Quick Navigation

Market Overview

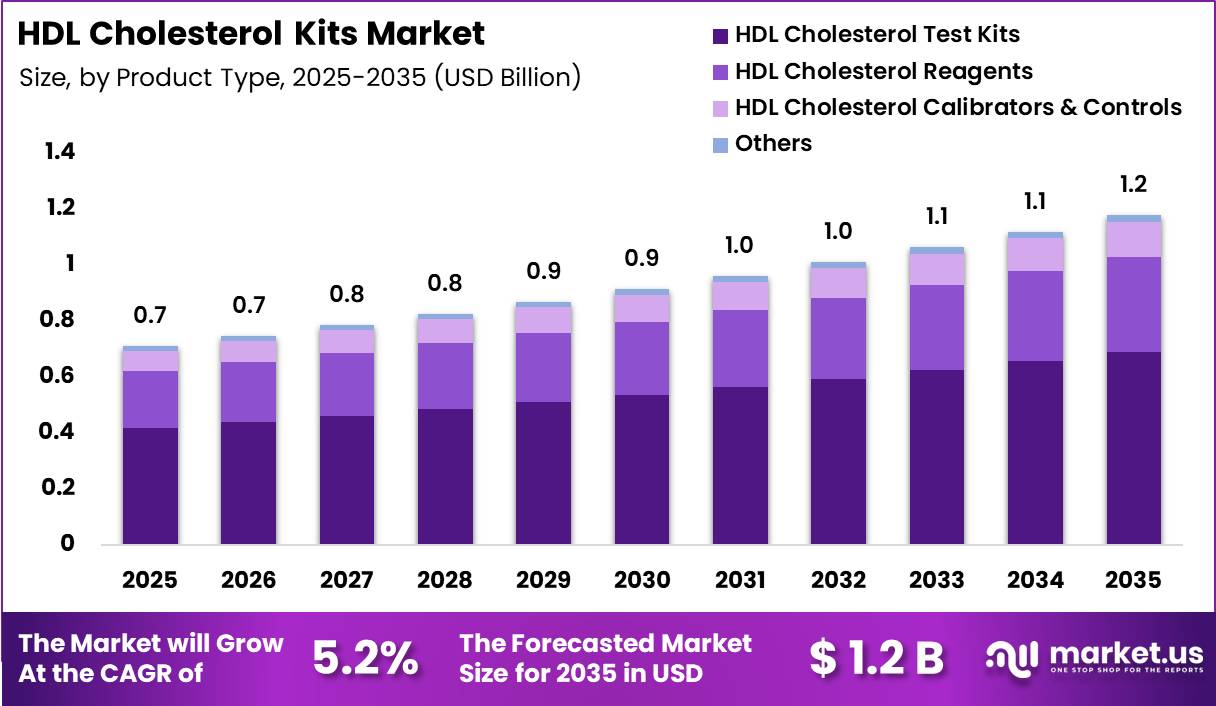

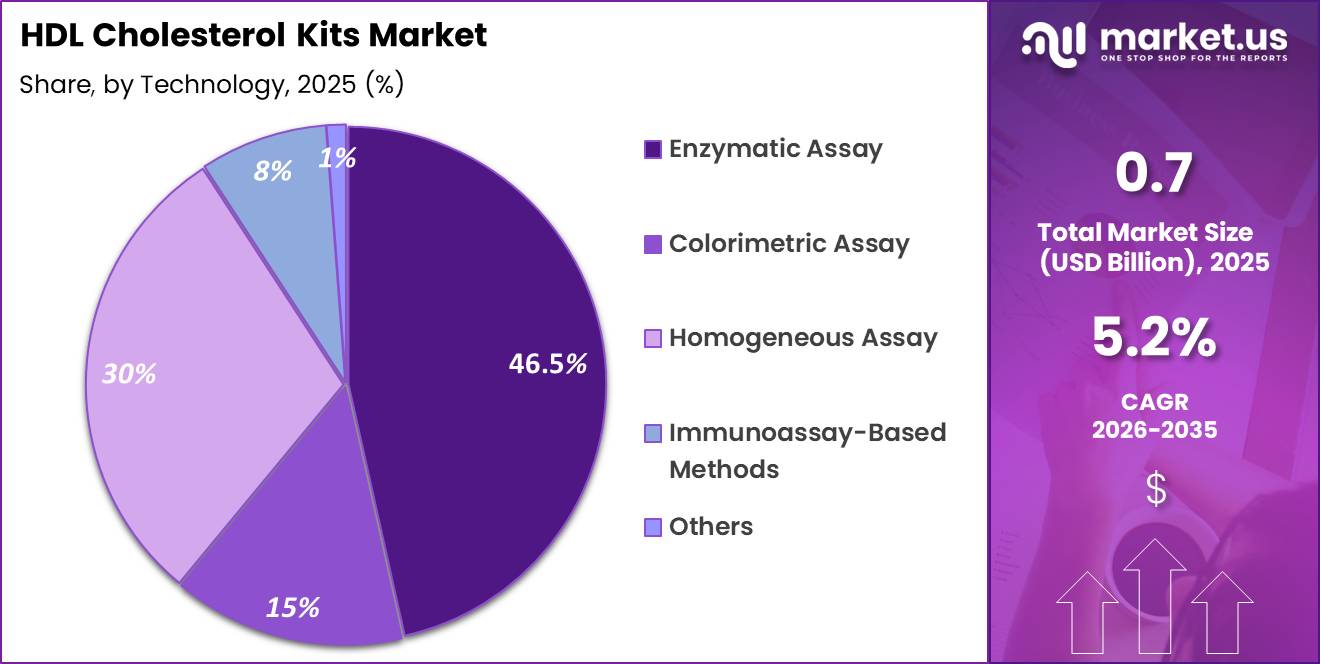

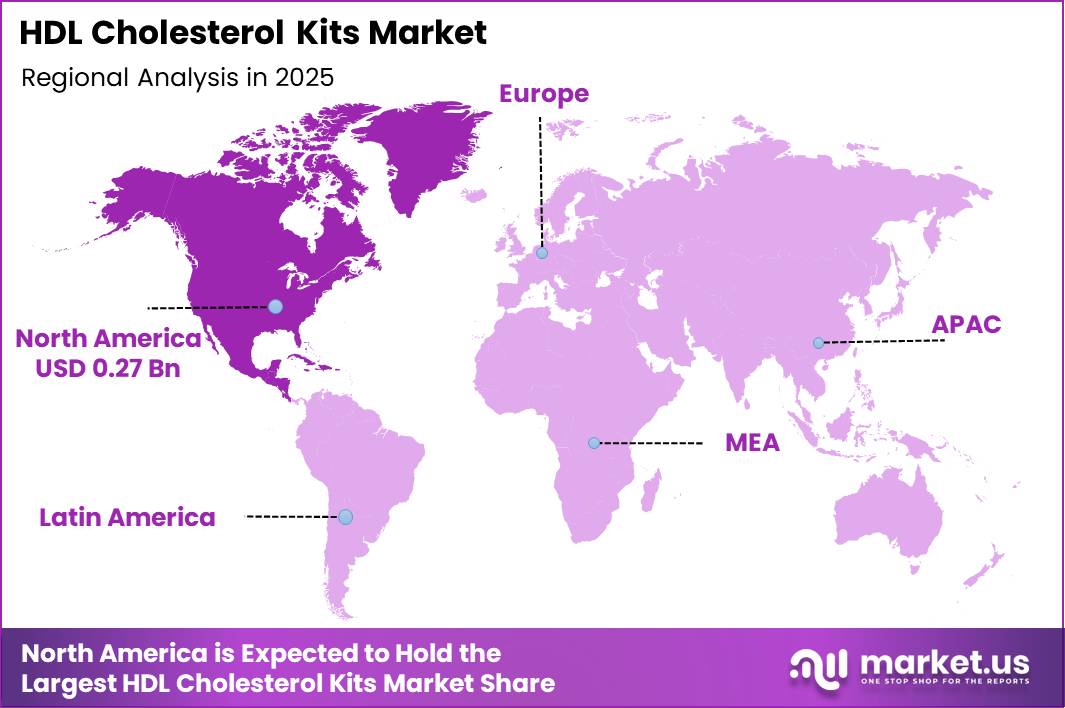

Global HDL Cholesterol Kits Market size is expected to be worth around US$ 1.2 Billion by 2035 from US$ 0.7 Billion in 2025, growing at a CAGR of 5.2% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 37.6% share with a revenue of US$0.27 Billion.

High-density lipoprotein (HDL) cholesterol testing plays a critical role in cardiovascular disease prevention, as HDL helps remove excess cholesterol from the bloodstream and reduces the risk of heart attack and stroke. According to the U.S. Centres for Disease Control and Prevention (CDC), heart disease remains the leading cause of death in the United States, accounting for approximately 695,000 deaths annually. Routine lipid testing, including HDL measurement, is a key tool in identifying at-risk populations.

CDC data indicate that between 2021 and 2023, around 13.8% of U.S. adults aged 20 years and older had low HDL cholesterol levels, defined as less than 40 mg/dL for men and 50 mg/dL for women. HDL cholesterol testing is typically performed as part of a lipid panel, which requires a small blood sample and delivers results within hours using laboratory-based or point-of-care diagnostic kits.

The World Health Organisation (WHO) highlights abnormal blood lipids as a major global risk factor, contributing to an estimated 2.6 million deaths worldwide each year. To ensure the accuracy and comparability of HDL cholesterol results, programs such as the CDC’s Cholesterol Reference Method Laboratory Network support analytical standardisation of cholesterol testing methods.

Healthcare authorities recommend cholesterol screening every 4 to 6 years for adults, with more frequent testing for individuals with diabetes, obesity, or a family history of cardiovascular disease. Growing emphasis on preventive healthcare and early risk detection continues to support sustained utilisation of HDL cholesterol testing kits across clinical and public health settings.

Key Takeaways

- Market Size: The Global HDL Cholesterol Kits Market size was US$ 0.7 billion in 2025. The market is estimated to grow to US$ 1.1 billion by 2035.

- Market Share: The market’s Compound Annual Growth Rate (CAGR) from 2026 to 2035 will be 5.2%

- Product Type: HDL Cholesterol Test Kits has the largest market share, accounting for 58.6% of total product type revenue.

- Technology: Enzymatic Assay leads the segment, accounting for 46.5% of total technology segment revenue.

- Sample Type: Serum leads the segment, accounting for 61.4% of total sample type revenue.

- End User: Diagnostic Laboratories leads the segment, accounting for 45.6% of total end-user revenue.

- Regional: North America is the dominant regional market, accounting for 37.6% of global revenue.

Product Type Analysis

The HDL Cholesterol Kits Market is segmented by product type into HDL Cholesterol Test Kits, HDL Cholesterol Reagents, HDL Cholesterol Calibrators & Controls, and Others. In 2025, HDL Cholesterol Test Kits dominate the market with a 58.6% share, reflecting their widespread adoption across clinical laboratories, hospitals, and point-of-care environments. These kits offer standardised, ready-to-use solutions that support rapid and reliable HDL measurement, making them the preferred choice for routine lipid profiling and large-scale screening programs.

HDL Cholesterol Reagents account for 28.7% of the market, driven by continuous testing demand in high-throughput laboratories that utilise automated analysers. Reagents are essential consumables and generate recurring demand, particularly in centralised diagnostic facilities.

HDL Cholesterol Calibrators & Controls hold a 10.5% share, supported by a growing emphasis on quality assurance, regulatory compliance, and result accuracy in clinical diagnostics. These products are critical for assay validation and instrument calibration.

The Others segment, representing 2.2%, includes accessories and niche testing components with limited but stable demand. Overall, product segmentation reflects a market anchored in routine diagnostic usage, with consumables supporting sustained long-term revenue streams.

Technology Analysis

Based on technology, the HDL Cholesterol Kits Market is segmented into Enzymatic Assay, Homogeneous Assay, Colourimetric Assay, Immunoassay-Based Methods, and Others. In 2025, Enzymatic Assay technology leads with a 46.5% market share, owing to its high accuracy, reproducibility, and compatibility with automated chemistry analysers. Enzymatic assays are widely used in clinical laboratories for standard lipid panels and large patient volumes.

Homogeneous Assays account for 29.8% of the market, benefiting from their ability to directly measure HDL cholesterol without pretreatment steps. This simplifies workflows and reduces turnaround time, making them attractive for high-throughput and routine testing environments.

Colorimetric Assays hold a 14.5% share, supported by their cost-effectiveness and suitability for basic laboratory settings, particularly in resource-limited regions.

Immunoassay-Based Methods represent 8.0%, mainly used in specialised research or reference laboratories where enhanced specificity is required. The Others segment, at 1.2%, includes emerging or hybrid technologies with limited commercial penetration. Overall, technology adoption is driven by the balance between automation compatibility, operational efficiency, and diagnostic accuracy.

Sample Type Analysis

By sample type, the HDL Cholesterol Kits Market is categorised into Serum, Plasma, and Whole Blood. In 2025, Serum-based testing dominates with a 61.4% market share, reflecting its long-standing role as the standard sample type in lipid profiling. Serum samples provide high analytical stability and compatibility with most automated HDL testing platforms, making them the preferred choice in diagnostic laboratories and hospitals.

Plasma samples represent a significant secondary segment, supported by their growing use in emergency and inpatient settings where faster processing is required. Plasma allows HDL testing without the clotting step, reducing sample preparation time and supporting quicker clinical decision-making. This advantage is particularly relevant in acute care environments and high-volume hospitals.

Whole Blood testing accounts for a smaller but expanding share, driven by the rise of point-of-care and decentralised testing models. Whole blood-based HDL kits enable rapid testing with minimal sample processing, supporting screening initiatives, outpatient clinics, and remote healthcare settings. However, variability and lower compatibility with traditional analysers currently limit broader adoption.

Overall, sample type segmentation highlights the dominance of conventional laboratory workflows, while plasma and whole blood samples support evolving testing needs focused on speed and accessibility.

End User Analysis

The HDL Cholesterol Kits Market is segmented by end user into Diagnostic Laboratories, Hospitals, Academic & Research Institutes, Point-of-Care Testing Centres, and Others. In 2025, Diagnostic Laboratories lead the market with a 45.6% share, driven by high test volumes, centralised infrastructure, and routine lipid panel testing. These laboratories benefit from automation, bulk procurement, and consistent demand from preventive health screening programs.

Hospitals represent the second-largest segment, supported by inpatient and outpatient diagnostic services, emergency testing, and chronic disease management. Hospitals increasingly rely on integrated laboratory systems to support cardiovascular risk assessment and treatment monitoring. Academic & Research Institutes contribute a smaller but important share, using HDL testing kits for clinical studies, epidemiological research, and assay development.

Point-of-Care Testing Centres are an emerging growth segment, fueled by demand for rapid, near-patient testing and decentralised healthcare delivery. These centres favour compact, easy-to-use HDL kits that provide quick results.

The Others segment includes public health laboratories and occupational health providers with stable but limited demand. End-user segmentation reflects a market anchored in centralised diagnostics, with expanding opportunities in decentralised and preventive care settings.

Key Market Segments

By Product Type

- HDL Cholesterol Test Kits

- HDL Cholesterol Reagents

- HDL Cholesterol Calibrators & Controls

- Others

By Technology

- Enzymatic Assay

- Homogeneous Assay

- Colorimetric Assay

- Immunoassay-Based Methods

- Others

By Sample Type

- Serum

- Plasma

- Whole Blood

By End User

- Hospitals

- Diagnostic Laboratories

- Academic & Research Institutes

- Point-of-Care Testing Centres

- Others

Driver

Preventive lipid screening expansion in routine care

HDL kit demand is first anchored by the simple fact that HDL-C remains embedded in standard lipid panel workflows used for cardiovascular risk evaluation, not as an isolated assay but as part of broad preventive testing volumes.

Quest Diagnostics’s standard lipid panel explicitly includes HDL-C, LDL-C, non-HDL-C, triglycerides, total cholesterol, and the cholesterol/HDL-C ratio, which indicates that every expansion in routine lipid screening directly lifts HDL reagent pull-through in core lab settings.

U.S. Food and Drug Administration consumer guidance also still frames cholesterol testing as a recurring adult screening activity and references HDL targets of at least 40 mg/dL, reinforcing ongoing public health relevance even though risk assessment has become more multi-parameter in recent years.

In commercial terms, this supports steady annual demand for HDL reagents in hospitals, diagnostic chains, and physician office networks because the assay is seldom purchased alone; it rides inside the higher-volume lipid-testing basket, which improves distributor economics, analyser utilisation, and reorder frequency.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preventive lipid screening expansion in routine care | +1.4% | North America core, EU5, Japan, urban China, GCC | Short term (≤ 2 years) |

| Automated chemistry platforms improving HDL test throughput | +1.1% | North America, Western Europe, China, India, tier-1 labs, South Korea | Short term (≤ 2 years) |

| Cardiovascular risk management protocols sustaining repeat lipid panels | +1.3% | North America core, EU, Australia, Japan, select LATAM private systems | Medium term (2-4 years) |

| Consumer and decentralised cholesterol testing broadening access | +0.8% | U.S., UK, Germany, Nordics, urban APAC retail-health channels | Medium term (2-4 years) |

| EU IVDR and quality compliance forcing kit replacement cycles | +0.9% | EU, EEA, UK spill-over, export-oriented manufacturers in APAC | Medium term (2-4 years) |

| Shift toward expanded lipid analytics lifting bundled HDL demand | +0.7% | U.S. speciality labs, EU referral labs, Japan, advanced APAC hospital networks | Long-term (≥ 4 years) |

Challenge

Shortage of skilled laboratory testing personnel

The HDL cholesterol kits market faces a persistent operating challenge from the shortage of trained laboratory personnel, particularly across clinical chemistry workflows where routine lipid testing competes with higher-priority testing volumes for bench time, validation attention, and technician hours; this does not stop current kit sales, but it steadily limits scalable throughput, slows instrument utilisation, and raises repeat-run risk.

Global health system staffing projections continue to indicate a broad healthcare worker shortfall through 2030 under the World Health Organisation, while laboratory-specific education pipelines remain narrower than replacement demand, especially in higher-income regions with ageing technical workforces.

In practical terms, laboratories running with even a mid-single-digit vacancy rate can experience 6–12% lower effective testing throughput, longer sample batching cycles, overtime-driven labour cost inflation in the high single digits, and slower onboarding of new assay formats, which together justify an estimated 1.1% point drag on the market’s achievable growth path.

The strategic response is not simple hiring alone; manufacturers and providers must reduce manual dependence through auto-calibration, simplified reagent handling, integrated QC, remote support layers, and workflow redesign that lowers the number of manual interventions per 100 tests, thereby protecting adoption momentum even when labour supply remains structurally tight.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Lab workforce scarcity | -1.1% | North America core, Western Europe, urban Asia | Long term (≥ 4 years) |

| Regulatory documentation burden | -0.8% | EU regulatory hubs, UK, selected APAC import markets | Medium term (2–4 years) |

| Reagent input volatility | -0.8% | US, EU, China-linked supply chains, ASEAN corridors | Medium term (2–4 years) |

| Decentralised testing transition | -0.7% | North America, Japan, South Korea, Western Europe | Medium term (2–4 years) |

| Cold-chain distribution friction | -0.6% | APAC export routes, Latin America, Middle East, Africa | Medium term (2–4 years) |

| Data interoperability gaps | -0.5% | Hospital networks globally, integrated diagnostics systems | Long term (≥ 4 years) |

Restraints

Reimbursement-driven pricing and margin compression pressures

A core restraint for the HDL cholesterol kits market is that demand is tied less to a premium stand-alone assay and more to routine lipid testing economics, which keeps pricing exposed to payer control and procurement scrutiny rather than allowing sustained value-based price expansion.

The Centres for Medicare & Medicaid Services have already signalled that while there is no phase-in reduction in 2026, Clinical Laboratory Fee Schedule payment reductions of up to 15% per year may apply from 2027 to 2029, which pushes laboratories and distributors to lock in lower-cost supply contracts ahead of the actual reimbursement reset.

Because lipid testing is usually purchased as part of a broader chemistry workflow, manufacturers face margin compression when freight, labour, packaging, and QA costs rise faster than reimbursement-linked selling prices, and that dynamic reduces reorder intensity, narrows room for distributor markups, and delays decentralised testing rollout, supporting an estimated -1.2% drag on forecast CAGR versus an unconstrained base case.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement pressure | -1.2% | North America core | Medium term |

| Regulatory complexity | -1.0% | US, EU, selected APAC | Short term |

| Consumable cost inflation | -1.3% | US, EU, APAC corridors | Short term |

| Lab capacity constraints | -0.9% | North America, EU core | Medium term |

| Shift to broader lipid menus | -1.1% | North America, EU, urban APAC | Medium term |

| Consumer trust limitations | -0.8% | US retail, EU consumer health | Short term |

Opportunity

Direct-to-consumer lipid subscriptions

This is an opportunity rather than a current driver because baseline HDL kit demand is still largely episodic, physician-triggered, and transaction-based, while subscription monitoring converts a low-frequency consumables category into a recurring revenue model tied to adherence, coaching, and repeat risk reassessment.

With most healthy adults still guided to check cholesterol only every 4 to 6 years in routine care, the white space is not the existence of testing but the monetisation of interim self-tracking among statin users, weight loss program enrollees, cardiometabolic consumers, and high-risk households.

A credible upside case comes from shifting even 6% to 9% of existing self pay lipid test users into 2 to 4 test annual plans, which can lift annual revenue per user by roughly 2.3x to 3.8x, raise gross margin 400 to 700 basis points through strip replenishment economics, and reduce customer acquisition cost payback from about 14 months to 8 to 10 months when bundled with app based reminders and digital interpretation.

In markets where home kits already retail from roughly $25 upward, subscription tiers around $79 to $149 per year can create a materially larger serviceable obtainable market without depending on new guideline changes.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Direct-to-consumer lipid subscriptions | +2.4% | North America core, EU, urban APAC | Short term |

| HDL-plus biomarker bundles | +2.1% | US, EU5, Japan, South Korea, GCC | Short term |

| Retail pharmacy screening networks | +1.8% | North America, UK, Australia, India metros | Medium term |

| Emerging-market micro-lab formats | +2.7% | APAC emerging, Latin America, Africa urban corridors | Medium term |

| Employer and insurer prevention contracts | +1.9% | US, EU, GCC, developed APAC | Medium term |

| Roll-up of fragmented kit brands and strip supply | +1.6% | Global, with US/EU manufacturing hubs | Long term |

Regional Analysis

In 2025, North America led the HDL Cholesterol Kits Market, capturing over 37.6% of the share with a revenue of US$ 0.27 billion. The region’s dominance is driven by a high prevalence of cardiovascular diseases, strong preventive healthcare practices, and widespread adoption of routine lipid screening.

North America benefits from well-established diagnostic laboratory networks, advanced clinical infrastructure, and strong adherence to cholesterol screening guidelines, which collectively support consistent demand for HDL cholesterol testing kits in hospitals and diagnostic centres.

Europe ranks as the second-largest regional market, bolstered by government-led cardiovascular prevention programs, an aging population, and an increasing emphasis on early detection of dyslipidemia. Countries across Western Europe demonstrate high testing volumes due to structured primary care systems and regular health check-up initiatives, while Eastern Europe is experiencing gradual growth as access to diagnostics improves.

The Asia Pacific region is expected to witness the fastest growth, driven by rising incidences of lifestyle-related disorders such as obesity, diabetes, and heart disease. Key factors contributing to market expansion in this region include an expanding healthcare infrastructure, growing awareness of preventive diagnostics, and an increasing presence of private diagnostic laboratories. Additionally, large population bases further amplify the demand for testing.

Latin America shows steady market development, supported by improving diagnostic capabilities and the gradual expansion of preventive healthcare services. Meanwhile, the Middle East and Africa region holds a smaller share due to limited access to routine screening in certain areas. However, ongoing investments in healthcare and public health initiatives are expected to foster long-term growth in this region.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

Suppliers in the global HDL cholesterol kits market pursue competitive advantage through assay technology innovation that improves analytical sensitivity, specificity, and resistance to interference from complex biological samples such as lipemic, hemolyzed, and icteric specimens.

Strategic priorities include homogeneous assay platforms enabling direct HDL measurement without precipitation, point-of-care kit miniaturisation for rapid bedside and clinic-level testing, and expanded compatibility with automated analysers to support high-throughput laboratory workflows.

At the same time, companies are investing in international regulatory approvals, including CE IVD and FDA 510(k), generating clinical validation data across diverse populations, and strengthening procurement relationships with hospital laboratories, clinical chemistry chains, and reference labs.

Growing adoption of comprehensive lipid panels that measure HDL, LDL, total cholesterol, and triglycerides in a single automated run is sustaining demand for high-quality HDL reagent systems compatible with major clinical chemistry analysers through 2035.

Top Key Players

- Abbott Laboratories

- Randox Laboratories Ltd.

- Thermo Fisher Scientific Inc.

- Abcam PLC

- Merck KGaA

- PerkinElmer Inc.

- Diazyme Laboratories Inc.

- Cell Biolabs Inc.

- Oscar Medicare Pvt. Ltd.

- BioVision Inc.

- Cayman Chemical Company

- Wako Pure Chemical Industries, Ltd.

- Sekisui Diagnostics

- Beckman Coulter Inc.

- Sigma-Aldrich (Part of Merck)

- Other Key Players

Recent Developments

- In February 2026, Randox Laboratories expanded its HDL cholesterol reagent portfolio with a new homogeneous assay format compatible with major automated clinical chemistry analyser platforms, targeting diagnostic laboratory institutional buyers seeking streamlined lipid panel testing workflows.

- In March 2026, Thermo Fisher Scientific secured a multi-year HDL cholesterol reagent supply agreement with a leading European clinical laboratory network, covering automated analyser-compatible reagent procurement across its regional diagnostic laboratory institutional buyer base.

- In May 2026, Beckman Coulter launched its next-generation point-of-care HDL cholesterol testing platform targeting primary care clinics and physician office laboratory buyers seeking rapid bedside lipid panel testing capability without centralised laboratory infrastructure requirements.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 0.7 Billion |

| Forecast Revenue (2035) | US$ 1.2 Billion |

| CAGR (2026-2035) | 5.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (HDL Cholesterol Test Kits, HDL Cholesterol Reagents, HDL Cholesterol Calibrators & Controls, Others), By Technology (Enzymatic Assay, Homogeneous Assay, Colorimetric Assay, Immunoassay-Based Methods, Others), By Sample Type (Serum, Plasma, Whole Blood), By End User (Hospitals, Diagnostic Laboratories, Academic & Research Institutes, Point-of-Care Testing Centers, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Abbott Laboratories, Randox Laboratories Ltd., Thermo Fisher Scientific Inc., Abcam PLC, Merck KGaA, PerkinElmer Inc., Diazyme Laboratories Inc., Cell Biolabs Inc., Oscar Medicare Pvt. Ltd., BioVision Inc., Cayman Chemical Company, Wako Pure Chemical Industries, Ltd., Sekisui Diagnostics, Beckman Coulter Inc., Sigma-Aldrich (Part of Merck), Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |