Quick Navigation

- Report Overview

- Key Takeaways

- Component Analysis

- End-User Industry Analysis

- Function Analysis

- Logistics Type Analysis

- Organization Size Analysis

- Software Application Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Emerging Trends

- Regional Analysis

- Competitive Landscape

- Recent Developments

- Report Scope

Report Overview

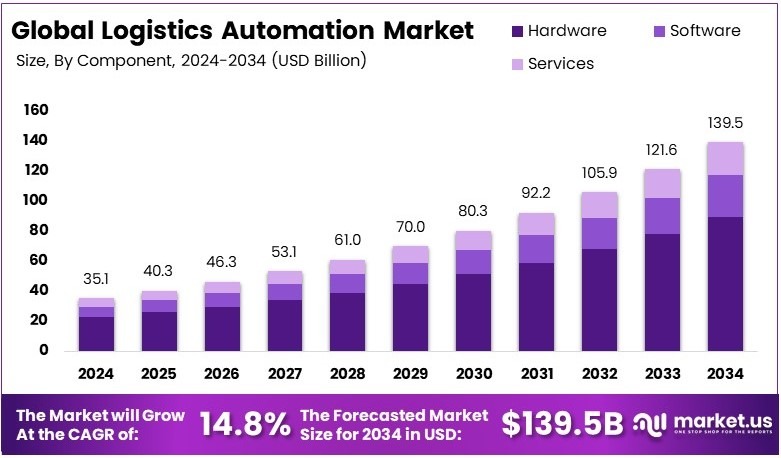

The Global Logistics Automation Market size is expected to be worth around USD 139.5 Billion by 2034, from USD 35.1 Billion in 2024, growing at a CAGR of 14.8% during the forecast period from 2025 to 2034.

Logistics Automation involves automated systems for inventory management, order processing, and shipment tracking. This approach reduces manual work and increases accuracy. Companies use these solutions to optimize operations. Automation in logistics supports decision-making and improves efficiency in transportation networks.

Logistics Automation Market consists of companies offering automated supply chain solutions. The market includes providers of software, hardware, and robotics for inventory control, order processing, and shipment tracking. Firms aim to boost operational efficiency and accuracy. Companies serve industries seeking reduced manual labor and enhanced process reliability across global markets.

The Logistics Automation market is rapidly expanding, driven by the surge in e-commerce. Amazon’s growth in Australia, with six fulfillment centers and plans for five more by 2026, highlights the escalating demand for automated logistics solutions. This expansion reflects the broader trend of increasing online shopping and the need for efficient distribution systems.

Moreover, the adoption of AI in logistics is becoming increasingly prevalent. Over 80% of businesses have integrated AI into their operations, with 35% using AI across multiple departments. This widespread use of AI enhances operational efficiencies and drives innovation within the logistics sector, demonstrating the market’s competitive edge.

Additionally, autonomous delivery innovations are revolutionizing logistics. Zipline, known for its drone delivery services, has covered nearly 100 million miles in Africa for medical supplies and is now expanding into U.S. cities with partners like Walmart. This not only shows the potential for scale in autonomous logistics but also underscores the significant impact on local and global supply chains.

Government regulations also play a crucial role in shaping the logistics automation market. They set standards that ensure safety and efficiency in automated systems, fostering a stable environment for growth and innovation. This governmental oversight helps maintain market integrity and encourages continual investment in new technologies.

Key Takeaways

- The Logistics Automation Market was valued at USD 35.1 billion in 2024 and is projected to reach USD 139.5 billion by 2034, with a CAGR of 14.8%.

- In 2024, Hardware dominates the component segment with 64.6%, driven by digital transformation and automation trends in supply chain management.

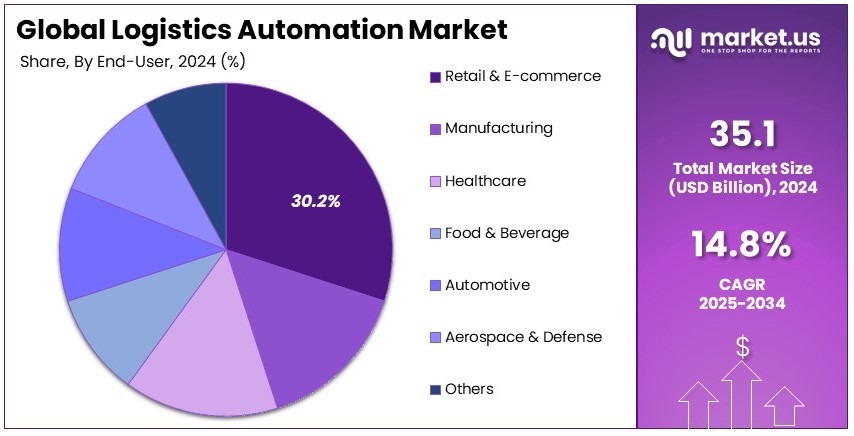

- In 2024, Retail & E-commerce leads the end-user industry segment with 30.2%, reflecting rising online retail and digital engagement.

- In 2024, Transportation Management dominates the function segment with 56.8%, optimizing logistics operations through streamlined process integration globally.

- In 2024, Large Enterprises lead the organization size segment with 58.4%, emphasizing scale-driven investments in advanced automation technologies.

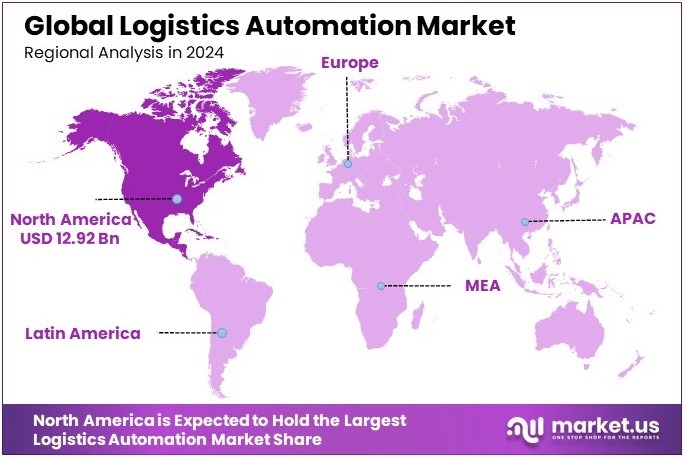

- In 2024, North America leads the regional segment with 36.8%, underpinned by a USD 12.92 billion market contribution and technological advancements.

Component Analysis

Hardware dominates with 64.6% due to strong performance and integration benefits.

In the Logistics Automation Market, the Hardware segment leads the way by capturing 64.6% of the growth share. This segment includes devices such as sensors, RFID tags, and robotics that help automate tasks and improve efficiency in warehouses and distribution centers. For example, large retailers in the United States have invested heavily in advanced scanning and robotic systems to speed up their order processing.

The use of smart hardware solutions helps companies track inventory accurately and reduce human error, which in turn drives overall market growth. This success is supported by increased consumer demand for faster deliveries and reduced operational costs, making hardware solutions the backbone of modern logistics operations.

Such progress is evident in major markets like Europe and Asia, where companies are rapidly adopting these solutions to stay competitive. Meanwhile, the Software sub-segment plays a supportive role by providing the necessary applications and platforms that interface with hardware, ensuring smooth data exchange and control.

Similarly, the Services sub-segment, which includes maintenance, consulting, and technical support, is essential for sustaining hardware performance. Its role is critical in educating users and ensuring that the hardware systems operate at peak efficiency. Together, these segments create a comprehensive ecosystem that drives the market forward.

End-User Industry Analysis

Retail & E-commerce dominates with 30.2% due to rising digital sales and supply chain innovation.

In the Logistics Automation Market, the Retail & E-commerce sector is the leader with a 30.2% growth share. This industry has embraced automation to handle increasing online orders, reduce delays, and manage inventory more accurately. Large retail chains and online giants in North America and Europe rely on automation to improve their order fulfillment speed and reduce errors.

As e-commerce continues to expand, companies invest in automated storage and picking systems to keep pace with demand. The sector’s focus on customer satisfaction and speedy deliveries fuels its need for innovative logistics solutions. In this context, the Manufacturing sub-segment is also growing as companies integrate automation to streamline production and distribution, thereby boosting efficiency in assembly lines.

Healthcare & Pharmaceuticals contribute by using automated systems for strict inventory control and to manage complex supply chains that require high precision. Food & Beverage businesses are increasingly relying on automation for temperature-controlled storage and fast distribution to meet safety standards. The Automotive industry uses automation to synchronize parts delivery with assembly schedules, ensuring minimal downtime.

Aerospace & Defense benefits from automated logistics by maintaining strict control over high-value components, and the Others category supports niche markets with specialized requirements. Each of these segments plays an important role by addressing unique challenges within their supply chains, thereby contributing to the overall market momentum.

Function Analysis

Transportation Management dominates with 56.8% due to its critical role in streamlining distribution and reducing delays.

In the Logistics Automation Market, the Transportation Management function stands out by capturing 56.8% of the growth share. This function is pivotal for planning, executing, and optimizing the physical movement of goods from one location to another.

Companies use advanced software and automated tracking systems to schedule shipments, choose optimal routes, and monitor delivery progress. For instance, global logistics providers in Asia and Europe have adopted automated transportation management systems to ensure that their fleets run efficiently and deliveries occur on time.

The reliance on real-time data enables quick adjustments to address unexpected delays, ensuring a smoother supply chain process. This critical role in reducing transportation costs and enhancing service quality drives significant investments in this area.

On the other hand, the Inventory & Storage Management sub-segment supports the market by ensuring that goods are stored in optimal conditions and are readily available when needed. Its contribution, though smaller in percentage, is essential for maintaining overall supply chain balance.

Logistics Type Analysis

Sales Logistics dominates with 41.5% due to its direct impact on revenue generation and market responsiveness.

In the Logistics Automation Market, the Sales Logistics category leads with 41.5% of the growth share. This segment focuses on the efficient delivery of products to customers, ensuring that goods reach retail outlets and end users quickly and reliably.

Companies in this category benefit from streamlined processes that enhance the speed of order fulfillment and customer satisfaction. For example, popular retail chains in urban centers have adopted automated sorting and dispatch systems that minimize delivery times and improve customer experiences.

The effectiveness of Sales Logistics is key to driving revenue, especially in fast-moving consumer goods and e-commerce sectors. Meanwhile, the Production Logistics sub-segment also plays a role by coordinating the supply of raw materials and components to manufacturing facilities, ensuring smooth production cycles.

The Recovery Logistics sub-segment contributes by managing the return or recycling of products, which is becoming more important in sustainable business practices. Procurement Logistics, though smaller, is crucial for the timely sourcing and delivery of parts and materials necessary for production.

Organization Size Analysis

Large Enterprises dominate with 58.4% due to their capacity for large-scale automation investments and extensive operational networks.

In the Logistics Automation Market, Large Enterprises capture 58.4% of the growth share by leveraging their scale and resources. These companies invest in robust automation systems to manage complex and high-volume logistics operations.

Their extensive supply chains and distribution networks require integrated solutions that combine hardware, software, and expert services to maintain efficiency. For example, multinational retailers and manufacturers in North America and Europe deploy advanced logistics automation systems to synchronize their global operations and ensure timely deliveries.

Software Application Analysis

Order Management dominates with 32.1% due to its central role in streamlining customer orders and ensuring operational accuracy.

In the Logistics Automation Market, the Order Management application stands out by capturing 32.1% of the growth share. This software plays a crucial role in managing the entire lifecycle of customer orders, from initial placement to final delivery confirmation.

Efficient order management systems help companies track orders, process payments, and schedule deliveries in a timely manner. For example, major e-commerce platforms in North America use automated order management software to handle high volumes of transactions and minimize errors.

The dominant position of Order Management reflects the market’s emphasis on customer-centric operations and the need for seamless integration across logistics processes. This focus is likely to continue as businesses seek to improve responsiveness and service quality in a competitive market environment.

Key Market Segments

By Component

- Hardware

- Software

- Services

By End-User Industry

- Retail & E-commerce

- Manufacturing

- Healthcare & Pharmaceuticals

- Food & Beverage

- Automotive

- Aerospace & Defense

- Others

By Function

- Inventory & Storage Management

- Transportation Management

By Logistics Type

- Sales Logistics

- Production Logistics

- Recovery Logistics

- Procurement Logistics

By Organization Size

- Large Enterprises

- Small & Medium Enterprises

By Software Application

- Inventory Management

- Order Management

- Yard Management

- Shipping Management

- Labor Management

- Vendor Management

- Customer Support

- Others

Driving Factors

Faster and Smarter Supply Chains Drive Market Growth

The logistics automation market is growing rapidly due to the increasing demand for faster and more efficient supply chain operations. Companies now need quicker processing and delivery systems to meet customer expectations and stay competitive.

The rise of e-commerce has led to a greater need for automated warehousing solutions. Retailers and distributors invest in technology that speeds up order fulfillment and minimizes human error. This trend is transforming traditional storage and distribution practices.

Advancements in robotics, artificial intelligence, and machine learning are making smart logistics a reality. These technologies optimize routes, reduce waste, and enhance operational accuracy. They enable firms to manage large volumes of data and streamline processes effectively.

The expansion of autonomous vehicles and drones for last-mile delivery is further boosting the market. These innovations reduce delivery times and lower costs while improving service reliability. They are set to redefine the future of urban logistics and customer satisfaction.

Restraining Factors

High Investment and Security Challenges Restraint Market Growth

High initial investment and implementation costs create a major hurdle for companies adopting automation technologies. The upfront expenditure on hardware and software often limits the pace of digital transformation.

Data security risks and cyber threats pose serious challenges to automated logistics systems. Companies must invest in robust cybersecurity measures to protect sensitive information and ensure operational integrity, which can add to overall expenses.

Workforce resistance to automation and potential job displacement concerns also slow market growth. Employees may be hesitant to embrace new technology, leading to training and adjustment challenges. This resistance can delay the full integration of automation.

Integration challenges with legacy logistics infrastructure and IT systems further restrain growth. Many organizations struggle to merge old systems with modern solutions, causing delays and increasing costs. These hurdles require careful planning and significant investment to overcome.

Growth Opportunities

AI and Connectivity Provide Opportunities

The development of AI-driven predictive analytics offers new opportunities for demand forecasting. Companies can now analyze trends and adjust their inventory levels to meet market needs more accurately.

Adoption of 5G and IoT technology enhances real-time inventory and fleet tracking. This connectivity allows for faster data transfer and better monitoring of logistics operations. It improves response times and minimizes delays in the supply chain.

Expansion of automated sorting and pick-and-pack technologies in warehouses is on the rise. These systems boost productivity and accuracy in order processing. They help reduce labor costs while increasing overall efficiency.

Increasing use of blockchain technology provides a secure and transparent way to manage supply chains. It enhances data integrity and builds trust among stakeholders. This innovation offers a reliable method to track shipments and verify transactions in real time.

Emerging Trends

Digital and Autonomous Trends Are Latest Trending Factor

The growing popularity of autonomous mobile robots (AMRs) in fulfillment centers is transforming warehouse operations. These robots efficiently move goods and reduce manual labor, enhancing productivity.

Adoption of cloud-based logistics platforms is gaining momentum for end-to-end visibility. These platforms allow companies to monitor their entire supply chain in real time. They help in making informed decisions quickly and efficiently.

The expansion of AI-powered chatbots and virtual assistants for order management is trending upward. These tools offer immediate support and streamline customer service processes. They reduce response times and improve customer satisfaction.

Integration of edge computing is also on the rise for faster and more secure logistics automation. This technology processes data closer to its source, reducing latency and enhancing security. It supports a more responsive and robust automation framework for modern logistics systems.

Regional Analysis

North America Dominates with 36.8% Market Share

North America leads the Logistics Automation Market with a 36.8% share, totaling USD 12.92 billion. This significant market presence is underpinned by robust investment in automation technologies and a strong logistics infrastructure.

The region benefits from the adoption of advanced technologies such as AI and robotics, which streamline warehouse and inventory management. Additionally, a thriving e-commerce sector drives the demand for efficient logistics solutions.

The future influence of North America in the global Logistics Automation Market is poised to grow as more companies adopt automation to enhance supply chain efficiency and reduce operating costs. The ongoing expansion of e-commerce and the integration of IoT devices are expected to further boost the demand for sophisticated logistics automation systems.

Regional Mentions:

- Europe: Europe holds a significant share in the Logistics Automation Market, driven by its focus on efficiency and sustainability. The region’s advanced manufacturing and supply chain operations utilize automation to reduce costs and environmental impact.

- Asia Pacific: Asia Pacific is rapidly advancing in the Logistics Automation Market, fueled by fast-paced industrial growth and the rise of digital commerce. Major economies like China and Japan are investing heavily in automation technologies to handle large volumes of manufacturing and retail logistics.

- Middle East & Africa: The Middle East and Africa are experiencing growth in Logistics Automation, with investments in smart logistics and warehouse management systems. These technologies are crucial in enhancing the efficiency of the region’s expanding trade and logistics sectors.

- Latin America: Latin America is making strides in the Logistics Automation Market as businesses modernize their supply chains. The adoption of automated systems is increasingly seen in sectors such as manufacturing and retail to improve competitiveness and operational agility.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

In the Logistics Automation market, four companies stand out for their influential roles and contributions: Honeywell International Inc., Siemens AG, KION Group AG, and Daifuku Co., Ltd. These leaders drive innovation and efficiency in the rapidly evolving logistics sector.

Honeywell International Inc. is a key player, known for its advanced automation solutions that enhance warehouse and supply chain operations. Their technologies focus on improving accuracy and reducing operational costs, making logistics processes smoother and more reliable.

Siemens AG offers cutting-edge automation technologies that integrate digitalization and smart logistics solutions. Their systems are pivotal in optimizing warehouse operations and supply chains, ensuring high efficiency and adaptability to changing market demands.

KION Group AG, including its subsidiary Dematic, leads in providing integrated automation solutions for warehouses and distribution centers. Their focus on scalable and flexible systems allows businesses to enhance productivity and accommodate growth effectively.

Daifuku Co., Ltd. is renowned for its expertise in material handling solutions, particularly in automating complex logistics tasks. Their commitment to innovation in automated storage and retrieval systems (ASRS) and robotics positions them at the forefront of the industry.

These companies significantly influence the Logistics Automation market by setting trends in technology and system integration. Their continued focus on research and development in smart logistics solutions will likely drive further advancements in the industry, meeting the increasing demands for faster, more efficient supply chain management.

Major Companies in the Market

- Honeywell International Inc.

- Siemens AG

- KION Group AG

- Daifuku Co., Ltd.

- Murata Machinery, Ltd.

- Dematic (KION Group)

- Jungheinrich AG

- SSI Schaefer AG

- Mecalux, S.A.

- Knapp AG

- TGW Logistics Group

- Swisslog Holding AG

- Vanderlande Industries

Recent Developments

- GXO Logistics and Clipper Logistics: On October 2022, GXO Logistics, the world’s largest pure-play contract logistics provider, finalized its acquisition of Clipper Logistics plc. This strategic move expanded GXO’s presence in Germany and Poland, adding over 50 sites, 10 million square feet of warehouse space, and approximately 10,000 employees to its operations.

- Columbus McKinnon and montratec GmbH: Columbus McKinnon Corporation, a motion technology manufacturer, entered into a definitive agreement to acquire montratec GmbH, a German automation company. This acquisition aims to enhance Columbus McKinnon’s automation solutions portfolio, particularly in material handling and logistics automation.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 35.1 Billion |

| Forecast Revenue (2034) | USD 139.5 Billion |

| CAGR (2025-2034) | 14.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Hardware, Software, Services), By End-User Industry (Retail & E-commerce, Manufacturing, Healthcare & Pharmaceuticals, Food & Beverage, Automotive, Aerospace & Defense, Others), By Function Outlook (Inventory & Storage Management, Transportation Management), By Logistics Type Outlook (Sales Logistics, Production Logistics, Recovery Logistics, Procurement Logistics), By Organization Size Outlook (Large Enterprises, Small & Medium Enterprises), By Software Application Outlook (Inventory Management, Order Management, Yard Management, Shipping Management, Labor Management, Vendor Management, Customer Support, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Honeywell International Inc., Siemens AG, KION Group AG, Daifuku Co., Ltd., Murata Machinery, Ltd., Dematic (KION Group), Jungheinrich AG, SSI Schaefer AG, Mecalux, S.A., Knapp AG, TGW Logistics Group, Swisslog Holding AG, Vanderlande Industries |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |