Quick Navigation

Report Overview

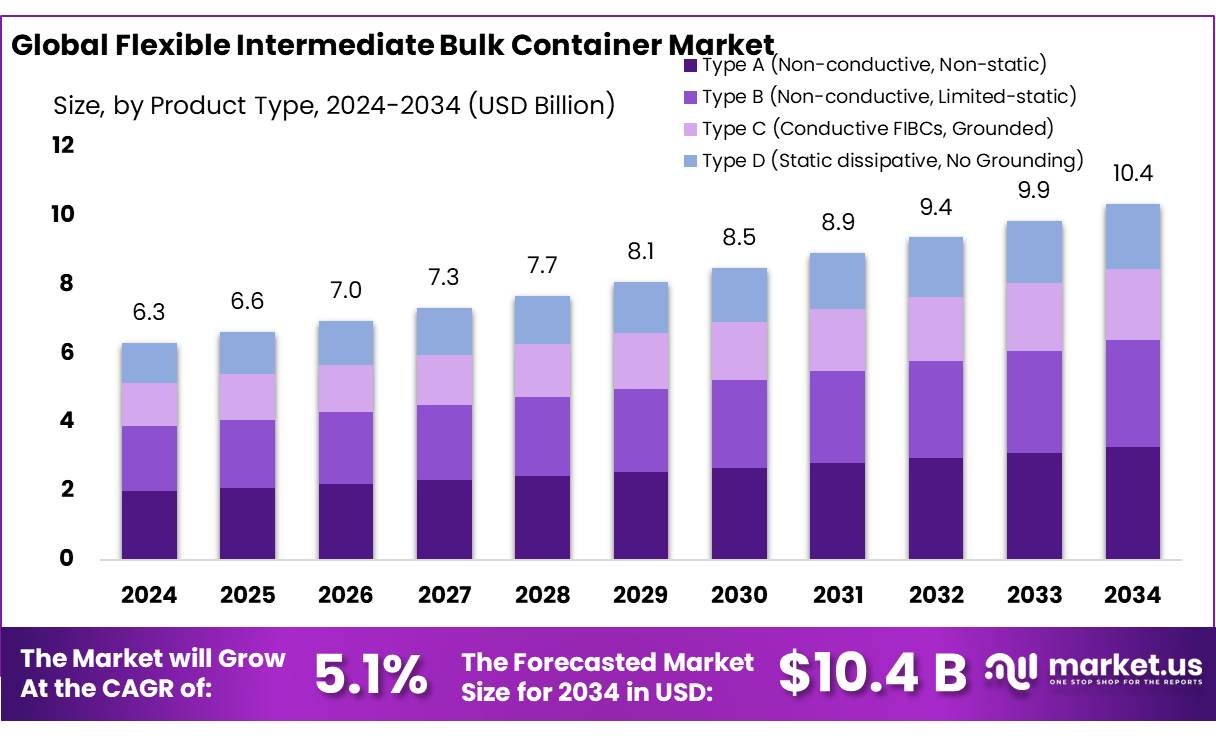

The Global Flexible Intermediate Bulk Container Market size is expected to be worth around USD 10.4 Bn by 2034, from USD 6.3 Bn in 2024, growing at a CAGR of 5.1% during the forecast period from 2025 to 2034.

The Flexible Intermediate Bulk Container (FIBC) industry is experiencing significant growth, driven by increasing demand across various sectors such as agriculture, chemicals, pharmaceuticals, and food processing. FIBCs, commonly known as bulk bags, are large, durable containers made from woven polypropylene, designed for storing and transporting dry, flowable products. Their cost-effectiveness, reusability, and ability to handle large volumes make them a preferred choice over traditional packaging methods.

The FIBC concentrates segment is witnessing robust growth due to rising industrialization and the need for efficient bulk packaging solutions. The chemical industry, a major end-user, accounts for over 30% of FIBC demand, as these containers safely handle hazardous and non-hazardous materials.

Additionally, the mining sector’s expansion, particularly in regions like Latin America and Africa, is boosting FIBC usage for mineral concentrates. For instance, Chile, the world’s largest copper producer, exported 5.6 million metric tons of copper concentrates in 2022, necessitating reliable bulk packaging solutions like FIBCs.

According to the Association of Industrial Mining Suppliers, there are over 3,000 official suppliers to the mining sector with combined sales of more than $13 billion. The United States supplies about 20 percent of parts and equipment to the sector and enjoys a reputation for quality and service. Export opportunities will remain for companies offering products and services that bring operational cost reductions, improved productivity, and more efficient use of energy, water, and cleaner and safer processes.

Key Takeaways

- Flexible Intermediate Bulk Container Market size is expected to be worth around USD 10.4 Bn by 2034, from USD 6.3 Bn in 2024, growing at a CAGR of 5.1%.

- Type A (Non-conductive, Non-static) held a dominant market position, capturing more than a 31.6% share.

- 250kg – 750kg capacity segment held a dominant market position, capturing more than a 54.3% share.

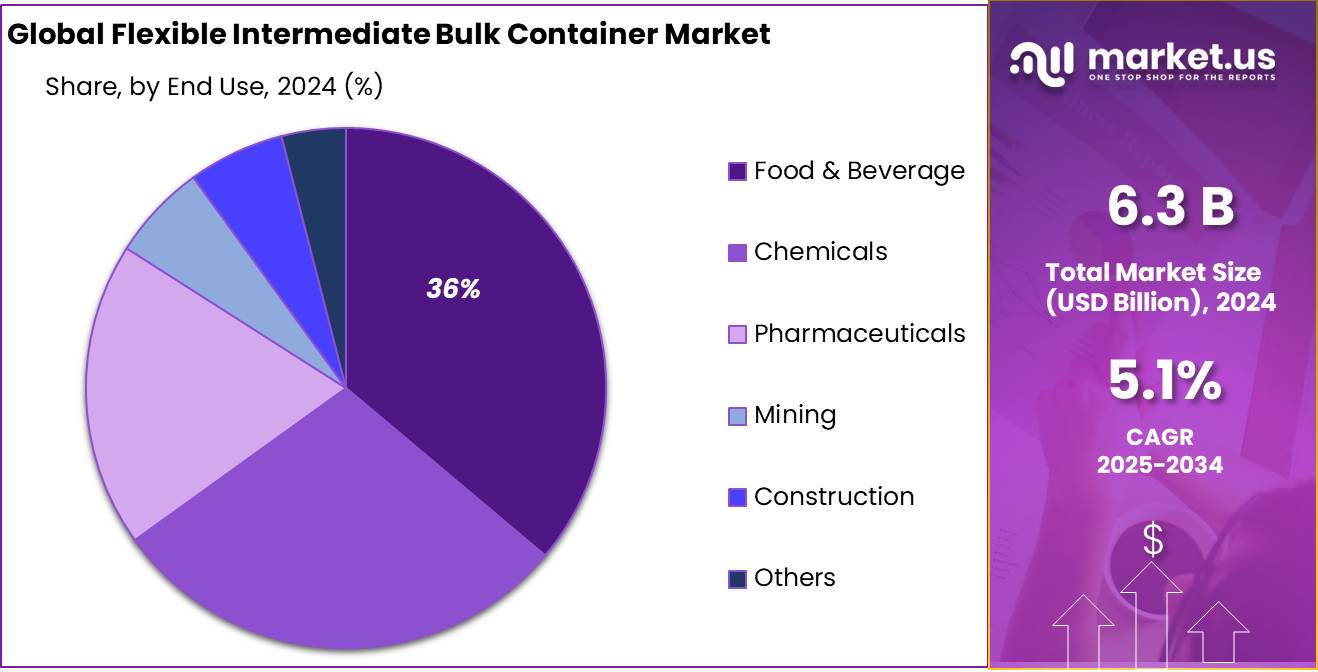

- Food & Beverage held a dominant market position, capturing more than a 36.2% share in the Flexible Intermediate Bulk Container market.

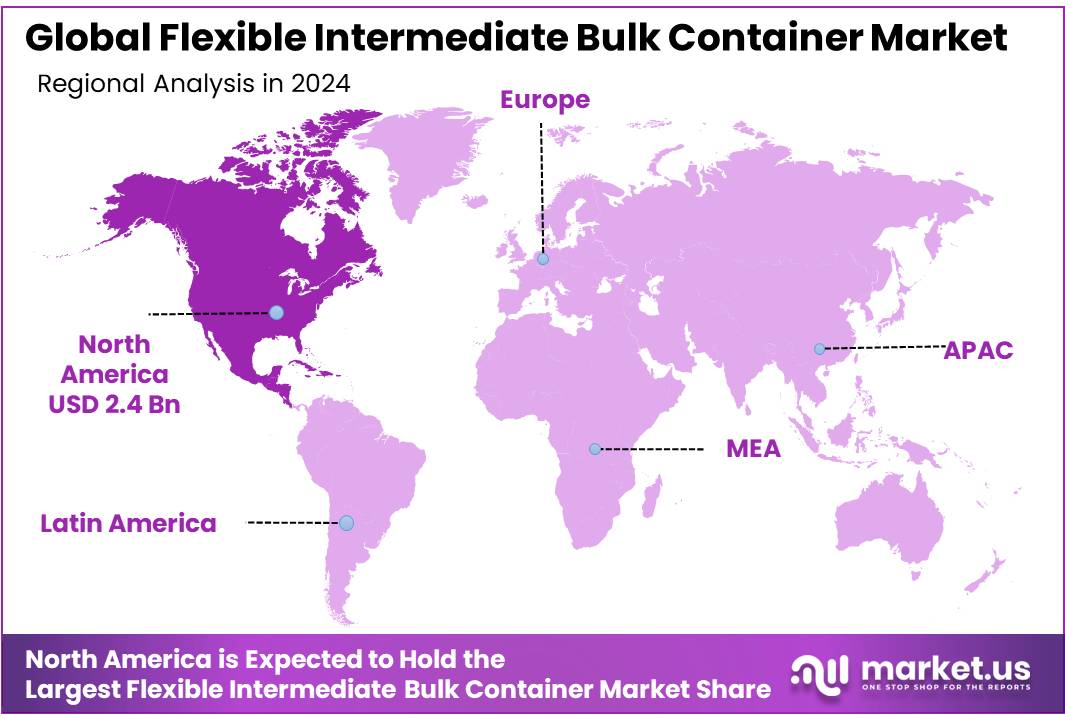

- North America stands as a dominant force in the global Flexible Intermediate Bulk Container (FIBC) market, commanding a substantial 39.1% share, equating to approximately USD 2.4 billion.

By Product Type

Type A (Non-conductive, Non-static) dominates with 31.6% due to its widespread usage in bulk handling.

In 2024, Type A (Non-conductive, Non-static) held a dominant market position, capturing more than a 31.6% share in the Flexible Intermediate Bulk Container market. The segment’s widespread use in transporting non-flammable, non-reactive goods such as grains, cement, and fertilizers significantly contributes to its market dominance.

Additionally, its cost-effectiveness and availability make it a preferred choice for various industries, further solidifying its position in the market. With increased demand for reliable, lightweight, and reusable containers in the logistics sector, Type A FIBCs are expected to maintain their substantial share throughout 2025. The ongoing industrial expansion in emerging economies is projected to sustain the demand for these containers, particularly in bulk transportation applications.

By Capacity

250kg – 750kg Capacity Leads with 54.3% Owing to Versatile Bulk Handling Applications.

In 2024, the 250kg – 750kg capacity segment held a dominant market position, capturing more than a 54.3% share in the Flexible Intermediate Bulk Container market. This capacity range remains highly sought after for handling medium-sized loads in sectors such as agriculture, chemicals, and construction. Its balanced weight capacity makes it an ideal choice for transporting diverse materials, from grains and minerals to chemicals and fertilizers.

The demand for cost-effective and reusable bulk containers is further propelling the uptake of this segment, with its share expected to remain significant throughout 2025 as industries continue to prioritize efficient logistics and material handling solutions.

By End Use

Food & Beverage Secures 36.2% Share, Driven by Increased Demand for Safe Bulk Packaging.

In 2024, Food & Beverage held a dominant market position, capturing more than a 36.2% share in the Flexible Intermediate Bulk Container market. The segment’s growth is attributed to the rising need for secure, hygienic, and durable packaging solutions for transporting bulk food products like grains, pulses, and processed foods.

With stringent food safety regulations in place, the demand for FIBCs that adhere to food-grade standards has surged, further solidifying the segment’s market position. As global food trade continues to expand, the demand for flexible containers capable of safeguarding product integrity is anticipated to maintain its stronghold throughout 2025, particularly in regions with high export volumes.

Key Market Segments

By Product Type

- Type A (Non-conductive, Non-static)

- Type B (Non-conductive, Limited-static)

- Type C (Conductive FIBCs, Grounded)

- Type D (Static dissipative, No Grounding)

By Capacity

- Upto 250 kg

- 250kg – 750 kg

- Above 750 kg

By End Use

- Food & Beverage

- Chemicals

- Pharmaceuticals

- Mining

- Construction

- Others

Drivers

Government Initiatives Driving the Growth of Flexible Intermediate Bulk Containers in the Food Industry

The global Flexible Intermediate Bulk Container (FIBC) market is experiencing significant growth, particularly in the food industry, due to various driving factors. One of the major contributors to this growth is the increasing adoption of sustainable packaging solutions, supported by government initiatives and industry standards.

Governments worldwide are implementing policies that encourage the use of eco-friendly packaging materials. For instance, in Europe, countries like Germany, France, and Italy have introduced regulations that promote the use of biodegradable and recyclable materials in packaging. These regulations are pushing industries, including the food sector, to adopt sustainable packaging solutions like FIBCs.

In the United States, the Food and Drug Administration (FDA) has established guidelines for food-grade packaging materials, ensuring that they are safe for food contact and do not pose health risks. Compliance with these regulations is essential for food manufacturers, leading to the increased use of certified FIBCs that meet FDA standards.

Moreover, the Global Food Safety Initiative (GFSI) recognizes various food safety programs that impact the bulk bag industry. GFSI’s certification ensures that food-grade FIBCs meet stringent safety and quality standards, providing assurance to food processors and producers.

The adoption of FIBCs in the food industry is not only driven by regulatory requirements but also by their practical benefits. FIBCs are lightweight, durable, and cost-effective, making them ideal for transporting and storing bulk food products. Their ability to be reused and recycled further aligns with the growing emphasis on sustainability in the food sector.

Restraints

Regulatory Compliance and Certification Challenges in the FIBC Market

One of the significant challenges facing the Flexible Intermediate Bulk Container (FIBC) market, particularly in the food industry, is adhering to stringent regulatory requirements and obtaining necessary certifications. These regulations are essential to ensure the safety and quality of food products during storage and transportation.

In the United States, the Food and Drug Administration (FDA) mandates that packaging materials in contact with food must be safe and suitable for their intended use. FIBCs used in food applications must comply with these standards, which often requires manufacturers to invest in specialized materials and processes to meet FDA guidelines.

Similarly, in the European Union, the European Food Safety Authority (EFSA) sets regulations that govern materials and articles intended to come into contact with food. FIBCs must meet these standards to be deemed safe for food use, necessitating rigorous testing and certification processes.

Achieving and maintaining these certifications can be resource-intensive for manufacturers. It involves not only meeting material and design specifications but also implementing comprehensive quality control systems and undergoing regular audits. This can lead to increased production costs and longer lead times, which may be challenging for smaller manufacturers or those operating in regions with less stringent regulatory environments.

Moreover, the complexity of these regulations can vary across different markets, requiring manufacturers to navigate a maze of local, national, and international standards. This regulatory fragmentation can complicate the export process and limit market access for FIBC producers.

Opportunity

Government Regulations and Sustainability Driving FIBC Market Growth

The Flexible Intermediate Bulk Container (FIBC) market is experiencing significant growth, particularly in the food industry, due to stringent government regulations promoting sustainable packaging solutions. Governments worldwide are implementing policies that encourage the use of eco-friendly materials and practices, which are directly influencing the adoption of FIBCs.

In the United States, the Food and Drug Administration (FDA) has established guidelines for food-grade packaging materials, ensuring that they are safe for food contact and do not pose health risks. Compliance with these regulations is essential for food manufacturers, leading to the increased use of certified FIBCs that meet FDA standards.

Similarly, in the European Union, the European Food Safety Authority (EFSA) sets regulations that govern materials and articles intended to come into contact with food. FIBCs must meet these standards to be deemed safe for food use, necessitating rigorous testing and certification processes.

Achieving and maintaining these certifications can be resource-intensive for manufacturers. It involves not only meeting material and design specifications but also implementing comprehensive quality control systems and undergoing regular audits. This can lead to increased production costs and longer lead times, which may be challenging for smaller manufacturers or those operating in regions with less stringent regulatory environments.

Trends

Sustainability and Regulatory Pressures Drive Innovation in the FIBC Market

A key driver of this growth is the increasing emphasis on eco-friendly packaging solutions. Governments worldwide are implementing stringent regulations to reduce plastic waste, compelling industries to adopt sustainable practices. For instance, the U.S. food industry, which generated USD 864 billion in 2025, is experiencing a shift towards biodegradable and reusable FIBCs, aligning with both regulatory requirements and consumer demand for environmentally responsible products.

In response to these pressures, manufacturers are innovating by incorporating recycled materials into FIBC production. Companies like FlexSack have introduced polypropylene FIBCs containing 30% recycled content, offering a sustainable alternative without compromising on performance.

This trend is not limited to the U.S.; globally, regions such as China and India are also witnessing a surge in demand for sustainable FIBCs. In China, the market is expected to reach USD 1.6 billion by 2034, driven by stringent plastic waste reduction regulations and the need for bulk packaging solutions in industries like tea and traditional medicine.

The shift towards sustainable FIBCs is further supported by industry associations and government initiatives. For example, the Indian FIBC Association (IFIBCA) plays a pivotal role in promoting sustainable practices within the industry.

Regional Analysis

North America stands as a dominant force in the global Flexible Intermediate Bulk Container (FIBC) market, commanding a substantial 39.1% share, equating to approximately USD 2.4 billion in market value. This leadership is primarily driven by the robust presence of key industries such as food processing, chemicals, pharmaceuticals, and agriculture, all of which are significant consumers of FIBCs.

The United States, in particular, is a major contributor to this dominance. The nation’s extensive manufacturing capabilities, coupled with a well-established logistics infrastructure, facilitate the widespread adoption of FIBCs. Additionally, the U.S. government’s stringent regulations on packaging materials, emphasizing safety and sustainability, have propelled the demand for high-quality, compliant FIBCs.

Canada also plays a pivotal role in this market. The country’s emphasis on sustainable practices and eco-friendly packaging solutions has led to a growing preference for recyclable and biodegradable FIBCs. Furthermore, Canada’s agricultural sector’s need for efficient bulk packaging solutions contributes to the increasing adoption of FIBCs.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Bag Corp. is a leading manufacturer of Flexible Intermediate Bulk Containers (FIBCs), specializing in custom-made solutions for various industries, including food, chemicals, and pharmaceuticals. The company focuses on producing high-quality, durable, and eco-friendly FIBCs. With a strong reputation in the market, Bag Corp. ensures compliance with international standards and regulations, offering tailored products to meet customer needs and promoting sustainability in bulk packaging solutions.

Berry Global Inc. is a global leader in packaging solutions, including FIBCs. The company offers a wide range of sustainable bulk packaging options, catering to the food, chemicals, and agriculture industries. Berry Global’s FIBCs are designed for durability and safety, ensuring efficient transportation and storage. With a commitment to innovation and sustainability, the company focuses on producing high-performance packaging that meets stringent regulatory requirements and addresses environmental concerns.

Bulk Lift International LLC is a prominent player in the FIBC market, providing high-quality bulk bags for industries like food, chemicals, and minerals. With decades of experience, the company offers a range of products, including single-trip and reusable FIBCs, ensuring optimal performance. Bulk Lift International is known for its commitment to customer satisfaction, offering tailored solutions that meet specific industry needs. The company emphasizes safety, compliance, and sustainability in its manufacturing processes.

Top Key Players in the Market

- Bag Corp.

- Berry Global Inc.

- Bulk Lift International LLC

- Dart Container Corporation

- Detmold Group

- Dispo International

- Genpak LLC

- Georgia-Pacific Consumer Products LP.

- Global-Pak Inc.

- Golden Paper Cups

- Greif Inc.

- Isbir Sentetik Dokuma Sanayi A.S.

- Langston Companies Inc.

- LC Packaging International BV

- Plastipak Group

- Rishi FIBC Solutions PVT. Ltd

Recent Developments

In 2024, the company reported a revenue of $19.1 billion, with a significant portion attributed to its packaging solutions, including FIBCs. Berry Global operates over 300 facilities worldwide, producing a wide range of FIBC products such as Type A, B, C, and D bags, catering to industries like chemicals, agriculture, and food processing.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 6.3 Bn |

| Forecast Revenue (2034) | USD 10.4 Bn |

| CAGR (2025-2034) | 5.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Type A (Non-conductive, Non-static), Type B (Non-conductive, Limited-static), Type C (Conductive FIBCs, Grounded), Type D (Static dissipative, No Grounding)), By Capacity (Upto 250 kg, 250kg – 750 kg, Above 750 kg), By End Use ( Food and Beverage, Chemicals, Pharmaceuticals, Mining, Construction, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Bag Corp., Berry Global Inc., Bulk Lift International LLC, Dart Container Corporation, Detmold Group, Dispo International, Genpak LLC, Georgia-Pacific Consumer Products LP., Global-Pak Inc., Golden Paper Cups, Greif Inc., Isbir Sentetik Dokuma Sanayi A.S., Langston Companies Inc., LC Packaging International BV, Plastipak Group, Rishi FIBC Solutions PVT. Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |