Quick Navigation

Report Overview

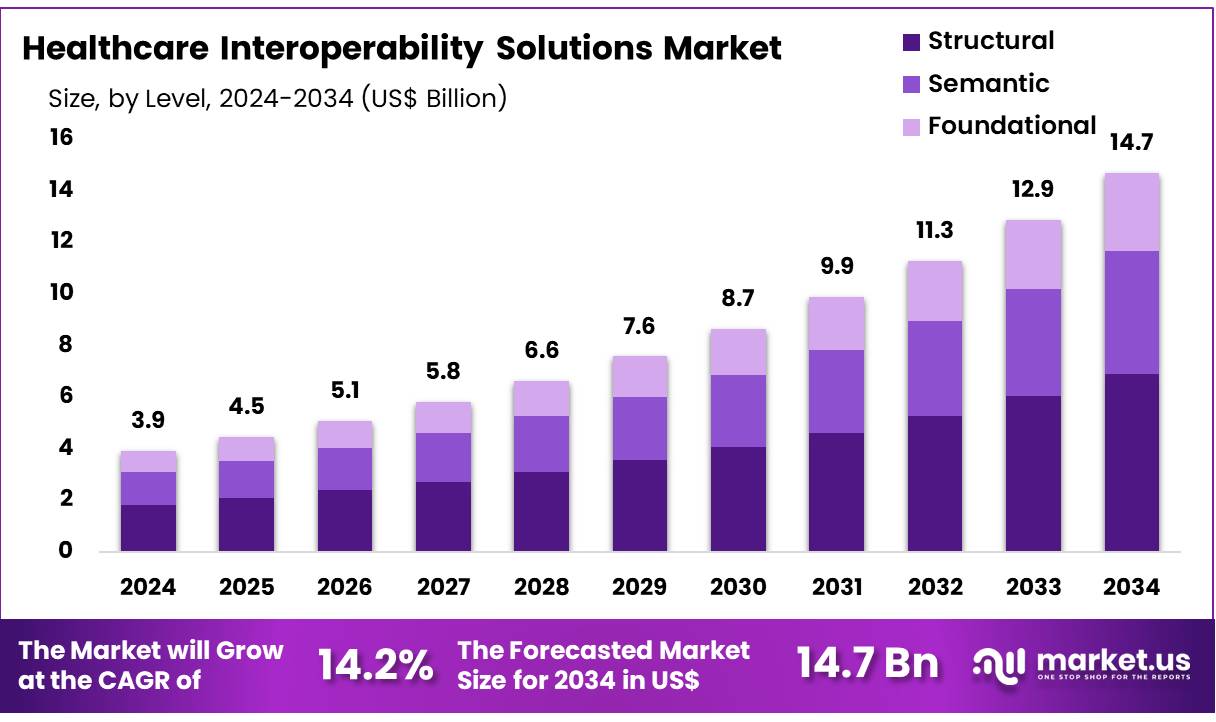

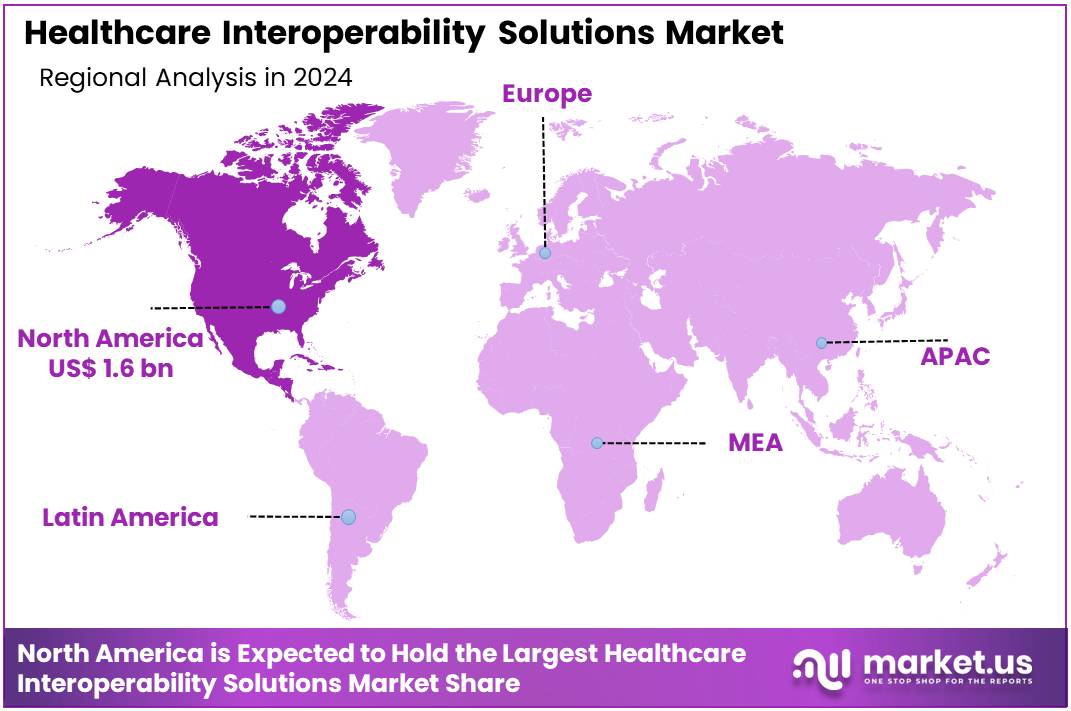

Global Healthcare Interoperability Solutions Market size is expected to be worth around US$ 14.7 billion by 2034 from US$ 3.9 billion in 2024, growing at a CAGR of 14.2% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 41.6% share with a revenue of US$ 1.6 Billion.

Growing adoption of electronic health records (EHRs) and the increasing need for seamless data exchange among healthcare systems are propelling the healthcare interoperability solutions market. Healthcare providers are prioritizing integrated systems to enhance patient care, reduce errors, and improve operational efficiency. Interoperability solutions facilitate the seamless sharing of patient information across various platforms, enabling informed clinical decisions and coordinated care.

A significant opportunity lies in the implementation of standardized data exchange frameworks, such as the Trusted Exchange Framework and Common Agreement (TEFCA). In 2023, over 60% of US hospitals were aware of TEFCA and planned to participate, up from 51% in 2022. This trend indicates a growing commitment to nationwide health information exchange.

Recent advancements include the integration of application programming interfaces (APIs) that allow third-party applications to access EHR data securely, promoting patient engagement and personalized care. The market also benefits from government initiatives aimed at improving healthcare outcomes through enhanced interoperability.

As healthcare systems continue to digitize, the demand for robust interoperability solutions is expected to rise, driving innovation and collaboration among stakeholders. These developments underscore the critical role of interoperability in achieving a cohesive and efficient healthcare ecosystem.

Key Takeaways

- In 2024, the market for healthcare interoperability solutions generated a revenue of US$ 3.9 billion, with a CAGR of 14.2%, and is expected to reach US$ 14.7 billion by the year 2034.

- The product type segment is divided into solutions and services, with services taking the lead in 2023 with a market share of 57.3%.

- Considering level, the market is divided into structural, semantic, and foundational. Among these, structural held a significant share of 46.8%.

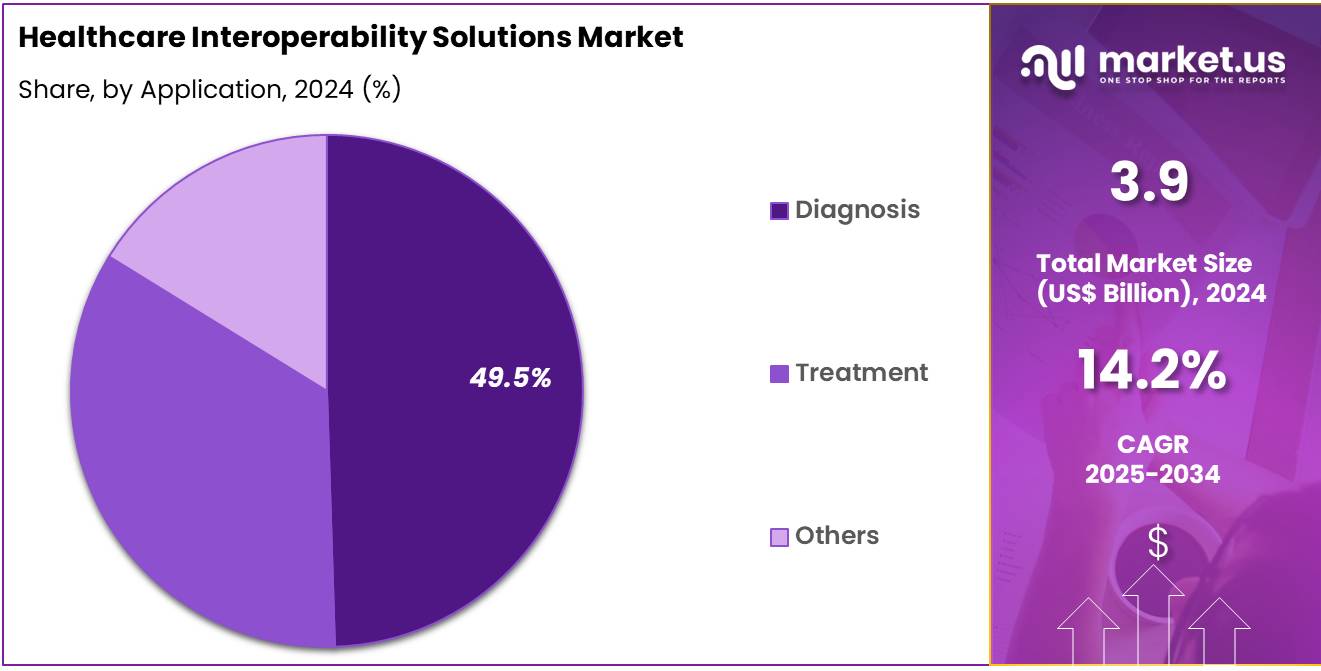

- Furthermore, concerning the application segment, the market is segregated into diagnosis, treatment, and others. The diagnosis sector stands out as the dominant player, holding the largest revenue share of 49.5% in the healthcare interoperability solutions market.

- The deployment segment is segregated into cloud based and on-premise, with the on-premise segment leading the market, holding a revenue share of 52.6%.

- Considering end-user, the market is divided into hospitals, ambulatory surgical centers, and others. Among these, hospitals held a significant share of 58.2%.

- North America led the market by securing a market share of 41.6% in 2023.

Product Type Analysis

The services segment led in 2023, claiming a market share of 57.3% owing to as healthcare organizations increasingly seek support in integrating their systems. The demand for consulting, integration, and managed services is anticipated to rise as healthcare providers and payers focus on streamlining their operations and improving care coordination.

Solutions and services that facilitate seamless data exchange between various healthcare systems are projected to be in high demand. Healthcare institutions are likely to prioritize service providers who can assist with system design, implementation, and ongoing support for interoperability platforms.

The increasing complexity of healthcare IT infrastructure and the need to comply with regulatory standards are expected to further drive the demand for these services. As healthcare organizations prioritize digital transformation, the services segment is projected to see continued growth in the coming years.

Level Analysis

The structural held a significant share of 46.8% due to the growing importance of data standardization in healthcare. The increasing need for standardized healthcare data exchange across different systems is likely to drive the adoption of structural interoperability solutions. With the rise of electronic health records (EHR) and the integration of disparate healthcare systems, healthcare organizations are projected to focus more on structural interoperability to ensure seamless data flow.

This segment’s growth is expected to be supported by regulatory incentives, such as the push for standardized coding and reporting systems. Additionally, the implementation of structural interoperability is likely to improve care coordination, reduce administrative costs, and enhance patient outcomes, all of which are expected to drive its expansion in the healthcare sector.

Application Analysis

The diagnosis segment had a tremendous growth rate, with a revenue share of 49.5% as the demand for accurate and timely diagnostic information increases. The integration of diagnostic data from various sources, including laboratories, imaging centers, and electronic health records, is expected to drive the growth of interoperability solutions for diagnostic purposes.

Healthcare providers are anticipated to increasingly rely on these solutions to ensure that diagnostic information flows seamlessly across platforms, improving decision-making and patient care. The rising adoption of artificial intelligence (AI) and machine learning technologies in diagnostics is likely to boost demand for interoperable solutions that facilitate real-time data access. Furthermore, the growing trend toward personalized medicine and the need for comprehensive diagnostic information are projected to fuel the expansion of this segment.

Deployment Analysis

The on-premise segment grew at a substantial rate, generating a revenue portion of 52.6% due to the ongoing preference for more control over sensitive healthcare data. Healthcare organizations that handle large volumes of patient data often prioritize on-premise deployment to ensure better security and compliance with regulations such as HIPAA. The projected growth of this segment is supported by healthcare providers’ concerns over data privacy and the need to adhere to strict regulatory requirements.

Additionally, on-premise solutions are expected to continue to be a popular choice for organizations with limited internet access or those in regions with unreliable cloud infrastructure. As healthcare institutions seek more customizable and secure solutions for managing patient data, the on-premise segment is anticipated to see sustained demand in the healthcare interoperability market.

End-user Analysis

The hospitals held a significant share of 58.2% due to the increasing focus on improving operational efficiency and patient outcomes. Hospitals are projected to be early adopters of interoperability solutions as they aim to enhance care coordination, streamline workflows, and ensure better access to patient data across departments.

The rising complexity of healthcare delivery, along with the growing need to manage electronic health records and integrate diagnostic information, is expected to drive the adoption of interoperability solutions in hospitals.

Additionally, the increasing number of patients with chronic conditions requiring long-term care is likely to spur demand for seamless information exchange across various healthcare providers. As hospitals invest in digital infrastructure to support the exchange of patient information, the healthcare interoperability solutions market within this segment is anticipated to expand.

Key Market Segments

By Product Type

- Solutions

- HIE Interoperability

- Enterprise Interoperability

- EHR Interoperability

- Others

- Services

By Level

- Structural

- Semantic

- Foundational

By Application

- Diagnosis

- Treatment

- Others

By Deployment

- Cloud Based

- On-premise

By End-user

- Hospitals

- Ambulatory Surgical Centers

- Others

Drivers

Growing Adoption of Electronic Health Records (EHRs) is Driving the Market

The healthcare interoperability solutions market is experiencing significant growth due to the widespread adoption of Electronic Health Records (EHRs). Healthcare providers are increasingly implementing EHR systems to improve patient care and streamline operations. This shift necessitates robust interoperability solutions to facilitate seamless data exchange between disparate systems.

For instance, the Office of the National Coordinator for Health Information Technology (ONC) reported that in 2023, approximately 86% of office-based physicians had adopted EHR systems, up from 78% in 2019. This increase underscores the critical need for interoperability to ensure that patient information is accessible across various healthcare settings.

Interoperable systems enable real-time access to patient data, reducing errors and enhancing clinical decision-making. As EHR adoption continues to rise, the demand for effective interoperability solutions is expected to grow correspondingly.

Restraints

Data Privacy and Security Concerns are Restraining the Market

Despite the benefits of interoperable healthcare systems, data privacy and security concerns pose significant challenges. The exchange of sensitive patient information across platforms raises the risk of data breaches and unauthorized access. In 2022, the US Department of Health and Human Services (HHS) reported over 700 healthcare data breaches affecting more than 52 million individuals.

These incidents highlight vulnerabilities in health information systems and contribute to hesitancy among providers to fully engage in interoperability initiatives. Ensuring compliance with regulations such as the Health Insurance Portability and Accountability Act (HIPAA) adds complexity and cost to implementing interoperable solutions.

Organizations must invest in advanced security measures and continuous monitoring to protect patient data, which can be resource-intensive. Balancing the need for data sharing with stringent privacy protections remains a critical hurdle in advancing healthcare interoperability.

Opportunities

Integration of Artificial Intelligence (AI) is Creating Growth Opportunities

The integration of Artificial Intelligence (AI) into healthcare interoperability solutions presents a significant opportunity for the industry. AI can analyze vast amounts of health data to identify patterns, predict outcomes, and support clinical decisions. In 2023, the National Institutes of Health (NIH) launched the Bridge2AI program, allocating US$130 million to accelerate the use of AI in biomedical and behavioral research.

This initiative aims to create interoperable datasets that AI technologies can leverage to improve health outcomes. By standardizing data and enhancing its accessibility, AI integration facilitates more efficient and accurate information exchange among healthcare systems. This advancement not only improves patient care but also streamlines administrative processes. As AI technologies continue to evolve, their incorporation into interoperability solutions is poised to transform healthcare delivery.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the healthcare interoperability market. Economic growth enables increased investment in health IT infrastructure, facilitating the adoption of interoperability solutions. Conversely, economic downturns can lead to budget constraints, hindering such investments. Geopolitical tensions may disrupt global supply chains, affecting the availability of necessary technologies and components.

For instance, trade disputes can result in tariffs or export restrictions on critical hardware. However, these challenges can also drive innovation, as organizations seek cost-effective and locally sourced solutions. Government policies promoting data sharing and interoperability standards can further stimulate market growth. Overall, while macroeconomic and geopolitical factors present both challenges and opportunities, proactive strategies can help navigate this complex landscape.

Latest Trends

Shift Towards Cloud-Based Solutions is Driving the Market

A notable trend in the healthcare interoperability market is the transition towards cloud-based solutions. Cloud computing offers scalable resources and facilitates easier integration of disparate health information systems. The COVID-19 pandemic accelerated this shift, as remote access to health data became imperative. In 2022, a survey by the Healthcare Information and Management Systems Society (HIMSS) found that 67% of healthcare organizations had increased their adoption of cloud services compared to the previous year.

Cloud-based interoperability solutions enable real-time data sharing and collaboration among healthcare providers, enhancing patient care coordination. Additionally, these solutions often offer cost savings by reducing the need for on-premises infrastructure. As healthcare systems continue to modernize, the adoption of cloud-based interoperability solutions is expected to rise, reflecting a broader trend towards digital transformation in the industry.

Regional Analysis

North America is leading the Healthcare Interoperability Solutions Market

North America dominated the market with the highest revenue share of 41.6% owing to the increasing adoption of electronic health records (EHRs) and health information exchanges (HIEs), which enhanced data sharing among healthcare providers. The US Food and Drug Administration (FDA) reported that about half of all Americans use FDA-approved software applications for managing their healthcare.

Furthermore, the Centers for Medicare & Medicaid Services (CMS) continued to push initiatives promoting interoperability, aiming to improve patient care and reduce costs. The American Telemedicine Association (ATA) reported that telehealth utilization remained 38 times higher than pre-pandemic levels, underscoring the importance of interoperable systems in sustaining virtual healthcare services. This growing reliance on digital health tools, coupled with a shift towards value-based care, drove the demand for seamless data exchange in North America, fueling the market’s growth.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the rising aging population and increasing chronic disease prevalence. According to the National Bureau of Statistics of China, individuals aged 60 and above are projected to account for 21.1% of the total population by 2024, further escalating healthcare demands.

The region is also experiencing rapid digital health adoption, with the World Health Organization (WHO) noting a surge in digital health initiatives aimed at improving access to healthcare. The Indian government’s National Digital Health Mission (NDHM) seeks to create an integrated digital health infrastructure, which will likely facilitate the adoption of interoperability standards.

As healthcare providers increasingly turn to integrated care models, the need for interoperable solutions to coordinate patient information and improve health outcomes will drive further growth in the market.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the healthcare interoperability solutions market focus on developing advanced software platforms and APIs to enable seamless data exchange across different healthcare systems. Companies invest in cloud-based solutions, ensuring secure, real-time access to patient data, and enhancing decision-making capabilities for healthcare providers.

Strategic collaborations with hospitals, insurance companies, and technology firms help expand market reach and improve the adoption of integrated systems. Many players emphasize regulatory compliance, including adherence to health data privacy standards such as HIPAA, to build trust and foster widespread use. Additionally, players explore artificial intelligence and machine learning to enhance data analytics and predictive capabilities.

Cerner Corporation is a leading company in this market, offering a comprehensive suite of interoperability solutions designed to streamline health information exchange. The company focuses on providing secure, scalable systems that enable healthcare providers to access and share patient data efficiently. Cerner’s dedication to advancing healthcare technology through innovation and strong industry partnerships positions it as a key player in the interoperability solutions market.

Top Key Players

- Cerner Corporation

- KMS Healthcare

- Google Cloud

- Allscripts Healthcare Solutions

- IBM Watson Health

- McKesson Corporation

- Epic Systems Corporation

- InterSystems

Recent Developments

- In August 2023, KMS Healthcare launched an advanced health information technology solution aimed at improving data interoperability in medical institutions. This platform enhances connectivity between healthcare systems, streamlining the integration and exchange of patient information.

- In February 2023, Google Cloud teamed up with Redox to enhance healthcare data exchange capabilities. The collaboration simplifies data integration processes, enabling medical organizations to make more informed decisions with greater efficiency.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 3.9 Billion |

| Forecast Revenue (2034) | US$ 14.7 Billion |

| CAGR (2025-2034) | 14.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Solutions (HIE Interoperability, Enterprise Interoperability, EHR Interoperability, and Others), and Services), By Level (Structural, Semantic, and Foundational), By Application (Diagnosis, Treatment, and Others), By Deployment (Cloud Based and On-premise), By End-user (Hospitals, Ambulatory Surgical Centers, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Cerner Corporation, KMS Healthcare, Google Cloud, Allscripts Healthcare Solutions, IBM Watson Health, McKesson Corporation, Epic Systems Corporation, and InterSystems. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |