Quick Navigation

Report Overview

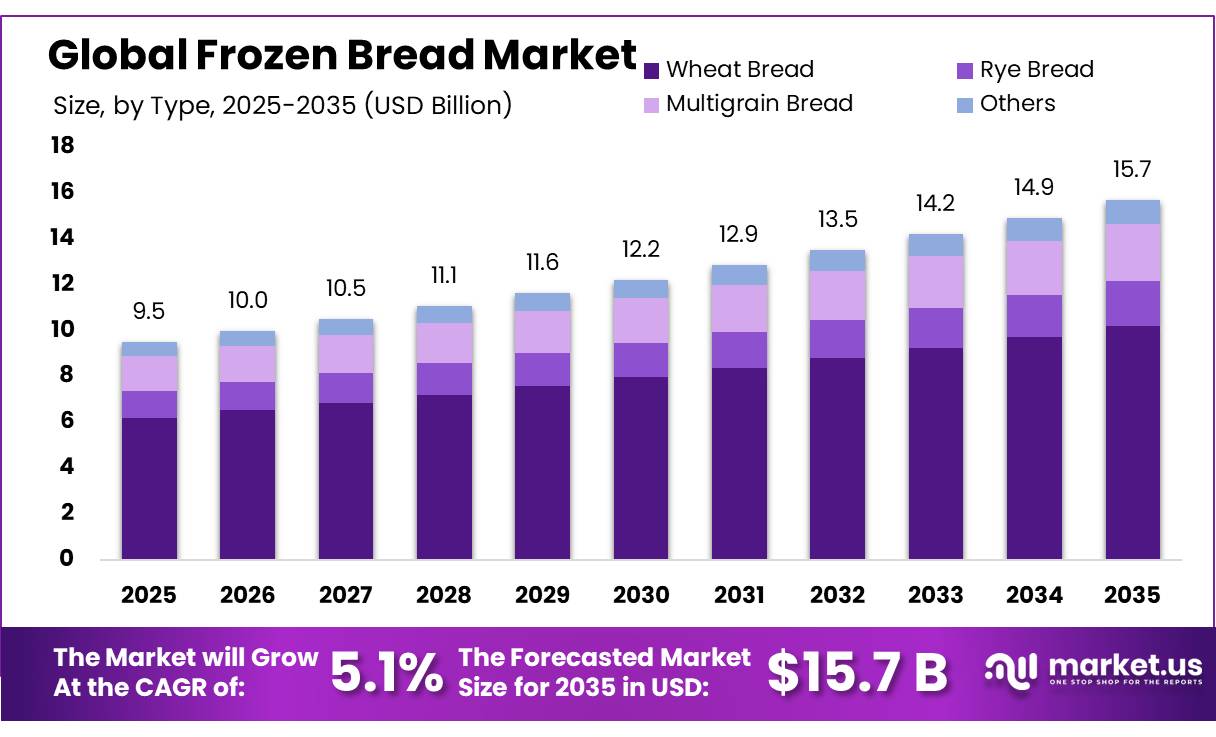

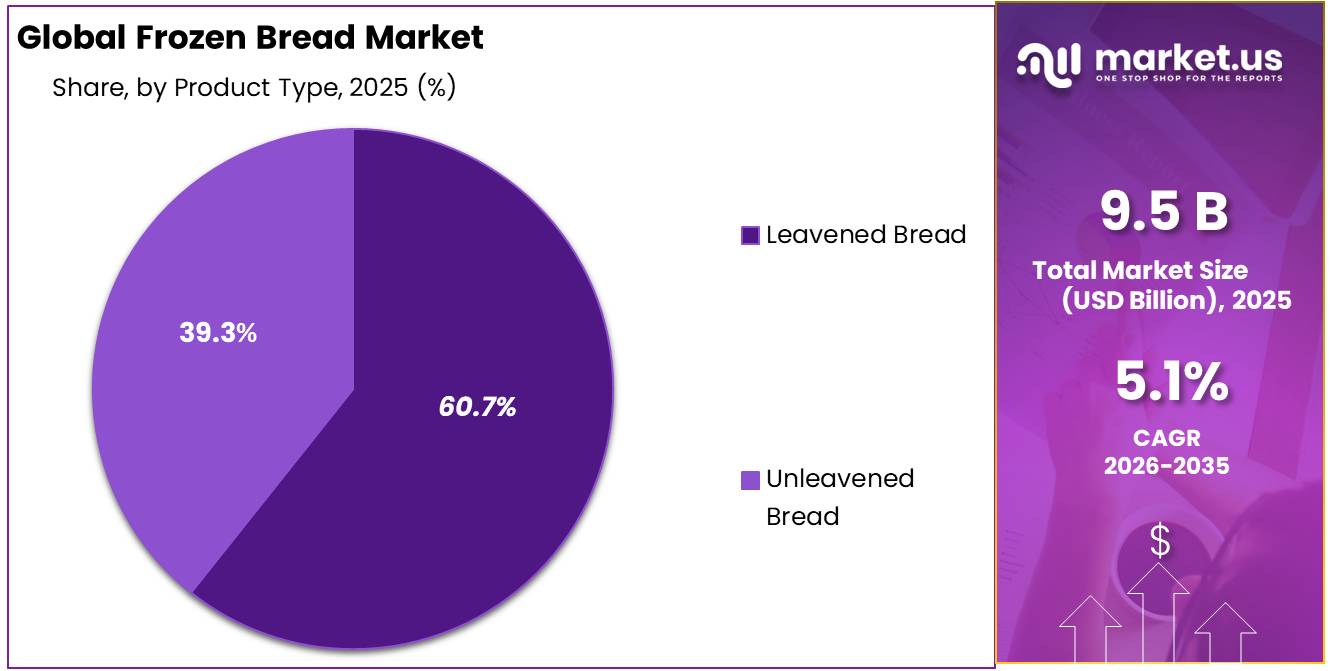

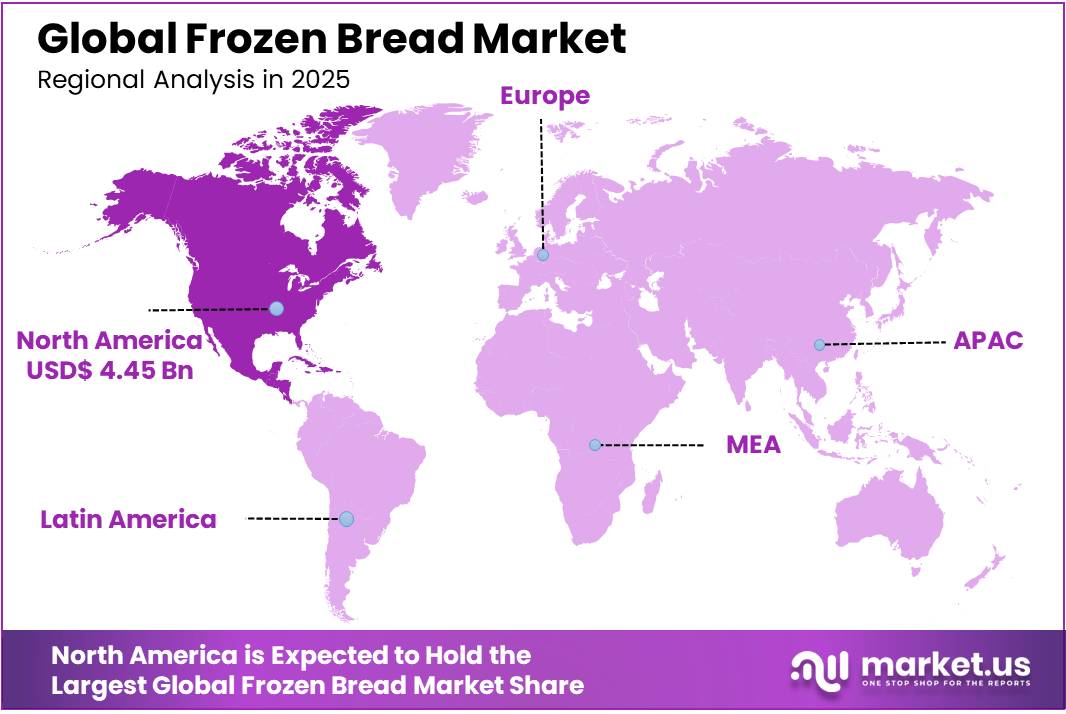

In 2025, the Global Frozen Bread Market was valued at US$9.5 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 5.1%, reaching about US$15.7 billion by 2035. North America held a dominant market position, capturing more than a 46.9% share, holding USD 4.46 billion in revenue.

The frozen bread plays a pivotal role within the frozen baked foods industry supply chain. The product helps make the consumption process simpler as well as extends the lifespan of the goods, but not at the cost of deteriorating their quality. The increase in the number of frozen bread products’ consumers can be accounted to the expansion of the foodservice sector, the development of the convenience store sector, and a rise in the number of consumers having an active lifestyle.

- In 2024, the number of bread consumers in the United States is projected to reach approximately 335.49 million people, increasing from nearly 326.91 million consumers recorded in 2020, according to estimates derived from the U.S. Census Bureau and the NHCS Simmons National Consumer Survey.

- Both production and consumption are largely concentrated in North America emerging as the dominant regional market holding 46.9% share in 2025. Such dominance is bolstered by strong cold chain infrastructure and B2B procurement channels for bulk distribution and consolidation within the cold chain framework.

Key Takeaways

- The Global frozen bread market was valued at USD 9.5 billion in 2025.

- The Global market is projected to grow at a CAGR of 5.1% and is estimated to reach USD 15.7 billion by 2035.

- On the basis of type, wheat bread dominated the market, constituting 65.1% of the total market share.

- Based on product type, leavened bread dominated the frozen bread market, with a substantial market share of around 57.3%.

- Among the distribution channels, B2B held a major share in the frozen bread market, accounting for 60.7% of the total market share.

- Among the end-users, the foodservice sector dominated the frozen bread market, accounting for around 65.5% of the market share.

- In 2025, North America was the most dominant region in the frozen bread market, accounting for 46.9% of the total market and reaching US$4.46 billion.

Product innovation efforts have focused on organic ingredients, gluten-free products, clean-labeling and freezing technologies to accommodate the demand for higher quality and convenience among health-conscious consumers and premium foodservice customers. Supply chain localization has become another tool to enhance competitiveness, yet the industry is facing several structural limitations such as high energy intensity involved in frozen storage and volatile inputs related to geopolitical instability in global wheat and energy trade flows.

Frozen Bread Market Segmentation

Type Analysis

Wheat Bread dominates with 65.1% due to its familiar taste and broad daily use

In 2025, Wheat Bread held a dominant market position, capturing more than a 65.1% share of the frozen bread market. As of December 2025, the segment recorded strong demand from households, restaurants, cafés, hotels, bakeries, and institutional kitchens. Its soft texture, familiar taste, and suitability for sandwiches, toast, and everyday meals supported its leadership. Wheat bread also maintains consistent quality during freezing, transportation, storage, and reheating. Its wide availability and suitability for large-scale production further strengthened its position.

Multigrain Bread emerged as a growing segment in 2025. Consumer interest increased due to its mixed-grain composition, distinctive texture, and suitability for premium meals. Its rising use in cafés, restaurants, and household breakfast options supported wider adoption.

Product Type Analysis

Leavened Bread leads with 57.3% due to its soft texture and wide application range

In 2025, Leavened Bread held a dominant market position, capturing more than a 57.3% share of the frozen bread market. As of December 2025, the segment remained widely preferred across households, bakeries, restaurants, cafés, hotels, and catering businesses. Its light structure, soft texture, and familiar taste made it suitable for sandwiches, breakfast meals, snacks, and side dishes. Leavened bread also retains its quality during freezing, storage, transportation, and reheating. Its convenience and suitability for large-scale production strengthened its leading position.

Unleavened Bread showed steady growth in 2025. Its simple preparation, compact form, and suitability for wraps, flatbreads, and traditional dishes supported demand across households and commercial kitchens.

Distribution Channel Analysis

B2B dominates with 60.7% due to strong bulk demand from commercial buyers

In 2025, B2B held a dominant market position, capturing more than a 60.7% share of the frozen bread market. As of December 2025, the channel benefited from bulk purchases by restaurants, hotels, cafés, bakeries, catering companies, and institutional kitchens. Frozen bread helps commercial buyers reduce preparation time, control waste, and maintain consistent quality across locations. B2B arrangements also support predictable procurement, larger order volumes, and dependable product availability. These operational benefits strengthened the channel’s leadership.

B2C continued to grow in 2025 as households increasingly preferred convenient bread products with longer storage periods. Wider availability through supermarkets, convenience stores, specialty outlets, and online platforms supported its expansion.

End-User Analysis

Foodservice dominates with 65.5% due to high-volume demand from commercial kitchens

In 2025, Foodservice held a dominant market position, capturing more than a 65.5% share of the frozen bread market. As of December 2025, the segment benefited from strong demand across restaurants, hotels, cafés, bakeries, catering businesses, and institutional kitchens. Frozen bread helps these operators reduce preparation time, lower food waste, and maintain consistent taste and quality during busy service hours. Its longer storage life and easy portion control also support efficient inventory management. Regular bulk purchases and the need for quick meal preparation further strengthened the position of foodservice users in the market.

Residential emerged as a growing segment in 2025. Household demand increased as consumers looked for convenient bread products that could be stored for longer periods and prepared when required. Easy availability through retail stores and online channels supported wider residential use.

Key Market Segments

By Type

- Wheat Bread

- Rye Bread

- Multigrain Bread

- Others

By Product Type

- Leavened Bread

- Unleavened Bread

By Distribution Channel

- B2B

- B2C

- Supermakets and Hypermarkets

- Convenience Store

- Speciality stores

- Online

By End-User

- Residential

- Foodservice

Drivers

Labor substitution via bake-off and par-baked operating models

Frozen bread, par-baked loaves, and ready-to-proof bakery systems let retailers and foodservice operators replace skilled bench work with lower-skill finishing steps, reducing labor intensity per store and improving output consistency. This is especially relevant in Europe because hourly labour costs in 2025 averaged €34.9 across the EU and €38.2 in the euro area, up 4.1% and 3.8% respectively from 2024, while euro area labour costs were still rising 3.3% year over year in Q3 2025.

The operating gain is fewer night-shift bakers, tighter production yields, and lower in-store training burden, which is why the strongest uptake is visible in supermarket in-store bakeries, convenience chains, hotels, and café chains rather than only in traditional bread aisles. This driver contributes about 1.1 percentage points to CAGR because wage inflation is persistent, and every 100 basis points of labor-cost escalation strengthens the ROI case for frozen formats that compress store-level touch time and reduce variability.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience-led frozen bread adoption in modern retail and e-grocery | +1.4% | North America core, Western Europe core, urban APAC | Short term (≤ 2 years) |

| Labor substitution via bake-off and par-baked operating models | +1.1% | EU core, UK, North America, GCC hospitality hubs | Short term (≤ 2 years) |

| Cold-chain network expansion and freezer-door availability | +0.9% | North America, EU, China, Southeast Asia tier-1 cities | Medium term (2-4 years) |

| Centralized production hedge against ingredient and energy volatility | +0.8% | US, Canada, EU milling corridors, Latin America spill-over | Short term (≤ 2 years) |

| Premiumization through artisan formats, clean-label, and foodservice quality replication | +0.7% | Western Europe, North America, Japan, South Korea | Medium term (2-4 years) |

| EU traceability and sustainability compliance reshaping formulations and sourcing | +0.5% | EU core, UK supply-linked exporters, Turkey/North Africa suppliers | Medium term (2-4 years) |

Restraints

Freight and route instability

Although container rates into Europe eased from late-2025 peaks and some Red Sea services began a controlled return in early 2026, shipping conditions are still not fully normalized, which matters for frozen bread because the category depends on reliable transit for imported specialty fats, enzymes, improvers, packaging films, and in some regions finished frozen bakery products themselves.

Long-term rates on Far East to Mediterranean lanes were down 25% to around USD 2,308 per FEU and down 10% to around USD 2,010 into North Europe in January 2026, but those lower nominal rates do not eliminate the strategic issue of schedule instability, buffer-stock requirements, reefer slot risk, and inventory carrying cost when transit windows stretch by even 7 to 14 days.

For import-reliant processors, that can add 40 to 90 basis points to landed cost and force 10 to 20 days of additional safety stock, tying up working capital, increasing write-off risk for packaging and ingredients, and discouraging aggressive geographic expansion, which supports a 0.6 percentage-point near-term CAGR drag.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wheat & fats volatility | -1.1% | North America core, EU, APAC importers, MENA | Short term (≤ 2 years) |

| Cold-chain energy burden | -0.9% | EU, UK, North America, India metros, GCC | Medium term (2-4 years) |

| Retail pass-through limits | -0.8% | EU grocery, North America retail, APAC urban chains | Short term (≤ 2 years) |

| Freight & route instability | -0.6% | EU-APAC corridors, MENA, import-reliant islands | Short term (≤ 2 years) |

| Compliance & traceability drag | -0.5% | US, EU, India, export-oriented APAC | Medium term (2-4 years) |

| Labor scarcity / automation hurdle | -0.7% | North America, Western Europe, developed APAC | Long term (≥ 4 years) |

Opportunities

Emerging-market cold-chain co-development

Many emerging markets still have frozen bakery penetration below 10–15% of total bread consumption, yet cold-chain logistics in regions like India and broader APAC are growing at double‑digit CAGRs (20–25% in some corridors) for perishable food segments. If frozen bread specialists partner with logistics firms and retailers to co‑invest in regional hubs, shared freezers at modern trade outlets, and targeted category-education campaigns, they could position frozen bread to own 20–30% of incremental bread growth in these markets by 2035, translating into USD 8–12 billion in additional TAM capture above baseline forecasts.

This would require committing 2–3% of annual revenue into co‑funded infrastructure and route design for at least 5–7 years, but would unlock line-haul efficiencies, early category leadership, and retailer stickiness that lower future customer acquisition costs by 25–40% compared with late entrants. As these initiatives are not yet mainstream outside a few GCC and China corridors, successfully executing them could add around 2.5 percentage points of CAGR upside for the global frozen bread market between 2026 and 2035, with most upside accruing in APAC emerging markets, Gulf states and select African urban centres.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Health-forward frozen bread platforms | +2.2% | EU, North America, APAC urban | Medium term (2-4 years) |

| Foodservice bake-off and QSR integration | +2.0% | Global QSR hubs, GCC, APAC | Short term (≤ 2 years) |

| Direct-to-consumer frozen subscription models | +1.8% | North America core, EU, East Asia | Medium term (2-4 years) |

| Emerging-market cold-chain co-development | +2.5% | APAC emerging, Africa, GCC | Long term (≥ 4 years) |

| M&A roll-up of regional frozen bakeries | +1.6% | Europe, North America, GCC | Medium term (2-4 years) |

| Digital demand-sensing and waste-optimized assortments | +1.4% | Global modern retail, e-commerce | Short term (≤ 2 years) |

Challenge

Structural bakery labour gaps

U.S. baking industry projections cited in 2025 pointed to 53,500 unfilled positions by 2030 across production, engineering and equipment maintenance, implying that frozen bread lines may routinely run one shift fewer per week or operate at 85–90% effective capacity even when order books support full utilization, with downstream macro‑effects such as potential losses of 148,000 jobs and USD 36.2 billion in output across wider baking ecosystems if no remediation occurs.

For frozen bread plants that require continuous mixing, proofing, par-bake and blast-freeze operations, every 5% shortfall in line staffing can add 3–4 hours of weekly downtime for changeovers and sanitation, reduce planned throughput by 8–12%, and increase overtime wage burdens by 10–15%, degrading unit productivity and squeezing margins by 50–70 basis points.

Strategically, leading manufacturers are responding by re‑engineering lines around high‑throughput spiral freezers, automated pan-handling, and remote diagnostics to cut manual touchpoints per loaf by 30–40%, while forming multi‑employer training consortia to push annual apprentice intakes up 25–30% and offering retention bonuses equivalent to 3–5% of annual pay in critical roles; however, because these programmes operate on 4–6 year skills maturation cycles, the underlying labour friction is expected to shave about 1.2 percentage points from achievable CAGR over the remainder of the decade, even as sales volumes continue to grow.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Volatile cold-chain energy costs | -1.4% | Europe core, North America | Medium term (2-4 years) |

| Structural bakery labour gaps | -1.2% | North America, EU industrial belts | Long term (≥ 4 years) |

| Ingredient cost and tariff volatility | -1.0% | North America, EU trade hubs | Medium term (2-4 years) |

| Fresh vs frozen consumer preference gap | -0.9% | Europe, Latin America urban | Long term (≥ 4 years) |

| Fragmented food-safety compliance in frozen | -0.8% | Global multicountry operators | Medium term (2-4 years) |

| Cold-chain capacity and routing constraints | -1.1% | APAC corridors, GCC, Africa | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Rising Crop Prices Impact Frozen Bread Sector During Geopolitical Strains.

The present geopolitical problems, which involve the ongoing Russia-Ukraine war, have had tangible effects on the world’s food production that have, in turn, had implications for the input materials used to manufacture frozen bread. For example, Ukraine was a major participant in the international trade of cereals since, every year, 9% of wheat produced in the country were traded internationally. In addition, Ukraine played a big role in the maize and barley trade.

- According to FAO, there was an increase of more than 40% in the price of wheat across the world at the beginning of the conflict. This has, to some extent, impacted the availability of inputs that are used to produce frozen bread.

In addition, the issues surrounding maritime security, such as disruptions in the Red Sea and Suez Canal, have led to increased time taken to deliver cargo as well as higher costs due to the need for re-routing of ships. According to the International Chamber of Shipping, re-routing via an African route causes the European and Asian shipping process to take an additional 10-14 days. Fuel costs and refrigeration costs have also gone up.

The above examples illustrate how instability can affect international trade by directly affecting the availability of raw materials, their prices, and logistics involved in frozen products, including frozen breads.

Regional Analysis

North America Accounted for the Largest Portion of the Global Frozen Bread Market.

North America has become the leading market in the frozen bread segment, accounting for about 46.9% of global market share in 2024 due to widespread household refrigeration availability and efficient retail facilities in the United States and Canada. North America is the main global market for frozen breads since it is characterized by a preference for convenience foods among consumers.

According to recent industry estimates from the American Frozen Food Institute (AFFI), a significant share of U.S. households continued to expand frozen food storage capacity through 2023 and 2024 due to rising consumer preference for bulk food purchases, convenience-oriented consumption patterns, and longer frozen food storage requirements. The trend has positively supported demand for frozen bakery products, including frozen bread, across retail and household applications.

Data obtained from the household survey conducted by the U.S. Census Bureau indicates that more than 99% of households in the United States have refrigeration devices with freezing capabilities, which provides infrastructure for the adoption of frozen foods, including frozen bread varieties. The Food Marketing Institute reports that the typical number of frozen foods carried by U.S. super markets is 3,000 with frozen bakery products being included as an emerging segment.

Key Regions and Countries Covered

North America

- The US

- Canada

Europe

- Germany

- France

- The Uk

- Spain

- Italy

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Producers of frozen bread adopt an integrated strategy that involves product development, operational excellence, and distribution improvement in order to strengthen their market position. There is an organized diversification of products using organic, whole grain, high fiber, and gluten-free products, as well as specialty products like ready-to-bake and par-baked products designed specifically for different markets.

The efforts towards operational excellence include utilizing advanced automation, energy-saving freezing equipment such as IQF and blast freezers, and cold chain management systems to realize economies of scale without compromising on quality standards. The International Association of Refrigerated Warehouses indicates that automatic cold storages use up to 25% less energy than manual operations.

The methods to expand distribution channels include strategic alliances with fast-food restaurant chains, private label manufacturing with large retail chains, and improved freezer aisle positioning by implementing category management programs in collaboration with grocery retailers. According to Private Label Manufacturers Association, store brands account for about 25% of overall food and beverages sales, suggesting significant potential for private label frozen bakery products.

Market Key Players

- Europastry S.A.

- Vandemoortele NV

- Grupo Bimbo

- Lantmännen Unibake

- Flower Foods Inc.

- The Campbell’s Company

- Bridgford Foods Corporation

- Sunbulah Group

- Dawn Food Products Inc.

- Gonnella Baking Co.

- Custom Foods Inc.

- Cole’s Quality Foods, Inc.

- Panamar Bakery Group

- Gonnella Baking Company

- Monbake

- Other Key Players

Key Development

- In May 2025, Vandemoortele announced its collaboration with VIVESCIA Group for the acquisition of Délifrance to strengthen its position within the European frozen bakery market. The acquisition is expected to enhance Vandemoortele’s frozen bread production capabilities, expand its premium bakery portfolio, and improve access to integrated grain supply operations across Europe.

- In July 2025, Europastry acquired Art of Baking from Minor International Public Company Limited and Srifa Frozen Food to expand its presence within the Southeast Asian frozen bakery market. The acquisition is aimed at strengthening Europastry’s regional manufacturing and distribution capabilities while accelerating growth opportunities across the premium frozen bread segment in Asia-Pacific.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 9.5 Bn |

| Forecast Revenue (2035) | USD 15.6 Bn |

| CAGR (2025-2035) | 5.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2025-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Wheat Bread, Rye Bread, Multigrain Bread, and Others), By Product Type (Leavened Bread and Unleavened Bread), By End-Use (Household and Foodservice), By Distribution Channel (B2B and B2C) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Europastry S.A., Vandemoortele NV, Grupo Bimbo, Lantmännen Unibake, Flower Foods Inc., The Campbell’s Company, Bridgford Foods Corporation, Sunbulah Group, Dawn Food Products Inc., Gonnella Baking Co., Custom Foods Inc., Cole’s Quality Foods, Inc., Panamar Bakery Group, Gonnella Baking Company, Monbake, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |