. In the US, the FDA approved the first generic version of Epclusa in 2023, further expanding access to affordable treatment. The availability of generics is transforming the market, making life-saving therapies accessible to a broader population.

Regional Analysis

North America is leading the Hepatitis C Market

North America dominated the market with the highest revenue share of 42.2% owing to advancements in treatment options, increased screening efforts, and government initiatives aimed at eliminating the disease. According to the Centers for Disease Control and Prevention (CDC), the US reported approximately 66,700 new cases of chronic hepatitis C in 2022, highlighting the ongoing need for effective treatments and diagnostics. The introduction of direct-acting antivirals (DAAs), which boast cure rates exceeding 95%, has been a major factor in this growth.

The US Department of Health and Human Services (HHS) noted that over 1 million individuals in the US have been treated with DAAs since their approval, with a significant increase in treatment accessibility due to Medicaid expansions and state-funded programs.

Additionally, the Canadian Institute for Health Information (CIHI) reported a 15% increase in hepatitis C-related healthcare spending in Canada between 2022 and 2023, reflecting the growing emphasis on eliminating the disease. Public health campaigns, such as the CDC’s “Hepatitis C Elimination Plan,” have also contributed to higher diagnosis rates and treatment uptake. These factors, combined with increased awareness and improved healthcare infrastructure, have positioned North America as a leader in addressing hepatitis C.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to rising prevalence rates, improved healthcare access, and government-led elimination programs. The World Health Organization (WHO) estimated that over 70 million people in the region were living with chronic hepatitis C in 2022, with countries like India and China accounting for a significant proportion of cases.

India’s National Health Mission reported a 25% increase in screening and diagnostic efforts for the disease between 2022 and 2023, supported by the introduction of affordable generic versions of DAAs. Similarly, China’s National Health Commission highlighted that over 1.5 million individuals had received treatment for hepatitis C by 2023, with a focus on expanding access to rural areas.

The Australian government’s National Hepatitis C Strategy, which aims to eliminate the disease by 2030, has also led to a 30% increase in treatment initiations between 2022 and 2023. These efforts, combined with regional collaborations and technological advancements in diagnostics, are expected to drive significant progress in addressing hepatitis C across the Asia Pacific. The region is likely to emerge as a key player in the global fight against the disease, supported by robust policy frameworks and increasing investments in healthcare infrastructure.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the hepatitis C market focus on drug innovation, expanding their treatment portfolios, and increasing access to therapies to drive growth. They invest in developing more effective, direct-acting antiviral drugs with shorter treatment durations and fewer side effects. Companies also engage in strategic collaborations with healthcare providers, governments, and nonprofit organizations to improve patient access to treatment, especially in low-income regions.

Expanding into emerging markets with rising hepatitis C prevalence further supports market growth. Additionally, regulatory approvals and ongoing research into curative therapies continue to enhance the industry’s growth prospects.

Gilead Sciences, headquartered in Foster City, California, is a leading biopharmaceutical company focused on developing innovative antiviral therapies. The company’s portfolio includes Sovaldi and Harvoni, two groundbreaking treatments for hepatitis C that revolutionized the way the disease is treated. Gilead focuses on advancing its hepatitis C therapies with better efficacy, affordability, and expanded access.

Through strategic collaborations with healthcare providers and governments worldwide, Gilead continues to strengthen its position in the global hepatitis C market. The company remains committed to developing cures for chronic viral infections.

Top Key Players

- Zydus Pharmaceuticals

- Teva Pharmaceuticals

- Roche Diagnostics

- J & J

- GlaxoSmithKline

- Dicerna Pharmaceuticals

- Bristol-Myers Squibb Company

- Abbvie

Recent Developments

- In July 2023, Roche Diagnostics India launched the Elecsys HCV Duo, a first-of-its-kind fully automated immunoassay in India. This test enables healthcare providers to assess both hepatitis C virus antigen and antibody status from a single blood or plasma sample, facilitating early detection and monitoring of infection stages.

- In March 2021, Dicerna Pharmaceuticals and Roche commenced a Phase II clinical trial to evaluate the potential of RG6346, an experimental RNA interference (RNAi) treatment, for chronic hepatitis C. This partnership underscores the industry’s commitment to advancing novel therapeutic approaches to combat the virus and improve patient outcomes.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 71.2 billion |

| Forecast Revenue (2034) | US$ 243.8 billion |

| CAGR (2025-2034) | 13.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Treatment (Vaccines, Antiviral Drugs, Immune Modulator Drugs, and Others), By Diagnosis (Liver Biopsy, Imaging Tests, Blood Tests, Others), By Route of Administration (Oral, Parenteral, and Others), By End-Users (Hospitals, Homecare, Specialty Clinics, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Zydus Pharmaceuticals, Teva Pharmaceuticals, Roche Diagnostics, J & J, GlaxoSmithKline, Dicerna Pharmaceuticals, Bristol-Myers Squibb Company, and Abbvie. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |