Global Glufosinate Market Size, Share, And Industry Analysis Report By Formulation Type (Aqueous Suspension, Liquid, Suspension Concentrate, Soluble (Liquid) Concentrate), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables), By Application (Herbicides, Fungicides, Desiccant, Defoliant), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180787

- Number of Pages: 247

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

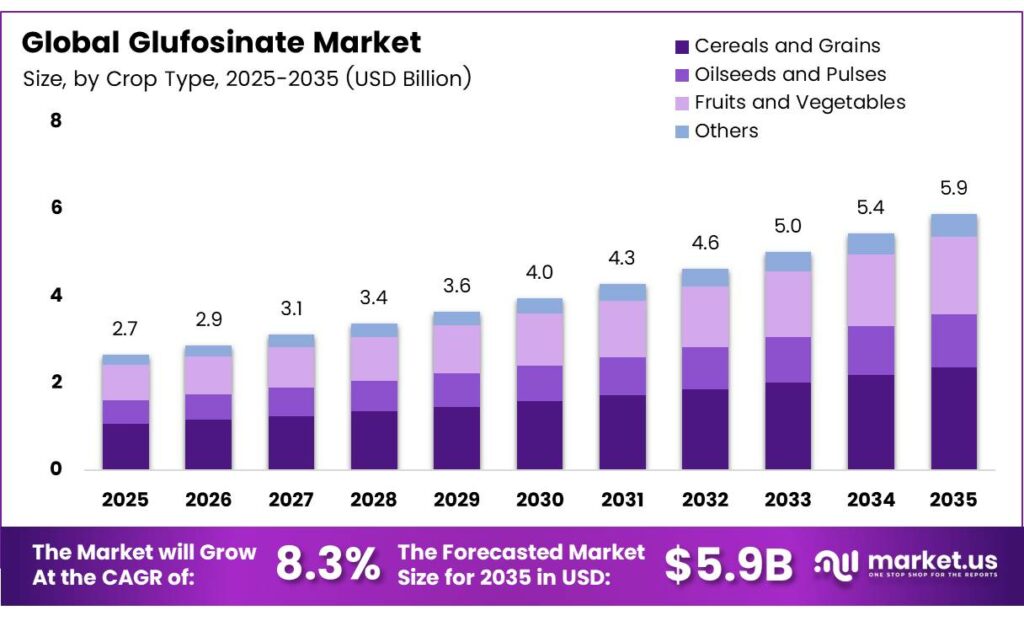

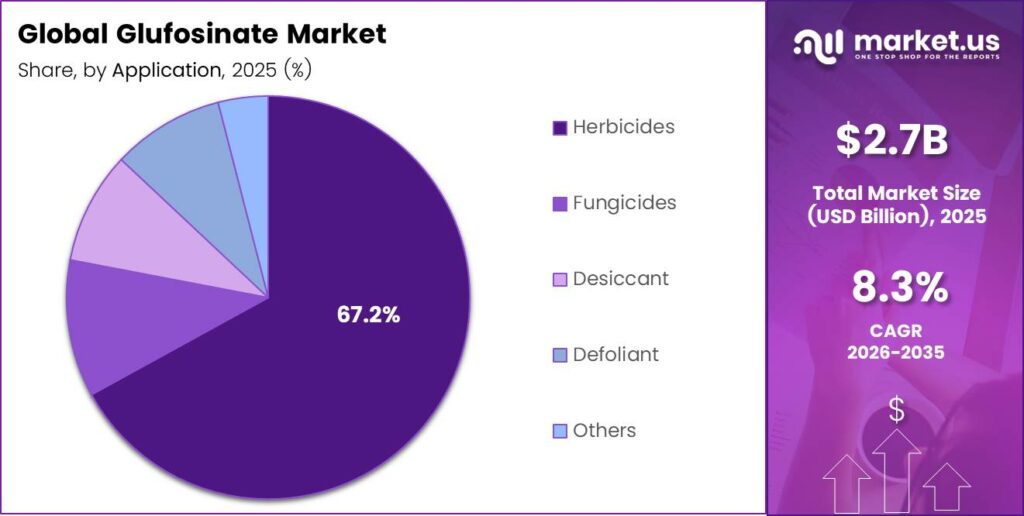

The Global Glufosinate Market size is expected to be worth around USD 5.9 billion by 2035 from USD 2.7 billion in 2025, growing at a CAGR of 8.3% during the forecast period 2026 to 2035.

Glufosinate is a broad-spectrum contact herbicide widely used in modern crop protection programs. Farmers and agribusinesses apply it to control a wide range of weeds in both agricultural and non-agricultural settings. The product works by inhibiting a key enzyme in plant nitrogen metabolism, making it effective across diverse weed species.

The market supports two major chemical forms: glufosinate-ammonium and the newer glufosinate-P isomer. Both forms serve herbicide applications in major row crops, oilseeds, and specialty crops. Moreover, glufosinate finds increasing use as a desiccant and defoliant, expanding its role beyond traditional weed control functions.

- According to USDA NASS, glufosinate-ammonium was applied to 10% of planted soybean acres in Iowa in 2023, at a yearly rate of 0.578 pounds per acre, totaling 394 thousand pounds. This reflects consistent adoption at the field level across major crop systems.

Growth in this market ties directly to the global rise of herbicide-resistant weeds. Farmers across North America, Europe, and the Asia Pacific increasingly turn to glufosinate as a reliable alternative to glyphosate. Consequently, demand for glufosinate-tolerant genetically modified crop varieties continues to accelerate adoption.

- Chinese manufacturers continue to expand production capacity, creating both supply opportunities and pricing pressures globally. Lier Chemical, a major Chinese agrochemical producer, reported revenue of RMB 7,310,881,683 in FY2024, exporting to more than 30 countries, including the United States, Brazil, and India. This scale of activity underlines the global reach and competitive intensity of the glufosinate supply chain.

Government agencies actively shape this market through registration approvals and regulatory reviews. The United States Environmental Protection Agency expanded access by proposing new approvals for next-generation formulations. The agency proposed registering glufosinate-P for 5 crops in May 2024, including corn, soybean, cotton, and canola, noting that glufosinate-P requires approximately half the application rate of standard glufosinate-ammonium.

Key Takeaways

- The Global Glufosinate Market is projected to reach USD 5.9 billion by 2035, up from USD 2.7 billion in 2025, at a CAGR of 8.3% during the forecast period 2026 to 2035.

- Aqueous Suspension holds the dominant share at 31.7%.

- Cereals and Grains lead with a 45.8% market share.

- Herbicides dominate with a 67.2% share of the total market.

- North America leads regional markets with a 36.5% share, valued at USD 0.9 billion.

Formulation Type Analysis

Aqueous Suspension dominates with 31.7% due to its ease of handling, mixing stability, and wide field compatibility.

In 2025, Aqueous Suspension held a dominant market position in the By Formulation Type segment of the Glufosinate Market, with a 31.7% share. This formulation type offers superior droplet coverage and reduced drift, making it the preferred choice among professional applicators and large-scale row crop farmers globally.

Liquid formulations represent a well-established category within the glufosinate portfolio. Formulators favor liquid concentrates for their straightforward dilution and compatibility with standard spraying equipment. Additionally, liquid products appeal to cost-sensitive markets where ease of storage and logistics remain important procurement criteria.

Suspension Concentrate formulations offer a stable alternative where active ingredient loading is high. Manufacturers develop suspension concentrates to improve shelf life and handling safety compared to older emulsifiable concentrates. Consequently, this format is gaining traction in markets with stringent chemical storage regulations.

Soluble (Liquid) Concentrate products dissolve fully in water, offering clean tank mixing with other crop protection inputs. This formulation type suits precision agriculture users who require consistent dosing. Moreover, soluble concentrates are increasingly adopted in integrated pest and weed management programs across developed markets.

Crop Type Analysis

Cereals and Grains dominate with 45.8% due to large cultivated acreage and widespread glufosinate-tolerant variety adoption.

In 2025, Cereals and Grains held a dominant market position in the By Crop Type segment of the Glufosinate Market, with a 45.8% share. The broad acreage under wheat, corn, and rice globally drives substantial herbicide consumption. Furthermore, the expansion of glufosinate-tolerant GM corn varieties continues to reinforce this segment’s leadership.

Oilseeds and Pulses represent the second-largest crop type segment for glufosinate usage. Soybean, canola, and sunflower growers increasingly apply glufosinate as resistance management against glyphosate-tolerant weeds. Therefore, oilseed-producing regions such as North America and South America record strong and growing herbicide uptake within this category.

Fruits and Vegetables growers use glufosinate primarily for pre-plant burndown and inter-row weed control. Specialty crop producers value its fast-acting, contact mode of action that limits weed competition during critical crop establishment windows. Moreover, non-residual properties make it suitable for use near harvest periods in select registrations.

Application Analysis

Herbicides dominate with 67.2% due to glufosinate’s effectiveness against resistant weed biotypes in row crop systems.

In 2025, Herbicides held a dominant market position in the By Application segment of the Glufosinate Market, with a 67.2% share. Glufosinate’s broad-spectrum, post-emergence activity makes it the herbicide of choice in resistance management programs. Farmers applying it in glufosinate-tolerant GM crop systems drive the largest share of global volume.

Fungicides and related protective applications represent a smaller but developing segment for glufosinate derivatives. Research into glufosinate’s secondary plant physiological effects continues to explore potential crop health benefits. However, the fungicide application category remains niche and dependent on further regulatory approvals in key markets.

Glufosinate also serves targeted roles as a Desiccant and Defoliant in crop maturation management. Cotton and oilseed producers use it to accelerate uniform crop drying before harvest. Additionally, emerging Other applications include industrial vegetation control and urban weed management, broadening the commercial scope of this active ingredient.

Key Market Segments

By Formulation Type

- Aqueous Suspension

- Liquid

- Suspension Concentrate

- Soluble (Liquid) Concentrate

- Others

By Crop Type

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Others

By Application

- Herbicides

- Fungicides

- Desiccant

- Defoliant

- Others

Emerging Trends

Glufosinate Gains Ground as the Primary Glyphosate Alternative in Resistance Management Programs

Farmers and agronomists increasingly position glufosinate as the leading replacement for glyphosate in weed resistance programs. Growing resistance to glyphosate across key weed species accelerates this shift. Moreover, agribusinesses design herbicide rotation programs specifically built around glufosinate’s unique glutamine synthase inhibition mechanism.

- Demand for broad-spectrum, post-emergence herbicide activity drives strong growth in glufosinate applications. Agricultural Solutions revenue reached €9,798 million in FY2024, though declining glufosinate-ammonium prices suppressed overall revenue, reflecting high competitive supply. This pricing pressure signals a maturing market where volume growth continues even as unit values compress.

Precision agriculture programs increasingly shape how farmers use glufosinate in field operations. Crop-specific herbicide protocols now integrate targeted application timing with drone and variable-rate spraying technologies. Additionally, pre-plant burndown strategies in major row crop systems drive expanded seasonal use across North America and South America.

Drivers

Herbicide-Resistant Weed Proliferation and GM Crop Expansion Drive Glufosinate Market Growth

Glyphosate-resistant weed species now cover millions of hectares across major agricultural regions globally. Farmers actively seek alternative herbicide modes of action to manage this growing challenge. Consequently, glufosinate herbicides gain strong adoption as farmers rotate away from over-reliant single-mode programs in corn and soybean rotations.

- The expansion of glufosinate-tolerant GM crops directly fuels market volume. Glufosinate-ammonium was applied across 19 program states in 2023 to 6% of planted soybean acres, at a yearly rate of 0.526 pounds per acre, totaling 2,029 thousand pounds. This consistent use pattern confirms that GM crop adoption creates predictable, sustained demand for glufosinate products.

Regulatory exits of competing herbicides like paraquat and dicamba create additional market space for glufosinate. Precision spraying technologies further enhance glufosinate targeting efficiency, reducing input waste. Therefore, agrochemical companies prioritize glufosinate portfolio development to address both the regulatory and resistance management needs of modern row crop farmers.

Restraints

Chinese Oversupply and Tightening European Regulations Create Significant Market Headwinds

Severe price volatility originating from excess production capacity in China continues to suppress the glufosinate market value. Chinese manufacturers aggressively expand output, pushing global prices downward and compressing margins for Western agrochemical companies. This oversupply dynamic directly reduces revenue even when sales volumes remain stable or grow.

- BASF herbicide segment sales totaled €2,965 million in FY2024, a decline of 12.3% from €3,380 million in FY2023, with weaker glufosinate-ammonium pricing cited as a key factor. This sharp revenue decline illustrates how supply-side pressure translates directly into financial underperformance for major global herbicide manufacturers.

European Union regulatory reviews of glufosinate’s toxicological profile create market uncertainty for European applicators and distributors. Tightened approval conditions in the EU and aligned markets restrict product use and reduce the addressable market size. India’s UPL reported a 60% year-over-year drop in Q4 FY2024 Crop Protection revenue, partly driven by elevated channel inventory from prior-year overstock of glufosinate products.

Growth Factors

Nano-Formulation Innovation and Non-Agricultural Applications Accelerate Glufosinate Market Expansion

Agrochemical companies invest actively in nano-formulated glufosinate products designed to deliver effective weed control at lower use rates. These advanced delivery systems improve active ingredient uptake while reducing environmental loading per application. Moreover, lower application rates align with regulatory preferences for reduced chemical inputs in precision agriculture markets.

- India’s growing glufosinate import demand confirms an expanding market opportunity in emerging agricultural regions. Glufosinate imports reached 1,296 metric tons during the period of investigation, up from 590 metric tons in the base year. This more than doubling of import volumes reflects rapid uptake as awareness and distribution infrastructure expand across Indian farming communities.

China’s Xinan invested RMB 2.541 billion in fixed assets in FY2024, including a 3,000-ton-per-year glufosinate technical project, signaling long-term supply expansion aligned with growing global demand. Additionally, stacked-trait seed programs enabling dual-mode herbicide application further increase glufosinate’s role in advanced crop production systems across multiple geographies.

Regional Analysis

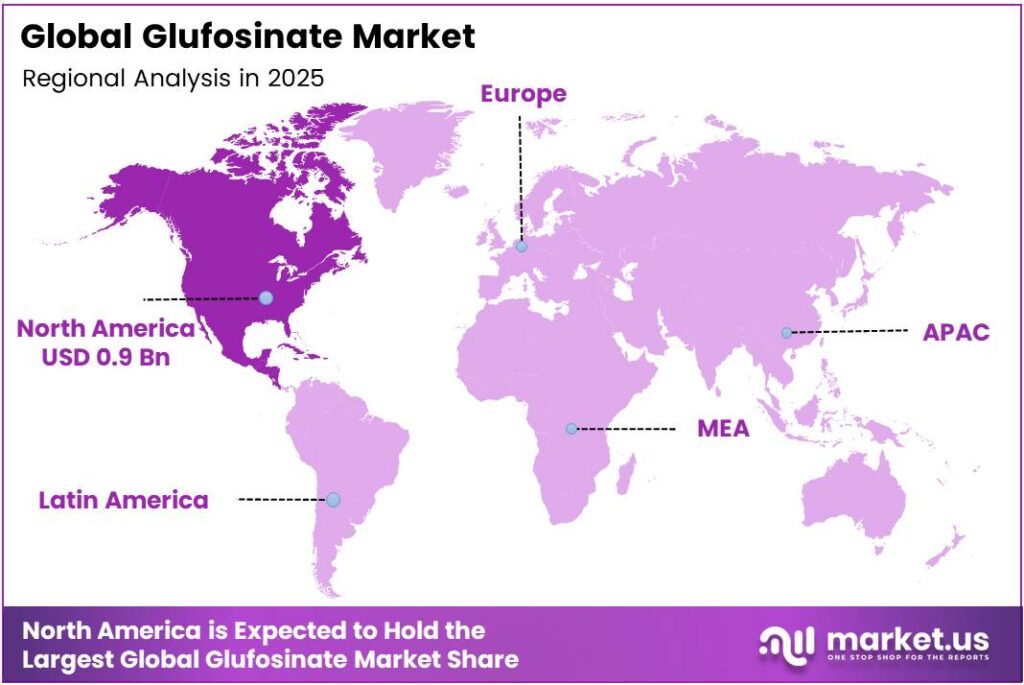

North America Dominates the Glufosinate Market with a Market Share of 36.5%, Valued at USD 0.9 Billion

North America leads global glufosinate consumption with a 36.5% market share, valued at USD 0.9 billion. The United States drives demand through large-scale adoption of glufosinate-tolerant GM corn, soybean, canola, and cotton programs. Furthermore, the EPA’s proposal to register glufosinate-P for five major crops in 2024 signals continued regulatory support for market growth across the region.

Europe maintains a significant glufosinate market presence despite ongoing EU regulatory review processes. Western European farmers apply glufosinate in weed burndown and resistance management programs across cereals, oilseeds, and specialty crops. However, tightened toxicology standards and approval restrictions limit product access compared to North American and Asian markets.

Asia Pacific represents a fast-growing region for glufosinate, driven by rising agricultural productivity demands in China, India, and Southeast Asia. India’s domestic market expanded significantly, supported by growing awareness and field demonstration programs conducted by major distributors. Moreover, China’s large-scale domestic production positions the region as both a major consumer and supplier of glufosinate active ingredient.

Latin America holds strong strategic importance for glufosinate due to the region’s massive soybean, corn, and cotton production base in Brazil and Argentina. Glufosinate-tolerant GM crop varieties drive consistent herbicide demand across major growing states. Additionally, increasing herbicide resistance challenges in Brazilian and Argentine farming systems accelerate the adoption of glufosinate as a rotation partner.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Bayer AG holds a commanding position in the global glufosinate market through its Liberty herbicide brand, which is deeply integrated with LibertyLink GM crop technology. The company markets glufosinate across North America, Europe, and the Asia Pacific, with established registration portfolios covering corn, soybean, canola, and cotton. Bayer’s investment in digital farming and precision application tools further strengthens its glufosinate product positioning among large-scale commercial growers.

Syngenta Crop Protection AG operates within the glufosinate space through its broad crop protection portfolio, targeting resistance management needs globally. The company supports farmer adoption through agronomic advisory services and integrated weed management programs that feature glufosinate as a key rotation partner. Additionally, Syngenta’s global distribution network across more than 100 countries enables consistent product availability in diverse agricultural markets.

UPL LTD has built a strong glufosinate presence in India and export markets through domestic manufacturing, launched, and full commercial rollout. Indian farmers about glufosinate applications. Furthermore, UPL’s global footprint enables cross-regional supply and distribution through its extensive agrochemical trade network.

Nufarm Limited delivers glufosinate products across North America, Europe, and the Asia Pacific through a broad generics and branded agrochemical portfolio. Nufarm’s manufacturing capabilities and regional distribution strength position it as a reliable supplier for glufosinate-based crop protection programs. Reflecting strong export demand from global glufosinate buyers, including major agrochemical companies.

Top Key Players in the Market

- Bayer AG

- Syngenta Crop Protection AG

- UPL LTD

- Nufarm Limited

- BASF SE

- Hebei Veyong Bio-Chemical Co., Ltd

- ZHEJIANG YONGNONG CHEM. IND. CO., LTD

- Clariant AG

Recent Developments

- In 2025, BASF SE registered the U.S. EPA-registered Liberty ULTRA herbicide, the next-generation formulation powered by patented Glu-L Technology (refines the active L-isomer for efficiency) and Liberty Lock formulation. It is approved for post-emergence weed control (broadleaves and grasses) in glufosinate-resistant soybean, cotton, corn, and canola.

- In 2025, Bayer advanced Vyconic soybeans (industry-first trait package tolerant to five herbicides: glyphosate, glufosinate, dicamba, 2,4-D, and mesotrione). This expands options for glufosinate use in weed management (pending certain EPA approvals for in-crop applications). Marketed via DEKALB and other Bayer seed brands.

Report Scope

Report Features Description Market Value (2025) USD 2.7 Billion Forecast Revenue (2035) USD 5.9 Billion CAGR (2026-2035) 8.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Formulation Type (Aqueous Suspension, Liquid, Suspension Concentrate, Soluble (Liquid) Concentrate, Others), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Others), By Application (Herbicides, Fungicides, Desiccant, Defoliant, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Bayer AG, Syngenta Crop Protection AG, UPL LTD, Nufarm Limited, BASF SE, Hebei Veyong Bio-Chemical Co. Ltd, ZHEJIANG YONGNONG CHEM. IND. CO., LTD, Clariant AG Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Bayer AG

- Syngenta Crop Protection AG

- UPL LTD

- Nufarm Limited

- BASF SE

- Hebei Veyong Bio-Chemical Co., Ltd

- ZHEJIANG YONGNONG CHEM. IND. CO., LTD

- Clariant AG

Our Clients

- 180787

- March 2026