Quick Navigation

Report Overview

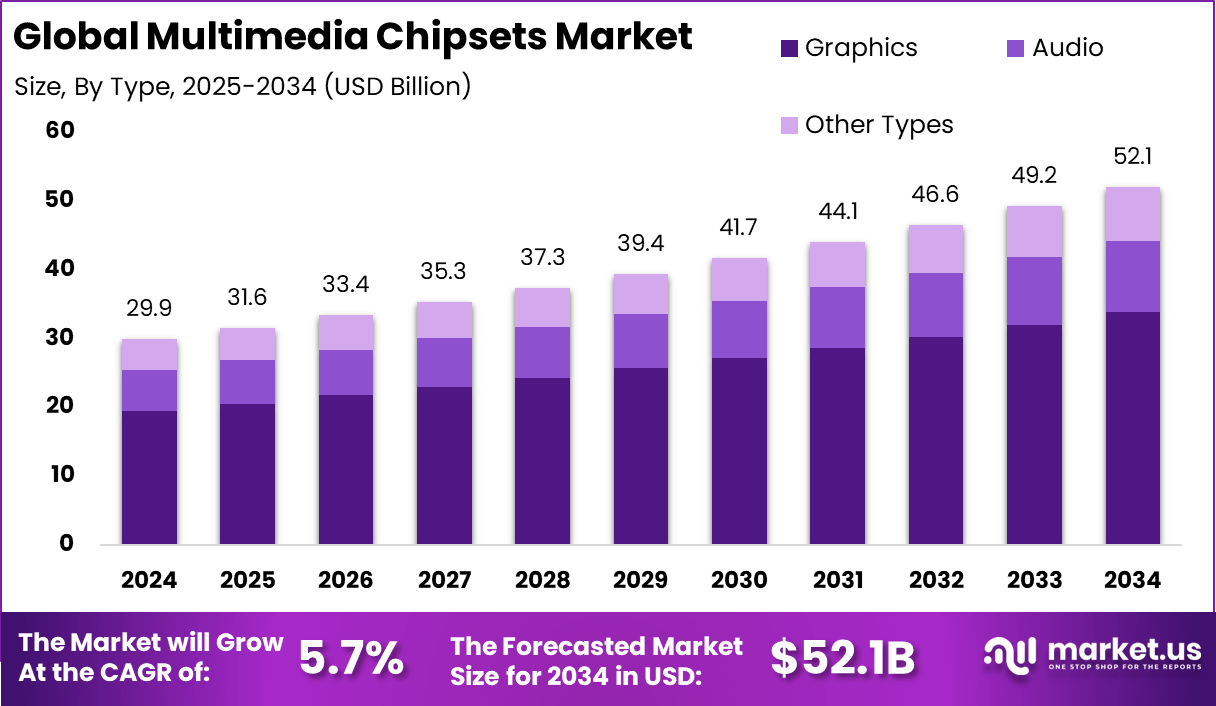

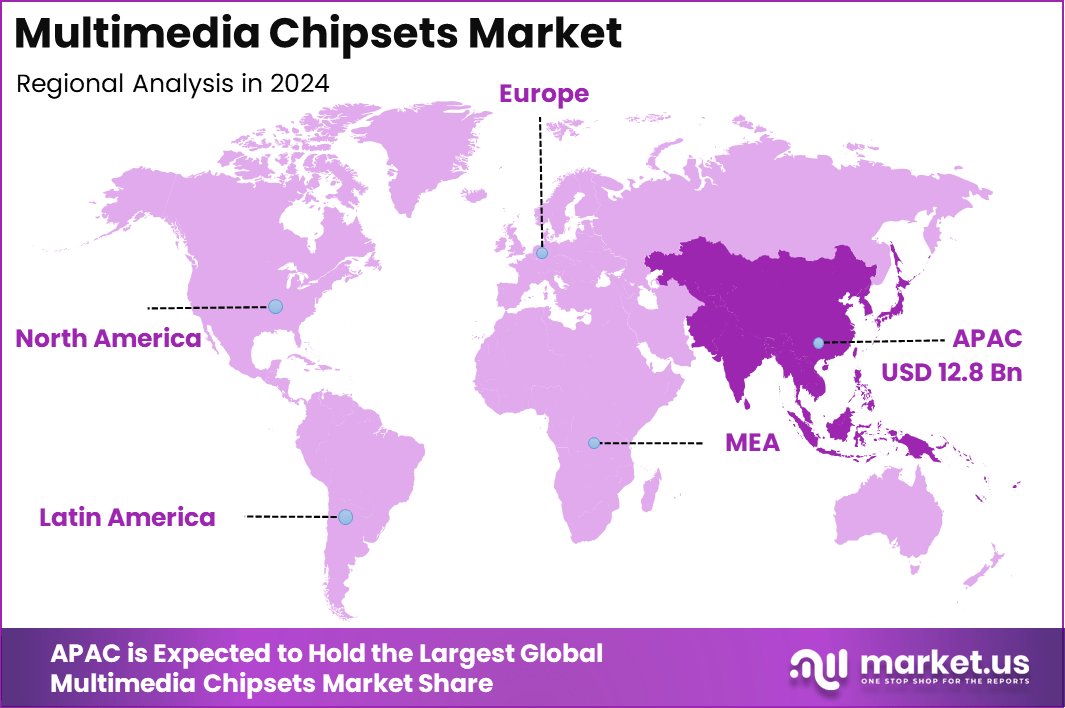

The Global Multimedia Chipsets Market size is expected to be worth around USD 52.1 Billion By 2034, from USD 29.9 billion in 2024, growing at a CAGR of 5.7% during the forecast period from 2025 to 2034. In 2024, APAC held a dominant market position, capturing more than a 43% share, holding USD 12.8 Billion revenue.

Multimedia chipsets are specialized integrated circuits designed to handle audio, video, and other multimedia processing in various devices. These chipsets are crucial for enabling features such as high-definition video playback, audio processing, and enhanced graphics in consumer electronics like smartphones, tablets, televisions, and gaming consoles.

The versatility of multimedia chipsets extends to applications in IT and telecommunications equipment, as well as in media and entertainment devices, where they manage and optimize the performance and quality of multimedia content. The multimedia chipsets market is projected to experience substantial growth, driven by increasing consumer demand for feature-rich multimedia devices and advancements in technology.

The market’s expansion is bolstered by the widespread adoption of high-speed internet and a surge in the use of connected devices, including mobile gaming and smart TVs. In particular, the integration of 5G technology and AI-enhanced processing is pushing the demand for sophisticated multimedia chipsets capable of supporting these advanced capabilities.

One of the primary growth drivers for the multimedia chipsets market is the significant shift towards streaming services and on-demand content, which requires high-performance processing capabilities to deliver smooth, high-quality video and audio experiences.

Additionally, the advent of technologies such as 4K and 8K resolutions and the proliferation of AI and machine learning in device functionalities are catalyzing the market growth. The gaming sector, in particular, is witnessing a robust increase in the need for advanced graphics processing units (GPUs) to support intensive video game graphics and virtual reality applications.

The demand for multimedia chipsets is also influenced by the increasing trend of smart homes and the IoT, where devices are interconnected and require seamless multimedia processing. The market is seeing a shift towards System-on-Chip (SoC) designs, which integrate all necessary electronic circuits and components onto a single chip, improving performance while reducing power consumption and cost.

Technological advancements are continuously being made in the materials and designs of chipsets, with developments in silicon, gallium arsenide, and silicon germanium enhancing the functionality and efficiency of multimedia chipsets. These materials are chosen based on their ability to handle different frequencies and performance demands, particularly in high-frequency and high-performance environments.

Key Takeaways

- The Global Multimedia Chipsets Market is anticipated to grow from USD 29.9 billion in 2024 to USD 52.1 billion by 2034, at a compound annual growth rate (CAGR) of 5.7%.

- In 2024, the Asia-Pacific region secured a leading position in the market, with a significant 43% share, translating to USD 12.8 billion in revenue.

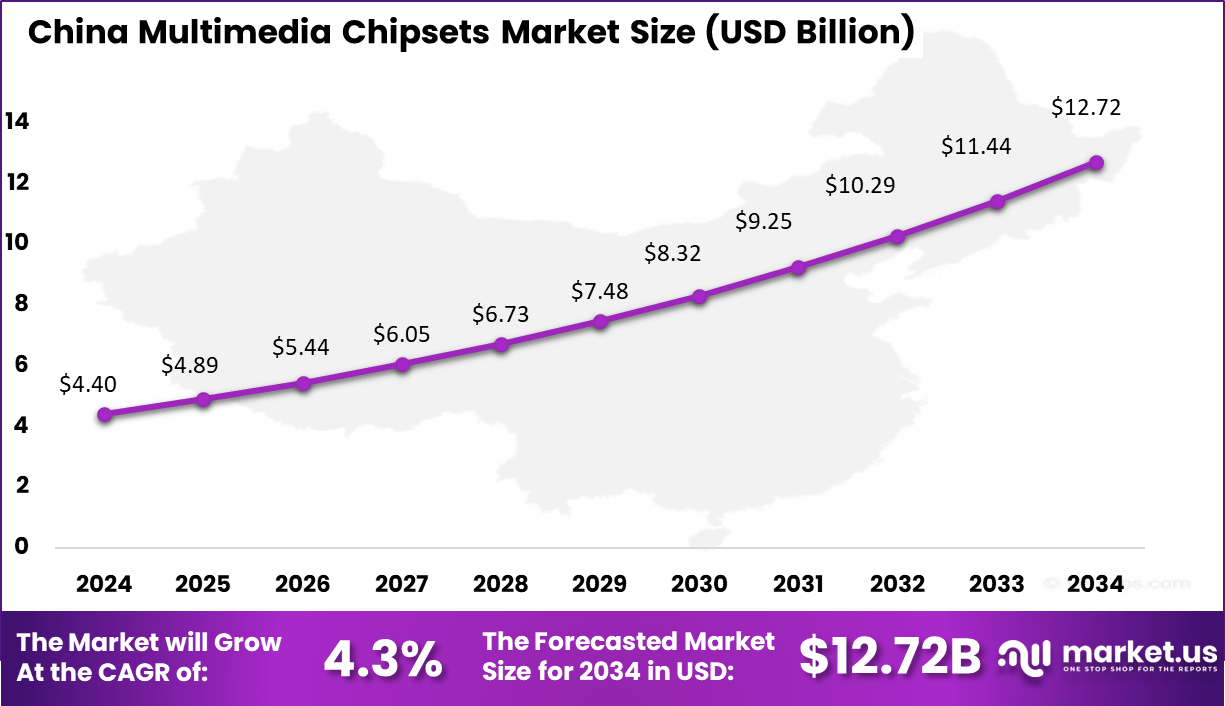

- The multimedia chipsets market in China is expected to expand from USD 4.40 billion in 2024 to USD 12.72 billion by 2034, achieving a CAGR of 4.3%.

- Within the industry, the graphics segment emerged as the predominant force, holding over 56% of the market share in 2024.

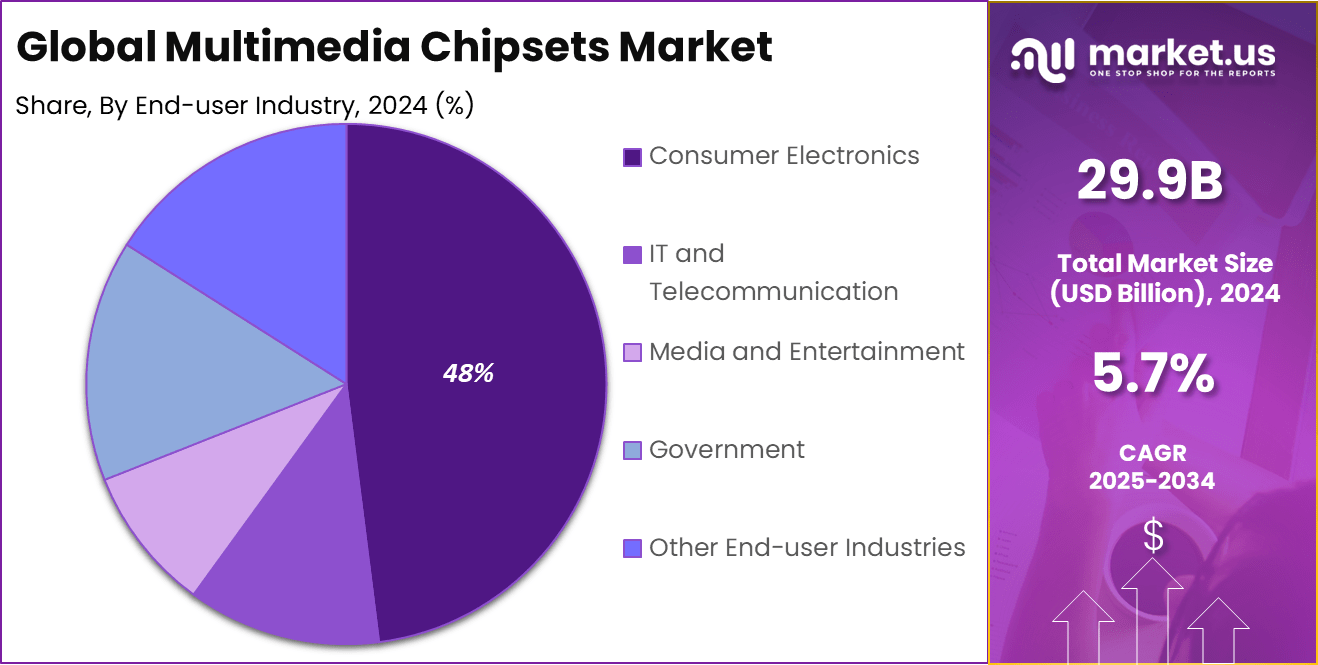

- The consumer electronics segment prominently led the multimedia chipsets market, with more than 48% market share in 2024.

US Tariff Impact Analysis

The recent imposition of tariffs by the U.S. government has significantly impacted the multimedia chipset market. Notably, the Trump administration’s decision to increase tariffs on Chinese semiconductors by 100% is a protective measure to bolster the domestic semiconductor industry following the substantial $53 billion investment under the CHIPS Act.

This increase in tariffs affects a broad range of semiconductor components, which are essential in the manufacturing of multimedia chipsets. These tariffs have compelled companies to adapt in several ways. For instance, some companies are shifting their production facilities to the U.S. to avoid the hefty tariffs on imported Chinese semiconductors.

This strategic move is part of a broader trend of re-shoring manufacturing operations to mitigate tariff impacts and ensure a more stable supply chain. However, the tariffs have also led to price increases in the multimedia chipset market.

The cost of components that are critical for manufacturing multimedia chipsets, such as GPUs and accelerators, has risen, as these components are directly affected by the tariffs. Specifically, products like consumer-class video cards, which include popular models from NVIDIA and AMD, have been exempt from these tariffs, thereby slightly cushioning the blow for certain segments of the market.

Regional Insights

China Market Growth

The China Multimedia Chipsets Market is valued at approximately USD 4.40 Billion in 2024 and is predicted to increase from USD 4.89 Billion in 2025 to approximately USD 12.72 Billion by 2034, projected at a CAGR of 4.3% from 2025 to 2034.

APAC Market Growth

In 2024, APAC held a dominant market position in the multimedia chipsets market, capturing more than a 43% share and generating revenue of USD 12.8 Billion. This leadership can be primarily attributed to the robust manufacturing capabilities and extensive industrial base in countries like China, South Korea, and Taiwan, which are key players in the semiconductor and electronics industries.

These nations have invested heavily in technological advancements and infrastructure development, supporting high-volume production of multimedia chipsets at competitive costs. Additionally, the region benefits from a strong ecosystem of suppliers and manufacturers, coupled with government policies that favor tech industry growth, such as subsidies and tax incentives.

The presence of major global electronics brands in APAC, which integrate these chipsets into various consumer electronics, further drives demand within the region. Furthermore, APAC’s strategic focus on research and development has facilitated innovations in chipset technology, enhancing their performance and application across multiple device platforms, thereby sustaining the region’s leading position in the global market.

Type Analysis

In 2024, the Graphics segment held a dominant market position within the multimedia chipsets industry, capturing more than a 56% share. This leading role can be attributed to several key factors. Primarily, the ever-increasing demand for high-resolution gaming, streaming, and augmented and virtual reality (AR/VR) applications has significantly driven the growth of this segment.

As multimedia content becomes more sophisticated and consumer expectations for visual quality heighten, graphics chipsets, which are essential for rendering detailed and immersive graphics, have seen heightened demand. Moreover, the proliferation of advanced gaming consoles and high-performance PCs, which rely heavily on powerful GPUs, continues to bolster this market segment.

Approximately 90% of gaming consoles and high-end PCs utilize advanced GPUs, highlighting the critical role graphics chipsets play in the consumer electronics space. The demand is further amplified by the widespread consumption of video content in high definition (HD) or ultra-high definition (UHD), with 80% of video content now being consumed in these formats.

Additionally, the technological advancements in graphics chipsets, coupled with their integration into a broader array of devices, including mobile devices and smart TVs, support their dominant status in the market. This segment’s growth is fueled not only by consumer electronics but also by professional and enterprise-level applications where high-quality visual output is crucial.

End-user Industry Analysis

In 2024, the Consumer Electronics segment held a dominant market position within the multimedia chipsets market, capturing more than a 48% share. This predominance is largely driven by the continuous growth in the demand for multimedia-rich devices such as smartphones, tablets, smart TVs, and gaming consoles.

These devices, integral to daily entertainment and communication, require advanced chipsets that support high-resolution displays and interactive functionalities, thereby heavily relying on the innovations within the multimedia chipset sector. Furthermore, the surge in adoption of smart home devices and the expansion of IoT (Internet of Things) applications contribute to the expansion of this segment.

Multimedia chipsets are critical in enhancing the user experience through superior audio and visual capabilities, which are key selling points for consumer electronics. The increasing consumer demand for more immersive and high-quality multimedia experiences encourages manufacturers to continually innovate and improve chipset capabilities.

The strategic focus on integrating advanced technologies such as artificial intelligence (AI) and machine learning for better media processing also plays a crucial role in this sector’s growth. These technologies enable smarter, context-aware electronic devices that enhance user interactions and functionalities, further solidifying the Consumer Electronics segment’s leadership in the multimedia chipset market.

Key Market Segments

By Type

- Graphics

- Audio

- Other Types

By End-user Industry

- Consumer Electronics

- IT and Telecommunication

- Media and Entertainment

- Government

- Other End-user Industries

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Surge in High-Resolution Multimedia Content

One of the primary drivers of the multimedia chipsets market is the escalating demand for high-resolution multimedia content across various platforms. This trend is predominantly fueled by the widespread adoption of digital entertainment and media consumption, particularly in streaming services, gaming, and augmented reality (AR) and virtual reality (VR) applications.

As consumers increasingly prefer content in high-definition (HD), ultra-high definition (UHD), and 4K resolutions, the need for robust graphics and audio chipsets that can process and render this content efficiently has intensified. This surge in demand is further supported by technological advancements in display and audio technologies, making sophisticated multimedia experiences more accessible to a broader audience.

For instance, the proliferation of smart TVs and advanced gaming consoles that support 4K and HDR content requires powerful graphics chipsets to deliver optimal performance. Additionally, as AR and VR technologies become more mainstream in educational, professional, and recreational sectors, the need for high-performance multimedia chipsets that can handle complex visual and auditory data in real time continues to grow, thereby driving market expansion.

Restraint

High Costs and Rapid Technological Obsolescence

A significant restraint in the multimedia chipsets market is the high cost associated with advanced chipset production, coupled with the rapid pace of technological obsolescence. Developing cutting-edge chipsets involves substantial investment in research and development (R&D), as well as state-of-the-art manufacturing processes, which can inflate production costs.

These high costs are often passed on to consumers, potentially limiting market growth in price-sensitive regions. Moreover, the fast-evolving nature of technology means that new chipset models can quickly become outdated as newer, more advanced versions are developed.

This rapid obsolescence can deter investment in high-end chipsets, as consumers and businesses may hesitate to invest in technology that could soon be eclipsed by newer models. Additionally, the intense competition among chipset manufacturers to offer the most advanced products can lead to a continuous cycle of development, which, while driving innovation, also contributes to the challenge of sustaining long-term product viability.

Opportunity

Integration of AI and Machine Learning

The integration of artificial intelligence (AI) and machine learning (ML) into multimedia chipsets presents a substantial opportunity for market growth. AI and ML technologies can significantly enhance the capabilities of multimedia chipsets, enabling more efficient processing, improved power management, and enhanced user experiences.

For example, AI-enhanced chipsets can optimize power consumption for devices, extend battery life, and improve processing speeds without sacrificing quality. Furthermore, as smart devices become increasingly ubiquitous, the demand for chipsets that can provide intelligent functionalities, such as voice and facial recognition, real-time language translation, and personalized content delivery, is rising.

The ability of multimedia chipsets to support these advanced features can open up new markets and applications, particularly in smart home devices, wearable technology, and smart vehicles, offering lucrative opportunities for chipset manufacturers.

Challenge

Supply Chain Disruptions

The multimedia chipset industry faces significant challenges due to supply chain disruptions, which have been exacerbated by global events such as the COVID-19 pandemic and geopolitical tensions. Supply chain issues can lead to shortages of critical raw materials and components, delaying production schedules and leading to increased costs. These disruptions can severely impact manufacturers’ ability to meet demand, especially during periods of high market growth.

Moreover, the dependency on specific regions, such as Asia-Pacific, for the bulk of semiconductor manufacturing, poses a risk of concentration, where any regional instability or logistical challenges can have a global impact on chipset availability. To mitigate these risks, companies are increasingly looking towards supply chain diversification and enhancing their inventory management strategies to better manage future disruptions and maintain steady supply lines.

Growth Factors

The multimedia chipsets market is experiencing robust growth driven by several key factors. The increasing demand for rich multimedia experiences across various devices, including smartphones, tablets, and gaming consoles, significantly propels this market.

Consumers’ growing appetite for high-definition and ultra-high-definition video content has necessitated the development of advanced graphics and audio chipsets, capable of supporting intensive media processing tasks. Moreover, the expansion of the Internet of Things (IoT) and smart home technologies further accelerates the growth of this market.

As more devices become interconnected, the requirement for sophisticated multimedia chipsets that can handle complex tasks and provide seamless user experiences is increasing. This trend is particularly evident with the advent of smart TVs and other connected home devices that rely on high-performance chipsets to deliver immersive audiovisual experiences.

Emerging Trends

Emerging trends in the multimedia chipsets industry highlight the rapid integration of cutting-edge technologies. Key among these trends is the incorporation of artificial intelligence (AI) and machine learning (ML) in multimedia processing, which enhances the capabilities of chipsets, making them more efficient and capable of handling sophisticated tasks such as real-time video processing and advanced gaming functionalities.

The rise of virtual and augmented reality technologies also marks a significant trend, creating new opportunities for the chipset market. These technologies require highly capable multimedia chipsets to render immersive environments, which is pushing manufacturers to innovate continuously.

Additionally, the adoption of 5G technology is set to revolutionize this market by enabling faster data transmission speeds and improved connectivity, thereby enhancing the overall performance of multimedia-driven applications.

Business Benefits

The integration of advanced multimedia chipsets into consumer electronics and other industries offers substantial business benefits. For manufacturers, these chipsets provide a competitive edge by enabling the production of devices that meet the high expectations of modern consumers for multimedia performance. This includes improved graphics for gamers, enhanced audio quality for music and video streaming, and superior processing power for complex applications.

Furthermore, multimedia chipsets are crucial in driving innovation in sectors such as automotive, where they support advanced driver-assistance systems (ADAS) and infotainment technologies. In the telecommunications sector, they play a pivotal role by supporting high-speed data transmission and high-quality video conferencing, essential for today’s digital communication needs.

Key Player Analysis

Top 3 Company Analysis

The multimedia chipset market is witnessing significant transformations, driven by strategic initiatives from leading companies. NVIDIA Corporation, Intel Corporation, and Qualcomm Inc. have each undertaken notable acquisitions, product launches, and mergers, shaping the industry’s future.

NVIDIA has solidified its position at the forefront of AI and multimedia processing. In 2024, the company completed the acquisition of Run:ai, an Israeli AI infrastructure platform, for $700 million, enhancing its capabilities in AI workload optimization. Additionally, NVIDIA is reportedly in advanced discussions to acquire Lepton AI, a startup specializing in AI server rentals, indicating a strategic move to bolster its AI infrastructure offerings.

Intel is undergoing a strategic transformation to strengthen its position in the semiconductor industry. In April 2025, the company agreed to sell a 51% stake in its Altera semiconductor business to Silver Lake, a private equity firm, aiming to streamline operations and focus on core competencies. Furthermore, Intel entered into a joint venture with Apollo Global Management related to its Fab 34 facility in Ireland.

Qualcomm has been actively expanding its AI and IoT capabilities through strategic acquisitions. In April 2025, the company acquired MovianAI, a firm specializing in generative AI applications, to enhance its AI portfolio across PCs and smartphones. Additionally, Qualcomm acquired Edge Impulse, an AI-powered IoT platform, aiming to strengthen its position in the industrial IoT sector.

List of Key Players

- NVIDIA Corporation

- Intel Corporation

- Qualcomm Inc.

- Cirrus Logic Inc.

- Advanced Micro Devices Inc.

- DSP Group Inc.

- Apple Inc.

- Broadcom Corporation

- Realtek Semiconductor Corporation

- Marvell Technology Group Ltd

- Samsung Group

- MediaTek Inc.

- ST Microelectronics

Recent Developments

- In March 2025, AMD completed the acquisition of ZT Systems, a leader in AI and compute infrastructure, to boost its data center AI capabilities. At CES 2025, AMD launched new Ryzen 9950X3D and 9900X3D desktop processors and the Ryzen Z2 for handheld gaming.

- Apple announced the M4 chip in May 2024, powering the new iPad Pro with advanced AI and graphics capabilities. In October 2024, Apple introduced the M4 Pro and M4 Max chips for the MacBook Pro, further improving performance and efficiency.

- In May 2024, Qualcomm introduced the Snapdragon X Elite and X Plus chipsets for Windows PCs, focusing on AI and performance. The company also launched the Snapdragon 8 Elite 2 chipset for flagship smartphones and announced the Snapdragon X80 5G modem with advanced AI features.

- Intel has been actively launching new products and expanding its AI capabilities. At CES 2025, Intel introduced the Core Ultra 200V, 200HX, and H series mobile processors, featuring integrated AI acceleration and improved power efficiency. The company is also preparing to roll out its next-generation Panther Lake processors using the advanced 18A process in late 2025.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 29.9 Bn |

| Forecast Revenue (2034) | USD 52.1 Bn |

| CAGR (2025-2034) | 5.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Type (Graphics, Audio, Other Types), By End-user Industry (Consumer Electronics, IT and Telecommunication, Media and Entertainment, Government, Other End-user Industries) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | NVIDIA Corporation, Intel Corporation, Qualcomm Inc., Cirrus Logic Inc., Advanced Micro Devices Inc., DSP Group Inc., Apple Inc., Broadcom Corporation, Realtek Semiconductor Corporation, Marvell Technology Group Ltd, Samsung Group, MediaTek Inc., ST Microelectronics, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |