Quick Navigation

Report Overview

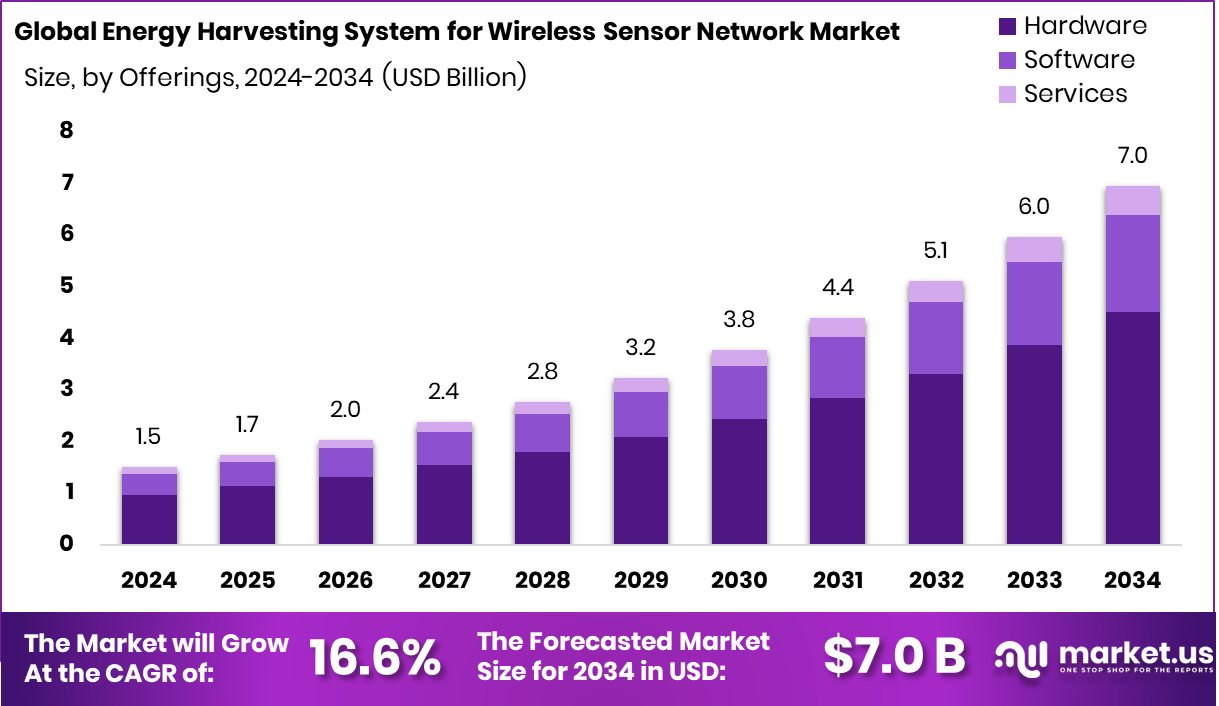

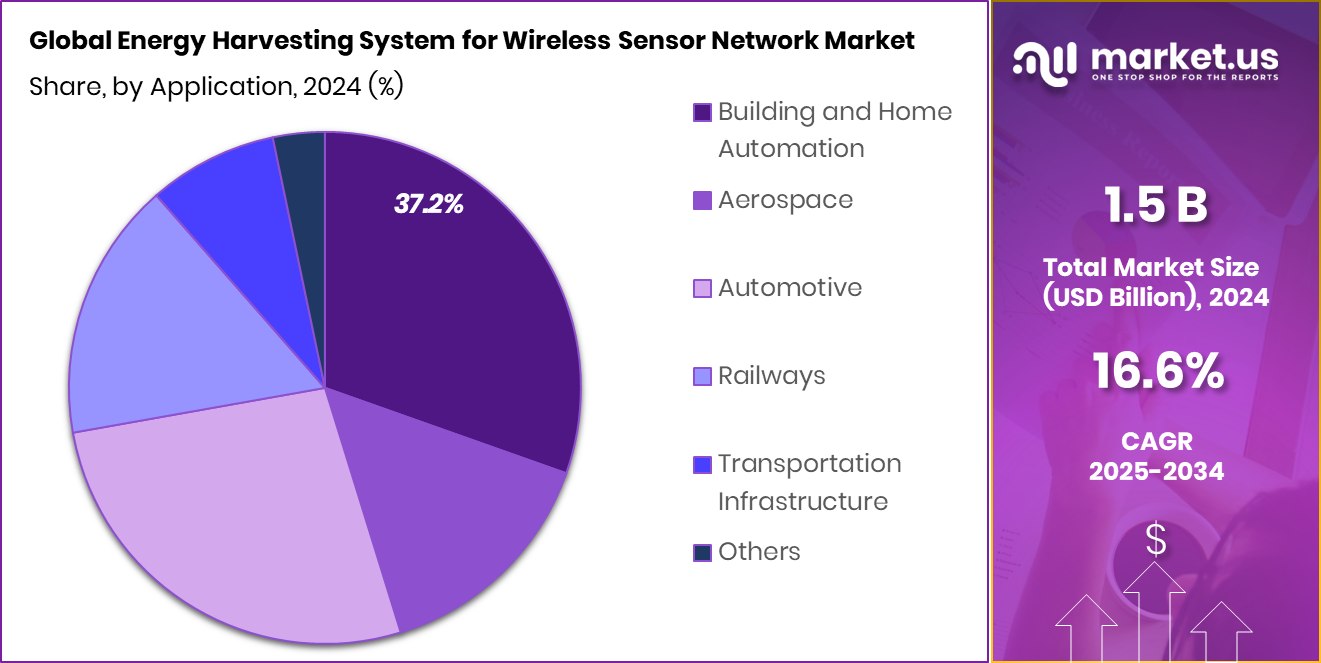

Global Energy Harvesting System for Wireless Sensor Network Market is expected to be worth around USD 7.0 billion by 2034, up from USD 1.5 billion in 2024, and grow at a CAGR of 16.6% from 2025 to 2034. North America’s 43.6% share reflects advanced deployment of wireless energy harvesting systems.

An energy harvesting system for wireless sensor networks (WSNs) refers to the technology that enables sensors to generate power from ambient sources like solar, thermal, vibration, or radio frequency. Instead of relying on batteries, these systems draw energy from their surroundings, allowing sensor nodes to function autonomously for extended periods.

This market encompasses the hardware, software, and integration services that support energy harvesting in WSNs. It includes components like transducers, power management circuits, and energy storage units tailored for small-scale, low-power devices. The market caters to sectors such as industrial automation, building management, transportation, agriculture, and smart cities, where self-powered sensor networks are vital for data collection and monitoring.

Increased adoption of the Internet of Things (IoT) and Industry 4.0 initiatives is are key growth driver. As devices become more connected, the need for maintenance-free, long-lasting sensors is rising. Energy harvesting addresses this by reducing operational costs and downtime associated with battery replacement.

The demand is rising due to the widespread use of wireless sensors in smart infrastructure and environmental monitoring. Government programs promoting sustainable energy and smart city development are encouraging investment in self-powered technologies. The growing number of sensors in logistics and agriculture is further fueling the need for reliable energy sources.

Key Takeaways

- Global Energy Harvesting System for Wireless Sensor Network Market is expected to be worth around USD 7.0 billion by 2034, up from USD 1.5 billion in 2024, and grow at a CAGR of 16.6% from 2025 to 2034.

- Hardware dominated the Energy Harvesting System for Wireless Sensor Network Market with a 64.8% share.

- Temperature sensors contributed 33.7%, highlighting demand in climate monitoring and smart building systems.

- Power Management Integrated Circuits (PMICs) held a strong 48.4% share due to efficient energy conversion.

- Vibration energy harvesting led with 46.3%, used widely in industrial and structural monitoring applications.

- Building and home automation accounted for 37.2%, driven by smart infrastructure and energy-saving initiatives.

- Strong adoption of smart infrastructure boosted North America’s USD 1.09 Bn market size.

By Offerings Analysis

Hardware accounted for a 64.8% share in the Energy Harvesting System Market in 2024.

In 2024, Hardware held a dominant market position in the By Offerings segment of the Energy Harvesting System for Wireless Sensor Network Market, with a 64.8% share. This dominance is primarily attributed to the widespread adoption of core components such as energy transducers, power management integrated circuits, and storage devices essential for enabling energy harvesting in wireless sensor nodes.

As industries increasingly implement self-powered sensing solutions for remote monitoring, the demand for robust, efficient, and miniaturized hardware has seen a steady rise. Hardware forms the backbone of the system, capturing ambient energy and converting it into usable electrical power that ensures continuous sensor operation without the need for frequent maintenance.

Moreover, the transition toward battery-less wireless sensor networks in critical applications, such as industrial automation, infrastructure monitoring, and environmental sensing, continues to drive the demand for specialized hardware solutions. Manufacturers are also focusing on optimizing power efficiency and durability, making hardware a strategic investment area for end users.

With the growing emphasis on sustainable and maintenance-free solutions, hardware is expected to remain a key revenue-generating segment in the near term. Its foundational role in system performance and reliability ensures its sustained preference across both developed and emerging markets deploying wireless sensor networks.

By Sensors Analysis

Temperature sensors held 33.7% market share, the leading sensor type in 2024.

In 2024, Temperature Sensors held a dominant market position in the By Sensors segment of the Energy Harvesting System for Wireless Sensor Network Market, with a 33.7% share. This strong foothold is due to their critical role in a wide range of applications, including industrial equipment monitoring, smart building systems, and environmental sensing.

As industries aim to reduce energy consumption and enhance operational safety, temperature sensors have become essential for detecting overheating, managing climate control, and maintaining system stability. Their integration with energy harvesting systems enables continuous, real-time monitoring without the need for battery replacements, especially in hard-to-access or hazardous environments.

The dominance of temperature sensors is further reinforced by their relatively low power requirements and compatibility with various energy harvesting sources like thermal gradients and ambient heat. These features make them ideal for long-term deployment in wireless sensor networks where power efficiency is paramount.

Their widespread use in sectors such as manufacturing, logistics, agriculture, and utilities supports their leading market share. With the growing implementation of smart infrastructure and condition-based maintenance practices, temperature sensors are expected to remain the preferred choice for energy-harvesting-enabled wireless sensor deployments across global industries.

By Component Analysis

PMIC components dominated with a 48.4% share in the component segmentation of 2024.

In 2024, PMIC held a dominant market position in the By Component segment of the Energy Harvesting System for Wireless Sensor Network Market, with a 48.4% share. Power Management Integrated Circuits (PMICs) are central to the functioning of energy harvesting systems, enabling the efficient conversion, regulation, and storage of harvested energy to ensure uninterrupted power supply to sensor nodes.

PMICs play a vital role in optimizing power usage, particularly in low-power wireless applications where energy availability can be inconsistent. Their integration allows for smart energy routing, load prioritization, and voltage regulation, which are essential for maintaining consistent sensor network operations. As industries adopt battery-free sensors in remote and harsh environments, the performance of PMICs directly impacts system efficiency and lifespan.

Their compact size, high reliability, and advanced functionalities make them indispensable in modern wireless sensor networks. Given their ability to support multi-source energy harvesting and boost overall system performance, PMICs are expected to maintain their leading share as core components within energy harvesting architectures across industrial and infrastructure applications.

By Technology Analysis

Vibration energy harvesting led with a 46.3% share among energy harvesting technologies.

In 2024, Vibration Energy Harvesting held a dominant market position in the By Technology segment of the Energy Harvesting System for Wireless Sensor Network Market, with a 46.3% share. This dominance is largely due to its effectiveness in industrial environments where mechanical movements and vibrations are abundant.

Equipment such as motors, pumps, and compressors consistently generates kinetic energy, which can be converted into electrical energy using vibration harvesting technologies. This has made it the preferred method for powering wireless sensors used in condition monitoring and predictive maintenance.

Vibration energy harvesting offers the advantage of continuous power generation in dynamic settings without relying on sunlight or ambient temperature differences. This reliability enhances the longevity and autonomy of sensor nodes deployed in manufacturing plants, transportation systems, and heavy machinery. The technology’s compatibility with rugged environments and its minimal maintenance requirements contribute to its growing adoption.

As industries push toward automation and real-time diagnostics, vibration-based systems offer a cost-effective and sustainable solution to support sensor networks. With the ability to operate in both high and low-frequency settings, vibration energy harvesting remains a practical and scalable option, reinforcing its leading position in powering wireless sensor networks across various industrial applications.

By Application Analysis

Building and home automation held 37.2% market share, the highest by application segment.

In 2024, Building and Home Automation held a dominant market position in the By Application segment of the Energy Harvesting System for Wireless Sensor Network Market, with a 37.2% share. This leadership is driven by the rising demand for energy-efficient and low-maintenance automation systems in residential and commercial buildings.

Wireless sensor networks powered by energy harvesting are increasingly used for lighting control, HVAC monitoring, occupancy detection, and security systems. These solutions eliminate the need for frequent battery replacements, offering long-term cost savings and operational convenience for building operators and homeowners.

As smart buildings become more mainstream, the role of self-powered wireless sensors has expanded significantly. Energy harvesting technologies such as light, vibration, and thermal energy are well-suited for indoor environments, enabling continuous sensor operation without external power sources. The flexibility to retrofit systems in existing structures without rewiring makes these solutions particularly appealing for modernization projects.

Additionally, regulatory support for green buildings and smart energy use further promotes the adoption of sustainable automation systems. With a strong focus on improving energy efficiency, user comfort, and system reliability, building and home automation continues to be the leading application area for energy harvesting systems in wireless sensor networks.

Key Market Segments

By Offerings

- Hardware

- Software

- Services

By Sensors

- Temperature Sensors

- Pressure Sensors

- Flow Sensors

- Level Sensors

- Humidity Sensors

- Motion and IR Sensors

- Position Sensors

- Gas Sensors

By Component

- Transducers

- PMIC

- Secondary Batteries

By Technology

- Light Energy Harvesting

- Vibration Energy Harvesting

- Radio Frequency Energy Harvesting

- Thermal Energy Harvesting

By Application

- Building and Home Automation

- Aerospace

- Automotive

- Railways

- Transportation Infrastructure

- Others

Driving Factors

Rising Demand for Battery-Free Smart Sensor Networks

One of the top driving factors for the Energy Harvesting System for Wireless Sensor Network Market is the growing demand for battery-free, self-sustaining smart sensor networks. Industries and governments are increasingly using wireless sensors for monitoring systems in remote, hazardous, or hard-to-reach areas where replacing batteries is either expensive or impossible.

Energy harvesting allows these sensors to run on energy captured from the environment, like sunlight, vibrations, or heat, making them more reliable and cost-effective over time. This is especially helpful in sectors like building automation, industrial maintenance, and environmental monitoring.

As smart cities and connected infrastructures grow worldwide, energy harvesting helps ensure long-term, maintenance-free performance of sensors, creating a strong push for adoption in modern sensor systems.

Restraining Factors

High Initial Costs Limit Widespread Market Adoption

A key restraining factor for the Energy Harvesting System for Wireless Sensor Network Market is the high initial cost of setup. Although energy harvesting reduces long-term maintenance expenses, the upfront investment in specialized hardware like transducers, power management circuits, and storage components can be expensive. This makes it difficult for small- and medium-sized enterprises or budget-sensitive projects to adopt the technology immediately.

Additionally, integrating these systems with existing infrastructure may require custom solutions, further raising costs. Many organizations hesitate to switch from traditional battery-powered sensors due to these financial barriers. Until component prices fall or economies of scale are achieved, the cost factor is expected to slow down wider adoption, particularly in emerging or cost-conscious markets.

Growth Opportunity

Expanding Smart City Projects Boost Market Potential

One major growth opportunity for the Energy Harvesting System for Wireless Sensor Network Market lies in the global expansion of smart city projects. Governments and municipalities are increasingly investing in technologies that improve energy efficiency, public safety, traffic flow, and environmental monitoring. Energy harvesting-powered wireless sensors are ideal for these applications because they operate without batteries and require little to no maintenance.

They can be used in streetlights, air quality monitors, parking systems, and building automation, making urban infrastructure more intelligent and efficient. As more cities adopt connected solutions, the demand for self-powered sensors is expected to rise sharply. This creates a strong opportunity for growth as energy harvesting systems become essential to future-proof smart urban environments.

Latest Trends

Hybrid Energy Harvesting Enhances Sensor Reliability

A notable trend in the Energy Harvesting System for Wireless Sensor Network Market is the increasing adoption of hybrid energy harvesting solutions. These systems combine multiple energy sources—such as solar, thermal, and vibration—to ensure a more reliable and consistent power supply for wireless sensors. By leveraging diverse ambient energies, hybrid systems can mitigate the limitations associated with single-source harvesting, such as variability in sunlight or mechanical vibrations.

This approach enhances the operational stability of sensor networks, particularly in environments where energy availability fluctuates. The integration of hybrid energy harvesting not only improves the longevity and maintenance-free operation of sensors but also expands their applicability across various sectors, including industrial automation, smart buildings, and environmental monitoring.

Regional Analysis

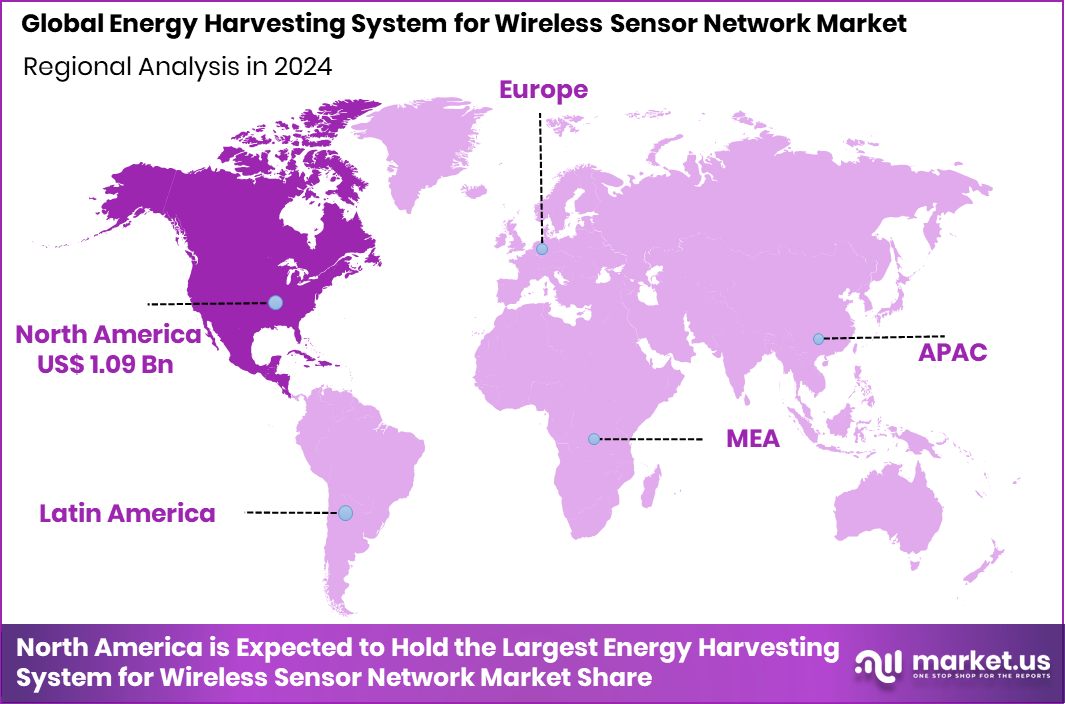

In 2024, North America led with a 43.6% market share, valued at USD 1.09 Bn.

In 2024, North America emerged as the leading region in the Energy Harvesting System for Wireless Sensor Network Market, commanding a dominant 43.6% share with a market value of USD 1.09 billion. This strong regional position is supported by advanced industrial infrastructure, early adoption of smart technologies, and government support for sustainable energy initiatives.

The U.S. and Canada have seen increased deployment of energy harvesting-enabled wireless sensor networks across smart buildings, industrial automation, and utility monitoring systems. Europe followed with a notable market presence, backed by regulatory directives encouraging the integration of energy-efficient technologies in smart grids and buildings.

In the Asia Pacific region, growth is being driven by rapid urbanization and the expansion of smart city projects, particularly in countries like China, Japan, and South Korea. Meanwhile, the Middle East & Africa region is gradually adopting these systems in infrastructure and oil & gas applications, with interest growing in remote sensing solutions.

Latin America remains in the early adoption phase, with pilot deployments underway in environmental monitoring and smart agriculture. Overall, North America’s leadership is underscored by its robust investment in maintenance-free wireless sensing technologies, making it the dominant regional force in the global market landscape for 2024.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, ABB Ltd continued to reinforce its presence in the global Energy Harvesting System for Wireless Sensor Network Market through its focus on industrial automation and smart infrastructure. ABB’s deep expertise in power and automation technologies enables it to design and deliver energy-efficient systems where self-powered sensor networks are integral. The company’s existing automation platforms benefit from the integration of energy harvesting solutions, particularly in applications requiring minimal human intervention and reduced maintenance cycles.

Infineon Technologies, a prominent semiconductor manufacturer, plays a pivotal role in advancing power management solutions for energy harvesting systems. In 2024, the company’s developments in ultra-low-power ICs and efficient power management chips supported the growth of compact and long-lasting wireless sensor nodes. Infineon’s innovations are critical in enabling reliable energy harvesting performance, especially for temperature, vibration, and RF-based sensor technologies, making it a preferred partner for OEMs and device integrators targeting scalable and sustainable deployments.

EnOcean GmbH, known for its energy harvesting wireless technology, maintained a strong foothold in building automation and smart home markets. In 2024, EnOcean’s self-powered sensors and switches were widely used in commercial buildings across Europe and North America, reducing reliance on batteries while supporting zero-maintenance systems.

Top Key Players in the Market

- ABB Ltd

- Infineon Technologies

- EnOcean GmbH

- Fujitsu Limited

- Lord Microstrain

- Microchip Technology Inc.

Recent Developments

- In October 2024, Fujitsu announced the global rollout of its AI-powered network technology, incorporating energy-efficient solutions into its O-RAN-compliant Service Management and Orchestration system.

- In March 2023, Infineon Technologies introduced a new NFC tag-side controller that integrates sensing and energy harvesting capabilities, enabling compact, battery-free smart sensing IoT solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.5 Billion |

| Forecast Revenue (2034) | USD 7.0 Billion |

| CAGR (2025-2034) | 16.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Offerings (Hardware, Software, Services), By Sensors (Temperature Sensors, Pressure Sensors, Flow Sensors, Level Sensors, Humidity Sensors, Motion and IR Sensors, Position Sensors, Gas Sensors), By Component (Transducers, PMIC, Secondary Batteries), By Technology (Light Energy Harvesting, Vibration Energy Harvesting, Radio Frequency Energy Harvesting, Thermal Energy Harvesting), By Application (Building and Home Automation, Aerospace, Automotive, Railways, Transportation Infrastructure, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | ABB Ltd, Infineon Technologies, EnOcean GmbH, Fujitsu Limited, Lord Microstrain, Microchip Technology Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |