Global Diesel Exhaust Fluid Market Size, Share, And Enhanced Productivity By Vehicle Type (Passenger Cars, LCVs, HCVs), By Component Type (Catalysts, Tanks, Injectors, Sensors, Others), By Application Type (Construction Equipment, Agricultural Tractors, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: March 2026

- Report ID: 179823

- Number of Pages: 252

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

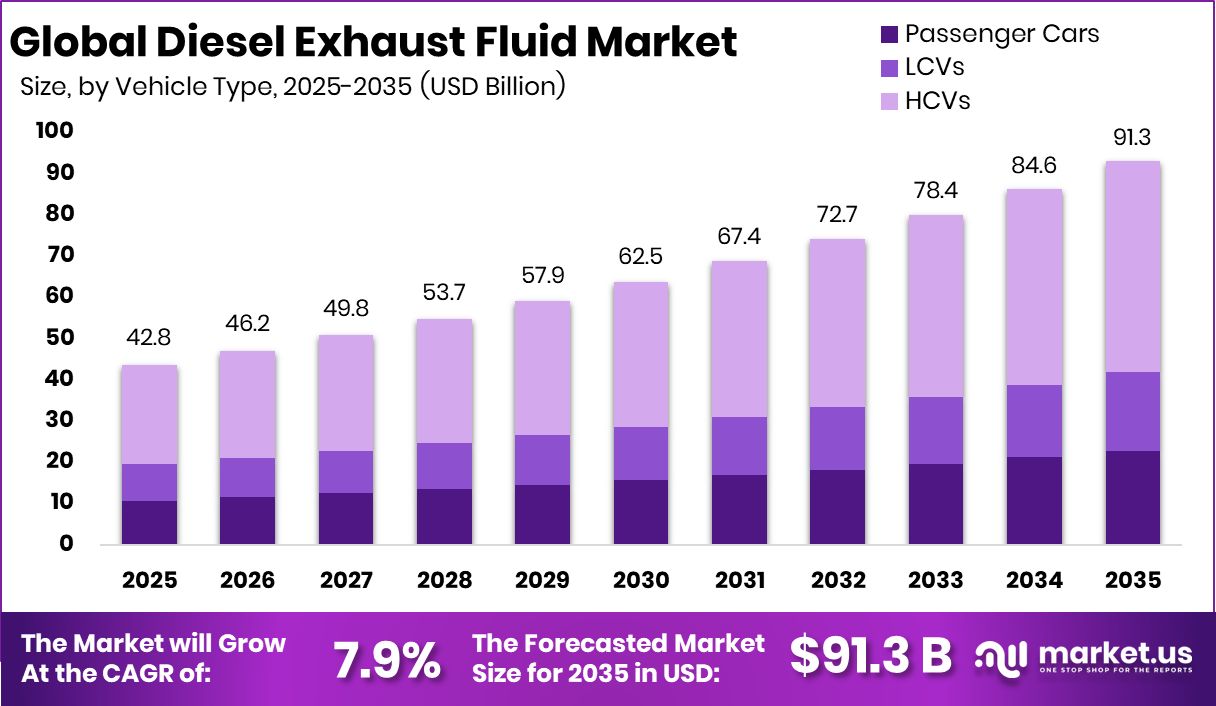

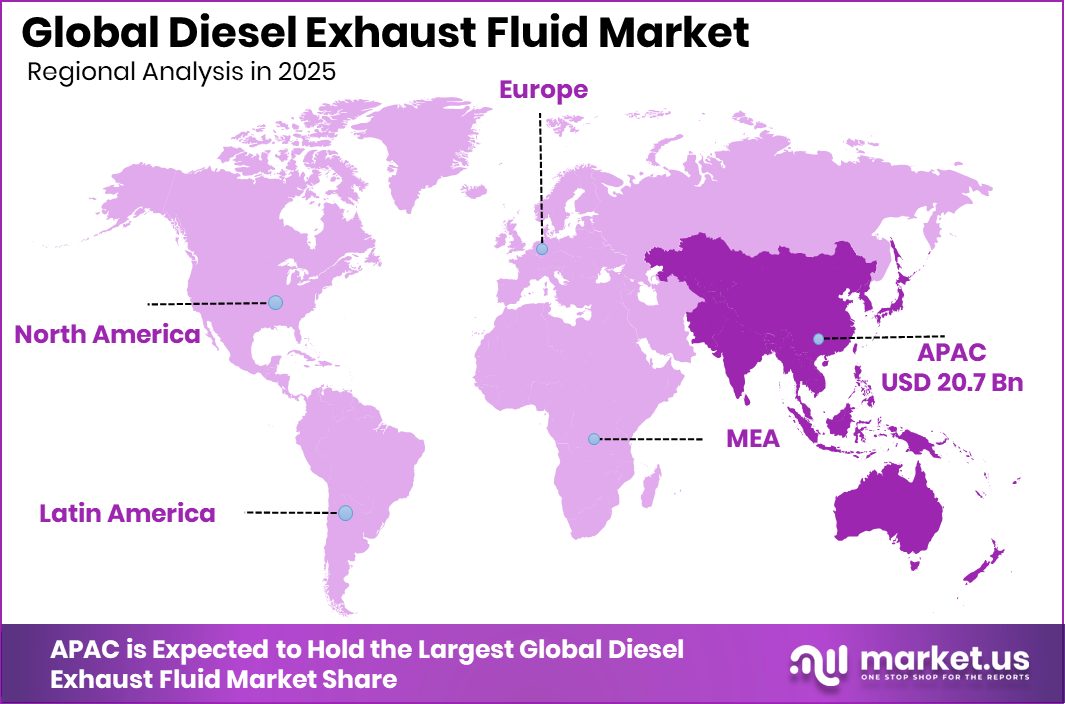

The Global Diesel Exhaust Fluid Market is expected to be worth around USD 91.3 billion by 2035, up from USD 42.7 billion in 2025, and is projected to grow at a CAGR of 7.9% from 2026 to 2035. Region Asia Pacific leads market at 48.6%, valuing Diesel Exhaust Fluid USD 20.7 Bn.

Diesel Exhaust Fluid is a urea-based liquid used in Selective Catalytic Reduction systems to reduce nitrogen oxide emissions from diesel engines. It works by injecting the fluid into the exhaust stream, converting harmful gases into water vapor and nitrogen. Across passenger cars, LCVs, and HCVs, the fluid has become essential for meeting tightening emission norms in transportation, agriculture, construction, and industrial machinery.

The Diesel Exhaust Fluid Market refers to the global demand, production, and distribution ecosystem supporting this essential emission-control fluid. Growth stems from expanding diesel fleets, rising construction activity, and government pressure to reduce air pollution. Demand increases further as SCR-equipped machinery becomes standard across equipment categories like construction equipment and agricultural tractors.

Growth factors include supportive government initiatives and fresh capital flowing into sectors relying on diesel systems. Recent financial movements—such as Propane unlocking access to $1.5 billion in federal transit grants and South Korea launching a $7.6 billion supply chain fund to boost local urea production—indirectly strengthen the market by improving supply stability and emission-control compliance.

Opportunities arise from new investments targeting industrial supply chains. Capital inflows like Plexus securing $1.3 billion, disaster-relief allocations such as $600 million for agricultural producers, and startup-focused initiatives like the Ag Innovation Challenge offering $165,000 in funding all support equipment upgrades that rely on DEF, reinforcing long-term market demand across multiple application segments.

Key Takeaways

- The Global Diesel Exhaust Fluid Market is expected to be worth around USD 91.3 billion by 2035, up from USD 42.7 billion in 2025, and is projected to grow at a CAGR of 7.9% from 2026 to 2035.

- Diesel Exhaust Fluid Market growth is influenced by HCVs holding a dominant 56.2% vehicle-type share.

- Strong demand in the Diesel Exhaust Fluid Market comes from catalysts, accounting for 44.7% component contribution.

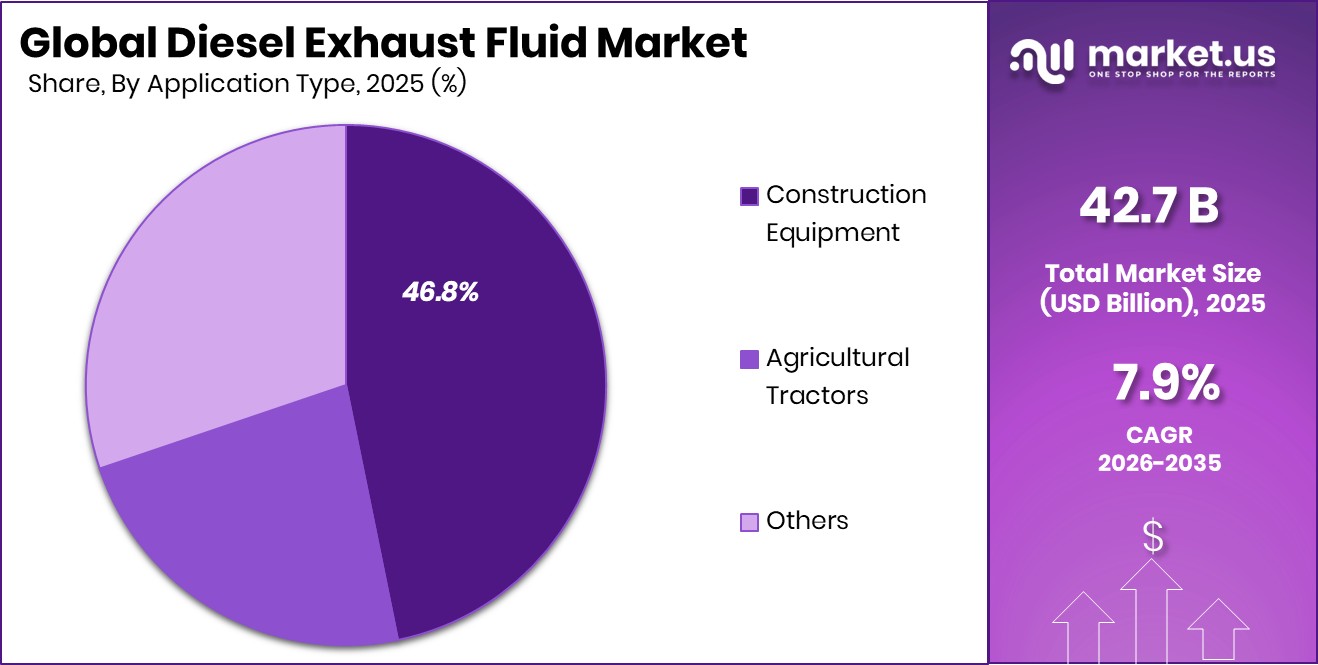

- The Diesel Exhaust Fluid Market expands steadily as construction equipment applications capture a 46.8% usage share.

- Diesel Exhaust Fluid Market in Asia Pacific reaches USD 20.7 Bn with 48.6% dominance.

By Vehicle Type Analysis

Diesel Exhaust Fluid Market sees HCVs dominating with a strong 56.2% share.

In 2025, the Diesel Exhaust Fluid market is expected to expand strongly as Heavy Commercial Vehicles (HCVs) account for nearly 56.2% of overall DEF consumption, reflecting the sector’s continued dependence on diesel fleets for logistics, mining, long-haul transport, and cross-border freight. Stricter emission norms across major economies are pushing fleet operators to maintain consistent DEF usage to keep Selective Catalytic Reduction systems operating efficiently.

The surge in infrastructure development projects and increasing freight movement in Asia, Europe, and North America further strengthens HCV demand. Fleet modernization trends, including the replacement of older trucks with emission-compliant models, also amplify fluid consumption rates, reinforcing HCVs as the leading demand generator in the DEF landscape.

By Component Type Analysis

Catalysts lead the Diesel Exhaust Fluid Market, contributing significantly with 44.7% overall share.

In 2025, catalysts are projected to contribute around 44.7% of the Diesel Exhaust Fluid market’s component demand, driven by industries upgrading emission-control technologies to meet tightening NOx reduction standards. Growth in SCR-equipped engines across trucks, buses, and industrial machinery enhances the need for high-quality catalysts capable of performing under varied operating temperatures.

Manufacturers are investing in durable catalytic materials to improve conversion efficiency, reduce maintenance cycles, and support longer engine life. With regulatory agencies pushing Euro VI, Bharat Stage VI, and EPA standards, catalyst demand is expanding across both developing and developed economies. This shift reinforces the component segment as a vital backbone of the DEF market, ensuring vehicles maintain compliance through dependable emission treatment systems.

By Application Type Analysis

Construction equipment drives the Diesel Exhaust Fluid Market, accounting for a notable 46.8% share.

In 2025, construction equipment is anticipated to contribute approximately 46.8% of the Diesel Exhaust Fluid market demand, reflecting the sector’s rapid growth driven by urban expansion, large-scale infrastructure projects, and increased mechanization of operations. Excavators, loaders, bulldozers, and heavy earthmoving machinery rely heavily on diesel engines integrated with SCR systems, making DEF essential for meeting emission norms at job sites.

Governments across the Asia Pacific, the Middle East, and North America continue to invest in transport infrastructure, smart cities, and renewable energy installations, which in turn boost equipment utilization hours and DEF consumption. OEMs are also focusing on fuel-efficient, emission-optimized machinery, ensuring that construction applications remain a dominant revenue-generating segment for the DEF industry.

Key Market Segments

By Vehicle Type

- Passenger Cars

- LCVs

- HCVs

By Component Type

- Catalysts

- Tanks

- Injectors

- Sensors

- Others

By Application Type

- Construction Equipment

- Agricultural Tractors

- Others

Driving Factors

Stricter emission norms increase DEF demand

In many regions, tougher emission rules continue to push the adoption of Selective Catalytic Reduction systems, directly increasing the need for Diesel Exhaust Fluid across commercial vehicles, construction machinery, and agricultural equipment. Governments are enforcing tighter limits on nitrogen oxide emissions, making DEF an essential operating fluid for diesel-powered fleets. The overall push toward cleaner transportation aligns with ongoing industrial investments.

A notable example is Singapore’s Amperesand raising $80 million in Series A funding, co-led by Walden Catalyst Ventures and Temasek, which signals rising financial support for technologies aimed at environmental compliance and cleaner operations. As industries modernize, this regulatory pressure keeps DEF demand consistently elevated across multiple segments.

Restraining Factors

Limited urea supply disrupts market stability

The Diesel Exhaust Fluid market often faces volatility because DEF production depends heavily on the stable availability of urea. Even small disruptions in feedstock supply can create shortages, raise prices, and impact the movement of logistics fleets and industrial equipment. Global supply chains occasionally face stress from agricultural, chemical, or geopolitical factors that influence urea availability. Capital market activity also shapes the broader environment in which supply chains operate.

A recent example is Latham advising General Catalyst and a16z on Mistral AI’s €1.7 billion Series C funding, demonstrating how large-scale capital flows redirect industry attention and resources. Such financial shifts can amplify uncertainty in urea-linked markets, making supply consistency a continuing challenge.

Growth Opportunity

Local urea manufacturing strengthens regional supply

Building more localized urea production offers one of the strongest opportunities for stabilizing Diesel Exhaust Fluid supply and reducing reliance on imports. Regions investing in domestic fertilizer and chemical manufacturing can secure steady feedstock availability for DEF producers, which supports smoother operations for transportation, construction, and agricultural businesses.

Local sourcing also helps minimize exposure to global price swings. Additional funding activity in wider innovation ecosystems reflects growing interest in industrial modernization. For instance, French preventive healthcare startup Lucis secured €7.2 million from General Catalyst, Y Combinator, and others, showcasing the broader momentum of venture activity. Such financial energy helps create an environment where localized industrial projects, including urea facilities, can expand more confidently.

Latest Trends

Shift toward high-purity DEF formulations

A notable trend in the Diesel Exhaust Fluid market is the shift toward higher-purity formulations that deliver more consistent performance in SCR systems, particularly for newer diesel engines used in logistics, construction, and agriculture. Higher purity ensures reduced risk of catalyst damage and better long-term fuel efficiency. This shift also aligns with a broader pattern of investment in cleaner, more reliable industrial supply chains.

A recent example is Venture Catalysts raising Rs 150 crore to scale its multi-stage VC platform, highlighting growing investor interest in industries that support operational efficiency and regulatory compliance. As cleaner fluid standards gain momentum, markets are moving toward advanced quality benchmarks that help engines meet stricter emission norms.

Regional Analysis

Asia Pacific holds 48.6% share, driving the Diesel Exhaust Fluid Market to USD 20.7 Bn.

The Diesel Exhaust Fluid market shows varied regional performance across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, with Asia Pacific emerging as the dominant region. Asia Pacific holds a 48.6% market share valued at USD 20.7 billion, supported by the region’s extensive commercial vehicle fleet and strong construction, mining, and industrial activity that drives consistent DEF consumption.

North America continues to maintain steady demand due to strict emission norms for heavy-duty trucks and widespread SCR system adoption. Europe remains a key market as well, benefiting from long-established environmental regulations and high compliance across transportation fleets.

The Middle East & Africa market grows gradually alongside expanding infrastructure and equipment needs, while Latin America shows stable uptake as emission standards strengthen across major economies. Together, these regions reflect an industry shaped by policy enforcement, rising diesel vehicle usage, and the ongoing shift toward cleaner engine operations.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, TotalEnergies is expected to maintain a strong position in the Diesel Exhaust Fluid landscape as the company continues expanding its downstream distribution capabilities across key transportation corridors. TotalEnergies’ integrated fuel and lubricant operations support consistent DEF availability for commercial fleets, especially in regions with rapid logistics growth. Its emphasis on energy transition strategies strengthens the company’s alignment with cleaner fuel technologies, which indirectly supports DEF adoption where diesel engines remain operationally essential. The company’s ability to leverage its wide service station network provides structural advantages in meeting the rising demand from heavy-duty vehicles requiring regular DEF replenishment.

Shell is expected to play a critical role in the DEF ecosystem through its global supply chain strength and strong commercial vehicle servicing footprint. Shell’s experience in diesel engine fluids and its established distribution infrastructure allow the company to respond efficiently to rising DEF requirements across developed and emerging markets. Its close engagement with fleet operators positions it to support compliance with emission standards while maintaining product quality and distribution consistency. Shell’s long-standing customer trust across fuel and lubricant categories also contributes to its resilience in the DEF segment.

For BASF SE, 2025 reinforces its importance as a core material producer supporting DEF-related technologies. BASF’s expertise in chemical formulations contributes to high-performance components that enable reliable emission control in diesel engines using SCR systems. As demand for consistent NOx reduction continues, BASF’s role in supplying essential materials for fluid stability and purity becomes increasingly relevant. Its strong industrial presence and relationships with automotive and heavy-equipment manufacturers allow the company to remain deeply embedded in the DEF value chain, supporting both performance advancements and global compliance requirements.

Top Key Players in the Market

- Total Energies

- Shell

- BASF SE

- Sinopec

- Cummins Filtration

- CF Industries Holdings, Inc.

- Dyno Nobel

- Agrium Inc.

- Honeywell International Inc.

- Faurecia SE

Recent Developments

- In July 2025, Shell completed the acquisition of Raj Petro Specialities Pvt. Ltd., strengthening its lubricants product portfolio and expanding its customer base in India. This move adds more industrial and automotive fluid products under Shell’s distribution channels, aiming to improve service support for commercial vehicles and diesel engine applications.

- In March 2025, TotalEnergies published its Sustainability & Climate 2025 Progress Report, outlining its continued efforts to strengthen emissions reduction targets and make progress toward lower greenhouse gas emissions. This development highlights the company’s broader emissions strategy, which supports cleaner operations in its energy and fuel supply businesses.

Report Scope

Report Features Description Market Value (2025) USD 42.7 Billion Forecast Revenue (2035) USD 91.3 Billion CAGR (2026-2035) 7.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Vehicle Type (Passenger Cars, LCVs, HCVs), By Component Type (Catalysts, Tanks, Injectors, Sensors, Others), By Application Type (Construction Equipment, Agricultural Tractors, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Total Energies, Shell, BASF SE, Sinopec, Cummins Filtration, CF Industries Holdings, Inc., Dyno Nobel, Agrium Inc., Honeywell International Inc., Faurecia SE Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Diesel Exhaust Fluid MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Diesel Exhaust Fluid MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Total Energies

- Shell

- BASF SE

- Sinopec

- Cummins Filtration

- CF Industries Holdings, Inc.

- Dyno Nobel

- Agrium Inc.

- Honeywell International Inc.

- Faurecia SE

Our Clients

- 179823

- March 2026