Global Ureteral Access Sheath Market By Type (Traditional (Rigid/Conventional) UAS, Flexible/Navigable UAS (FANS), Suction-Active UAS (S-UAS/FV-UAS) and Others) By Clinical Indication (Stone Management and Others (Strictures, Diagnostic Access)), By End Use (Hospitals, Specialty Clinics, Diagnostic Centers, Ambulatory Surgical Centers (ASCs) and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180503

- Number of Pages: 286

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

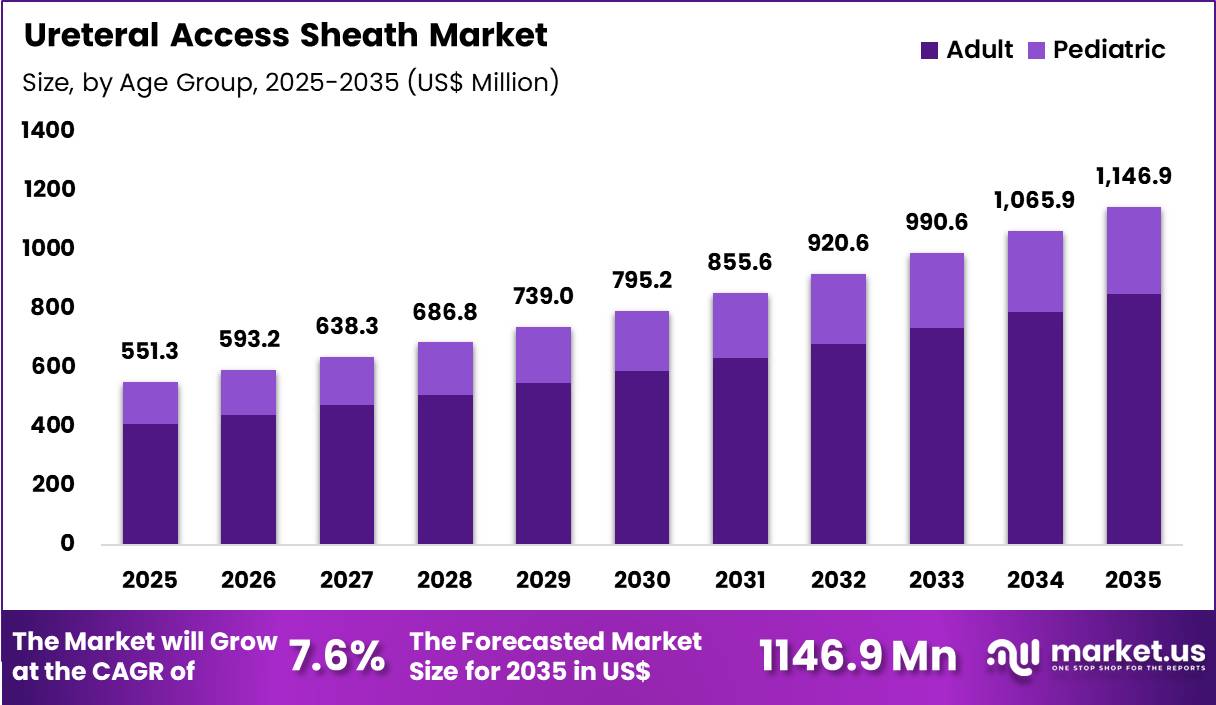

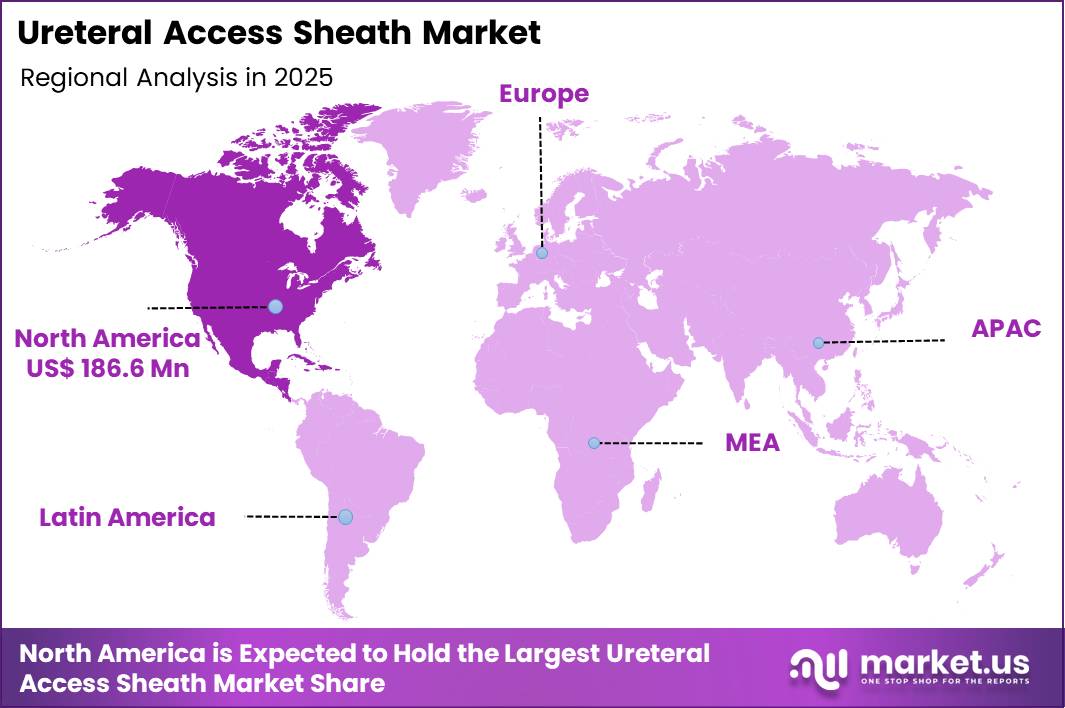

The Global Ureteral Access Sheath Market size is expected to be worth around US$ 1146.9 Million by 2035 from US$ 551.3 Million in 2025, growing at a CAGR of 7.6% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 33.8% share with a revenue of US$ 186.6 Million.

Increasing demand for minimally invasive urological procedures propels the ureteral access sheath market as urologists seek reliable tools that facilitate safe, repeated instrument passage during complex endourologic interventions. These sheaths enable efficient access to the upper urinary tract in percutaneous nephrolithotomy, allowing large-bore instruments to fragment and extract renal calculi while protecting the ureteral wall from trauma.

Surgeons utilize ureteral access sheaths in flexible ureteroscopy for kidney stone removal, providing a stable conduit that reduces ureteral injury risk and improves stone-free rates in cases of multiple or large stones. These devices support diagnostic ureteroscopy by maintaining ureteral patency during biopsy and laser ablation of upper tract tumors, ensuring clear visualization and precise tissue sampling.

In cases of ureteral strictures or obstructions, urologists employ sheaths to deliver balloons or stents, enabling dilation and drainage with minimal manipulation. The sheaths also facilitate retrograde intrarenal surgery for calyceal diverticula, offering a protected pathway for laser lithotripsy and stone evacuation.

Manufacturers pursue opportunities to develop hydrophilic-coated and reinforced sheaths with enhanced kink resistance, expanding applications in challenging anatomies such as tortuous ureters or in patients with prior instrumentation. Developers advance variable-length and adjustable-diameter designs that accommodate diverse stone burdens and procedural needs, improving procedural versatility in both rigid and flexible endourology.

These innovations facilitate integration with digital ureteroscopes and laser systems for real-time navigation and treatment. Opportunities emerge in disposable, single-use sheaths that minimize cross-contamination risks in high-volume stone centers. Companies invest in radiopaque markers and ergonomic handles that enhance precision and reduce operator fatigue.

In January 2026, Boston Scientific signed an agreement to acquire Valencia Technologies Corporation as part of its effort to expand capabilities within the urology treatment space. The transaction supports the company’s strategic focus on minimally invasive technologies used in modern urological interventions.

Recent trends emphasize sheath durability, reduced friction, and procedural efficiency, positioning the market for growth in advanced endourologic care focused on safety and stone clearance outcomes.

Key Takeaways

- In 2025, the market generated a revenue of US$ 551.3 Million, with a CAGR of 7.6%, and is expected to reach US$ 1146.9 Million by the year 2035.

- The type segment is divided into traditional (rigid/conventional) UAS, flexible/navigable UAS (FANS), suction-active UAS (S-UAS/FV-UAS) and others, with traditional taking the lead with a market share of 42.2%.

- Considering size, the market is divided into <10 fr, 10 to 12 fr and more than or equal to 13 – 15 fr. Among these, 10 to 12 fr held a significant share of 61..8%.

- Furthermore, concerning the age group segment, the market is segregated into adult and pediatric. The adult sector stands out as the dominant player, holding the largest revenue share of 74.2% in the market.

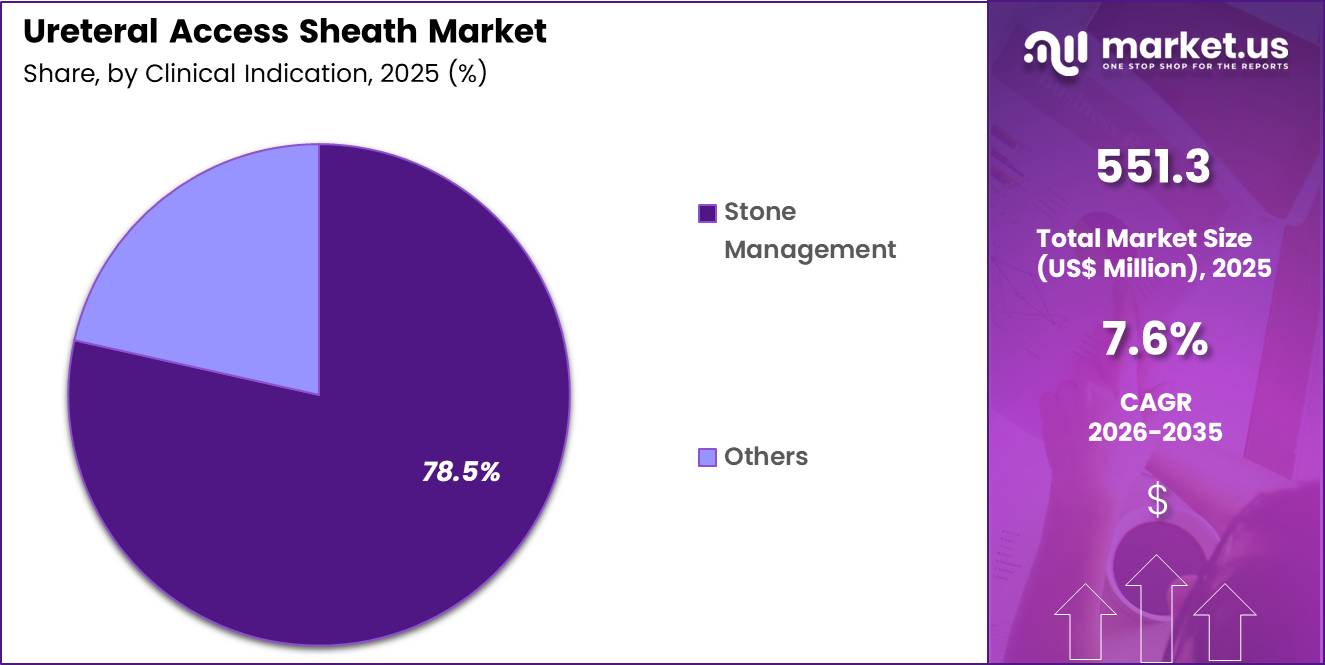

- The clinical indication segment is segregated into stone management and others, with the stone management segment leading the market, holding a revenue share of 78.5%.

- Moreover, concerning the end use segment, the market is segregated into hospitals, specialty clinics, diagnostic centers, ambulatory surgical centers (ASCs) and others. The hospitals sector stands out as the dominant player, holding the largest revenue share of 54.6% in the market.

- North America led the market by securing a market share of 33.8%.

Type Analysis

Traditional rigid or conventional ureteral access sheaths accounted for 42.2% of growth within type and dominate the ureteral access sheath market due to their reliability and long clinical history in ureteroscopy procedures. Urologists widely utilize these devices because they offer stable access to the urinary tract during endoscopic stone removal procedures.

The segment growth is expected to strengthen as minimally invasive urological surgeries continue to expand worldwide. Healthcare providers prefer conventional sheaths due to their predictable performance and compatibility with existing ureteroscopic instruments. Increasing prevalence of kidney stone disease supports higher procedure volumes in hospitals and specialty clinics.

Clinical guidelines from urological associations emphasize ureteroscopy as a primary treatment for certain stone cases, which reinforces demand for traditional access sheaths. Hospitals invest in standardized surgical tools that support efficient endoscopic workflows. The segment is projected to maintain strong adoption as surgeons prioritize procedural safety and device familiarity.

Size Analysis

The 10 to 12 Fr size segment accounted for 61.8% of growth within size and dominate due to its optimal balance between ureteral safety and instrument maneuverability. Urologists frequently select this size because it supports effective irrigation flow and easier stone fragment retrieval during ureteroscopy.

The segment growth is anticipated to expand as stone management procedures continue to rise globally. Medical professionals consider this size appropriate for most adult ureteroscopic interventions because it reduces ureteral trauma while maintaining operational efficiency.

Increasing clinical preference for flexible ureteroscopy strengthens the demand for 10 to 12 Fr sheaths. Hospitals standardize this size within procedural kits for routine stone surgeries. The segment is likely to maintain leadership as surgeons prioritize device dimensions that enhance procedural precision and safety.

Age Group Analysis

Adult patients accounted for 74.2% of growth within age group and dominate the ureteral access sheath market due to the higher prevalence of kidney stones among the adult population. Epidemiological studies in the United States and Europe indicate that kidney stone disease affects a significant share of adults during their lifetime.

The segment growth is projected to strengthen as lifestyle factors such as obesity, dehydration, and dietary habits increase stone formation risk. Urologists frequently perform ureteroscopy procedures in adults to remove stones and manage urinary tract obstructions.

Hospitals record high volumes of adult urological procedures, which drives consistent demand for ureteral access devices. Increasing diagnostic imaging usage also contributes to earlier detection of kidney stones in adults. The adult segment is anticipated to maintain strong growth as aging populations experience higher incidence of urological disorders.

Clinical Indication Analysis

Stone management accounted for 78.5% of growth within clinical indications and dominate the ureteral access sheath market because ureteroscopy remains a primary procedure for kidney and ureteral stone treatment. Healthcare data show that kidney stone prevalence continues to rise in many countries due to dietary and metabolic factors.

Ureteral access sheaths support efficient stone removal by facilitating repeated instrument entry and improved irrigation during lithotripsy procedures. The segment growth is expected to accelerate as minimally invasive endourological techniques replace traditional open surgeries.

Physicians prefer ureteroscopy due to shorter recovery times and reduced complication rates. Hospitals continue to expand endourology units that specialize in stone disease treatment. The segment is projected to remain dominant as technological advances in laser lithotripsy increase procedural success rates.

End-Use Analysis

Hospitals accounted for 54.6% of growth within end use and dominate the ureteral access sheath market due to their capacity to perform complex urological surgeries and provide comprehensive patient care. Hospitals house specialized operating rooms, imaging systems, and trained urology teams that support advanced endoscopic procedures.

The segment growth is expected to strengthen as surgical volumes increase for kidney stone treatment. Hospitals perform a large share of ureteroscopy procedures because they manage emergency cases and complicated stone conditions.

Healthcare infrastructure investments also expand surgical capabilities in many regions. The segment is anticipated to grow further as hospitals adopt advanced urological equipment and minimally invasive surgical technologies. Continuous improvements in endourology practices reinforce the central role of hospitals in this market.

Key Market Segments

By Type

- Traditional (Rigid/Conventional) UAS

- Flexible/Navigable UAS (FANS)

- Suction-Active UAS (S-UAS/FV-UAS)

- Others

By Size

- <10 Fr

- 10 to 12 Fr

- More than or equal to 13 – 15 Fr

By Age Group

- Adult

- Pediatric

By Clinical Indication

- Stone Management

- Others (Strictures, Diagnostic Access)

By End Use

- Hospitals

- Specialty Clinics

- Diagnostic Centers

- Ambulatory Surgical Centers (ASCs)

- Others

Drivers

Increasing net sales of urology products is driving the market.

Boston Scientific, a key player, reported net sales in its Urology segment of $1.773 billion for the full year 2022. This figure rose to $1.964 billion in 2023. The segment achieved $2.200 billion in net sales during 2024. Full-year 2025 net sales reached $2.709 billion. The consistent year-over-year increases demonstrate robust demand for devices supporting ureteroscopic interventions.

Ureteral access sheaths form an integral component of the stone management portfolio within this segment. The growth trajectory aligns with expanded utilization in minimally invasive kidney stone procedures.

Clinicians increasingly rely on these sheaths for safe ureteral dilation and repeated instrument passage. Such performance underscores the clinical value of reliable access solutions in urological practice. This driver sustains investment in next-generation sheath technologies across the sector.

Restraints

Procedural complexities associated with ureteral anatomy are restraining the market.

Ureteral access sheaths require precise navigation through variable ureteral tortuosity and narrow segments. Anatomical differences among patients can complicate initial placement and increase risks of mucosal injury. Practitioners must possess advanced endoscopic skills to mitigate potential complications during sheath deployment.

Training requirements limit immediate adoption in smaller or less specialized facilities. The need for fluoroscopic guidance adds procedural time and resource demands. Patient-specific factors such as prior surgeries or strictures further hinder consistent success rates. These challenges reduce confidence among less experienced urologists in routine sheath utilization.

Supply chain participants encounter moderated demand from facilities still building expertise. The restraint affects overall penetration despite technological improvements. This factor continues to moderate the pace of broader market expansion in diverse clinical settings.

Opportunities

Advancements in flexible and navigable suction ureteral access sheaths are creating growth opportunities.

Innovative designs incorporating suction capabilities enable simultaneous irrigation and stone fragment evacuation. These systems maintain lower intrarenal pressure during lithotripsy procedures. Opportunities arise for improved stone-free rates through enhanced visibility and debris clearance. Manufacturers can differentiate offerings by integrating navigable distal tips for challenging calyceal access.

The technology supports reduced operative times and fewer auxiliary procedures. Providers gain options for complex cases previously limited by conventional rigid sheaths. Opportunities extend to training programs that highlight efficiency gains in retrograde intrarenal surgery.

Integration with existing ureteroscopes creates comprehensive single-use platforms. The development fosters partnerships between device companies and urology departments. Such frameworks promote scalable adoption and long-term sector profitability.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the ureteral access sheath market through hospital procurement budgets, surgical procedure volumes, and capital allocation for urology departments. Inflation increases costs for medical grade polymers, coatings, and sterilization processes, which raises production expenses for device manufacturers.

Higher interest rates reduce flexibility in hospital purchasing plans and slow bulk ordering of disposable surgical tools. Geopolitical tensions affect global sourcing of specialty plastics, catheter components, and packaging materials, which introduces supply chain uncertainty.

Current US tariffs on imported medical materials and device components increase manufacturing and distribution costs for suppliers serving the US market. These pressures can tighten margins and delay purchasing decisions in cost-sensitive healthcare facilities.

At the same time, manufacturers invest in regional production and strengthen supplier diversification to maintain stable supply. Rising incidence of kidney stones and growing adoption of minimally invasive urological procedures continue to support steady and confident market expansion.

Latest Trends

Full U.S. commercial launch of advanced suction-enabled ureteral access sheaths is driving the market.

Dornier MedTech America completed the full commercial rollout of the Dornier Hoover Flexible & Navigable Suction Ureteral Access Sheath in September 2025. The device features continuous suction alongside irrigation and instrument exchange functionality. This launch builds upon prior FDA clearance and limited market release phases.

The sheath complements the Dornier Axis II Slim ureteroscope for integrated stone management. Urologists benefit from best-in-class deflection and suction performance in flexible ureteroscopy. The 2025 introduction aligns with evolving preferences for single-use technologies in high-volume centers.

Practices achieve streamlined workflows through reduced intrarenal pressure and improved fragment retrieval. The trend reflects broader innovation in suction-assisted endoscopic tools. Stakeholders observe accelerated interest in these systems for complex renal stone cases. Overall, the development positions advanced sheath designs as a central element of contemporary urological practice.

Regional Analysis

North America is leading the Ureteral Access Sheath Market

North America accounted for 33.8% of the ureteral access sheath market in 2025, supported by rising urological procedure volumes and continuous adoption of minimally invasive stone management techniques across major healthcare systems. Kidney stone prevalence remains a key clinical driver, with the US National Institute of Diabetes and Digestive and Kidney Diseases reporting that about 1 in 11 people in the United States experience kidney stones.

Growing incidence of metabolic disorders, obesity, and dehydration-related conditions has increased the number of ureteroscopic procedures performed in hospitals and ambulatory surgical centers. Surgeons increasingly rely on access sheaths to improve visualization, reduce intrarenal pressure, and enable efficient instrument exchange during endourological interventions.

Technological improvements in flexible ureteroscopy and laser lithotripsy have also expanded the role of supportive devices that enhance procedural safety and efficiency. Hospital systems across the US and Canada have continued investing in advanced urology suites and outpatient surgical infrastructure.

Clinical training programs for endourology have further promoted standardized use of specialized access tools during stone removal procedures. Collaboration between device manufacturers and academic medical centers has accelerated product refinement and clinical familiarity. These factors collectively supported sustained regional growth in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience strong expansion during the forecast period as urological care capacity increases and awareness of kidney stone disease rises across emerging healthcare systems. China and India alone report large patient pools affected by urinary stone disease, and regional health authorities estimate that urolithiasis prevalence ranges between 5% and 19% in many Asian populations.

Rapid urbanization, dietary changes, and warmer climates contribute to higher stone formation risk, encouraging healthcare providers to expand minimally invasive treatment programs. Governments and private healthcare groups are investing in specialized urology centers and advanced surgical equipment to address rising procedural demand.

Medical training institutions across the region are strengthening expertise in endourology and flexible ureteroscopy, enabling wider clinical use of supportive surgical tools. Expanding health insurance coverage and improving access to tertiary hospitals are encouraging more patients to seek early intervention rather than delaying treatment.

Regional device manufacturers are introducing cost-effective surgical accessories that align with hospital procurement budgets. Increasing collaboration between Asian hospitals and global medical technology firms is also accelerating technology transfer and clinical adoption. Together, these developments are expected to drive steady growth in urological procedure support devices throughout Asia Pacific.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key participants in the Ureteral Access Sheath market expand their presence through continuous product innovation, clinical collaborations with urology centers, and wider distribution partnerships with hospitals and ambulatory surgery facilities. Companies invest in improved materials, hydrophilic coatings, and advanced sheath designs that support smoother instrument passage and safer ureteroscopic procedures.

Boston Scientific stands among the major manufacturers in this segment and develops urology technologies used in minimally invasive stone management procedures. The firm operates from Marlborough, Massachusetts and provides a broad portfolio of interventional medical devices across specialties such as urology, endoscopy, and cardiology.

Industry competitors also strengthen growth through regulatory approvals, strategic alliances, and product launches designed for better surgical efficiency and patient safety. Several global suppliers including Cook Medical, Olympus, and Coloplast compete by expanding minimally invasive treatment solutions and strengthening surgeon training initiatives.

Top Key Players

- Boston Scientific Corporation

- BD (Becton, Dickinson and Company)

- Olympus

- Coloplast

- Cook Medical

- Advin Health Care

- ACE Medical Devices

- Blue Neem Medical Devices Private Limited

- AMECATH

- Creo Medical

- Volkmann Medizintechnik GmbH

- Urovision-Urotech

Recent Developments

- In September 2025, Olympus Corporation formed an exclusive worldwide distribution alliance with MacroLux Medical Technology to broaden its disposable urology device offerings. The partnership includes single-use cystoscopes, ureteroscopes, and suction-enabled access sheaths designed for the diagnosis and management of urinary tract conditions, particularly kidney stone procedures.

- In September 2025, Dornier MedTech initiated the full US market release of two disposable urology instruments, the Hoover flexible suction ureteral access sheath and the Axis II Slim ureteroscope. The suction-enabled sheath supports fluid control and instrument exchange during endourological stone procedures, helping physicians maintain clearer visualization and smoother procedural workflow.

- During 2025, Flexible and Navigable Suction ureteral access sheaths began gaining wider clinical use in kidney stone treatment. These systems help maintain controlled pressure inside the kidney while improving fragment evacuation, which may contribute to higher stone clearance rates and lower risk of ureteral complications during complex intrarenal procedures.

Report Scope

Report Features Description Market Value (2025) US$ 551.3 Million Forecast Revenue (2035) US$ 1146.9 Million CAGR (2026-2035) 7.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (Traditional (Rigid/Conventional) UAS, Flexible/Navigable UAS (FANS), Suction-Active UAS (S-UAS/FV-UAS) and Others), By Size (<10 Fr, 10 to 12 Fr and More than or equal to 13 – 15 Fr), By Age Group (Adult and Pediatric), By Clinical Indication (Stone Management and Others (Strictures, Diagnostic Access)), By End Use (Hospitals, Specialty Clinics, Diagnostic Centers, Ambulatory Surgical Centers (ASCs) and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Boston Scientific, BD, Olympus, Coloplast, Cook Medical, Advin Health Care, ACE Medical Devices, Blue Neem Medical Devices, AMECATH, Creo Medical, Volkmann Medizintechnik, Urovision-Urotech. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Ureteral Access Sheath MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Ureteral Access Sheath MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Boston Scientific Corporation

- BD (Becton, Dickinson and Company)

- Olympus

- Coloplast

- Cook Medical

- Advin Health Care

- ACE Medical Devices

- Blue Neem Medical Devices Private Limited

- AMECATH

- Creo Medical

- Volkmann Medizintechnik GmbH

- Urovision-Urotech

Our Clients

- 180503

- March 2026