Global Livestock Monitoring Market By Components (Hardware (GPS Trackers, Health Monitoring Tags, Rumination and Feeding Monitors, Biometric Sensors and Others), Software and Services), By Animal Type (Cattle (Bovine), Swine (Pigs), Poultry (Chickens/Broilers), Equine (Horses) and Others), By Application (Health and Disease Detection, Location and Tracking, Reproductive Management, Behavioral Analysis, Environmental Monitoring, Automated Feeding and Others), By End User (Dairy Farms, Beef Farms & Feedlots, Poultry Farms, Swine Farms and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180301

- Number of Pages: 332

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

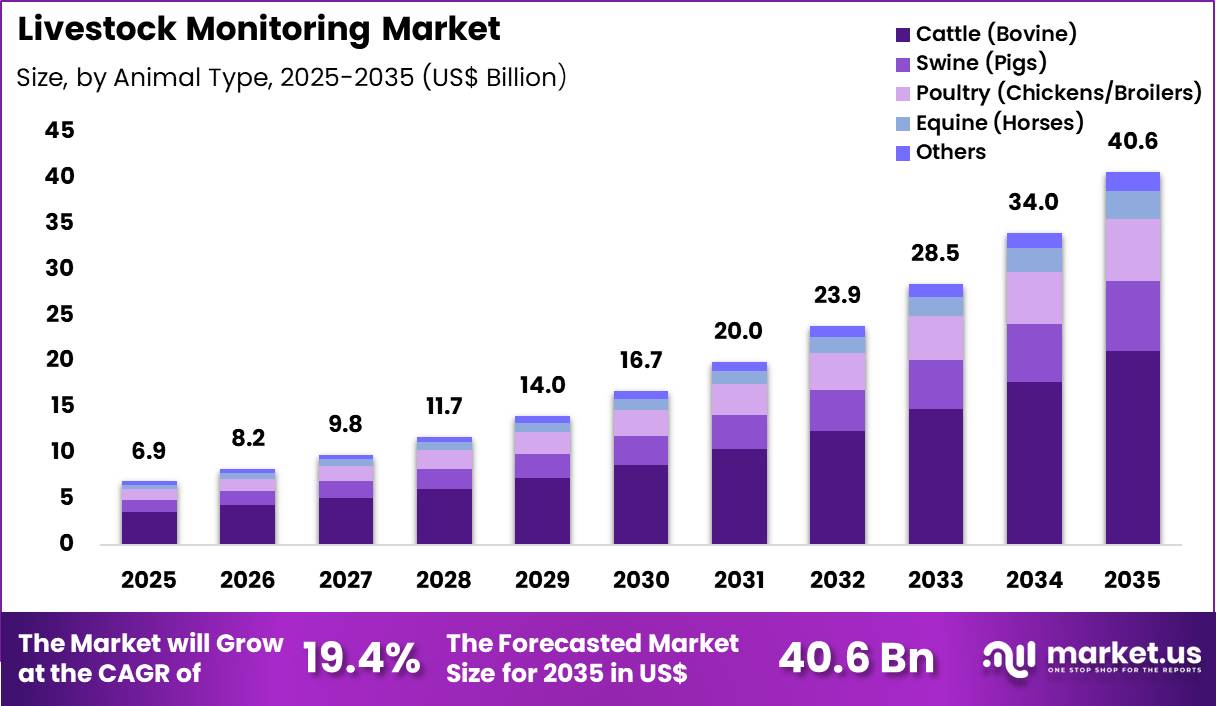

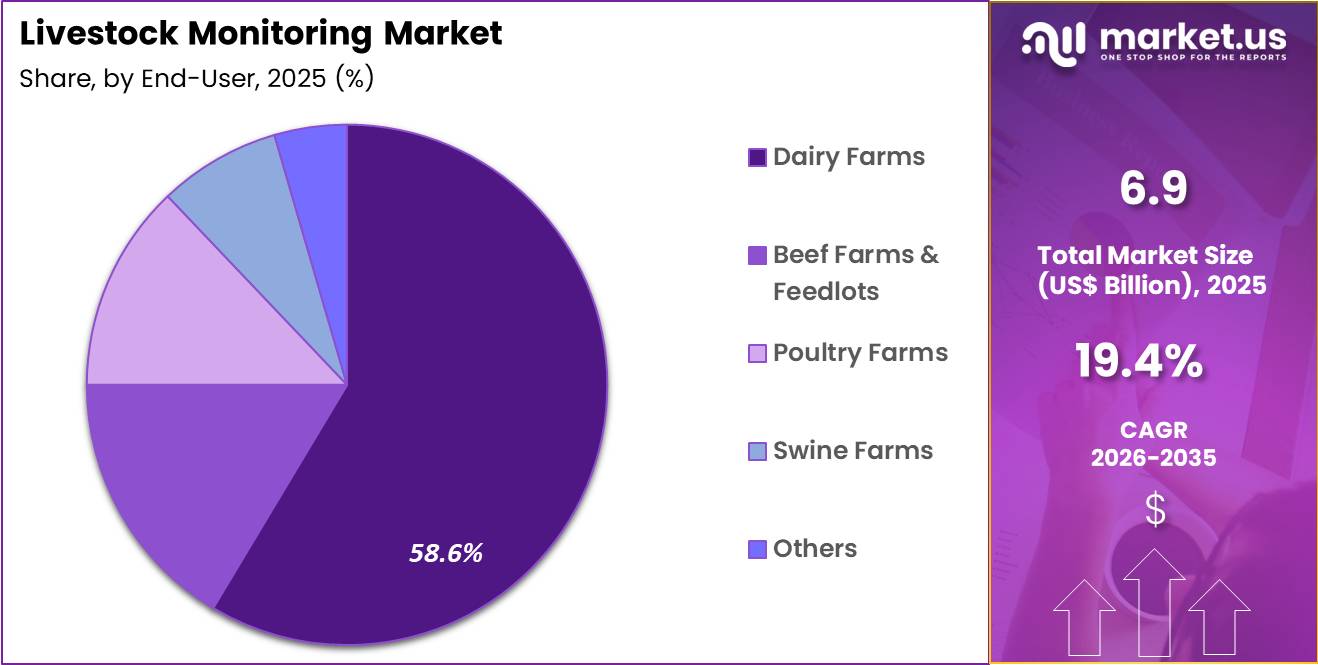

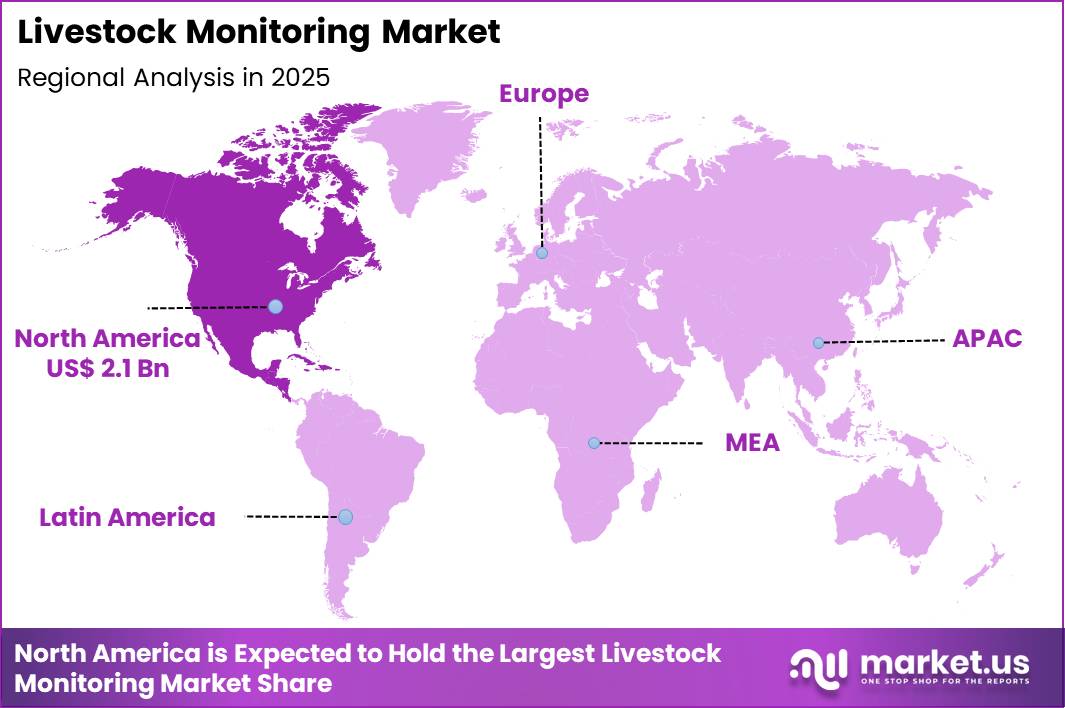

The Global Livestock Monitoring Market size is expected to be worth around US$ 40.6 Billion by 2035 from US$ 6.9 Billion in 2025, growing at a CAGR of 19.4% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 29.5% share with a revenue of US$ 2.1 Billion.

Increasing need for efficient livestock management drives the Livestock Monitoring market as producers adopt technologies that enhance animal welfare and productivity. Farmers increasingly use sensor-based collars on dairy cows to track rumination time and activity, identifying health issues like ketosis or mastitis before clinical signs appear.

These devices support reproductive management by detecting estrus in beef cattle through behavioral changes, optimizing breeding schedules and improving conception rates. Swine producers apply camera systems and weight scales to monitor growth rates and feed intake, allowing precision feeding that minimizes waste and maximizes growth.

Poultry operations utilize environmental sensors to regulate temperature and humidity, preventing heat stress and improving flock uniformity and egg production. Manufacturers pursue opportunities to integrate artificial intelligence that predicts disease outbreaks, expanding applications in large-scale operations where early alerts reduce mortality and antibiotic use.

Developers advance multi-parameter wearable devices that combine location tracking with vital signs monitoring, broadening utility in extensive grazing systems for sheep and cattle. These innovations facilitate sustainable practices by optimizing resource use in feed and water management.

Opportunities emerge in cloud-based platforms that enable remote decision-making for multi-farm enterprises. Recent trends emphasize integration with automated feeding and milking systems, positioning the market for growth in data-driven livestock production focused on welfare, efficiency, and environmental sustainability.

Key Takeaways

- In 2025, the market generated a revenue of US$ 6.9 Billion, with a CAGR of 19.4%, and is expected to reach US$ 40.6 Billion by the year 2035.

- The components segment is divided into hardware, software and services, with hardware taking the lead with a market share of 73.5%.

- Considering animal type, the market is divided into cattle (bovine), swine (pigs), poultry (chickens/broilers), equine (horses) and others. Among these, cattle (bovine)held a significant share of 52.1%.

- Furthermore, concerning the application segment, the market is segregated into health and disease detection, location and tracking, reproductive management, behavioral analysis, environmental monitoring, automated feeding and others. The health and disease detection sector stands out as the dominant player, holding the largest revenue share of 61.3% in the market.

- The end user segment is segregated into dairy farms, beef farms & feedlots, poultry farms, swine farms and others, with the dairy farms segment leading the market, holding a revenue share of 58.6%.

- North America led the market by securing a market share of 29.5%.

Components Analysis

Hardware accounted for 73.5% of growth within components and dominates the livestock monitoring market due to the increasing deployment of wearable sensors, smart collars, RFID tags, and automated monitoring devices across commercial farms. Farmers increasingly rely on real-time health tracking systems to monitor animal productivity and detect illness early.

Hardware solutions enable accurate physiological monitoring such as temperature, movement, and rumination patterns, improving herd management efficiency. Segment growth is projected to strengthen as large-scale farms invest in digital transformation to reduce labor dependency and improve operational productivity.

Rising demand for precision livestock farming supports the installation of advanced monitoring equipment across dairy and meat production facilities. Governments and agricultural institutions promote smart farming initiatives to improve livestock health outcomes.

Integration of IoT-enabled devices enhances decision-making capabilities at the farm level. Hardware adoption is anticipated to expand as farmers prioritize preventive health management and disease control. Increased focus on sustainable farming practices further drives investment in automated livestock monitoring infrastructure.

Animal Type Analysis

Cattle accounted for 52.1% of growth within animal type and dominate the livestock monitoring market due to their economic importance in dairy and beef production systems. Monitoring cattle health, feeding behavior, and reproductive cycles supports higher milk yield and improved meat quality.

Farmers increasingly implement sensor-based tracking solutions to identify early signs of infection and nutritional deficiencies. Segment growth is expected to accelerate as dairy farm operators adopt digital herd management platforms to improve breeding efficiency.

Monitoring technologies help reduce mortality rates and optimize productivity across large herds. Increasing demand for dairy products supports continuous investment in cattle monitoring infrastructure. Livestock producers aim to enhance traceability and regulatory compliance through digital monitoring tools.

Automated health alerts assist in improving veterinary intervention timelines. Adoption is likely to increase as farmers recognize the benefits of precision livestock management for profitability and sustainability.

Application Analysis

Health and disease detection accounted for 61.3% of growth within applications and dominate due to the growing need for early diagnosis of infections and metabolic disorders in livestock populations. Continuous monitoring of physiological parameters helps farmers reduce treatment costs and improve animal welfare standards. Real-time alerts assist in preventing disease outbreaks and minimizing productivity losses across farms.

Segment growth is projected to strengthen as veterinary diagnostics increasingly integrate sensor-driven monitoring technologies. Automated health tracking improves intervention efficiency and reduces dependency on manual observation.

Regulatory emphasis on animal health and food safety supports adoption across commercial farming operations. Digital health monitoring systems enhance productivity by enabling proactive disease management.

Integration with farm management software improves treatment planning and outcome tracking. Growth is anticipated to continue as livestock producers prioritize preventive healthcare strategies.

End-User Analysis

Dairy farms accounted for 58.6% of growth within end-users and dominate the livestock monitoring market due to their reliance on consistent milk production and herd health optimization. Monitoring technologies help dairy operators track lactation cycles, feeding behavior, and stress levels in cattle.

Smart monitoring systems enable timely intervention for health issues that affect milk yield and quality. Segment growth is expected to increase as dairy farms adopt automated solutions to improve productivity and reduce operational costs.

Rising consumer demand for dairy products supports investment in advanced herd management technologies. Monitoring platforms assist in optimizing breeding programs and improving reproductive success rates.

Integration with digital farm management systems enhances decision-making efficiency. Adoption is likely to expand as dairy farms implement precision livestock farming practices to ensure sustainable production and improved animal welfare.

Key Market Segments

By Components

- Hardware

- GPS Trackers

- Health Monitoring Tags

- Rumination and Feeding Monitors

- Biometric Sensors

- Others

- Software

- Services

By Animal Type

- Cattle (Bovine)

- Swine (Pigs)

- Poultry (Chickens/Broilers)

- Equine (Horses)

- Others

By Application

- Health and Disease Detection

- Location and Tracking

- Reproductive Management

- Behavioral Analysis

- Environmental Monitoring

- Automated Feeding

- Others

By End User

- Dairy Farms

- Beef Farms & Feedlots

- Poultry Farms

- Swine Farms

- Others

Drivers

Rising demand for precision livestock farming to enhance productivity is driving the market.

The expanding adoption of precision farming practices in livestock operations has substantially increased the need for continuous monitoring solutions to optimize feed efficiency and health management. Larger commercial farms are implementing monitoring technologies to track individual animal behavior and physiological parameters.

Producers are seeking real-time data to make informed decisions on breeding and disease prevention. The correlation between herd size expansion and operational complexity further amplifies the requirement for advanced monitoring systems.

Government agricultural programs encourage technology use to improve overall farm efficiency. Livestock monitoring enables early detection of health issues, reducing mortality rates in commercial herds. National agricultural statistics reflect the shift toward data-driven management in animal production.

Leading suppliers are developing integrated sensor platforms to support this trend. This driver promotes the integration of monitoring with farm management software. The number of beef cows in the United States increased by 5.9% from 2012 to 2022 according to USDA National Agricultural Statistics Service data.

Restraints

High initial investment required for sensor deployment is restraining the market.

The considerable upfront costs associated with installing sensors, tags, and supporting infrastructure limit adoption among smaller livestock operations. Many producers face challenges securing financing for monitoring equipment amid fluctuating commodity prices. Smaller farms often lack the technical expertise to implement and maintain complex monitoring systems effectively.

The correlation between farm size and technology affordability further restricts market penetration in the sector. Government subsidy programs for precision agriculture provide partial support but are insufficient for full deployment.

Producers may delay investments due to uncertain return on investment timelines. This restraint is especially evident in extensive grazing systems where infrastructure is limited. Suppliers are exploring leasing options to address these barriers. Despite long-term productivity benefits, financial constraints slow widespread implementation. High initial investment required for sensor deployment remains a primary market restraint.

Opportunities

Government initiatives for animal disease traceability are creating growth opportunities.

The implementation of national animal identification and traceability programs offers significant potential for livestock monitoring systems to enhance disease control and supply chain transparency. Governmental regulations on animal movement require reliable identification and health tracking technologies.

Increasing focus on food safety and export compliance amplifies demand for monitoring solutions in livestock supply chains. Partnerships between producers and government agencies facilitate adoption of compliant monitoring platforms.

The large number of livestock movements across state lines magnifies opportunities for integrated tracking systems. Educational campaigns for producers promote the benefits of monitoring for regulatory compliance. This opportunity enables suppliers to develop systems aligned with national traceability standards.

Leading organizations are expanding offerings to include regulatory reporting features. Overall, traceability initiatives align with efforts to strengthen animal health security. Government initiatives for animal disease traceability are a key growth opportunity.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the livestock monitoring market through farm income levels, feed prices, and capital spending by commercial producers. Inflation increases the cost of sensors, tracking tags, connectivity modules, and farm management software, which slows technology adoption among small and mid sized farms.

Higher interest rates limit access to affordable financing for precision livestock investments and smart monitoring infrastructure. Geopolitical tensions disrupt supplies of electronic components, GPS units, and wireless communication hardware, creating procurement delays and pricing uncertainty.

Current US tariffs on imported monitoring devices and semiconductors raise equipment costs and tighten margins for solution providers. These pressures can delay digital transformation plans in price sensitive agricultural operations.

At the same time, producers strengthen local supplier partnerships and focus on improving herd productivity through data driven insights. Growing demand for animal health tracking and operational efficiency continues to support steady and confident market growth.

Latest Trends

Adoption of wearable sensors for individual animal monitoring is a recent trend in the market.

In 2024, the deployment of wearable sensors and ear tags with real-time health monitoring capabilities has gained momentum in commercial livestock operations. These devices provide continuous data on activity, temperature, and rumination patterns for early disease detection.

Producers have adopted collar and tag systems for dairy and beef herds to optimize breeding and feeding decisions. Clinical evaluations in 2024 confirmed improved health outcomes through proactive interventions.

Adoption rates of wearable livestock technologies were 1% for small farms and 12% for large farms in the United States according to the U.S. Department of Agriculture Economic Research Service 2024 report. This development addresses limitations in traditional visual observation methods.

The trend emphasizes integration with farm management software for comprehensive data analysis. Regulatory support for electronic identification has accelerated deployment in commercial herds. Industry efforts focus on battery life and data accuracy improvements. These innovations aim to enhance animal welfare while improving operational efficiency in modern livestock production.

Regional Analysis

North America is leading the Livestock Monitoring Market

North America accounted for 29.5% of the Livestock Monitoring market in 2025, supported by strong digital farming adoption across the US and Canada. Regional producers have increasingly integrated sensor based tracking systems, automated feeding technologies, and health surveillance platforms to improve productivity and reduce operational losses.

Government backed precision agriculture programs and rising labor shortages have accelerated the shift toward real time herd analytics. The US Department of Agriculture reported in its 2022 Census of Agriculture that farms using precision livestock technologies such as automated monitoring tools increased notably as over 60% of dairy operations adopted some form of digital management system.

Large scale dairy and beef producers continue to invest in RFID enabled ear tags and behavior tracking software to enhance disease detection. Expanding commercial farm sizes have also created demand for centralized monitoring dashboards.

Cloud connected farm management platforms now allow ranchers to make faster breeding and feeding decisions. Growing concerns over animal welfare standards have further encouraged the deployment of continuous surveillance solutions across intensive farming systems.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to witness rapid expansion during the forecast period as farmers actively modernize traditional livestock practices through connected farm infrastructure. Countries such as India, China, and Australia continue to promote smart animal husbandry initiatives that encourage the use of wearable sensors and automated disease alert systems.

The Food and Agriculture Organization stated in 2023 that Asia produces nearly 40% of the global livestock output, which increases the urgency for productivity enhancing digital tools across high density farming zones. Regional governments now support pilot programs that link herd tracking data with mobile based advisory platforms.

Growing protein demand in urban markets drives farm owners to improve reproductive efficiency and reduce mortality rates. Technology providers also collaborate with dairy cooperatives to introduce affordable animal health monitoring kits.

Expanding rural internet access enables real time farm supervision even in remote grazing areas. These structural changes continue to strengthen the role of intelligent livestock analytics across emerging agricultural economies.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the livestock monitoring market focus on expanding their connected device ecosystems through sensor innovation, cloud based analytics, and AI driven herd management platforms that support real time health and productivity tracking. They form strategic alliances with dairy cooperatives and precision agriculture firms to improve on farm deployment efficiency and integrate data across feeding, breeding, and disease detection workflows.

Companies also invest in mobile enabled dashboards that allow farm operators to monitor cattle behavior, reproductive cycles, and environmental conditions through a unified interface. For instance, DeLaval, a Sweden based agricultural technology provider established in 1883, strengthens its market position through smart milking systems and wearable animal health sensors designed to improve dairy herd performance.

The company operates in more than 100 countries and continues to expand its digital farming portfolio by combining automation tools with predictive analytics capabilities. Through ongoing investments in farm digitization platforms and localized service networks, DeLaval enhances customer retention and supports data led decision making across modern livestock operations.

Top Key Players

- DeLaval

- Affimilk Ltd.

- BouMatic

- Merck & Co., Inc. (Allflex)

- Zoetis

- Lely

- Moocall

- GEA Group Aktiengesellschaft

- Fullwood JOZ

- Dairymaster

- Fancom BV

- Nysbys

- PsiBorg Technologies Pvt. Ltd

Recent Developments

- In June 2025, Globalstar expanded its collaboration with CERES TAG to enhance satellite-based livestock monitoring capabilities in response to New World Screwworm risks. The partnership supports continuous connectivity, real-time animal tracking, and improved biosecurity oversight for herds located in remote grazing environments.

- In May 2025, CERES TAG introduced the CERES RANCHER device in the US, a next-generation livestock monitoring solution designed to provide real-time herd intelligence. The upgraded system offers improved durability and data accuracy, supporting producers, veterinarians, and research institutions in managing cattle health and movement more effectively.

Report Scope

Report Features Description Market Value (2025) US$ 6.9 Billion Forecast Revenue (2035) US$ 40.6 Billion CAGR (2026-2035) 19.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Components (Hardware (GPS Trackers, Health Monitoring Tags, Rumination and Feeding Monitors, Biometric Sensors and Others), Software and Services), By Animal Type (Cattle (Bovine), Swine (Pigs), Poultry (Chickens/Broilers), Equine (Horses) and Others), By Application (Health and Disease Detection, Location and Tracking, Reproductive Management, Behavioral Analysis, Environmental Monitoring, Automated Feeding and Others), By End User (Dairy Farms, Beef Farms & Feedlots, Poultry Farms, Swine Farms and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape DeLaval, Affimilk Ltd., BouMatic, Merck & Co., Inc. (Allflex), Zoetis, Lely, Moocall, GEA Group Aktiengesellschaft, Fullwood JOZ, Dairymaster, Fancom BV, Nysbys, PsiBorg Technologies. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Livestock Monitoring MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Livestock Monitoring MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- DeLaval

- Affimilk Ltd.

- BouMatic

- Merck & Co., Inc. (Allflex)

- Zoetis

- Lely

- Moocall

- GEA Group Aktiengesellschaft

- Fullwood JOZ

- Dairymaster

- Fancom BV

- Nysbys

- PsiBorg Technologies Pvt. Ltd

Our Clients

- 180301

- March 2026