Quick Navigation

Report Overview

The Global Electrical Stimulation Devices Market size is expected to be worth around US$ 10.7 Billion by 2033, from US$ 6.5 Billion in 2023, growing at a CAGR of 5.1% during the forecast period from 2024 to 2033.

Electrical stimulation therapies such as Transcutaneous Electrical Nerve Stimulation (TENS), Electrical Muscle Stimulation (EMS), and Functional Electrical Stimulation (FES) play a crucial role in pain management and rehabilitation. For example, a systematic review and meta-analysis from BMJ OPEN involving 381 studies and 24,532 participants revealed that TENS significantly reduces pain intensity with a standardized mean difference of -0.96 (95% CI -1.14 to -0.78). Similarly, research from FRONTIERS indicates that EMS enhances muscle strength and endurance through thrice-weekly sessions over 4 to 6 weeks.

Safety considerations are paramount with these therapies. The aforementioned BMJ OPEN study noted that TENS-related adverse events were mild and comparable to those with placebo treatments. EMS also demonstrates a strong safety profile, provided that the devices are used correctly, highlighting the importance of proper training and settings to avoid potential discomfort or injuries. These findings advocate for the broader adoption of these therapies in clinical practices, supported by robust evidence of their effectiveness and safety.

The market for electrical stimulation devices is tightly regulated by authorities such as the U.S. FDA and the European Medicines Agency. These regulatory bodies enforce rigorous standards that ensure the safety and efficacy of these devices but also pose challenges by extending the product development cycle and escalating costs. Compliance with these standards is crucial for maintaining consumer trust and market stability.

Government initiatives also significantly influence the growth of the electrical stimulation device sector. Through favorable reimbursement policies and healthcare infrastructure investments, especially in developing economies, governments facilitate the adoption of these advanced medical technologies. These policies are vital for integrating new therapies into the healthcare system, reflecting a governmental commitment to enhancing public health outcomes.

Investment dynamics in the sector highlight its potential for substantial returns, driven by continuous innovation and growing demand for treatment options. Noteworthy developments include Boston Scientific’s acquisition of Axonics, Inc. for $3.7 billion in November 2024, broadening its urology portfolio. Furthermore, in February 2024, Philips introduced the Zenition 90 Motorized Mobile C-arm System, designed to support complex vascular and other clinical procedures, expected to be available commercially from Q2 2024. These strategic moves illustrate the vibrant activity and competitive nature of this market.

Key Takeaways

- The global electrical stimulation devices market is projected to reach US$ 10.7 billion by 2033, growing at a CAGR of 5.1% from 2024 to 2033.

- In 2023, the Transcutaneous Electrical Nerve Stimulation (TENS) segment led the device type category, accounting for over 25.5% of the market share.

- The Orthopaedic Disorders segment dominated the application category in 2023, holding more than 29% of the total market share.

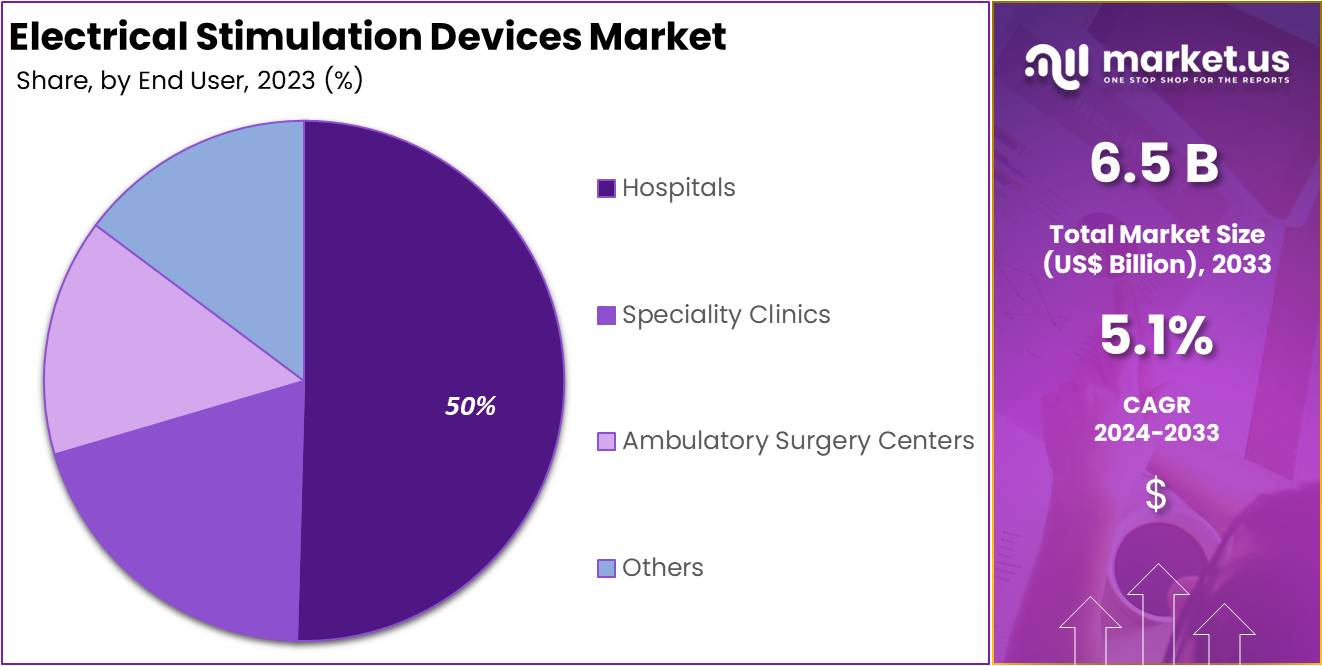

- In 2023, hospitals were the leading end-user segment, capturing more than 58% of the electrical stimulation devices market share.

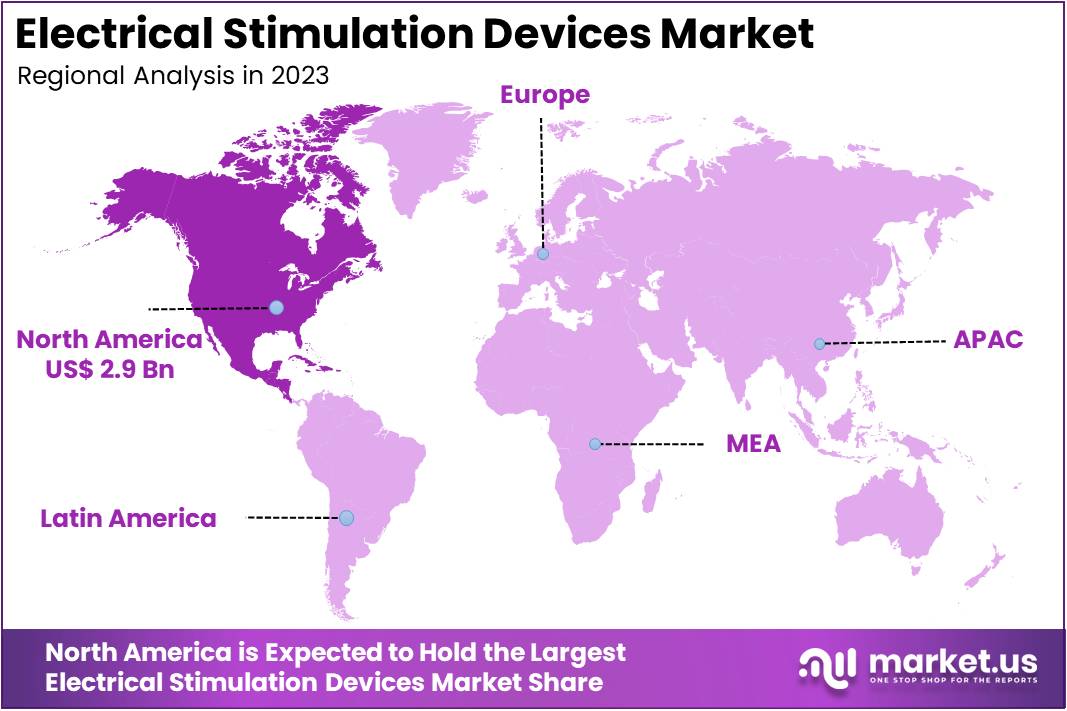

- In 2023, North America maintained a leading market position, accounting for over 45% of the market share and achieving a market value of US$ 2.9 billion.

Industrial Advantages

The electrical stimulation devices market offers significant growth opportunities. These devices are increasingly sought after for non-invasive pain management and rehabilitation. The growing demand, driven by the aging population, positions businesses to expand their customer base. Moreover, these devices offer cost-effective treatment alternatives, making them attractive to both healthcare providers and consumers. Companies can capitalize on this trend by offering affordable solutions. As healthcare systems embrace these technologies, favorable reimbursement and regulatory environments enhance market stability and growth for key players.

Electrical stimulation devices bring substantial benefits to healthcare providers. They help improve patient outcomes, such as pain relief, muscle strength, and rehabilitation. These devices are gaining popularity for their effectiveness in treating various conditions. Technological advancements, such as wireless connectivity and portability, increase patient satisfaction and market adoption. The growing home healthcare sector further boosts demand for these devices, providing an opportunity for companies to target at-home therapy needs. Customizable solutions for different conditions also allow manufacturers to create a competitive edge in the market.

There are numerous opportunities for businesses to expand in the electrical stimulation device market. Emerging markets, such as Asia Pacific and Latin America, are showing increased demand for affordable healthcare solutions. Collaborations with healthcare providers or research institutions can drive product adoption. Investment in R&D enables key players to explore new applications, such as stroke recovery and mental health therapies. Additionally, telehealth integration and government initiatives present new avenues for market growth. Companies that adapt to these trends can gain a significant advantage in the competitive landscape.

Device Type Analysis

In 2023, Transcutaneous Electrical Nerve Stimulation (TENS) segment held a dominant market position in the Device Type Segment of the Electrical Stimulation Devices Market, capturing more than a 25.5% share. This growth is primarily due to the increasing use of TENS devices for pain management. TENS has become a popular option in various clinical settings, as it offers effective, non-invasive relief for chronic pain, benefiting both patients and healthcare professionals.

The Interferential Current Electrical Stimulation (IFC) segment has also experienced notable growth. IFC devices are widely used for deep tissue pain relief and rehabilitation. Their ability to treat pain without relying on medication has led to an increase in their adoption. This is particularly evident in physical therapy, where IFC is highly valued for its effectiveness and non-invasive nature, making it an attractive treatment option for many patients.

Electrical Muscle Stimulation (EMS) devices are another key segment in the market. These devices are commonly used for muscle rehabilitation and preventing muscle atrophy. The growing demand for post-surgical rehabilitation, coupled with an increasing incidence of muscle-related injuries, has driven the growth of the EMS segment. EMS devices help improve muscle strength and assist in faster recovery, which makes them essential in both clinical and home therapy settings.

Neuromuscular Electrical Stimulation (NMES) and Functional Electrical Stimulation (FES) are gaining prominence in rehabilitation treatments. NMES aids in restoring movement to impaired muscles, while FES helps with functional movements, such as walking. Both devices are particularly beneficial for patients recovering from strokes or spinal cord injuries. The Others segment, which includes niche electrical stimulation devices, is also growing due to technological advancements and a rising demand for alternative therapeutic options.

Application Analysis

In 2023, the Orthopaedic Disorders segment held a dominant market position in the Application Segment of the Electrical Stimulation Devices Market, capturing more than 29% of the market share. This growth is driven by the rising prevalence of musculoskeletal injuries. Electrical stimulation devices are effective in promoting tissue healing, reducing pain, and improving muscle function. These benefits have led to a growing preference for electrical stimulation as a non-invasive treatment option in orthopaedic rehabilitation.

The Neurological Disorders segment is also seeing significant growth. This is largely due to the increasing number of patients with conditions like stroke, multiple sclerosis, and cerebral palsy. Electrical stimulation devices aid in muscle re-education and functional improvement for individuals with neurological impairments. The demand for such devices continues to rise as more people seek alternative treatments to help manage neurological conditions.

The Musculoskeletal Disorder Management segment is growing as well. Electrical stimulation devices help treat chronic pain, muscle spasms, and joint stiffness associated with musculoskeletal disorders. These devices offer a non-invasive alternative to traditional pain management methods. As awareness of their benefits increases, the adoption of electrical stimulation devices in treating musculoskeletal conditions is expected to rise further in the coming years.

The Incontinence Management segment is gaining traction. Electrical stimulation provides an effective, drug-free solution for urinary and fecal incontinence. This treatment is becoming more popular, especially with the aging population. Additionally, the Metabolism & GIT Management segment is experiencing moderate growth. Electrical stimulation helps improve gastrointestinal motility, offering potential benefits for digestive disorders, though this segment remains smaller compared to orthopaedic and neurological applications.

End User Analysis

In 2023, the Hospitals segment held a dominant market position in the End User Segment of the Electrical Stimulation Devices Market, capturing more than a 58% share. Hospitals remain the largest end-users of electrical stimulation devices due to their advanced infrastructure. These devices are widely used in hospitals for various treatments, including pain management, rehabilitation, and neurological care. The ability to offer diverse treatment options drives the continuous adoption of these devices in hospital settings.

The Specialty Clinics segment follows closely as a significant end user in the market. These clinics focus on specific treatments like physical therapy and pain management. As awareness about the benefits of electrical stimulation devices grows, more specialty clinics are incorporating them into their services. This trend is expected to continue as patients seek specialized care that offers more targeted and effective treatments for various conditions.

Ambulatory Surgery Centers (ASCs) are another growing segment in the electrical stimulation devices market. These centers have seen an increase in outpatient procedures, which has led to higher adoption rates for electrical stimulation devices. ASCs offer cost-effective solutions and enhanced patient care. This trend is expected to continue as patients and healthcare providers seek more affordable options without compromising on treatment effectiveness.

Other end users, such as rehabilitation centers, home healthcare services, and research institutions, hold a smaller but growing share in the market. These sectors are increasingly adopting electrical stimulation devices for their therapeutic benefits. Awareness of the advantages of these devices in non-hospital settings is driving their growth. As technology advances, the use of electrical stimulation devices in these areas is expected to expand steadily in the coming years.

Key Market Segments

By Device Type

- Transcutaneous Electrical Nerve Stimulation (TENS)

- Interferential Current Electrical Stimulation (IFC)

- Electrical Muscle Stimulation (EMS)

- Russian Stimulation

- Neuromuscular Electrical Stimulation (NMES)

- Functional Electrical Stimulation (FES)

- Others

By Application

- Orthopaedic Disorders

- Neurological Disorders

- Musculoskeletal Disorder Management

- Metabolism & GIT Management

- Incontinence Management

- Others

By End User

- Hospitals

- Speciality Clinics

- Ambulatory Surgery Centers

- Others

Drivers

Increasing Prevalence Of Chronic Pain Conditions And Neurological Disorders

The escalating prevalence of chronic pain conditions and neurological disorders is a significant driver of the global electrical stimulation devices market. According to the World Health Organization, over 3 billion people worldwide were living with a neurological condition in 2021, making neurological disorders the leading cause of illness and disability globally. This surge in prevalence has heightened the demand for effective, non-invasive pain management solutions, positioning electrical stimulation devices as a viable alternative to traditional drug-based treatments.

Electrical stimulation therapies, such as spinal cord stimulation (SCS) and transcutaneous electrical nerve stimulation (TENS), have demonstrated efficacy in alleviating chronic pain. For instance, SCS has been shown to provide significant relief for individuals with chronic back pain, especially when other treatments have failed. Similarly, TENS units offer drug-free pain relief by sending electrical currents through the skin to disrupt pain signals.

Restraints

High Cost Of Electrical Stimulation Devices

The high cost of electrical stimulation devices, such as Transcutaneous Electrical Nerve Stimulation (TENS) units and Neuromuscular Electrical Stimulation (NMES) devices, poses a significant barrier to their widespread adoption, especially in price-sensitive markets. According to Medical News Today, the PowerDot 2.0 Duo, a TENS and NMES device, is priced at approximately $349.00. Similarly, the Aleve Direct Therapy TENS device is available for around $99.99 on AMAZON. These prices can be prohibitive for many individuals, limiting access to these therapeutic options.

Moreover, the complexity of using these devices and the limited reimbursement options in certain regions further restrict their adoption. In the United States, Medicare covers TENS units under the Durable Medical Equipment benefit, but only if specific criteria are met, such as a trial of other pain management methods. Additionally, the Centers for Medicare & Medicaid Services (CMS) has determined that certain devices, like the Cala device for essential tremor, do not qualify as durable medical equipment due to their expected lifespan being less than three years. This lack of reimbursement can deter patients from utilizing these devices, even when they may be beneficial.

Opportunities

Growing Demand For Home-Based Healthcare Solutions

The escalating demand for home-based healthcare solutions presents a significant opportunity for the electrical stimulation devices market. As the global population ages, the prevalence of chronic conditions such as diabetes, cardiovascular diseases, and neurological disorders is rising, necessitating continuous care and rehabilitation. Electrical stimulation devices are pivotal in managing these conditions, offering therapies that enhance muscle strength, alleviate pain, and promote healing.

The global home healthcare market is projected to experience substantial growth, with estimates indicating a compound annual growth rate (CAGR) of 8.2% Till 2032, expected to reach US$ 797.8 billion. This expansion is driven by technological advancements and a preference for cost-effective healthcare delivery. Electrical stimulation devices, as integral components of home healthcare, are poised to benefit from this trend.

The convergence of an aging population, rising chronic disease prevalence, and the widespread adoption of telemedicine creates a fertile environment for the growth of the electrical stimulation devices market. Developing portable, user-friendly devices tailored for home use can meet the evolving needs of patients and healthcare providers, capitalizing on the expanding home healthcare sector.

Trends

Advancements In Technology

Advancements in technology are significantly enhancing the effectiveness and personalization of electrical stimulation therapies. Modern devices now offer customizable settings, including adjustable intensity levels and treatment durations, allowing for individualized patient care. This trend is evident in the growing adoption of devices like Transcutaneous Electrical Nerve Stimulation (TENS) units, which provide patients with control over their pain management.

For instance, the development of non-invasive devices like Arc-EX, which delivers electrical stimulation to the spinal cord via skin electrodes, has shown promising results in improving hand and arm function in individuals with severe paralysis. Similarly, advancements in brain stimulation technologies, such as transcranial direct current stimulation (tDCS), have been explored for treating conditions like depression.

A recent study found that individuals using a home-use headset delivering small electric currents to the brain were more than twice as likely to experience improvements or remission of depressive symptoms compared to those using a placebo device. These developments underscore the transformative potential of electrical stimulation therapies, offering patients more effective and personalized treatment options.

Regional Analysis

In 2023, North America held a dominant market position, capturing more than a 45% share and holding a market value of US$ 2.9 billion for the year. This strong performance is attributed to the high adoption rate of electrical stimulation devices across the region. The growing prevalence of chronic conditions, such as musculoskeletal disorders, has driven demand for pain management solutions. Additionally, the presence of advanced healthcare infrastructure and increasing healthcare expenditures further support the region’s market leadership.

The demand for electrical stimulation devices in North America is also fueled by technological advancements. Innovative features, such as portable and user-friendly devices, have enhanced patient comfort and ease of use. This has led to increased consumer adoption, particularly for at-home therapy. Furthermore, regulatory support and a favorable reimbursement landscape have facilitated market growth. These factors together continue to strengthen North America’s position in the global electrical stimulation devices market.

North America’s dominance is expected to persist due to ongoing investments in research and development. The region is home to several key players that are continually introducing advanced solutions to cater to a diverse range of therapeutic needs. Moreover, healthcare policies in North America increasingly focus on improving access to non-invasive pain management treatments. This trend is likely to drive further demand for electrical stimulation devices in the coming years, solidifying North America’s market share.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Medtronic is a major player in the electrical stimulation devices market. The company offers a wide range of devices for pain management, neuromodulation, and spinal cord stimulation. Known for its continuous investment in research and development, Medtronic leads in technological advancements. Its strong market presence is supported by global reach and strategic partnerships, helping the company maintain a competitive advantage. Medtronic’s innovations continue to shape the future of the electrical stimulation sector, meeting the evolving needs of healthcare providers and patients worldwide.

Asahi Kasei Corporation has become a significant player in the electrical stimulation devices market, particularly in Asia. The company focuses on advanced technologies to treat chronic pain and neurological disorders. Asahi Kasei places great emphasis on research and patient-centered solutions. This approach allows the company to strengthen its position and meet the growing demand for electrical stimulation devices. With continuous investments in technology and market expansion, Asahi Kasei is poised to further its growth and enhance its footprint in the global market.

Boston Scientific is another key player in this market, especially known for its spinal cord stimulation and deep brain stimulation products. The company’s focus on innovation has allowed it to expand its product range. Boston Scientific integrates cutting-edge technologies such as wireless and rechargeable systems into its devices. These advancements provide patients with more flexible and effective treatment options. The company continues to grow through strategic acquisitions and partnerships, solidifying its position as a leading player in the electrical stimulation devices market.

Market Key Players

- Medtronic

- Asahi Kasei Corporation

- Boston Scientific Corporation

- Koninklijke Philips N.V.

- Zynex Medical

- Abbott

- NeuroMetrix Inc.

- Cyberonics Inc.

- BIOTRONIK Inc.

- Defibtech LLC.

- CU Medical System Inc

- Beijing Pins Medical Co. Ltd

- DJO Global

- MicroPort Scientific Corporation

- Aleva Neurotherapeutics SA.

Recent Developments

- In April 2024: Medtronic received U.S. Food and Drug Administration (FDA) approval for its Inceptiv™ closed-loop rechargeable spinal cord stimulator (SCS) designed to treat chronic pain. This device features a closed-loop system that senses biological signals along the spinal cord and automatically adjusts stimulation in real time, aligning therapy with patients’ daily activities. Notably, Inceptiv offers full-body 1.5T and 3T MRI access without power or impedance restrictions, and it is recognized as the world’s smallest and thinnest fully implantable SCS device.

- In February 2024: Asahi Kasei participated in a Series C funding round for Avation Medical, contributing to a total of over $22 million raised. This investment supports the U.S. launch of the Vivally System, a non-invasive, FDA-cleared wearable neuromodulation device designed to treat urge urinary incontinence and urinary urgency caused by overactive bladder syndrome. The device delivers closed-loop, autonomously adjusted electrical stimulation and is intended for at-home use in weekly 30-minute sessions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 6.5 Billion |

| Forecast Revenue (2033) | USD 10.7 Billion |

| CAGR (2024-2033) | 5.1% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Device Type (Transcutaneous Electrical Nerve Stimulation (TENS), Interferential Current Electrical Stimulation (IFC), Electrical Muscle Stimulation (EMS), Russian Stimulation, Neuromuscular Electrical Stimulation (NMES), Functional Electrical Stimulation (FES), Others), By Application (Orthopaedic Disorders, Neurological Disorders, Musculoskeletal Disorder Management, Metabolism & GIT Management, Incontinence Management, Others), By End User (Hospitals, Speciality Clinics, Ambulatory Surgery Centers, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Medtronic, Asahi Kasei Corporation, Boston Scientific Corporation, Koninklijke Philips N.V., Zynex Medical, Abbott, NeuroMetrix Inc., Cyberonics Inc., BIOTRONIK Inc., Defibtech LLC., CU Medical System Inc, Beijing Pins Medical Co. Ltd, DJO Global, MicroPort Scientific Corporation, Aleva Neurotherapeutics SA. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |