Quick Navigation

Report Overview

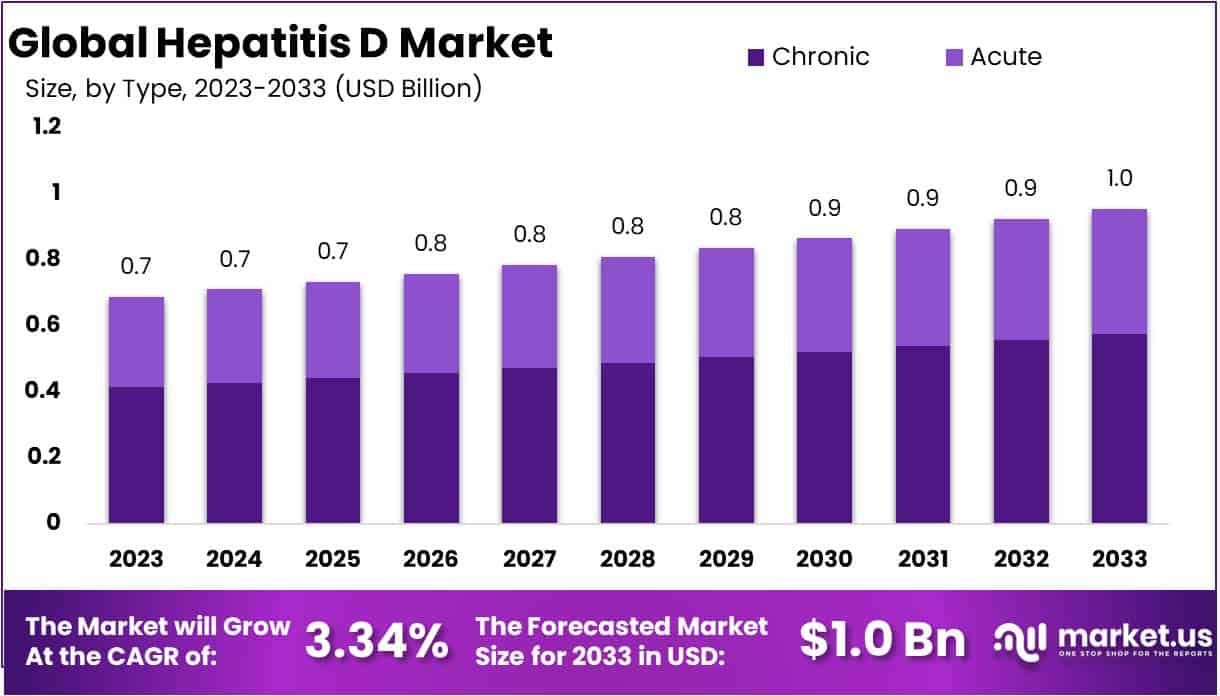

The Global Hepatitis D Market size is expected to be worth around USD 1 Billion by 2033, from USD 0.7 Billion in 2023, growing at a CAGR of 3.34% during the forecast period from 2024 to 2033.

The market for hepatitis D, a viral ailment brought on by the hepatitis D virus (HDV), refers to commercial elements and dynamics surrounding its management, diagnosis, treatment and prevention. The development, production, distribution and use of goods and services associated with hepatitis D are undertaken by a variety of stakeholders, including pharmaceutical companies, biotechnology businesses, manufacturers of diagnostic tests, healthcare providers, governmental organizations, research institutions and patients.

Hepatitis D is becoming more common throughout the world, which is one of the main factor supporting the market expansion. The market for hepatitis D is greatly influenced by increasing incidences of hepatitis D and hepatitis B, as well as consumption of an unbalanced diet. In addition to this, the escalating healthcare expenses, enhanced government funding, and expanded efforts by both public and private organizations to spread knowledge of illness boosts the dimensions of the market.

- According to World Health Organization, around 292 individual or about 5% of the worlds’ population, have chronic hepatitis B or C infections, which can result in the development of Hepatitis D.

Key Takeaways

- Based on type, chronic hepatitis D segment occupied a notable market revenue share of 60.2%, dominating the global Hepatitis D market in the year 2023.

- Based on diagnosis, blood test segment owing to its first priority by healthcare professionals marks its dominance in the global Hepatitis D market.

- Based on Distribution channel, hospital pharmacies came up as a front runner in the global Hepatitis D market.

- Rising prevalence of Hepatitis D viral infection necessitates medical treatments, thereby boosting the market growth.

- Side effects and high cost of treatment associated with hepatitis D medications may hamper the market in the near future.

- North America held a prominent market revenue share of 52.4% in the year 2023.

Type Analysis

Chronic Hepatitis D segment overshadows the market

Based on type, the global Hepatitis D market is broadly classified into acute and chronic segments. A commendable market revenue shares 60.2% is withheld by chronic hepatitis D segment, dominating the global Hepatitis D market in the year 2023. Chronic Hepatitis D is characterized by persistent infection and long term liver inflammation caused by hepatitis D virus, which persist and progress over time, leading to rising demand for medical management.

Chronic Hepatitis D is associated with more severe liver disease than hepatitis B alone. Cirrhosis, liver failure, and hepatocellular carcinoma are some of the common risks associated to chronic hepatitis D. This, in turn, necessitates regular monitoring, treatment and specialized care, leading to an escalated ultimatum for healthcare services and therapies specific to chronic hepatitis D. The lack of specific antiviral drugs targeting HDV replication contributes to the challenges in managing chronic hepatitis D effectively.

Thus, the limited treatment options and the rising need for ongoing management contribute to the dominance of chronic hepatitis D segment in the market. As the disease require long-term disease management and regular follow up to monitor liver function and disease progression, this leads to steady demand for healthcare services, such as diagnostic tests, routine monitoring, and potential treatment interventions.

- According to Journal of Infectious Diseases, the overall prevalence of Hepatitis D virus in the general population was around 0.80% and 13.02% HBV carriers, equating to 48-60 million infections globally.

Diagnosis Analysis

Blood tests segment occupied a major market portion

Based on diagnosis, the global hepatitis D market is fragmented into Blood Tests, Elastography, Liver Biopsy, Serologic Testing and other segments. Usually for identification of hepatitis D, doctors primarily go with blood tests. Through blood tests, the level of anti-HDV immunoglobulin G (IgG) and immunoglobulin M (IgM) are noted, which confirms the presence of hepatitis D infection inside the patients’ body. Thus, blood test segment accounts for highest revenue generation in the global Hepatitis D market, leading to market excellence.

Distribution Channel Analysis

Owing to systematic management hospital pharmacy segment dominated the market

Based on distribution channel, the market for hepatitis D bifurcates into Hospital pharmacies, Retail pharmacies and Online Pharmacies segment. Amongst these, hospital pharmacy category accounted for highest revenue share of 71.5%, dominating the market in the year 2023. The segmental dominance is ascribed to well-equipped infrastructure of hospital pharmacies along with presence of professional staff to handle these requirements and temperature controlled storage facilities.

Hospital pharmacies are better equipped to manage and coordinate the logistics of such treatment regimens, ensuring precise drug supply, dosage adjustments, and monitoring of patient adherence. In addition to this, patients have a strong trust, as hospital pharmacies work closely with healthcare providers, including hepatologist and Infection disease specialist.

The segment further dominates by virtue of ongoing collaborations among hospitals and healthcare providers ensuring optimal medication selection, dosing, and monitoring depending on patients’ need and treatment response. Thus, these benefactors contribute towards global hepatitis D market growth in recent years.

Key Market Segments

By Type

- Chronic

- Acute

By Diagnosis

- Blood Tests

- Elastography

- Liver Biopsy

- Serologic Testing

- Other

By Distribution channel

- Hospital pharmacies

- Retail pharmacies

- Online Pharmacies

Market Drivers

Rising prevalence of Hepatitis D

The global hepatitis D market witness’s robust growth by virtue of rising prevalence of hepatitis D in recent years. Hepatitis D is usually caused by defective single stranded RNA virus known as hepatitis delta virus which depends on presence of hepatitis B virus for both expression and replication. This leads to liver inflammation, further impairing liver functions and resulting in chronic liver issues like liver cancer and scarring.

Some of the common symptoms of Hepatitis D include nausea, vomiting, fatigue, jaundice, joint pain, loss of appetite, abdominal pain and dark urine. The rise of Hepatitis D cases basically scales due to high intake of unbalanced diet, affecting the market growth. In addition to this, awareness regarding hepatitis D infection, its control and preventive measures is increasing with rising government funding, escalating healthcare expenditures and initiatives by government and private organizations, thus resulting into market expansion.

- According to World Health Organization, in 2022, nearly 5% of people worldwide had chronic hepatitis B infection, resulting into Hepatitis D disease.

Another crucial factors driving the market growth of hepatitis D includes increasing number of product launches and item endorsements, escalated research and development efforts, and development of new hepatitis drugs for the treatment of various hepatitis types.

Market Restraints

High cost of treatment

Though hepatitis D infection treatments prove to be beneficial by many people, still market may hinder due to high cost of treatment and associated side effects like liver failure, liver cirrhosis and hepatocellular carcinoma. Additional challenge may be faced by the market by virtue of lack of knowledge about preventive measures. Hepatitis D market is expected to grow slowly during the prophecy period as high capital is needed for hepatitis pharmaceutical production.

This results in expensive hepatitis medications, as these are made by expensive basic materials such as active pharmaceutical ingredients (APIs) and pharmacological intermediates. In addition to this, there is a necessity for skilled labors for intricate process of producing, separating, and utilizing raw materials for the formulation of pharmaceuticals and biopharmaceutical treatments, thereby leading to overall rise in the expense of Hepatitis D medications.

- According to DNA labs India, the average cost of PCR test for detection of hepatitis D ranges between 7500-8500 rupees.

Opportunities

Ongoing Clinical Trials

Lucrative opportunities are gained by global hepatitis D market as there are escalating clinical trials going on to bring out new products and treatments for treating hepatitis D infections. One of the known and only medication being approved for hepatitis D treatment includes Pegylated interferon, which works by boosting the immune system’s ability to combat the infection. But when this medication is administered once a week, approximately 30% of the patients go into remission.

New study indicates that long term injections have higher success rates. Although they have no impact on hepatitis D, oral nucleosides approved for Hepatitis B are occasionally used in conjugation with interferon therapy to help control hepatitis B viral loads. Recently, seven medications are currently undergoing clinical studies to determine how well the work to treat the Hepatitis D virus. Thus, these rising clinical trials related to hepatitis D infection, presents many opportunities towards market expansion.

- According to German Center for Infection Research, TherVacB, a novel therapeutic vaccine to combat hepatitis B, entered first clinical trial, which is developed under the leadership of Helmhotz Munich.

- In December 2022, the Medical Devices Safety Authority and New Zealand Medicines permitted Bluejay Therapeutics a regulatory approval to inititate clinical trials of BJT-778 for treating chronic hepatitis B and chronic Hepatitis D.

Latest Trends

Nucleoside analogues or oral antivirals

Antivirals or NAs stop the hepatitis B virus from reproducing, slowing down the risk of liver damage. Less liver damage occurs when there is less virus present. People consuming NAs orally as a pill experiences very few side effects.

Pegylated Interferon

It is an immune modulator drug, currently approved by United States Food and Drug Administration. Doctors give this drug by injection once a week for around 6 weeks to 1 year. Unfortunately, the drug is associated with side effects such as flu-like symptoms and depression.

Combination therapy

A combination of two or more drugs proves to more beneficial in treating chronic Hepatitis D. Clinical trials are being carried out involving a combination of immune modulatory drugs and nucleoside analogues to treat chronic HBV.

Covalently closed circular DNA (cccDNA) inhibitors

These target small cccDNA molecule in the nucleus of liver cell associated with infection. The cccDNA molecule is a source of all HBV gene products. Developing these drugs remains very challenging but represents the most sought-after cure for this condition.

Impact of Macroeconomic Factors

Inflation has impacted the market for Hepatitis D treatment to a considerable extent. With the increase in prices of goods and services, the costs of products skyrockets. Healthcare industry, while fairly resilient is not exempt from the influence of such an economic downturn. The increasing costs may deter consumers from seeking medical help when they need it. Especially considering the unfamiliarity with the disease itself, inflation has proven to be challenging for the global Hepatitis D market.

Regional Analysis

North America Holds Region Accounted Significant Share of the Global Hepatitis D Treatment Market

North America dominates the global Hepatitis D market occupying a laudable market revenue share of 52.4%, as compared to the other geographies considered in the year 2023. The region underscores its dominance by virtue of rising burden of hepatitis D, especially in certain population. The region has pockets of high prevalence, including communities with high rates of injection drug use and individuals with chronic hepatitis B infection.

This leads to increased demand for diagnostic tests, treatment options, and specialized care, boosting the dominance of North America. In addition to this, the region comprises advanced healthcare infrastructure, such as well-established healthcare systems, hospitals and clinics. Existence of specialized healthcare professionals, advanced diagnostic technologies and access to specialized treatments adds a plus point for the regions’ growth. Thus, region maintains a steady growth with the continuation of these benefactors in recent years.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Strong Focus On Product Portfolio Expansion Through Various Strategies Maintain the Dominance Of Industry Leaders. Key players in this market are operating several strategies through partnerships, investments in expanding their product portfolio, mergers, and acquisitions, etc. With the presence of several key players across the globe, the Hepatitis D treatment market is fragmented.

New key players are subject to intense competition from leading market players, particularly those with strong brand recognition and high distribution networks. Companies have gained various expansion strategies, partnerships, and development in new research technologies to stay on top of the market.

Hepatitis D Market Key Players

- Merck and Co Inc.

- Gilead Sciences Inc.

- Eiger Bio-pharmaceuticals Inc.

- Antios Therapeutics Inc.

- GlaxoSmithKline Inc.

- Janssen Pharmaceuticals Inc.

- Amega Biotech

- Hepion Pharmaceuticals Inc.

- PharmaEssentia Corporation

- Apotex Corp.

- Aurobindo Pharma Limited

- Zydus Pharmaceuticals

- Mylan N.V.

Recent Development

- In March 2024, Hepion Pharmaceuticals Inc. shared pre-clinical findings on their innovative RNA interference (RNAi) therapeutic candidate aimed at targeting the Hepatitis D virus. This presentation at a prominent scientific conference underscores Hepion’s strides in developing cutting-edge treatment modalities for Hepatitis D.

- In October 2023, Mylan N.V., finalized the acquisition of generic drug manufacturer Strides Pharma Science Ltd. This strategic move may enhance their ability to produce and distribute cost-effective medications for Hepatitis D in specific regions.

- In June 2023, Eiger Bio-Pharmaceuticals Inc. revealed encouraging outcomes from the phase 2 trial assessing peginterferon lambda in conjunction with ribavirin for chronic Hepatitis D infection treatment. This advancement sets the stage for potential phase 3 trials, indicating a promising avenue for a novel treatment option in the market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 0.7 Billion |

| Forecast Revenue (2033) | USD 1.0 Billion |

| CAGR (2024-2033) | 3.34% |

| Base Year for Estimation | 2022 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Impact of macroeconomic factors, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Acute, Chronic), By Diagnosis (Blood Tests, Elastography, Liver Biopsy, Serologic Testing, Others), By Distribution Channel (Hospital pharmacies, Retail pharmacies, Online Pharmacies) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherland, Rest of Europe; APAC- China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- South Africa, Saudi Arabia, UAE & Rest of MEA |

| Competitive Landscape | Merck and Co Inc., Gilead Sciences Inc., Eiger Bio-pharmaceuticals Inc., Antios Therapeutics Inc., GlaxoSmithKline Inc., Janssen Pharmaceuticals Inc., Amega Biotech, Hepion Pharmaceuticals Inc., PharmaEssentia Corporation, Apotex Corp., Aurobindo Pharma Limited, Zydus Pharmaceuticals, Mylan N.V. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |