Global Hemostasis Products Market By Product Type (Topical, Infusible and Advanced), By Application (Surgery, Myocardial Infarction, Trauma, Hemophilia and Others), By End-user (Hospitals, ASCs and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179145

- Number of Pages: 374

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

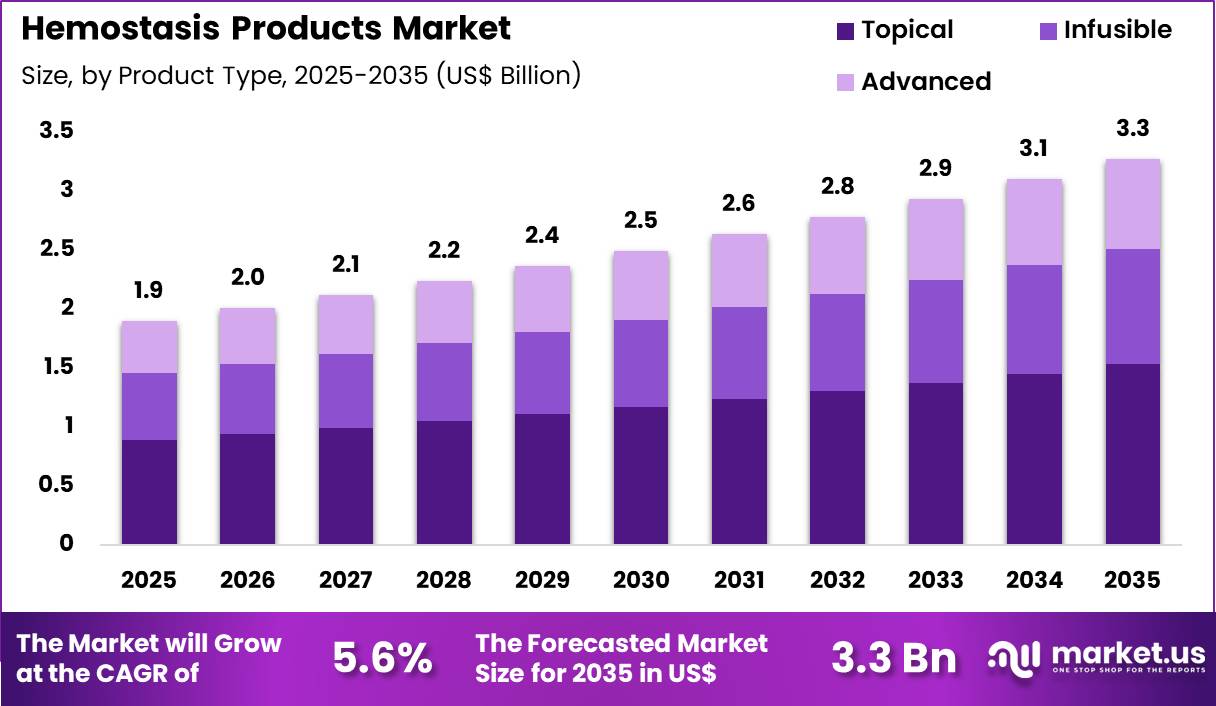

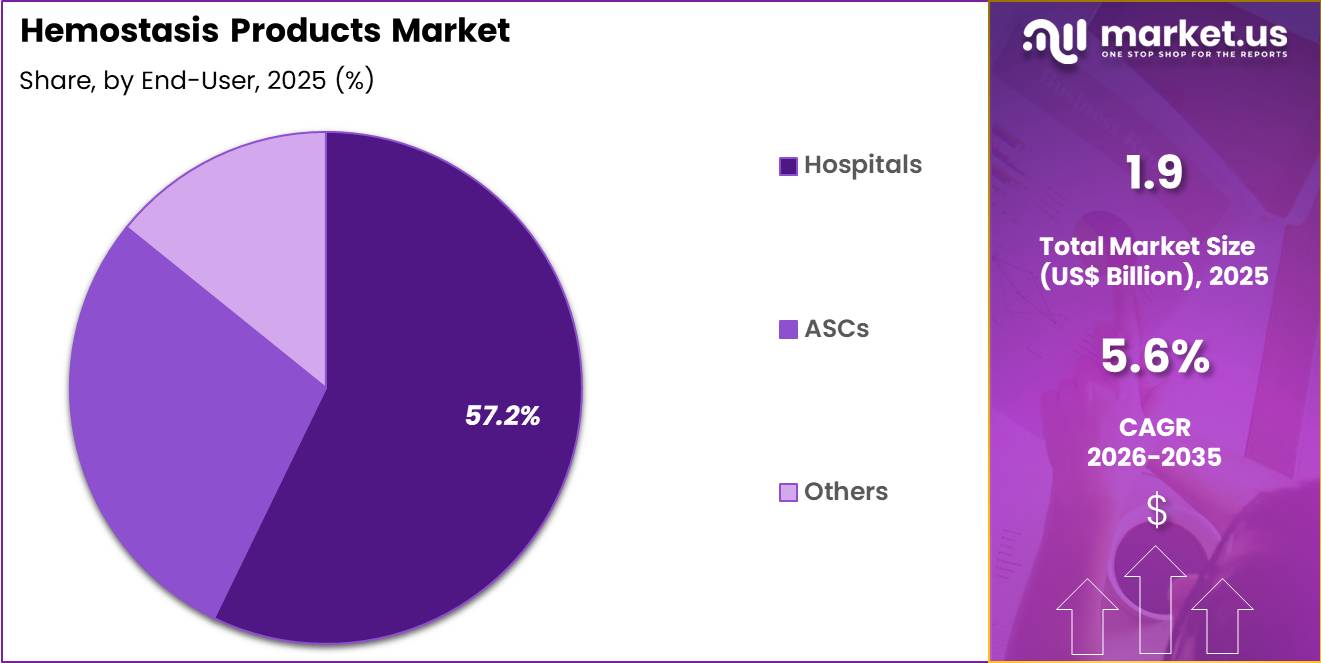

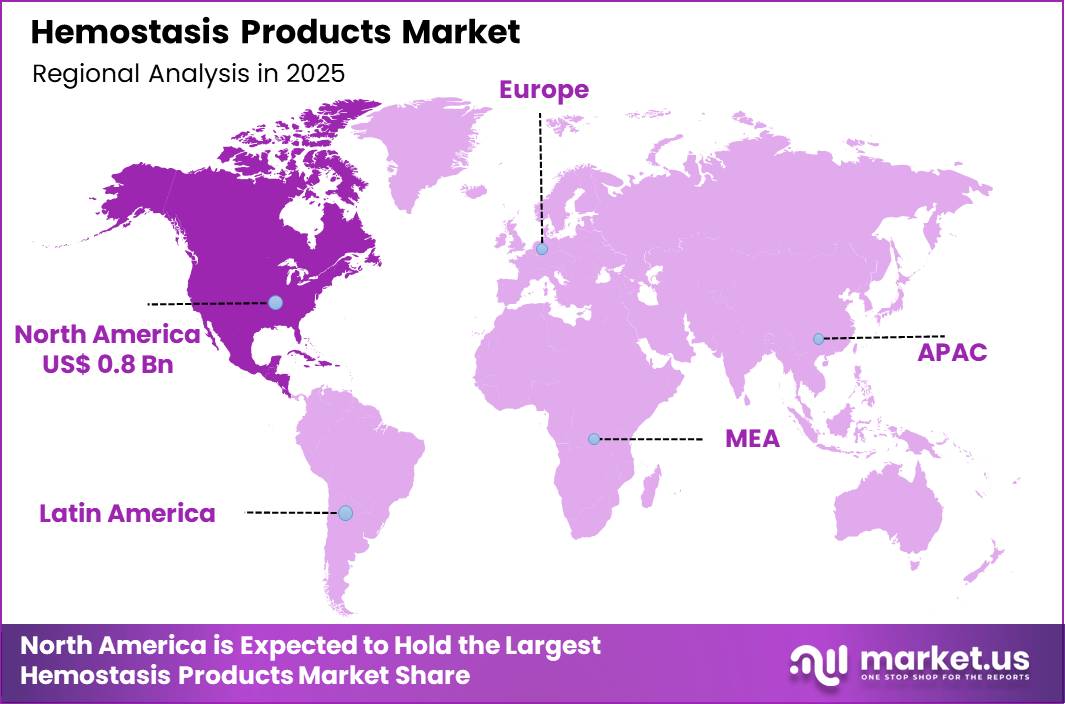

The Global Hemostasis Products Market size is expected to be worth around US$ 3.3 Billion by 2035 from US$ 1.9 Billion in 2025, growing at a CAGR of 5.6% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 41.3% share with a revenue of US$ 0.8 Billion.

Increasing prevalence of surgical procedures and trauma cases drives the hemostasis products market as healthcare providers prioritize rapid bleeding control to minimize blood loss and enhance patient outcomes. Surgeons increasingly apply topical hemostatic agents like fibrin sealants during cardiovascular surgeries to secure vessel anastomoses and prevent postoperative hematomas in coronary artery bypass grafting.

These products support orthopedic interventions by using gelatin sponges and oxidized cellulose to manage oozing in joint replacements and spinal fusions, ensuring clear surgical fields and reducing transfusion needs. Clinicians utilize mechanical hemostats such as absorbable clips and ligatures in gastrointestinal procedures to close bleeding sites during endoscopic resections or bowel anastomoses.

Hemostasis powders and sprays find applications in emergency trauma care, where providers deploy them to arrest diffuse hemorrhage in abdominal or thoracic wounds. In obstetrics, these solutions enable effective management of postpartum hemorrhage through intrauterine balloon tamponade combined with pharmacological hemostatics.

Manufacturers pursue opportunities to develop bioengineered hemostats with antimicrobial properties, expanding applications in infected wounds and high-risk surgical sites to lower sepsis rates. Developers advance nanoparticle-infused gels that provide sustained release of clotting factors, broadening utility in minimally invasive and robotic surgeries where precision delivery remains critical.

These innovations facilitate hybrid products combining mechanical and biological mechanisms for enhanced efficacy in neurosurgical hemostasis. Opportunities emerge in portable, ready-to-use kits for field trauma response, addressing pre-hospital bleeding control.

Companies invest in sustainable, plant-derived alternatives to reduce allergen risks. Recent trends emphasize smart hemostats with integrated sensors for real-time clotting feedback and AI-guided application, positioning the market for growth in value-based care focused on efficiency and reduced complications.

Key Takeaways

- In 2025, the market generated a revenue of US$ 1.9 Billion, with a CAGR of 5.6%, and is expected to reach US$ 3.3 Billion by the year 2035.

- The product type segment is divided into topical, infusible and advanced, with topical taking the lead with a market share of 46.8%.

- Considering application, the market is divided into surgery, myocardial infarction, trauma, hemophilia and others. Among these, surgery held a significant share of 38.9%.

- Furthermore, concerning the end-user segment, the market is segregated into hospitals, ASCs and others. The hospitals sector stands out as the dominant player, holding the largest revenue share of 57.2% in the market.

- North America led the market by securing a market share of 41.3%.

Product Type Analysis

Topical products accounted for 46.8% of growth within product type and led the hemostasis products market due to widespread use in surgical and emergency settings. Surgeons rely on topical agents to control bleeding quickly during open and minimally invasive procedures.

These products offer rapid clot formation and ease of application, which strengthens operating room efficiency. Increasing surgical volumes across cardiovascular, orthopedic, and general procedures further expand demand.

Growth accelerates as manufacturers develop bioactive and absorbable formulations that enhance safety and healing. Rising adoption of minimally invasive techniques increases the need for localized bleeding control solutions.

Hospitals prefer topical agents that reduce procedure time and transfusion requirements. Ongoing clinical research supports broader indications for advanced topical sealants. The segment is expected to remain dominant as surgical innovation and patient safety priorities continue to advance.

Application Analysis

Surgery generated 38.9% of growth within application and emerged as the leading segment due to rising global surgical procedures. Expanding access to elective and emergency surgeries increases demand for effective hemostatic solutions. Surgeons prioritize bleeding management to minimize complications and shorten hospital stays. Complex procedures in oncology and cardiovascular care require reliable intraoperative bleeding control.

Growth strengthens as aging populations undergo more surgical interventions. Technological advancements improve precision in surgical techniques, which raises the need for adjunct hemostatic products. Enhanced recovery protocols emphasize reduced blood loss and faster healing.

Hospitals integrate standardized bleeding management protocols into perioperative care. The segment is projected to maintain leadership as procedural volumes continue to expand worldwide.

End-User Analysis

Hospitals contributed 57.2% of growth within end-user and dominated the hemostasis products market due to high surgical throughput and advanced care infrastructure. Tertiary and quaternary hospitals perform complex procedures that require dependable bleeding control solutions.

Emergency departments and trauma units maintain consistent demand for rapid hemostatic interventions. Multidisciplinary surgical teams rely on comprehensive product portfolios for diverse procedures.

Growth continues as hospitals expand specialty departments such as cardiac surgery and transplant units. Investment in modern operating theaters increases procurement of advanced hemostatic agents. Clinical training programs enhance surgeon familiarity with new products. Strict patient safety standards drive consistent product utilization. The segment is anticipated to sustain its leadership as hospitals remain the primary centers for surgical and critical care services.

Key Market Segments

By Product Type

- Topical

- Infusible

- Advanced

By Application

- Surgery

- Myocardial Infarction

- Trauma

- Hemophilia

- Others

By End-user

- Hospitals

- ASCs

- Others

Drivers

Rising demand for minimally invasive surgical techniques is driving the market.

The increasing preference for minimally invasive procedures has substantially elevated the demand for advanced endoscopy visualization systems that provide high-definition imaging and enhanced maneuverability. Surgeons require superior visualization to perform delicate interventions with greater precision and reduced tissue trauma.

Healthcare facilities are upgrading their endoscopy suites to support complex laparoscopic and endoscopic surgeries. The correlation between minimally invasive approaches and shorter recovery times further accelerates adoption of these systems. Government policies promoting outpatient care encourage the use of visualization tools that enable same-day procedures.

Endoscopy systems with 4K resolution and narrow-band imaging improve detection of subtle mucosal changes. National surgical guidelines emphasize the importance of high-quality imaging in modern endoscopy. Key manufacturers continue to refine camera heads and processors to meet evolving clinical expectations. This driver supports long-term investment in endoscopy infrastructure across hospitals and ambulatory centers.

Restraints

Limited reimbursement for advanced endoscopic procedures is restraining the market.

Inconsistent or inadequate reimbursement policies for advanced endoscopic procedures create financial disincentives for healthcare providers to invest in premium visualization systems. Many payers apply restrictive criteria or lower payment rates for endoscopic procedures using high-definition or specialized imaging technologies.

Hospitals and ambulatory surgery centers face challenges justifying capital investments when revenue recovery remains uncertain. Regulatory bodies often delay updates to reimbursement schedules for emerging endoscopic innovations. This restraint particularly affects independent endoscopy centers and smaller group practices with limited financial flexibility.

Providers may continue using conventional systems to avoid potential revenue shortfalls. Economic pressures from rising operational costs further complicate budget planning for equipment upgrades. Advocacy efforts to expand coverage have achieved only partial success.

Despite clear clinical advantages, reimbursement limitations slow the replacement cycle of older visualization systems. Insufficient reimbursement for advanced endoscopic procedures remains a primary market restraint.

Opportunities

Rapid growth of outpatient endoscopy centers is creating growth opportunities.

The expanding network of dedicated outpatient endoscopy centers presents significant potential for endoscopy visualization systems in community-based diagnostic and therapeutic settings. Governmental policies supporting ambulatory surgery reimbursement encourage the establishment of standalone endoscopy facilities.

Patients increasingly prefer convenient, lower-cost outpatient procedures over hospital-based interventions. Partnerships between endoscopy centers and device manufacturers facilitate customized visualization solutions for high-volume practices. The large volume of routine endoscopic examinations in outpatient settings magnifies demand for efficient imaging systems.

Educational programs for gastroenterologists promote standardized use of advanced visualization in ambulatory environments. This opportunity allows manufacturers to develop compact, high-performance systems optimized for office-based procedures. Leading companies are expanding product lines with features tailored for outpatient workflows.

Overall, outpatient growth aligns with efforts to reduce healthcare costs and improve patient access. The proportion of endoscopic procedures performed in outpatient settings increased notably between 2022 and 2024.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the hemostasis products market through hospital procurement priorities, surgical volumes, and reimbursement dynamics. Inflation increases costs for biologic materials, collagen, thrombin, and synthetic polymers, which raises production and purchasing expenses.

Higher interest rates tighten capital availability for healthcare providers, which slows bulk inventory purchases and new product adoption. Geopolitical tensions affect global sourcing of raw materials, sterile packaging, and manufacturing inputs, creating supply variability and delivery delays.

Current US tariffs on imported medical components and biologic processing materials elevate landed costs and compress supplier margins. These financial pressures can delay contract renewals and limit expansion into cost sensitive markets.

At the same time, providers strengthen domestic sourcing strategies and focus on clinically proven products to justify spending. Growing surgical procedures and trauma care demand continue to sustain consistent utilization, supporting stable long term market growth.

Latest Trends

Introduction of single-use duodenoscopes is a recent trend in the market.

In 2024, the adoption of single-use duodenoscopes has transformed infection control practices in endoscopic retrograde cholangiopancreatography procedures. These disposable devices eliminate reprocessing requirements and reduce the risk of patient-to-patient transmission.

Manufacturers have prioritized optical quality and maneuverability comparable to reusable models. Clinical evaluations in 2024 confirmed equivalent performance in diagnostic and therapeutic ERCP. Boston Scientific launched the EXALT Model D Single-Use Duodenoscope in 2024, expanding its single-use portfolio for advanced endoscopy.

This development addresses longstanding concerns about duodenoscope-related infections. The trend emphasizes cost-effectiveness for high-risk procedures in infection-sensitive populations. Regulatory clearances in 2024 for single-use duodenoscopes have accelerated clinical integration.

Industry collaborations optimize working channel design for therapeutic accessories. These innovations aim to enhance patient safety while maintaining procedural efficacy in gastroenterology practice.

Regional Analysis

North America is leading the Hemostasis Products Market

North America accounted for 41.3% of the Hemostasis Products market, reflecting strong procedural volumes and rapid adoption of advanced surgical technologies in 2024. The region benefits from a high number of complex cardiovascular, orthopedic, and trauma surgeries that require reliable bleeding control solutions.

According to the American Society of Plastic Surgeons, surgeons performed 1.6 million cosmetic surgical procedures in the United States in 2023, highlighting sustained operative activity that directly supports demand for topical sealants, patches, and adjunctive hemostatic agents. Hospitals continue to prioritize blood management protocols to reduce transfusion rates and shorten operating time.

Favorable reimbursement systems and well-established hospital infrastructure encourage the routine use of premium surgical adjuncts. Leading manufacturers actively expand product portfolios through innovation in absorbable materials and combination sealant technologies.

Trauma incidence and elective procedure backlogs cleared after the pandemic have further increased utilization rates. These structural clinical and institutional drivers have strengthened regional growth momentum throughout 2024.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to witness strong expansion during the forecast period as surgical access, healthcare investment, and trauma management capacity improve across major economies. India’s Ministry of Road Transport and Highways reported 461,312 road accidents in 2022, emphasizing the substantial trauma burden that requires rapid bleeding control in emergency settings.

Governments across China, India, Japan, and Southeast Asia are upgrading tertiary hospitals and expanding insurance coverage for surgical care. Surgeons increasingly adopt advanced sealants and hemostatic matrices to improve operative outcomes and reduce complications.

Medical tourism hubs such as Thailand and India attract rising volumes of elective and reconstructive procedures, which support greater product utilization. Local manufacturers are strengthening domestic production capabilities to meet rising hospital demand.

Training initiatives and technology partnerships are improving surgeon familiarity with modern bleeding control solutions. Expanding surgical capacity, trauma incidence, and healthcare modernization efforts are projected to sustain steady regional growth in the coming years.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the hemostasis products market grow by advancing formulations and delivery systems that accelerate clot formation, improve handling in surgical settings, and reduce bleeding-related complications across specialties such as trauma, cardiovascular, and orthopedics. They also strengthen their value propositions by combining hemostatic agents with adhesives and sealants that support comprehensive wound management and procedural efficiency.

Firms expand reach through training programs, surgeon engagement initiatives, and procedural support services that deepen clinical confidence and drive product preference in high-volume care pathways. Strategic partnerships with hospital networks, surgical centers, and group purchasing organizations help secure preferred supplier agreements and stable demand.

Ethicon, a subsidiary of Johnson & Johnson, exemplifies a diversified medical technology company with a broad portfolio of advanced hemostatic agents, sealants, and surgical solutions backed by extensive global distribution and clinician education efforts.

The company advances its competitive agenda through disciplined investment in R&D, targeted acquisitions that expand complementary offerings, and a customer-focused commercialization strategy that aligns product performance with evolving procedural needs.

Top Key Players

- Johnson & Johnson

- Medtronic

- Baxter International

- B. Braun

- Teleflex

- Integra LifeSciences

- Pfizer

- Zimmer Biomet

- CryoLife

- Smith & Nephew

Recent Developments

- In April 2025, Baxter International Inc. introduced a room-temperature formulation of its Hemopatch Sealing Hemostat. The updated product eliminates the need for refrigerated storage, allowing faster intraoperative use while extending overall shelf stability and logistical flexibility.

- In March 2025, the FDA granted approval for Qfitlia as a routine prophylactic treatment for patients aged 12 years and older with hemophilia A or B. Clinical data supporting the decision demonstrated a 73% reduction in bleeding events, highlighting the therapy’s potential to significantly improve disease management outcomes.

Report Scope

Report Features Description Market Value (2025) US$ 1.9 Billion Forecast Revenue (2035) US$ 3.3 Billion CAGR (2026-2035) 5.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Topical, Infusible and Advanced), By Application (Surgery, Myocardial Infarction, Trauma, Hemophilia and Others), By End-user (Hospitals, ASCs and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Johnson & Johnson, Medtronic, Baxter International, B. Braun, Teleflex, Integra LifeSciences, Pfizer, Zimmer Biomet, CryoLife, Smith & Nephew Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Johnson & Johnson

- Medtronic

- Baxter International

- B. Braun

- Teleflex

- Integra LifeSciences

- Pfizer

- Zimmer Biomet

- CryoLife

- Smith & Nephew

Our Clients

- 179145

- Feb 2026