Quick Navigation

Report Overview

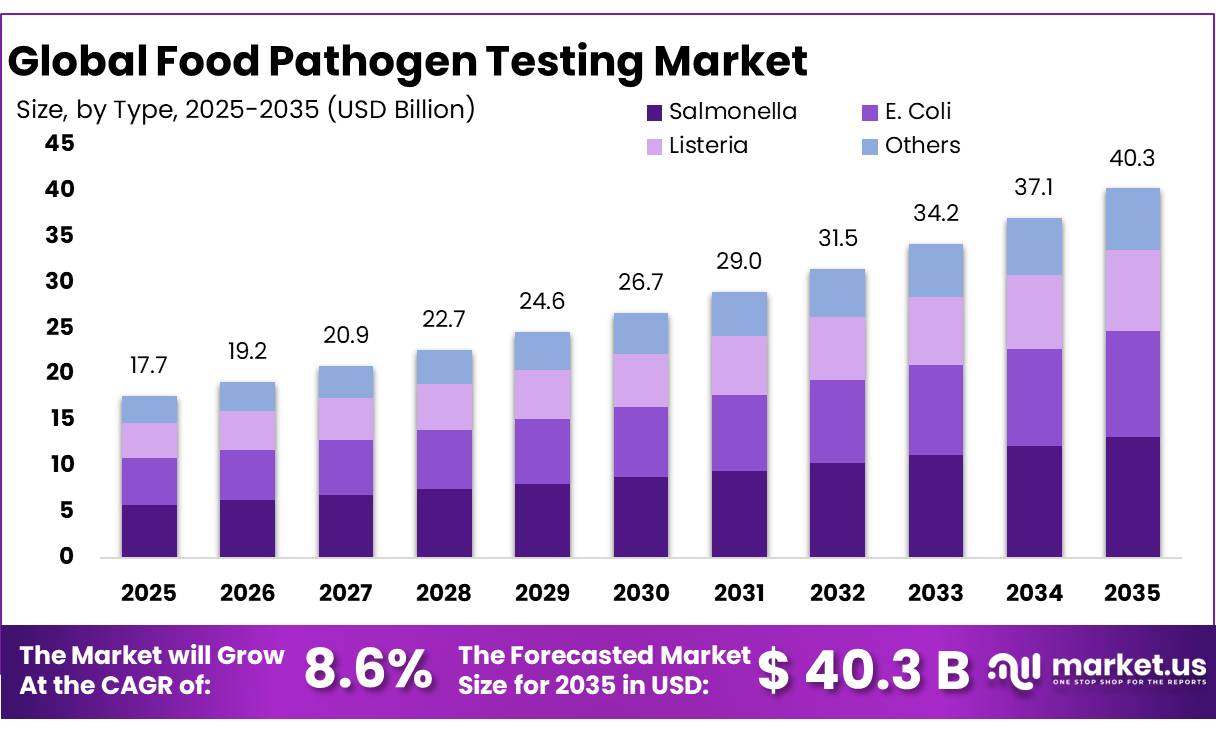

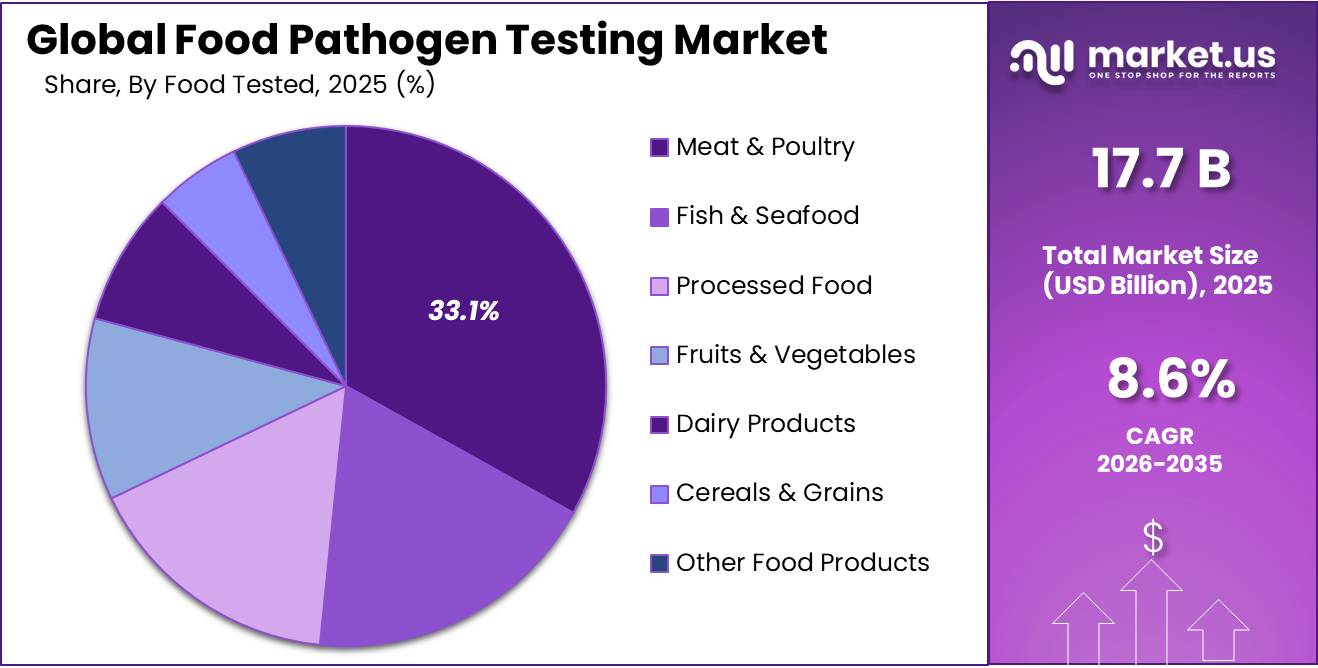

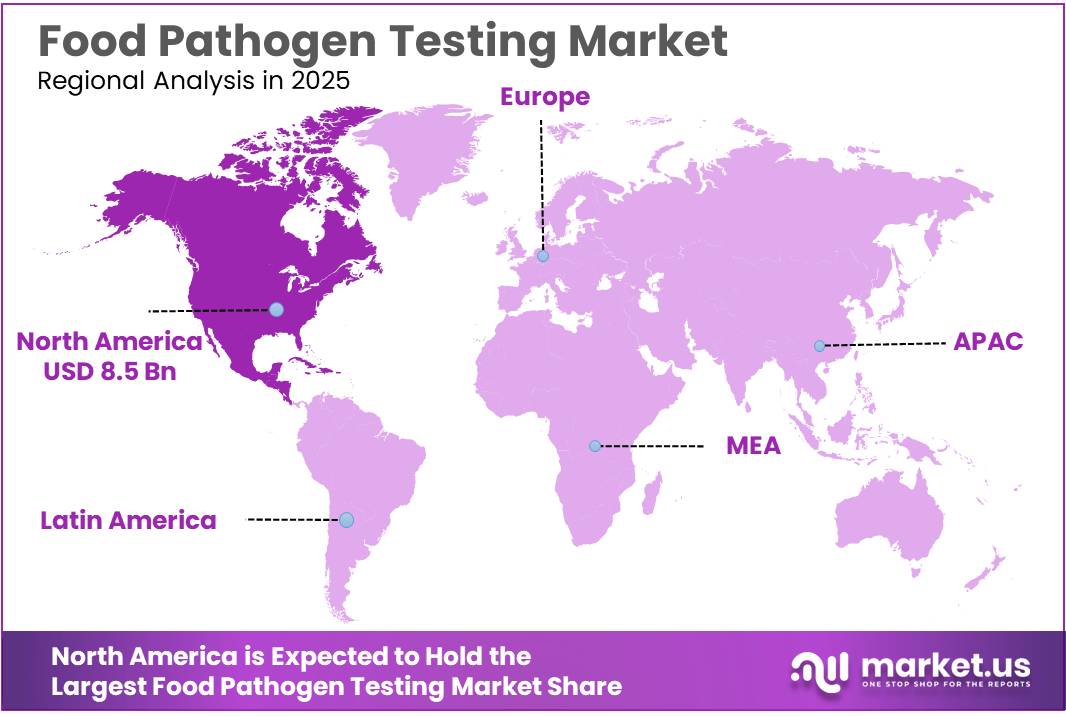

The Global Food Pathogen Testing Market size is expected to be worth around USD 40.3 Billion by 2035, from USD 17.7 Billion in 2025, growing at a CAGR of 8.6% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 48.1% share, holding USD 8.5 Billion revenue.

Food pathogen testing is becoming a core quality-control requirement across the global food chain, as contamination risks from Salmonella, Listeria, E. coli, Campylobacter, and other microbes remain a major public-health and trade concern. WHO states that unsafe food causes 866 million illnesses, 1.52 million deaths, and US$310 billion in annual productivity and medical-cost losses worldwide, creating strong demand for faster and more reliable pathogen detection.

Key Takeaways

- Food Pathogen Testing Market size is expected to be worth around USD 40.3 Billion by 2035, from USD 17.7 Billion in 2025, growing at a CAGR of 8.6%.

- Salmonella held a dominant market position, capturing more than a 32.80% share in the Food Pathogen Testing Market.

- Conventional held a dominant market position, capturing more than a 41.80% share in the Food Pathogen Testing Market.

- Meat & Poultry held a dominant market position, capturing more than a 33.10% share in the Food Pathogen Testing Market.

- North America held a dominant position in the Food Pathogen Testing Market, accounting for 48% of the global market and reaching approximately USD 8.5 Billion.

The industrial scenario is shaped by stricter food safety systems in North America and Europe. In the U.S., CDC estimates 48 million foodborne illness cases, 128,000 hospitalizations, and 3,000 deaths every year, which keeps pressure on food processors to strengthen routine testing and outbreak prevention. In Europe, EFSA reported 6,558 foodborne outbreaks in 2024, up 14.5% from 2023, with 62,481 human cases and 3,336 hospitalizations, led by Salmonella, norovirus, and Campylobacter.

The main driving factor is stricter food regulation and traceability. The U.S. FDA’s Food Traceability Rule under FSMA Section 204 requires additional records for selected high-risk foods, with the compliance date listed as January 20, 2026, supporting demand for verified testing and faster contamination tracking. Food companies are also increasing testing frequency because global supply chains now involve longer transport routes, multi-country sourcing, and higher exposure to cross-contamination.

Regulation is another major driver. In the U.S., the FDA’s FSMA Section 204 Food Traceability Rule requires additional recordkeeping for high-risk foods to support faster identification and removal of potentially contaminated products. This supports pathogen testing because traceability systems need verified safety data across production, processing, storage, and distribution.

In 2025, Bureau Veritas completed a major portfolio move by selling its global food testing business to Mérieux NutriSciences. The transaction covered food laboratory testing activities including microbiological, chemical, and molecular testing, with 34 laboratories, 1,900 technical staff, and operations across 15 countries. Bureau Veritas stated the divestment involved EUR 133 million in 2023 revenue and an enterprise value of EUR 360 million.

By Type Analysis

Salmonella Dominates with 32.80% Due to Rising Food Safety Monitoring

In 2025, Salmonella held a dominant market position, capturing more than a 32.80% share in the Food Pathogen Testing Market. This leadership was supported by the continued global focus on controlling foodborne illnesses across meat, poultry, dairy, processed food, and fresh produce categories. Salmonella remained one of the most closely monitored pathogens because of its frequent association with contamination events and strict food safety compliance requirements across manufacturing and retail supply chains.

By Technology Analysis

Conventional Technology dominates with 41.80% due to its proven reliability and broad adoption across food testing laboratories.

In 2025, Conventional held a dominant market position, capturing more than a 41.80% share in the Food Pathogen Testing Market. The segment maintained its leading position because conventional testing methods continue to serve as a trusted approach for detecting foodborne pathogens across food processing and quality control environments. These methods remain widely used due to their established validation processes, familiarity among laboratory professionals, and acceptance within routine food safety protocols.

By Food Tested Analysis

Meat & Poultry dominates with 33.10% due to higher contamination risks and strict food safety monitoring.

In 2025, Meat & Poultry held a dominant market position, capturing more than a 33.10% share in the Food Pathogen Testing Market. The segment maintained its leading position because meat and poultry products remain among the most actively monitored food categories for microbial contamination and foodborne disease prevention. Testing demand stayed high as producers continued focusing on maintaining product safety across slaughtering, processing, packaging, storage, and distribution stages.

Key Market Segments

By Type

- Salmonella

- E. Coli

- Listeria

- Others

By Technology

- Conventional

- Agar Culturing

- Polymerase Chain Reaction (PCR)

- Others

- Rapid

- Biosensor-based

- Immunological-based

- Others

By Food Tested

- Meat & Poultry

- Fish & Seafood

- Processed Food

- Fruits & Vegetables

- Dairy Products

- Cereals & Grains

- Other Food Products

Market Dynamics

Driver Analysis - Rising Global Food Safety Concerns Accelerate Pathogen Testing

One of the strongest driving factors for the Food Pathogen Testing Market is the growing global burden of foodborne diseases and the increasing pressure on food producers to deliver safer products across the supply chain. As food production becomes more industrialized and international trade expands, testing for harmful microorganisms has become an essential part of food manufacturing and quality assurance programs.

- According to the World Health Organization (WHO), unsafe food causes around 866 million cases of foodborne illness and nearly 1.52 million deaths globally each year based on updated estimates covering 2021. These numbers highlight the scale of contamination risks and explain why food testing systems are receiving greater attention across both developed and developing economies. WHO also reported that foodborne diseases result in approximately USD 310 billion in annual productivity losses and medical costs worldwide, creating a strong economic reason to strengthen food safety infrastructure.

Government agencies and international food organizations have responded with stricter monitoring and stronger food control frameworks. The WHO Global Strategy for Food Safety 2022–2030 encourages countries to modernize surveillance systems, improve laboratory capacity, and strengthen preventive testing practices across food production and distribution networks. Food pathogen testing has become increasingly important for detecting contamination early and reducing public health risks before products reach consumers.

Restraint Analysis - High Testing Costs And Infrastructure Limit Wider Adoption

One major restraining factor for the Food Pathogen Testing Market is the high cost associated with testing infrastructure, laboratory operations, and continuous compliance requirements. Although food safety standards are becoming stricter across global markets, many food manufacturers—especially small and medium-sized processors—continue to face challenges in adopting large-scale pathogen testing programs due to financial and operational limitations.

- According to the World Bank, foodborne diseases create an estimated US$ 95.2 billion in annual productivity losses and an additional US$ 15 billion in yearly treatment costs across low- and middle-income countries. Despite these large economic losses, investment in preventive food safety systems and testing capacity remains uneven across regions.

Food pathogen testing requires investment across multiple stages including sample collection, laboratory equipment, trained technical staff, validation procedures, quality documentation, and regular monitoring cycles. For businesses operating with limited budgets, maintaining frequent testing schedules can increase operating costs and slow wider adoption of advanced food safety systems. This challenge becomes more visible in developing food economies where food production volumes are expanding faster than testing infrastructure.

Opportunity Analysis - Rapid Testing Expansion Supports Safer Food Supply

One major growth opportunity for the Food Pathogen Testing Market is the increasing global shift from reactive food inspection toward preventive food safety systems. Food manufacturers, processors, and regulatory agencies are investing more in early detection and continuous monitoring to stop contamination before products enter distribution channels. This transition is creating stronger long-term demand for food pathogen testing across production, processing, storage, and export operations.

In the U.S., CDC estimates that foodborne illness affects 48 million people yearly, leading to 128,000 hospitalizations and 3,000 deaths. This creates strong demand for testing of Salmonella, E. coli, Listeria, Campylobacter, and norovirus in meat, poultry, dairy, seafood, fresh produce, and ready-to-eat food.

Government rules are also opening new demand. The FDA Food Traceability Rule under FSMA requires stronger recordkeeping for high-risk foods, with a listed compliance date of January 20, 2026. This pushes food manufacturers, processors, and distributors to connect pathogen testing with traceability systems, so contaminated products can be found and removed faster.

Europe also shows clear opportunity. EFSA and ECDC reported 6,558 food-borne outbreaks in 2024, up 14.5% from 2023, with 62,481 human cases and 3,336 hospitalizations. Salmonella, norovirus, and Campylobacter were among the most common causes.

Emerging Trend Analysis - Rapid Molecular Detection Is Transforming Food Safety

One major latest trend in the Food Pathogen Testing industry is the shift from traditional culture-based testing toward rapid molecular detection technologies, especially PCR (Polymerase Chain Reaction), genomic sequencing, and automated pathogen screening systems. Food manufacturers are increasingly adopting these methods because they shorten testing cycles from several days to hours, helping reduce product recalls, improve shelf-life management, and support faster release of food products into the market.

This transition is being supported by growing food safety pressure worldwide. According to the World Health Organization (WHO), unsafe food causes an estimated 600 million cases of foodborne illness and around 420,000 deaths globally every year, with children under five carrying nearly 40% of the disease burden and accounting for 125,000 deaths annually. These figures continue to push governments and food industries toward earlier and faster pathogen detection systems.

Government programs are also accelerating this trend. In the United States, the Food Safety Modernization Act (FSMA) and the FDA’s food traceability requirements encourage stronger preventive controls and quicker identification of contamination events across food supply chains. The focus has moved from reacting to outbreaks toward predicting and preventing them through continuous monitoring and rapid diagnostics. This change increases demand for real-time testing platforms and automated laboratory workflows.

Regional Insights

North America Leads with 48% Share Driven by Strong Food Safety Infrastructure

In 2025, North America held a dominant position in the Food Pathogen Testing Market, accounting for 48% of the global market and reaching approximately USD 8.5 Billion in value. The region maintained leadership due to its highly developed food processing industry, strong regulatory oversight, and widespread adoption of food quality monitoring practices across the supply chain.

The region continues to demonstrate high demand for pathogen testing across meat, poultry, dairy, packaged food, seafood, and ready-to-eat product categories. Food manufacturers across North America place significant emphasis on preventive testing procedures to reduce contamination risks, improve traceability, and maintain product consistency. Routine screening and quality assurance programs have become standard operating practices across production facilities.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2026, SGS remained an important participant in food pathogen testing through laboratory testing, inspection, verification, and certification activities. The company continued supporting food manufacturers with microbiological screening and contamination control services across food categories. SGS maintained operations through a network of more than 2,600 offices and laboratories globally and employed over 99,000 professionals.

In 2026, Eurofins Scientific maintained a strong position in food pathogen testing through extensive laboratory infrastructure and specialized food analytical services. The company supported contamination monitoring, microbial testing, and food safety validation for global food producers. Eurofins operated more than 900 laboratories across over 60 countries with a workforce exceeding 63,000 employees.

In 2026, Intertek Group Plc strengthened its food assurance and pathogen testing capabilities through laboratory services and quality verification programs. The company supported food manufacturers through testing, auditing, inspection, and supply chain compliance services. Intertek operated across more than 100 countries and employed approximately 46,000 people globally. Continued investment in laboratory technologies and quality assurance services supported its presence across processed food and agricultural testing applications.

Top Key Players Outlook

- Bureau Veritas S.A.

- SGS S.A.

- Silliker

- Intertek Group Plc

- Eurofins Scientific

- Microbac Laboratories, Inc

- ALS Limited

- Tentamus

- Genetic Id Na Inc.

Recent Developments

In September 2025, Eurofins also completed the purchase of strategic related-party-owned laboratory sites after 95.6% shareholder approval, reducing future rent burden and supporting long-term site ownership. In 2026, Eurofins’ capital focus remained on core testing areas such as food, environment, and pharmaceutical testing, supported by planned investment in AI, robotics, strategic acquisitions, and laboratory automation.

In 2025–2026, Microbac Laboratories, Inc. remained active in the food pathogen testing sector by supporting food manufacturers with microbiology, pathogen, molecular, ingredient, allergen, GMO, environmental monitoring, nutritional labeling, and consulting services. The company positions itself as one of the top 5 largest U.S. analytical laboratory networks, with 30+ locations nationwide and 50+ years of testing experience.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 17.7 Bn |

| Forecast Revenue (2035) | USD 40.3 Bn |

| CAGR (2026-2035) | 8.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Salmonella, E. Coli, Listeria, Others), By Technology (Conventional, Rapid, Biosensor-based, Immunological-based, Others), By Food Tested ( Meat And Poultry, Fish And Seafood, Processed Food, Fruits And Vegetables, Dairy Products, Cereals And Grains, Other Food Products) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Bureau Veritas S.A., SGS S.A., Silliker, Intertek Group Plc, Eurofins Scientific, Microbac Laboratories, Inc, ALS Limited, Tentamus, Genetic Id Na Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |