Quick Navigation

Report Overview

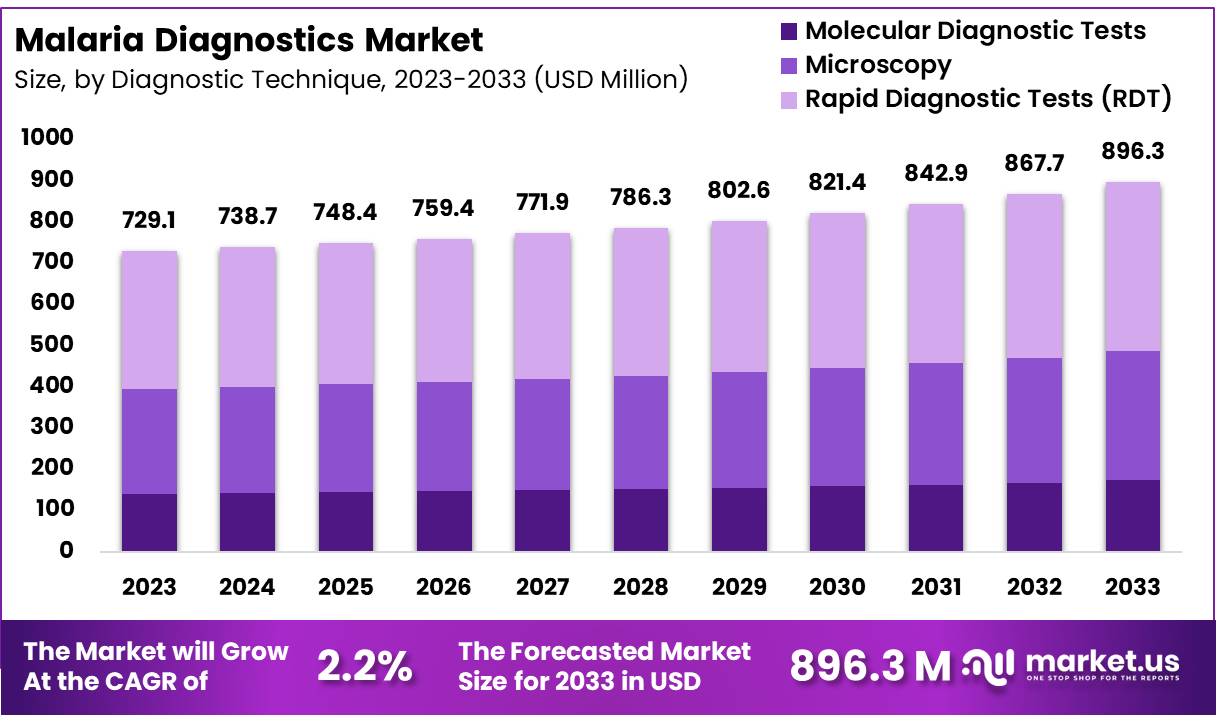

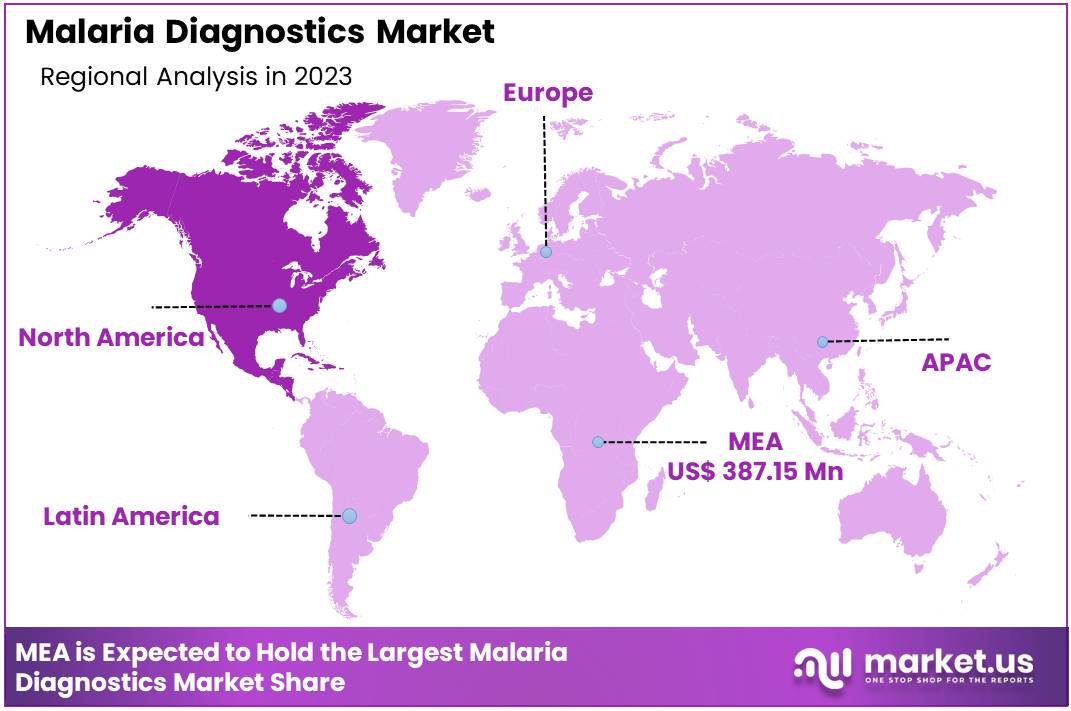

Global Malaria Diagnostics Market size is expected to be worth around US$ 896.3 Million by 2033 from US$ 729.10 Million in 2023, growing at a CAGR of 2.2% during the forecast period from 2024 to 2033. In 2023, North America led the market, achieving over 53.10% share with a revenue of US$ 90 Million.

The growth of the malaria diagnostic market is being fueled by increasing demand for advanced diagnostic solutions and the development of innovative technologies. Malaria, a life-threatening disease predominantly found in tropical and subtropical regions, remains a critical global health challenge. Its prevalence is influenced by factors such as climate change, limited economic development, inadequate healthcare infrastructure, and restricted access to advanced treatments.

Globally, malaria cases surged significantly in 2022, exceeding pre-pandemic levels recorded in 2019. Between 2000 and 2019, malaria cases declined from 243 million to 233 million. However, the pandemic disrupted progress, with an additional 11 million cases recorded in 2020 and a further increase of 5 million cases in 2022, bringing the global total to 249 million. This upward trend underscores the urgent need for advancements in malaria diagnostics to address the growing burden effectively.

Nearly half of the global population remains at risk of malaria, which caused 249 million cases and 608,000 deaths in 2022. Sub-Saharan Africa continues to bear the highest disease burden. The COVID-19 pandemic further exacerbated malaria cases and deaths, reversing pre-pandemic progress.

In response, U.S. funding for malaria control and research increased to nearly $1 billion in FY 2023, up from $822 million in FY 2013, reinforcing its position as the largest contributor to the Global Fund to Fight AIDS, Tuberculosis, and Malaria.

The President’s Malaria Initiative (PMI) Strategy for 2021 set ambitious goals to reduce mortality, significantly cut cases, and support malaria elimination efforts in high-burden regions. These initiatives, supported by increased funding, are propelling market growth and aligning with global health objectives.

Technological advancements have revolutionized malaria diagnostics, improving detection methods and disease management. Modern molecular techniques, such as Loop-Mediated Isothermal Amplification (LAMP) and nucleic acid amplification tests (NAATs), offer superior sensitivity and specificity compared to traditional methods.

The introduction of efficient rapid diagnostic tests (RDTs) has simplified point-of-care diagnosis, enabling timely and accurate identification of malaria parasites. These innovations are critical for early treatment and effective disease control, particularly in resource-limited settings with minimal access to advanced laboratory facilities.

Key Takeaways

- The Malaria Diagnostics market generated a revenue of US$ 729.10 Million and is predicted to reach US$ 896.33 Million, with a CAGR of 2.2%.

- Based on the Diagnostic Technique, the Microscopy segment generated the most revenue for the market with a market share of 34.9%.

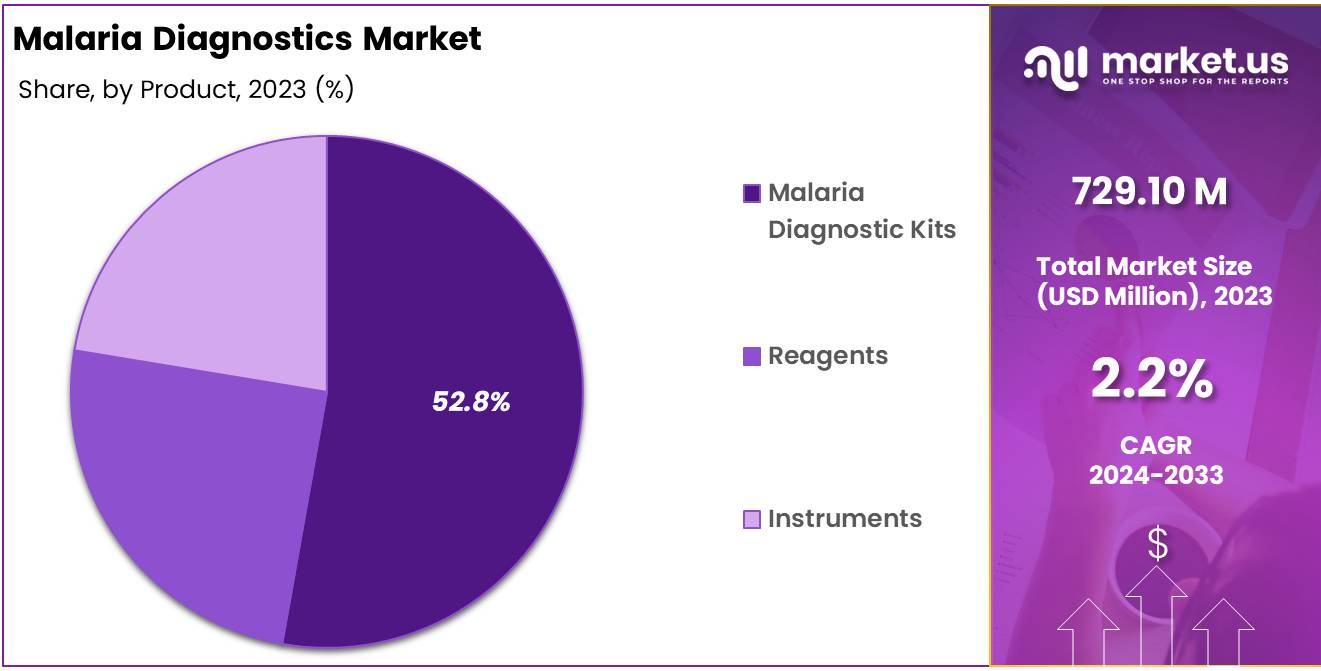

- Based on the product, the Malaria Diagnostic Kits segment generated the most revenue for the market with a market share of 52.8%.

- By End-Use, the Hospitals & Clinics segment contributed the most to the market and secured a market share of 44.8%.

- Region-wise, Middle East and Africa remained the lead contributor to the market, by claiming the highest market share, amounting to 53.10%.

By Diagnostic Technique Analysis

The Rapid Diagnostic Tests (RDT) segment led the malaria diagnostics market in 2023, capturing the largest revenue share of 45.8%. RDTs have been integral to global malaria diagnostics, with manufacturers selling 3.9 billion units between 2010 and 2022, 82% of which were distributed in sub-Saharan Africa. During this period, National Malaria Programs (NMPs) supplied 2.9 billion RDTs, with 90% directed to sub-Saharan Africa.

In 2022 alone, manufacturers sold 415.5 million RDTs, while NMPs distributed 345 million. The widespread adoption of RDTs is driven by their simplicity, rapid results, and critical role in providing efficient and accessible malaria diagnosis, especially in regions heavily burdened by the disease.

Meanwhile, the molecular diagnostic tests segment is anticipated to grow steadily over the forecast period. Techniques such as polymerase chain reaction (PCR) and Loop-Mediated Isothermal Amplification (LAMP) offer high sensitivity and specificity, enabling the detection of low parasite levels and precise identification of Plasmodium species.

These capabilities are vital for targeted treatments, early diagnosis, and effective surveillance efforts. Continuous advancements in molecular diagnostics enhance their contribution to global malaria control initiatives, improving disease management through accurate and timely intervention.

By Product Analysis

Malaria diagnostic kits emerged as the leading product segment in the malaria diagnostics market, driven by their widespread adoption and versatility in various healthcare settings. These kits provide a comprehensive solution by combining essential components like reagents, buffers, and testing devices into a single package, ensuring accuracy and ease of use. Their dominance can be attributed to the rising demand for rapid and reliable diagnostic solutions, particularly in resource-limited regions where laboratory infrastructure is scarce.

The ability of diagnostic kits to deliver quick results at the point of care has significantly contributed to their popularity, especially in regions with high malaria burden such as sub-Saharan Africa and Southeast Asia.

Additionally, advancements in kit design, including improved sensitivity and specificity, have enhanced their effectiveness in detecting Plasmodium species. The continuous distribution of these kits through government health initiatives and non-governmental organizations further supports their leading position in the market.

By End Use Analysis

The Hospitals & Clinics segment dominated the malaria diagnostics market in 2023, accounting for the largest revenue share of 44.8%. This can be attributed to the growing adoption of Rapid Diagnostic Tests (RDTs) due to their quick turnaround time, cost-effectiveness, and accessibility.

Clinics, with their smaller patient loads compared to hospitals, facilitate prompt diagnosis and administration of appropriate antimalarial treatments, thereby improving patient outcomes. Early detection and timely treatment play a vital role in managing malaria and reducing associated complications, further reinforcing the prominence of clinics in this market.

The diagnostics centers segment is projected to grow at a steady CAGR during the forecast period. Increased awareness among the target population has driven a shift towards specialized healthcare providers for disease diagnosis.

Diagnostic centers offer advanced testing capabilities, state-of-the-art laboratories, and stringent quality control measures, ensuring accurate results. Additionally, government initiatives promoting services like reimbursement are anticipated to further boost the segment’s growth.

Key Market Segments

By Diagnostic Technique

- Molecular Diagnostic Tests

- Conventional PCR

- Modernized PCR

- Microscopy

- Rapid Diagnostic Tests (RDT)

By Product

- Malaria Diagnostic Kits

- Reagents

- Instruments

By End Use

- Hospitals & Clinics

- Diagnostic Centers

- Academic and Research Institutes

Drivers

Increase in Malaria Cases Globally

The rise in global malaria cases is significantly driving the malaria diagnostics market. According to the World Health Organization (WHO), there were an estimated 247 million malaria cases worldwide in 2021, up from 245 million in 2020, with over 95% of cases occurring in the WHO African Region. This increase highlights the urgent need for robust diagnostic solutions to facilitate early detection and treatment.

Rapid diagnostic tests (RDTs) and microscopy are widely used, with RDTs accounting for a major share of diagnostic procedures due to their speed and cost-effectiveness. WHO reported the delivery of over 260 million RDTs in 2021, a rise compared to previous years, reflecting growing adoption.

The market growth is further supported by government initiatives and funding, such as the Global Fund, which allocated $4.2 billion for malaria programs in 2022-2024, and increasing technological advancements in diagnostic tools, including molecular testing and AI-based solutions.

Restrains

Limited Access in Remote Areas

Limited access to healthcare infrastructure in remote regions significantly hampers the effectiveness of malaria diagnostics, particularly in areas like Sub-Saharan Africa and rural Southeast Asia, which account for the majority of global malaria cases. According to the World Health Organization (WHO), these regions report over 95% of malaria cases, yet lack adequate diagnostic facilities.

Healthcare centers in these areas are often located far from communities, requiring extensive travel that delays timely diagnosis and treatment. Additionally, many clinics lack essential resources, such as electricity, refrigeration, and trained personnel, necessary for using advanced diagnostic tools like microscopy or molecular testing.

Even widely-used Rapid Diagnostic Tests (RDTs) face logistical challenges, as poor supply chains and insufficient distribution networks limit their availability. This is compounded by economic constraints, making even affordable solutions inaccessible to vulnerable populations. Strengthening diagnostic infrastructure in remote areas is essential to ensuring early detection, reducing disease burden, and achieving global malaria control targets..

Opportunities

Rising Awareness and Public Health Campaigns

Rising awareness about malaria’s severe health and economic impacts has spurred public health campaigns, driving demand for early diagnosis and creating growth opportunities in the malaria diagnostics market. According to the World Health Organization (WHO), malaria accounted for 619,000 deaths in 2021, with a significant portion preventable through timely diagnosis and treatment.

Global campaigns such as World Malaria Day and regional programs led by organizations like the Roll Back Malaria Partnership have increased awareness among at-risk populations about the importance of early detection. Governments and NGOs have been actively disseminating educational materials and providing free or subsidized diagnostic tools in endemic areas.

For instance, initiatives under the President’s Malaria Initiative (PMI) in Africa have scaled up diagnostic testing, with coverage expanding to over 600 million people since 2005. These efforts not only reduce disease burden but also promote widespread adoption of advanced diagnostic technologies, enhancing market prospects.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly impact the global malaria diagnostics market, influencing both demand and access. Economic disparities in malaria-endemic regions, particularly in Sub-Saharan Africa and Southeast Asia, limit healthcare funding, affecting the availability of diagnostic tools. Geopolitical instability in these areas often disrupts supply chains, delaying the distribution of diagnostic kits and resources.

For example, conflicts in regions like the Sahel have exacerbated healthcare access challenges, leaving vulnerable populations underserved. Additionally, fluctuating currency exchange rates and inflation in low-income countries increase the cost of importing diagnostic technologies, straining budgets for public health initiatives.

On a broader scale, international funding from organizations such as the Global Fund or the Bill & Melinda Gates Foundation can be impacted by macroeconomic conditions, such as global recessions, potentially reducing investments in malaria eradication programs. Addressing these factors through coordinated international efforts and policy stability is critical for market growth and accessibility.

Latest Trends

The global malaria diagnostics market is witnessing several key trends driven by technological advancements and evolving healthcare needs. One major trend is the integration of AI and machine learning in diagnostic tools, enhancing the accuracy and efficiency of malaria detection. AI-powered algorithms can analyze blood smears more quickly and accurately than traditional methods, reducing dependency on skilled personnel.

Another significant trend is the adoption of point-of-care (POC) diagnostics, such as portable Rapid Diagnostic Tests (RDTs), tailored for use in remote and resource-limited settings. Additionally, the market is experiencing a shift toward molecular diagnostics, like polymerase chain reaction (PCR) tests, which offer higher sensitivity and specificity, particularly for detecting low parasite densities.

Efforts to develop cost-effective and environmentally sustainable diagnostic kits are also gaining traction, supported by increased global funding for malaria eradication. Collaborative initiatives between public and private sectors are further driving innovations and expanding market reach..

Regional Analysis

Middle East and Africa Dominates the Global Malaria Diagnostics Market

The Middle East and Africa malaria diagnostics market dominated the global market in 2023, accounting for a 53.10% share, driven by the region’s significant malaria burden, which represents over 90% of global cases. Robust growth in the market is fueled by increased government efforts and international support from organizations such as the World Health Organization (WHO) and the Global Fund, which are actively promoting early detection and treatment initiatives.

Improved healthcare infrastructure, along with advancements in diagnostic technologies like Rapid Diagnostic Tests (RDTs) and molecular diagnostics, is enhancing accessibility and accuracy across the region. Public-private partnerships and collaborations between local governments and international entities are further expanding the availability of diagnostics, particularly in rural and underserved areas.

Additionally, rising awareness of the importance of early diagnosis in endemic regions is driving demand. Continued research and development to improve diagnostic sensitivity, specificity, and affordability is strengthening the region’s fight against malaria.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The competitive landscape in the global malaria diagnostics market is highly fragmented, with numerous players offering a range of diagnostic solutions, from Rapid Diagnostic Tests (RDTs) to molecular diagnostics. Key players in the market include Abbott Laboratories, Roche Diagnostics, Thermo Fisher Scientific, Siemens Healthineers, and BD (Becton, Dickinson and Company), which dominate with innovative and widely adopted technologies.

These companies are focusing on product development, enhancing diagnostic sensitivity, and lowering costs to expand their reach in malaria-endemic regions. The market is also seeing an increase in partnerships and collaborations, with public-private partnerships playing a pivotal role in improving diagnostic access in underserved areas.

Emerging players are introducing cost-effective solutions, including mobile and portable diagnostics, to address challenges in remote areas. Companies are also investing in advanced technologies, such as AI-driven diagnostics and next-generation sequencing platforms, to offer faster, more accurate, and affordable malaria detection. The market’s competitiveness is further driven by strategic mergers, acquisitions, and collaborations aimed at boosting market share..

Top Key Players

- Access Bio., Inc.

- Abbott Laboratories

- Premier Medical Corporation Pvt. Ltd.

- Sysmex Partec GmbH

- bioMérieux

- Beckman Coulter, Inc.

- Siemens Healthineers

- Leica Microsystems GmbH

- Nikon Corporation

- Olympus Corporation

- Bio-Rad Laboratories, Inc.

Recent Developments

- In July 2022, Mylab Discovery Solutions introduced the first combined PCR test capable of distinguishing between Chikungunya, Zika, malaria, dengue, Salmonellosis bacterial species, Leptospirosis, and Leishmaniasis parasites.

- In February 2024, researchers from Rice University developed a new malaria diagnostic test that offers a faster and more user-friendly alternative to traditional methods. This innovation has the potential to significantly improve patient outcomes, especially in rural regions with limited healthcare resources.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 729.10 Million |

| Forecast Revenue (2033) | US$ 896.33 Million |

| CAGR (2024-2033) | 2.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Diagnostic Technique- Molecular Diagnostic Tests, Microscopy, and Rapid Diagnostic Tests (RDT), By Product – Malaria Diagnostic Kits, Reagents and Instruments, End Use- Hospitals & Clinics, Diagnostic Centers and Academic and Research Institutes. |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Access Bio., Inc., Abbott Laboratories, Premier Medical Corporation Pvt. Ltd., Sysmex Partec GmbH, bioMérieux, Beckman Coulter, Inc., Siemens Healthineers, Leica Microsystems GmbH, Nikon Corporation, Olympus Corporation and Bio-Rad Laboratories, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |