Quick Navigation

Report Overview

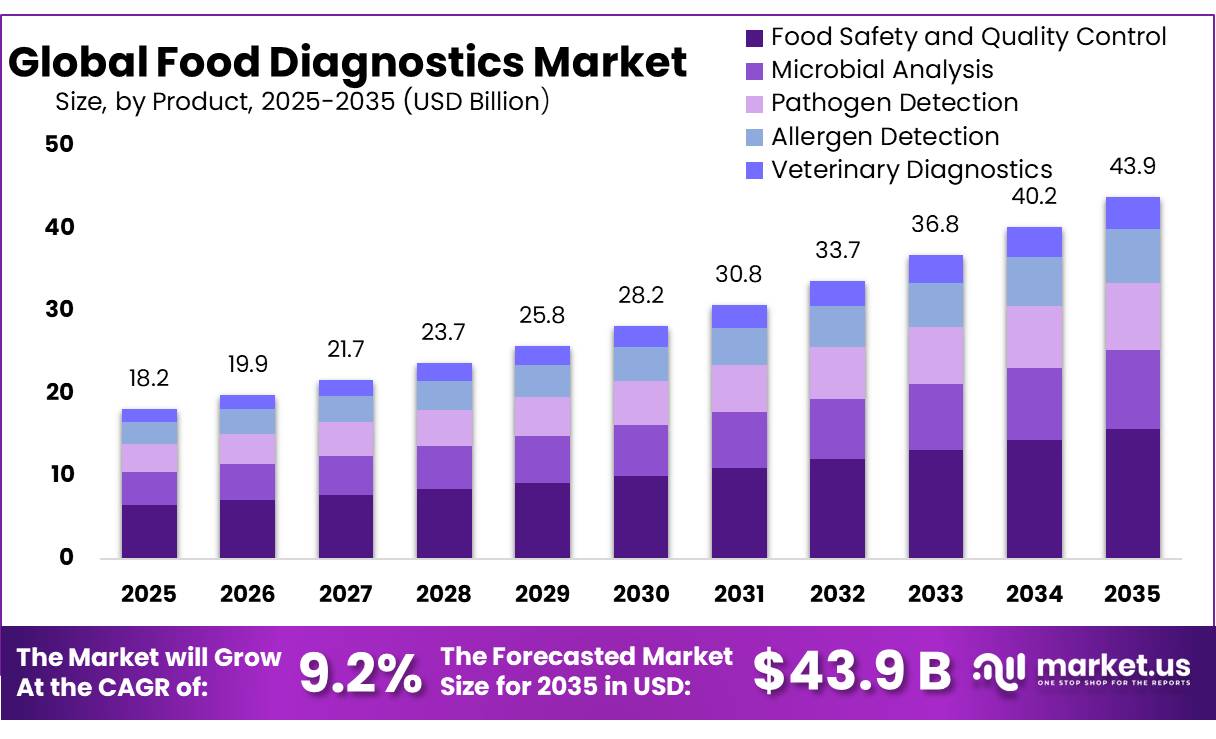

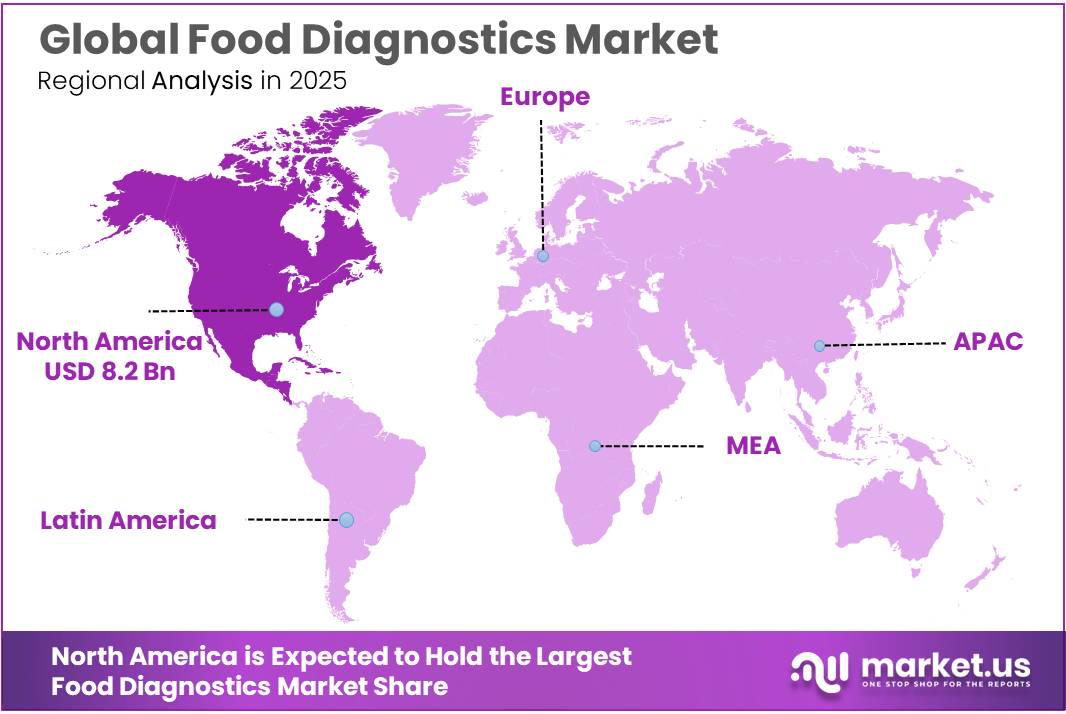

The Global Food Diagnostics Market size is expected to be worth around USD 43.9 Billion by 2035, from USD 18.2 Billion in 2025, growing at a CAGR of 9.2% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 45.2% share, holding USD 8.2 Billion revenue.

Food diagnostics refers to laboratory and rapid testing systems used to detect pathogens, allergens, toxins, pesticide residues, heavy metals, adulterants, and other unsafe materials in food. The industry is becoming more important because food supply chains are longer, processed food consumption is rising, and regulators are demanding stronger proof of safety before products reach consumers. In 2026, WHO estimated that unsafe food causes 866 million illnesses, 1.52 million deaths, and around US$310 billion in productivity and medical losses every year, showing why diagnostics has become a core part of food quality control.

Key Takeaways

- Food Diagnostics Market size is expected to be worth around USD 43.9 Billion by 2035, from USD 18.2 Billion in 2025, growing at a CAGR of 9.2%.

- Food Safety and Quality Control held a dominant market position, capturing more than a 35.2% share in the Food Diagnostics Market.

- Meat, Poultry, and Seafood held a dominant market position, capturing more than a 32.30% share in the Food Diagnostics Market.

- Molecular Diagnostics held a dominant market position, capturing more than a 54.10% share in the Food Diagnostics Market.

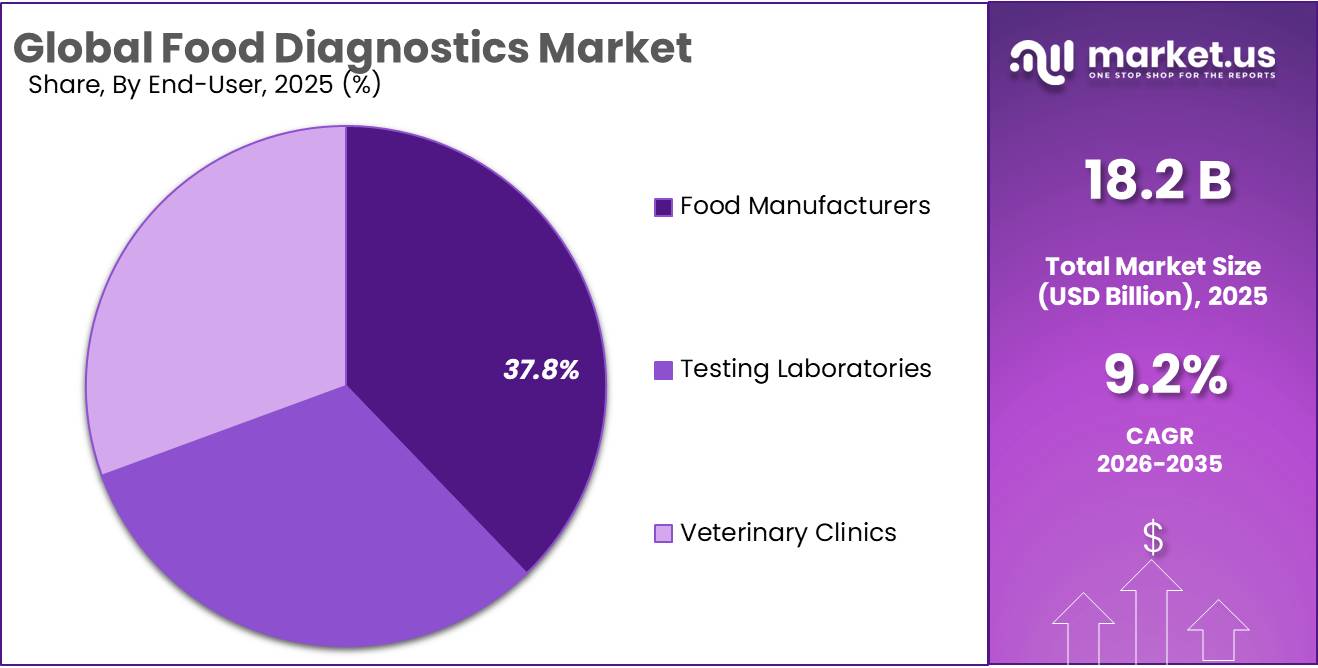

- Food Manufacturers held a dominant market position, capturing more than a 37.80% share in the Food Diagnostics Market.

- North America held a dominant position in the Food Diagnostics market, capturing more than 45.20% of the global market share, representing an estimated market value of approximately USD 8.2 billion.

This creates steady demand for testing across meat, poultry, dairy, seafood, processed food, beverages, grains, fruits, and environmental samples. In the U.S., CDC has historically estimated 48 million foodborne illnesses, 128,000 hospitalizations, and 3,000 deaths each year, showing why food manufacturers continue investing in diagnostics.

Growth is mainly driven by stricter food safety rules, higher packaged-food trade, recall prevention, and retailer pressure for clean supply chains. FDA requested US$7.2 billion for FY2025 to strengthen food safety, nutrition, medical product safety, supply-chain resilience, and infrastructure. In Europe, the RASFF system provides 24/7 rapid exchange of food and feed risk alerts, supporting continuous testing and product recall activity.

Regulation is a major growth driver. The U.S. FDA Food Traceability Rule was originally set with a January 20, 2026 compliance date, pushing food businesses to strengthen lot-level tracking, recordkeeping, and testing discipline. Globally, Codex Alimentarius also supports food trade by providing science-based food safety and quality standards across 188 members. These policies are encouraging food companies to use validated diagnostic tools that can support audits, recalls, export documentation, and risk-based quality programs.

Technology adoption is also improving the market outlook. Thermo Fisher Scientific supports food diagnostics through PCR-based pathogen testing, microbiology media, sample preparation, chromatography, and analytical workflow solutions. Its food safety PCR assays cover major pathogens such as Salmonella, Listeria, E. coli O157, and Cronobacter, helping laboratories shorten release time and improve contamination response. Thermo Fisher reported full-year 2025 revenue of US$44.56 billion, giving it strong scale to serve food, clinical, pharmaceutical, and environmental laboratories.

Agilent Technologies remains important in food diagnostics through LC/MS, GC/MS, sample preparation, spectroscopy, and analytical software used for pesticide residues, contaminants, authenticity, and quality testing. In fiscal 2025, Agilent reported US$6.95 billion revenue, 6.7% reported growth, and 4.9% core growth. Its installed base across laboratories supports wider adoption of high-sensitivity food testing workflows, especially where exporters and regulators require low-level detection of residues, toxins, and chemical contaminants.

By Product Analysis

Food Safety and Quality Control dominates with 35.2% driven by stricter compliance and rising demand for reliable food quality assurance

In 2025, Food Safety and Quality Control held a dominant market position, capturing more than a 35.2% share in the Food Diagnostics Market. The segment maintained leadership as food manufacturers, processors, and regulatory authorities increased focus on preventing contamination, maintaining product consistency, and meeting evolving food safety requirements across global supply chains. Growing consumer attention toward food transparency and product integrity also supported broader adoption of diagnostic solutions across production environments.

By Sample Analysis

Meat, Poultry, and Seafood dominates with 32.30% as food safety monitoring becomes more critical across protein supply chains

In 2025, Meat, Poultry, and Seafood held a dominant market position, capturing more than a 32.30% share in the Food Diagnostics Market. The segment led the market due to the high sensitivity of animal-based food products to contamination, spoilage, and microbial growth during processing, transportation, and storage. Producers across these categories continued strengthening diagnostic practices to maintain food quality, comply with safety requirements, and reduce the risk of product recalls.

By Technology Analysis

Molecular Diagnostics dominates with 54.10% as rapid and precise food testing gains industry preference

In 2025, Molecular Diagnostics held a dominant market position, capturing more than a 54.10% share in the Food Diagnostics Market. The segment maintained market leadership due to its ability to deliver faster, more sensitive, and highly accurate detection of contaminants, pathogens, and food quality indicators across diverse food categories. Food manufacturers increasingly adopted molecular diagnostic methods to improve testing reliability and reduce the time required for decision-making during production and distribution.

By End User Analysis

Food Manufacturers dominate with 37.80% as in-house testing and quality assurance become operational priorities

In 2025, Food Manufacturers held a dominant market position, capturing more than a 37.80% share in the Food Diagnostics Market. The segment maintained its leading position as food producers increasingly integrated diagnostic testing directly into manufacturing operations to strengthen product quality, maintain regulatory compliance, and improve production efficiency. Rising pressure to deliver safe and consistent food products encouraged manufacturers to expand routine testing across multiple stages of processing.

Key Market Segments

By Product

- Food Safety and Quality Contro

- Contaminant Testing

- Quality Assurance Testing

- Microbial Analysis

- Bacterial Detection

- Fungal Analysis

- Pathogen Detection

- Salmonella Detection

- Listeria Detection

- Allergen Detection

- Gluten Detection

- Peanut Allergen Testing

- Veterinary Diagnostics

- Animal Disease Testing

- Livestock Health Monitoring

By Sample

- Meat, Poultry, and Seafood

- Dairy Products

- Fruits and Vegetables

- Processed Foods

- Beverages

By Technology

- Molecular Diagnostics

- Biosensors

- Microscopy

- Immunoassays

By End User

- Food Manufacturers

- Packaged Food Producers

- Dairy Producers

- Testing Laboratories

- Private Labs

- Government Labs

- Veterinary Clinics

- Animal Hospitals

- Livestock Service Centers

Market Dynamics

Driver Analysis - Rising Global Food Safety Concerns Accelerate Diagnostics Adoption

One of the strongest driving factors supporting the growth of the Food Diagnostics Market is the increasing global focus on preventing food contamination and improving food safety across the supply chain. Food producers, processors, retailers, and regulatory agencies are expanding diagnostic testing practices to identify biological, chemical, and quality-related risks before products reach consumers. As food production becomes more industrialized and international trade volumes continue to expand, faster and more reliable food testing has become an operational necessity rather than an optional quality measure.

One of the strongest driving factors supporting the growth of the Food Diagnostics Market is the increasing global focus on preventing food contamination and improving food safety across the supply chain. Food producers, processors, retailers, and regulatory agencies are expanding diagnostic testing practices to identify biological, chemical, and quality-related risks before products reach consumers. As food production becomes more industrialized and international trade volumes continue to expand, faster and more reliable food testing has become an operational necessity rather than an optional quality measure.

Government and international initiatives are also supporting market expansion. The WHO Global Strategy for Food Safety 2022–2030 encourages countries to modernize food control systems, strengthen surveillance programs, and adopt science-based monitoring approaches across production and distribution networks. At the international level, food safety standards developed under global regulatory frameworks continue encouraging broader use of rapid diagnostics, molecular testing, and traceability solutions.

Restraint Analysis - High Testing Costs Limit Wider Food Diagnostics Adoption

One of the major restraining factors for the Food Diagnostics market is the high cost of advanced testing infrastructure and compliance requirements across the food supply chain. While food producers are under increasing pressure to improve food quality and safety, many small and medium-sized food manufacturers continue to face budget limitations when adopting molecular diagnostics, rapid pathogen testing, PCR systems, chromatography platforms, and automated laboratory solutions.

- According to the World Health Organization (WHO), around 866 million people globally fall ill every year due to contaminated food, while nearly 1.52 million deaths are linked to unsafe food consumption annually. WHO also estimates that the global economic burden from unsafe food reaches approximately US$310 billion each year through productivity losses and healthcare costs. Despite these large economic losses, building and operating diagnostic capacity remains expensive for food businesses and public agencies.

Governments and international bodies continue investing in stronger food control systems to reduce this gap. The FAO and WHO support countries through food surveillance frameworks, laboratory strengthening programs, risk-based inspection systems, and international food standards under Codex initiatives. These programs aim to improve access to reliable diagnostics and reduce long-term food safety costs.

Opportunity Analysis - Expanding Government Food Safety Programs Create Diagnostic Opportunities

One of the strongest growth opportunities for the Food Diagnostics market is the rapid expansion of government-led food safety infrastructure and stronger global monitoring systems. As food supply chains become longer and more international, governments and food organizations are increasing investments in testing laboratories, contaminant detection, pathogen screening, and digital traceability systems. This shift is creating sustained demand for advanced food diagnostics technologies across manufacturers, exporters, processors, and regulatory agencies.

The scale of the opportunity is supported by global food safety data. According to the World Health Organization (WHO), food safety has become a strategic public health priority under its Global Strategy for Food Safety 2022–2030, with countries being encouraged to strengthen national food control systems, emergency response capabilities, and laboratory networks. WHO and FAO continue supporting international food standards through Codex Alimentarius to improve food monitoring and compliance across regions.

Government programs are also moving from policy to infrastructure investment. In 2025, the Government of India’s Ministry of Food Processing Industries introduced updated guidelines under the Food Safety and Quality Assurance Infrastructure (FSQAI) scheme to support the establishment of NABL-accredited food testing laboratories. Such initiatives directly expand opportunities for diagnostic equipment suppliers, molecular testing providers, rapid detection platforms, and analytical service companies.

Emerging Trend Analysis - Rapid Molecular Testing and Digital Traceability Reshape Food Diagnostics

One of the strongest latest trends in the Food Diagnostics industry is the shift toward rapid molecular testing combined with digital food traceability systems. Food manufacturers, processors, and regulators are moving away from traditional laboratory-only testing and adopting faster diagnostic tools that can identify pathogens, contaminants, allergens, and quality issues in much shorter timeframes. This change is being driven by rising food safety concerns, stricter compliance requirements, and the need to monitor increasingly complex global food supply chains.

Government and international initiatives are accelerating this trend. The WHO Global Strategy for Food Safety 2022–2030 promotes stronger surveillance systems, integration of Whole Genome Sequencing (WGS) for foodborne disease monitoring, and risk-based food control frameworks. At the same time, the Food and Agriculture Organization (FAO) is advancing food safety foresight programs that encourage countries to adopt predictive diagnostics and modern testing infrastructure to prepare for future food risks.

A major technology shift is the growing use of PCR-based testing, genomic sequencing, and AI-supported diagnostic platforms for food safety verification. These technologies allow laboratories and food producers to detect contamination earlier, reduce sample processing time, and improve decision-making across production lines. Rapid diagnostics are also becoming more important as international food trade expands and consumers expect greater transparency regarding food origin and safety.

Regional Insights

North America Dominates Food Diagnostics Market with 45.20% Share

In 2025, North America held a dominant position in the Food Diagnostics market, capturing more than 45.20% of the global market share, representing an estimated market value of approximately USD 8.2 billion. The region maintained leadership due to its advanced food safety infrastructure, strong regulatory oversight, high testing adoption across food processing facilities, and continuous investment in diagnostic technologies.

The United States remained the largest contributor within North America, supported by a highly developed food manufacturing sector and extensive laboratory testing networks. According to data from the U.S. Department of Agriculture (USDA), food and beverage manufacturing shipments exceeded USD 1 trillion annually, creating a large addressable base for routine food quality and safety diagnostics. In parallel, government agencies continued investments in modernized food surveillance and preventive food safety programs.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, Thermo Fisher reported USD 44.56 billion in total revenue, reflecting 4% annual growth. Its Specialty Diagnostics business continued supporting food and microbiology applications, while one microbiology-related business generated approximately USD 645 million revenue during 2025.

In fiscal 2025, Agilent recorded USD 6.95 billion in revenue, supported by increasing demand across diagnostics and laboratory applications. The company also employed approximately 18,000 people globally, strengthening its operational reach and laboratory support capabilities.

Top Key Players Outlook

- Thermo Fisher Scientific (US)

- Agilent Technologies (US)

- Bio-Rad Laboratories (US)

- Merck KGaA (DE)

- Danaher Corporation (US)

- Romer Labs (AT)

- Neogen Corporation (US)

- Intertek Group (GB)

- SGS SA (CH)

- PerkinElmer Inc.

Recent Developments

Danaher reported USD 24.6 billion revenue in 2025, with 3.0% year-over-year growth, and USD 5.3 billion free cash flow, giving it strong capacity for product development and expansion. In 2025, Danaher also announced a diagnostic development partnership with AstraZeneca to scale AI-powered diagnostics, while in 2026 it agreed to acquire Masimo for about USD 9.9 billion, strengthening its diagnostics segment further.

In 2025, Merck KGaA strengthened its Food Diagnostics work through its Life Science business, which supplies microbiology testing products, culture media, filtration tools, lab chemicals, and analytical solutions used for food safety and quality checks. The company reported €21,102 million net sales, €6,109 million EBITDA pre, and €3,932 million operating cash flow in 2025, giving it a strong base for food testing innovation and laboratory expansion.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 18.2 Bn |

| Forecast Revenue (2035) | USD 43.9 Bn |

| CAGR (2026-2035) | 9.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Food Safety and Quality Contro, Microbial Analysis, Pathogen Detection, Allergen Detection, Veterinary Diagnostics, Animal Disease Testing, Livestock Health Monitoring), By Sample (Meat, Poultry, and Seafood, Dairy Products, Fruits and Vegetables, Processed Foods, Beverages), By Technology (Molecular Diagnostics, Biosensors, Microscopy, Immunoassays), By End User (Food Manufacturers, Testing Laboratories, Veterinary Clinics) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Thermo Fisher Scientific (US), Agilent Technologies (US), Bio-Rad Laboratories (US), Merck KGaA (DE), Danaher Corporation (US), Romer Labs (AT), Neogen Corporation (US), Intertek Group (GB), SGS SA (CH), PerkinElmer Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |