Quick Navigation

Report Overview

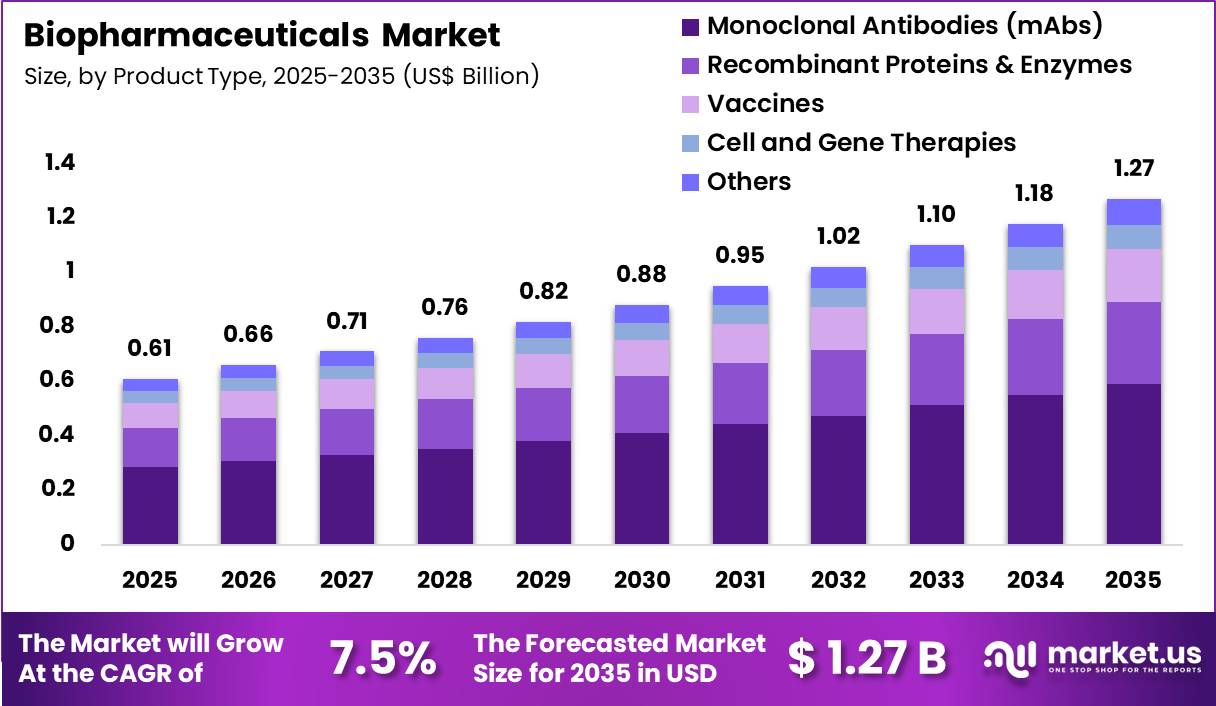

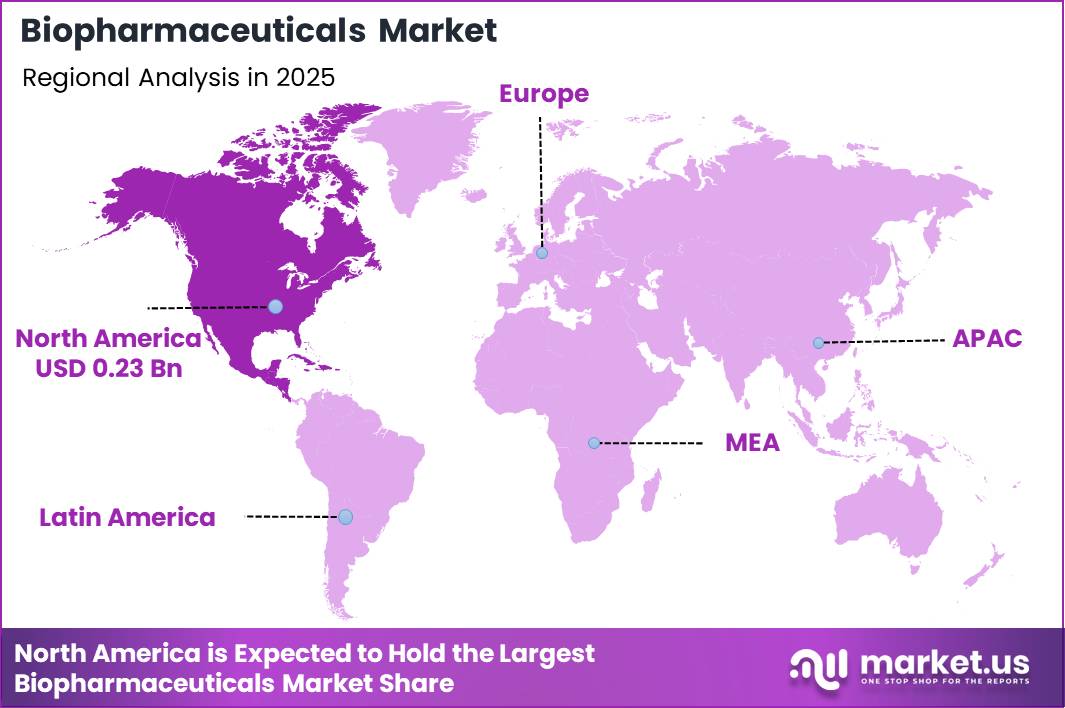

Global Biopharmaceuticals Market revolution is currently sweeping the world worth a valuation of USD 0.61 Billion in 2025, expected to reach USD 1.27 Billion by 2035 recording at a CAGR of 7.5%. In 2025, North America led the market, achieving over 38% share with a revenue of US$ 0.23 Billion.

These biopharmaceuticals are defined as a form of drug produced using living systems, such as cells, bacteria, or yeast, through biotechnological processes, not through chemical synthesis. This includes complex biologics such as monoclonal antibodies, vaccines, and recombinant proteins, which unlike regular drugs like aspirin, target biological mechanisms.

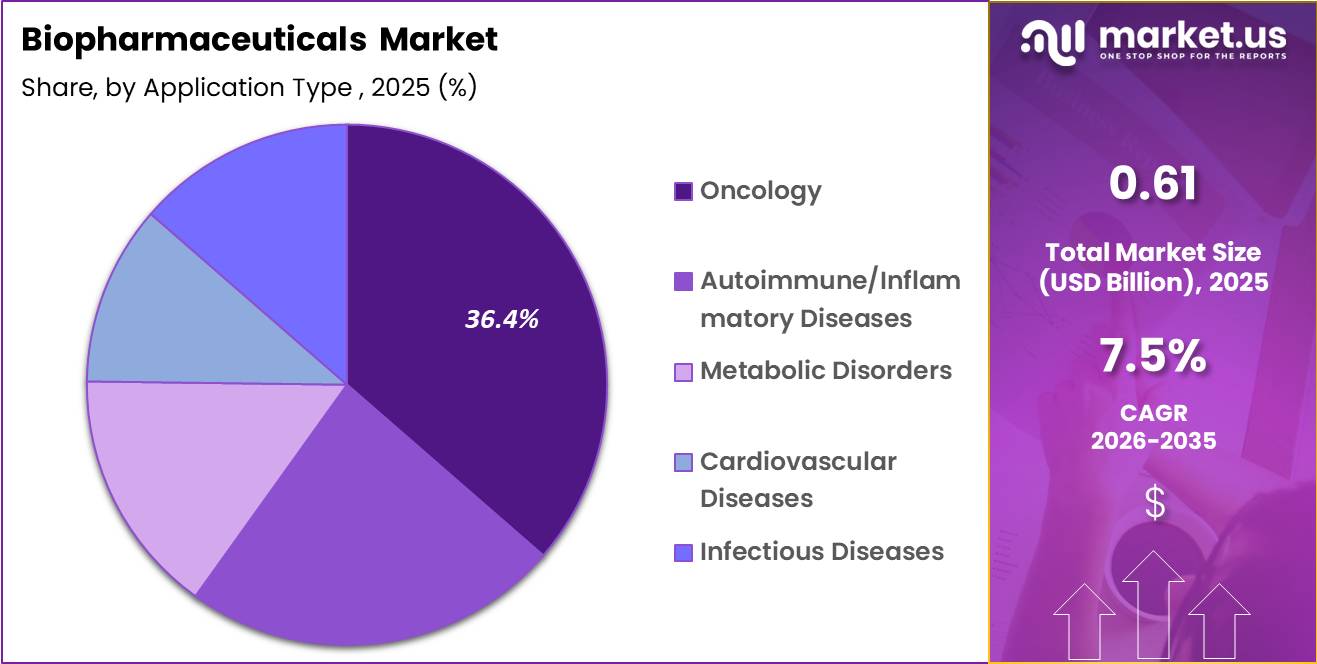

Several factors are leading to the revolution, mainly due to an increased preference for biopharmaceuticals for chronic diseases, with monoclonal antibodies taking the largest market share at 46.5%. The oncology application segment accounts for 36.4% of the industry, with metabolic and autoimmune disorders following after.

Key strategic initiatives responsible for this development include Eli Lilly’s USD 4.5 billion manufacturing expansion and AstraZeneca’s vision to achieve a USD 80 billion market share by 2030. Currently, North America holds the largest regional share at 38%, followed by the Asia-Pacific region which is the fastest-growing one owing to its increasing biologic capabilities.

Key Takeaways

- Market Size: A biopharmaceuticals revolution is currently sweeping the world worth a valuation of USD 0.61 Billion in 2025, expected to reach USD 1.27 Billion by 2035

- Market Share: The market is projected to have a CAGR of 7.5% during 2026–2035.

- Product Type Analysis: Monoclonal antibodies are expected to dominate the market with 46.5% market share.

- Application Type Analysis: The oncology segment accounted for the largest application share at 36.4%.

- Formulation Type Analysis: In terms of formulations, injectable products (IV, IM, SC) held a 92.64% share.

- Distribution Channel Type Analysis: Hospital pharmacies dominated the distribution channel segment with a 62.4% market share.

- Regional Analysis: In 2025, North America led the market, achieving over 38% share with a revenue of US$ 0.23 Billion.

Product Type Analysis

Monoclonal Antibodies Dominate Market Segments in the Biopharmaceuticals Market.

Monoclonal Antibodies form the largest segment in the Biopharmaceuticals Market, occupying a market share of 46.5%, owing to their high specificity in targeting, high clinical efficacy, and broad use in oncology, autoimmune conditions, and infectious diseases. The precision and reduced side-effects associated with monoclonal antibodies, as opposed to conventional medicine, have been key contributors to their adoption. According to SelectUSA, the USA still leads in terms of biopharmaceutical research and development, while oncology continues to dominate among therapeutic areas with a 36.4% market share.

The growth of the market will be primarily affected by two factors the use of artificial intelligence in discovering new drugs that cut down development time for the R&D department by leaps and bounds and the introduction of single use bioprocessing technology that decreases production costs. Although monoclonal antibodies represent the lion’s share of the profits made in the business, vaccines have become profitable thanks to mRNA developments.

Application Type Analysis

Oncology Holds the Largest Share in Biopharmaceuticals Market.

The global biopharmaceuticals market is intelligently classified based on their applications, and Oncology is still leading with its market dominance of 36.4% in 2025. This dominance is attributed to the increasing prevalence of global cancer incidences and the growing adoption of monoclonal antibodies for breast, lung, and prostate cancer. Although oncology contributes significantly to the overall market revenue, Cardiometabolic and Immunology represent the most rapidly growing application areas. The global cardiometabolic treatment is expected to show a noteworthy growth rate of 22.3% CAGR till 2035

The market growth is primarily determined by two major factors – first, drug discovery enabled by AI, making target identification much faster; and second, single-use bioprocessing that reduces costs associated with manufacturing biological treatments for a wide range of uses.

As SelectUSA states, R&D intensity is at its peak in the USA, whereas according to IFPMA, the adoption of personalized medicine, along with accelerated approvals by the FDA, is extremely important. Such trends guarantee greater efficiency of the biological treatment in Metabolic Disorders (15.3%), and Infectious Diseases (13.6%).

Formulation Type Analysis

Injectables (IV, IM, SC) Dominate Amid Rapid Delivery Innovation.

Injectables (IV, IM, SC) continue to dominate the biopharmaceutical product segment, accounting for an enormous market share of 92.64% in 2025. The key reason behind their prevalence is the high bioavailability necessary for biological drugs when used for the treatment of oncology and autoimmune disorders. Although injectable lead the segment in volume terms, Oral Biologics are emerging as the most rapidly growing one, growing at 21% CAGR.

The growth of market depends greatly on AI-based formulation optimization, which increases drug stability, and the application of single-use technology to reduce manufacturing expenses. As IQVIA states, the emergence of bio similar and self-administration devices such as auto injectors plays an important role in expanding global accessibility and increasing adherence.

Distribution Channel Type Analysis

Hospital Pharmacies Lead as Major Distribution Channel for Biopharmaceuticals

The hospital pharmacy is expected to hold a dominant position in the biopharmaceuticals market share with around 62.4% in 2025 on the back of superior cold chain storage infrastructure and clinical monitoring required while administering biopharmaceuticals like oncological drugs and cellular therapies. Conversely, the online pharmacy is projected to witness rapid growth, recording an annual compound growth rate of about 20% owing to telemedicine and consumer-direct online portals for chronic ailments.

AI-based inventory systems and blockchain-powered traceability solutions have been vital in boosting market growth. As per IQVIA, one of the primary growth drivers would be the transition to specialty pharmacy networks and home-based care delivery channels that facilitate greater access to biologics without overburdening hospitals.

Key Market Segments

By Product Type

- Monoclonal Antibodies (mAbs)

- Recombinant Proteins & Enzymes

- Vaccines

- Cell and Gene Therapies

- Others

By Application

- Oncology

- Autoimmune/Inflammatory Diseases

- Metabolic Disorders

- Cardiovascular Diseases

- Infectious Diseases

By Formulation

- Injectables (IV, IM, SC)

- Inhalation / Nasal Sprays

- Other Formulations

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Driver

Oncology led biologics launch intensity

The 2025 approval cycle confirms that biologics innovation remains commercially concentrated in specialty care, especially oncology and immune mediated disease. FDA CDER approved 46 novel drugs in 2025, including multiple biologics such as ADCs, monoclonal antibodies, and protein based products, while an industry review of the same cycle noted that biologics accounted for about one quarter of approvals and that cancer remained the main therapeutic focus.

That matters for 2026 forecasting because oncology biologics typically carry higher annual revenue density per launch than primary care products, benefit from faster uptake through concentrated prescriber networks, and are increasingly paired with biomarker led patient selection that improves pricing defensibility and treatment persistence.

Commercially, this driver supports above baseline growth by lifting launch value per approved asset, increasing infusion center and specialty pharmacy throughput, and extending lifecycle economics through line extension strategies such as subcutaneous reformulations and combo regimens, as seen in the continued cadence of antibody and oncology approvals during 2025.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oncology-led biologics launch intensity | +1.4% | North America core, EU, Japan, China urban specialty centers | Short term (≤ 2 years) |

| Biosimilar scale-up and interchangeability expansion | +1.1% | EU core, U.S. catch-up, Canada, select APAC | Medium term (2-4 years) |

| Cell and gene therapy commercialization broadening | +1.6% | U.S. core, EU5, UK, Japan, Gulf premium hubs | Medium term (2-4 years) |

| Manufacturing platform standardization and faster CMC pathways | +0.9% | U.S., EU, Singapore, South Korea, India biologics corridors | Short term (≤ 2 years) |

| Medicare pricing pressure shifting portfolio mix toward high-value biologics | +0.8% | U.S. core with global portfolio spill-over | Medium term (2-4 years) |

| Prevention, immunology, and rare-disease biologics diversification | +1.0% | North America, EU, affluent APAC, LatAm private-channel spill-over | Long term (≥ 4 years) |

Challenge

Sterile Capacity Bottlenecks

Sterile biologics capacity remains a growth friction because demand has shifted faster than qualified fill finish, aseptic suite, and high containment expansion cycles, while the approval pipeline continues to refresh commercial scale needs, including 55 new FDA approvals in 2025 that sustain downstream manufacturing loading across biologics and specialty injectables.

In practical terms, a new commercial biologics line still typically requires 24 to 36 months to design, validate, and stabilize, with ramp losses of roughly 8% to 15% in initial throughput as media fills, line clearances, campaign sequencing, and tech transfer deviations suppress asset utilization below modeled nameplate. This does not stop sales today, but it can shave about 1.4% points from the market’s achievable CAGR by extending launch to steady state timelines by 2 to 4 quarters, pushing CMO slot premiums higher, and forcing firms to hold 3 to 6 months of extra safety stock for high value SKUs.

The strategic response is not just more steel in the ground; firms increasingly need modular fill finish footprints, dual region release capacity, and earlier late stage network locking so capacity risk is absorbed during phase III rather than after filing, especially in North America, Western Europe, Singapore, and South Korea where biologics node concentration is highest.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Sterile Capacity Bottlenecks | -1.4% | North America core; EU biologics hubs; APAC export bases | Medium term (2-4 years) |

| Quality Deviation Recurrence | -1.2% | US FDA supply chain; EU regulatory hubs; Japan/Korea plants | Medium term (2-4 years) |

| Cold-Chain Integrity Gaps | -0.9% | Global vaccine lanes; EM logistics corridors; rural last-mile networks | Medium term (2-4 years) |

| Bioprocess Talent Deficit | -1.0% | US and EU advanced plants; India; Singapore; Korea | Long term (≥ 4 years) |

| Multi-Node Supply Fragility | -1.1% | EU import-dependent markets; US biologics network; APAC input clusters | Medium term (2-4 years) |

| Regulatory Data Burden | -0.8% | US; EU; ICH markets; cross-border launch programs | Short term (≤ 2 years) |

Restraints

U.S. tariff shock on patented biologics inputs

The April 2026 U.S. proclamation created a new cost overhang for patented pharmaceutical products and associated ingredients, with headline duty rates reaching 100% for covered imports, 20% for firms with approved onshoring plans, and 15% for imports from the EU, Japan, Korea, Switzerland and Liechtenstein, while generics and biosimilars were exempt for now; for biopharma, that sharply raises landed-cost uncertainty around monoclonal antibody intermediates, high-value APIs, and single-use processing inputs embedded in patented therapy supply chains.

The direct bottleneck is not only tariff expense but network redesign: companies now face qualification of alternate supply nodes, inventory buffering, and duplicate release testing, all of which lengthen planning cycles and can push procurement and tech-transfer timelines out by two to four quarters for complex biologics.

Strategically, this acts as a near-term drag on revenue conversion and operating margin because manufacturers cannot fully pass through cost inflation in contracted channels, especially where payer pressure is rising, so management teams are more likely to defer incremental line expansions, prioritize domestic fill finish over new molecule launches, and re-rank portfolios toward exempt orphan, plasma derived, or biosimilar categories.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S. tariff shock on patented biologics inputs | -1.4% | North America core, EU export nodes, Japan, Korea, Switzerland | Short term (≤ 2 years) |

| GMP failures and batch-release disruptions | -1.1% | North America core, EU, India, APAC biologics hubs | Short term (≤ 2 years) |

| IRA price compression on mature biologics | -1.3% | U.S. core; spillover to EU pricing corridors | Medium term (2-4 years) |

| CDMO/outsourcing realignment under BIOSECURE rules | -0.9% | U.S., China-linked supply chains, Singapore, Korea, EU | Medium term (2-4 years) |

| Weak biotech funding and delayed scale-up CapEx | -1.0% | U.S., EU, UK, selective APAC innovation clusters | Short term (≤ 2 years) |

| EU regulatory transition and compliance burden | -0.6% | EU core, UK-linked exporters, global filing hubs | Medium term (2-4 years) |

Opportunity

Building Regional Biologics and mRNA Hubs in LMICs to Unlock New Demand Pools

This qualifies as an opportunity because baseline forecasts generally assume demand growth is served by today’s established production geographies, while the untapped upside comes from building regional manufacturing and commercialization ecosystems in low and middle income countries that can create new demand pools, procurement access, and sovereign supply contracts not yet fully captured in current models.

WHO’s mRNA technology transfer program had 15 partners as of May 2025 and is explicitly expanding from COVID vaccines toward other mRNA vaccines and therapeutics, including monoclonal antibodies, while Gavi has approved up to $1.2 billion for the African Vaccine Manufacturing Accelerator and broader 2026 to 2030 support for regional manufacturing, creating a rare policy financing window to localize fill finish, drug substance, and platform technologies.

Companies that move early can convert this into 20% to 30% lower logistics exposure, 10% to 15% tender price advantages in public procurement, faster emergency access positioning, and a new long duration TAM across Africa, MENA, Southeast Asia, and parts of Latin America where localized production can support $300 million to $800 million regional revenue platforms per asset class by 2030, especially when using modular mRNA or recombinant platforms that can be repurposed across vaccines, antibodies, and outbreak response products

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Biosimilar void capture | +2.4% | U.S., EU, India, select LATAM | Medium term (2-4 years) |

| AI-native bioprocess monetization | +1.6% | North America core, EU, Japan, Korea | Short term (≤ 2 years) |

| LMIC regional biologics hubs | +2.1% | Africa, Southeast Asia, MENA, LATAM | Medium term (2-4 years) |

| ADC/CGT platform roll-ups | +1.9% | U.S., EU, China, Korea | Medium term (2-4 years) |

| Outcomes-based specialty access | +1.3% | U.S., EU5, Gulf states | Short term (≤ 2 years) |

| Lifecycle reformulation plays | +1.1% | U.S., EU, Japan, urban China | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping the Biopharmaceuticals Market

The current geopolitical climate is impacting the biopharmaceuticals industry in terms of threats posed by supply chain concentration, export controls, regulatory differences, and regionalization policies of biologics manufacturing processes. Raw materials and expertise required for producing biologics are concentrated in certain geographic locations, leading to supply chain disruptions.

North America and Europe lead in terms of monoclonal antibodies, vaccine, and gene therapy production, whereas Asia-Pacific countries are increasing their capacity. Interruptions in active pharmaceutical ingredient (APIs), biological intermediate, or cold storage supply chain can lead to delays in bringing the products to the market

Export control regulations, trade tariffs, and regulations differ between various geographic regions, leading to additional uncertainty in global supply chains. Geopolitical influences on the import, approval, and manufacturing of biologics will delay their launch in the market, especially in the case of novel therapies such as cell and gene therapies.

The top biopharmaceutical companies are moving toward building more manufacturing plants regionally, decentralizing manufacturing operations, and sourcing from varied sources in order to minimize risks associated with operational and logistics functions, making the companies resilient to changes.

Nevertheless, there still exist many challenges because of the high level of concentration that exists with respect to production processes of biologics, excipients, and cold chain infrastructure. This leaves the companies exposed to various risks including shortages and lengthy supplier qualification processes.

The geopolitical factors are promoting local manufacturing capacity, clinical trial centers, and biotech infrastructure in North America, Europe, and Asia Pacific, while at the same time changing the competitive landscape of the industry.

Regional Analysis

North America Generated Highest Revenue Globally and Dominated the Biopharmaceuticals Market.

North America was leading the biopharmaceuticals market in terms of market share with around 38% of the overall consumption in the world in 2025, because of its robust revenue generation capability from the presence of well-developed healthcare infrastructure, along with substantial investments in R&D activities. The growth in the market is fueled by increased investments by various companies as well as governments in major regions such as the United States.

Moreover, most innovative biologics developed are protected under strong patents in the US, fostering R&D activities. Increasing cost of health care services, rising popularity of biopharmaceutical drugs, and rising incidences of chronic illnesses such as cancer, autoimmune diseases, and cardiovascular diseases have further helped North America in establishing dominance in the global market.

Asia Pacific Anticipated to Offer High Growth Opportunities.

In the forecast period, the highest growth potential will be offered by the Asia Pacific region owing to the large population that constitutes almost two-thirds of the total world population. Chronic illnesses and other complex ailments are increasingly common in the region, and the investment in health care expenditure and infrastructure is also rising.

With several prominent contract manufacturing organizations existing in the region and rising biotechnology investment in countries including China, India, and Japan, the market will experience positive impacts on expansion.

Key Regions

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The global biopharmaceutical industry is characterized by fierce competition among many local, regional, and multinational companies. Large companies in this industry have been able to secure their positions in the market through brand equity, effective marketing network, and high-quality research and development.

Strategic alliances, mergers, acquisitions, licensing, and product development are some of the strategies that companies in this industry are using to improve their competitiveness in the global market. Others include expanding production facilities, entering new geographical regions, and adopting biologics technology.

Such competition is bound to lead to constant innovation in areas such as monoclonal antibodies, vaccines, and cell and gene therapy treatments for various chronic and complex diseases around the world.

Market Key Players

- Roche Holding AG

- Johnson & Johnson (Janssen Pharmaceuticals)

- AbbVie Inc.

- Amgen Inc.

- Pfizer Inc.

- Novartis AG

- Bristol-Myers Squibb Company

- Sanofi S.A.

- Eli Lilly and Company

- AstraZeneca PLC

- Merck & Co., Inc.

- Biogen Inc.

- Regeneron Pharmaceuticals

- Gilead Sciences Inc.

- Novo Nordisk A/S

Key Development

- May 2026, Eli Lilly made another USD 4.5 billion investment into its Lebanon, Indiana manufacturing facilities, including a new dedicated genetic medicines manufacturing facility

- May 2026, Odyssey Therapeutics increased its upsized U.S. IPO pricing to USD 18 per share to raise an estimated USD 279 billion for the development of its portfolio of immune disorders and inflammatory diseases therapies.

- Feb 2026, AstraZeneca reiterated its strategic plan to achieve USD 80 billion revenues by 2030 with the planned release of more than 25 blockbuster drugs before the end of the decade.

- May 2026: Bayer entered into an agreement to acquire Perfuse Therapeutics for up to USD 2.45 billion, securing exclusive rights to PER-001, a novel therapy developed for ischemic ophthalmic conditions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 0.61 Bn |

| Forecast Revenue (2035) | US$ 1.27 Bn |

| CAGR (2026-2035) | 7.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Forecast for Revenue, Dynamics of the Market, Competitive Scenario, Recent Developments, Trends, and Geopolitical Factors. |

| Segments Covered | By Product Type (Monoclonal Antibodies, Recombinant Proteins & Enzymes, Vaccines, Cell and Gene Therapies), By Application (Oncology, Neurological Disease, Metabolic Disease), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa & Rest of MEA |

| Competitive Landscape | Roche Holding AG, Johnson & Johnson (Janssen Pharmaceuticals), AbbVie Inc., Amgen Inc., Pfizer Inc., Novartis AG, Bristol-Myers Squibb Company, Sanofi S.A., Eli Lilly and Company, AstraZeneca PLC, Merck & Co., Inc., Biogen Inc., Regeneron Pharmaceuticals, Gilead Sciences Inc., Novo Nordisk A/S |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |